Barclays Warns of Prolonged Market Volatility Under New Fed Reality

19 hrs ago

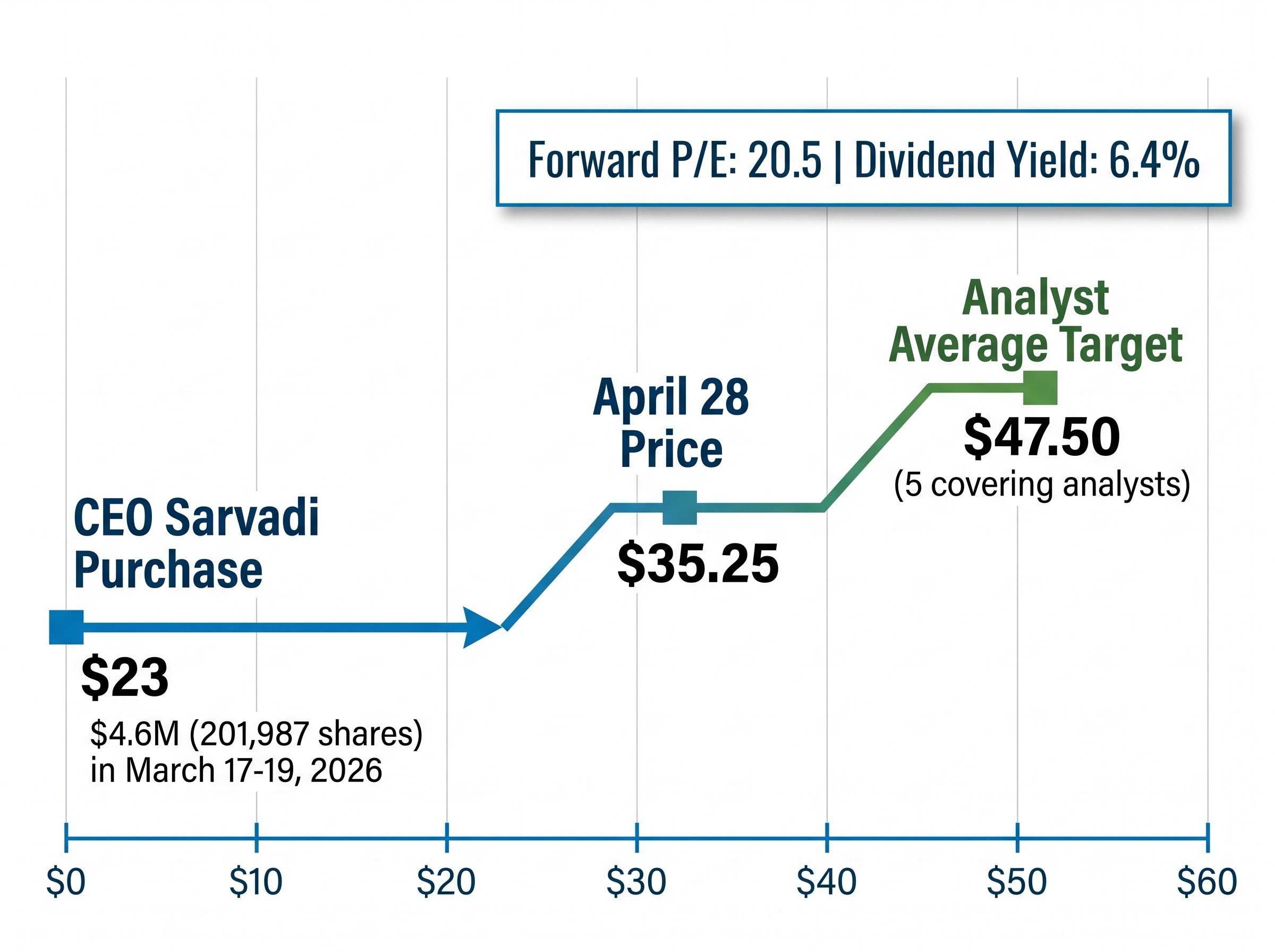

Between March 17 and March 19, 2026, Chief Executive Officer Paul Sarvadi committed approximately $4.6 million of his own capital to his company’s shares. This aggressive acquisition arrived just before a major product launch and an impending earnings period. The broader human resources sector sits at a precarious juncture on April 29, 2026, following a difficult late-year period where elevated benefit expenses and customer attrition battered domestic providers.

A broader Insperity stock analysis reveals that this decisive executive action arrives just as the company battles severe macroeconomic pressures and rising client attrition across its core markets.

For commercial evaluators and prospective investors, this sudden display of insider conviction requires careful parsing. Determining the long-term viability of Insperity stock depends on evaluating whether the provider’s newly integrated artificial intelligence platform and strict compliance focus can actually justify capital allocation. The upcoming earnings report tests these structural changes against immediate financial realities, providing a definitive framework to gauge if the underlying business model can support a sustained turnaround.

The executive capital deployment provides an immediate anchor for valuation modelling. Sarvadi purchased 201,987 shares at approximately $23 per share, signalling profound confidence in the underlying operational mechanics. By the close of trading on April 28, the price had recovered to $35.25, representing a significant rebound that still sits well below historical peaks.

The official SEC Form 4 filing documents this specific accumulation of equity, establishing a clear public record of executive capital deployment that institutional analysts often use to gauge internal sentiment during transitional periods.

This recovery trajectory is supported by compelling valuation metrics relative to the broader staffing sector. The forward price-to-earnings multiple currently is approximately 20.5, suggesting the market remains hesitant to price in a full operational turnaround. However, an accompanying 6.4% dividend yield provides a substantial defensive cushion for institutional portfolios willing to wait for the strategy to materialise.

Despite the internal optimism, mainstream Wall Street professionals maintain a distinctly cautious posture. Five covering analysts currently maintain consensus ratings leaning toward Hold or Reduce. Their average price target sits at $47.50, indicating persistent doubts about near-term margin expansion.

Analyst Sentiment on Turnaround Execution “While the insider purchasing activity establishes a definitive floor for the valuation, leadership must demonstrate that their technology integrations can translate into margin recovery before institutional capital fully rotates back into the name,” noted industry coverage teams.

Understanding this gap between executive conviction and analyst caution is necessary for commercial evaluators. The divergence highlights the inherent risks of a turnaround play where historical competence must overcome immediate macroeconomic headwinds. Investors must weigh the Chief Executive Officer’s deep visibility into the pipeline against the strict empirical standards of the financial community.

The professional employer organisation model thrives on regulatory friction. These entities operate by co-employing a client’s workforce, legally assuming the burden of payroll processing, benefits administration, and risk management. As federal and state-level regulatory burdens escalate, small and mid-sized businesses are increasingly forced to outsource these human resources functions to avoid costly penalties.

This compliance complexity serves as the primary defensive moat protecting industry market share. According to first-quarter 2026 survey data, 42% of small and mid-sized businesses cite navigating regulations as their primary reason for adopting this co-employment structure. The underlying demand engine is structurally supported by a constant stream of new administrative requirements.

The recent IRS guidelines on Form 1099-K reporting exemplify this growing burden, as lower monetary thresholds for third-party settlements force business owners to implement more sophisticated tracking systems.

Current compliance frameworks shaping this adoption curve include several specific operational hurdles:

The Department of Labor maintaining its 2026 overtime rule, which enforces a strict $35,568 annual salary threshold for exempt employees. The Internal Revenue Service enforcing the Form 1099-K reporting threshold at $20,000 and 200 transactions, complicating contractor management. * State-level developments like California Senate Bill 642, which mandated comprehensive new pay transparency updates effective January 1, 2026.

By breaking down these mechanics, the resilience of the business model becomes evident to commercial evaluators. The overwhelming administrative strain on smaller enterprises translates directly into sticky, recurring revenue for established providers equipped to handle the legal labyrinth. For a business with limited administrative headcount, transferring this liability is often more cost-effective than building internal compliance departments.

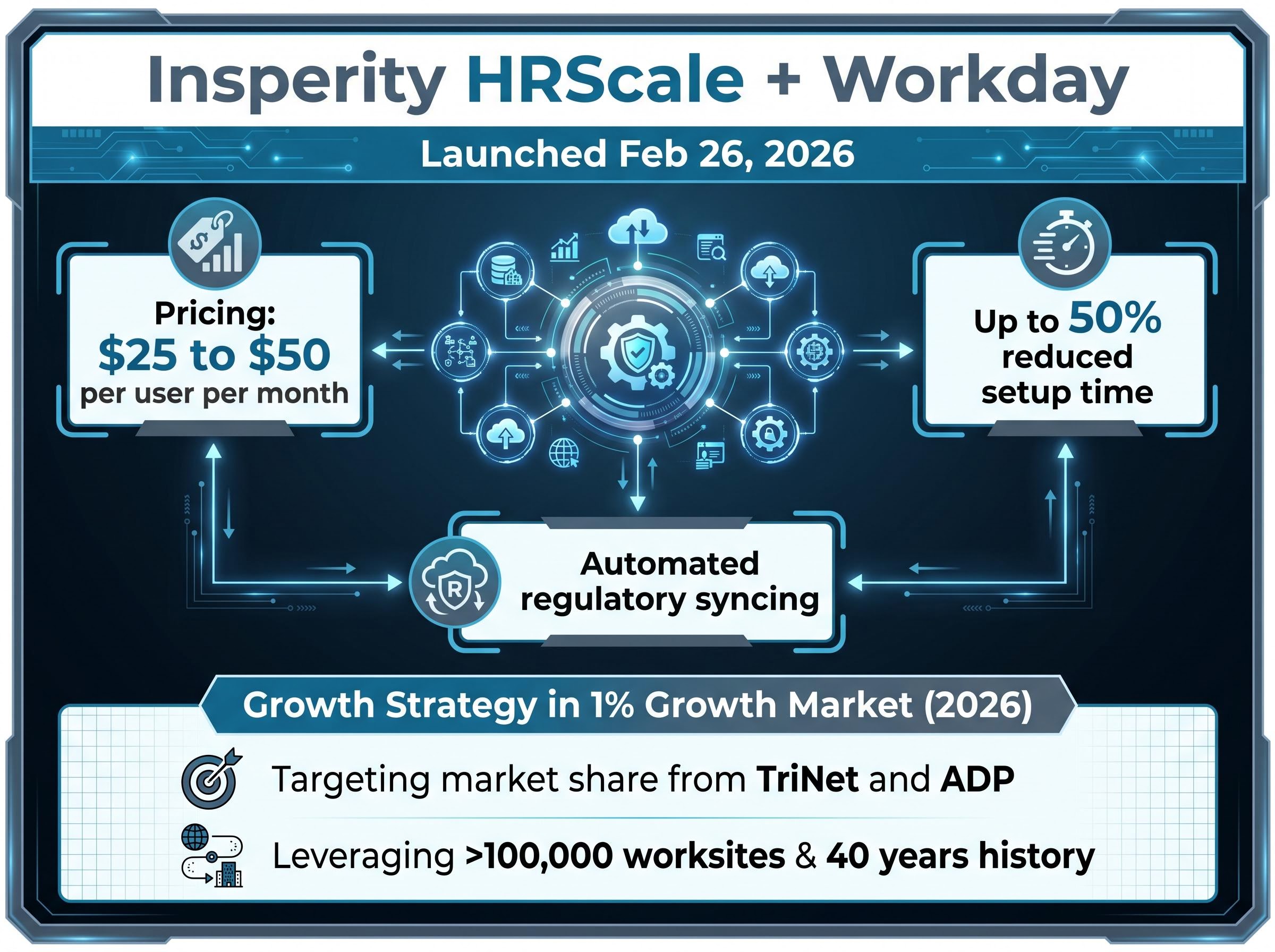

The traditional service model is actively transitioning into a tech-enabled growth thesis. On February 26, 2026, leadership announced the general availability of Insperity HRScale, a strategic partnership integrating their legacy services with Workday and its artificial intelligence ecosystem. This bundled offering directly targets the small to mid-sized market with a software-as-a-service model priced between $25 and $50 per user per month.

The human resources sector is increasingly shifting toward these interconnected ecosystems; similar Xref platform integrations have successfully combined applicant tracking interfaces with core enterprise software to drive scalable, high-margin revenue.

According to Staffing Industry Analysts, the overall staffing market is forecast to grow by just 1% in 2026. In a stagnant macroeconomic environment, organic industry expansion is insufficient, demanding aggressive market share theft from standalone competitors like TriNet and ADP.

This integrated platform is designed to execute that theft through three specific commercial advantages:

This initiative leverages a massive existing footprint of more than 100,000 worksites and 40 years of operational history. Readers can observe exactly how leadership is attempting to solve the margin compression issues of the past year by scaling their technology infrastructure without proportionally increasing internal headcount.

Adding a human-in-the-loop professional service to a top-tier software ecosystem creates exceptionally high switching costs. Pure software-as-a-service tools provide administrative dashboards, but they do not absorb the legal liability of co-employment.

By marrying enterprise-grade technology with fiduciary responsibility, the bundle establishes a formidable defensive barrier against pure software rivals. Industry data suggests clients may be far less likely to churn when abandoning the platform means simultaneously losing their technological infrastructure and their legal compliance shield. This hybrid approach allows the company to command premium pricing while simultaneously insulating its client base from aggressive discounting by lightweight software startups.

The forward-looking optimism surrounding the technology pivot must eventually reconcile with hard financial deliverables. The upcoming April 30 earnings release presents an immediate hurdle following a weak fourth quarter in 2025, where elevated benefit expenses severely damaged profitability.

Wall Street analysts have recalibrated their models for the first quarter of 2026, projecting a sharp sequential recovery. Earnings per share are projected to land between $1.03 and $1.50, setting the foundation for full-year 2026 guidance ranging from $1.69 to $2.72.

This aggressive projection highlights the tension between necessary strategic investments and the urgent need to improve trailing metrics. The company currently operates with a trailing twelve-month revenue of $6.81 billion.

| Financial Metric | Q4 2025 Actual | Q1 2026 Consensus Range |

|---|---|---|

| Earnings Per Share (EPS) | N/A | $1.03 to $1.50 |

| Revenue Profile | N/A | N/A |

This data equips commercial evaluators with the exact parameters to watch during the impending earnings call. Proving the turnaround requires more than just revenue growth; leadership must demonstrate that their new pricing structures are actively repairing the damaged gross profit margins. If the technology partnership fails to deliver these anticipated margin improvements, the aggressive top-line expansion offers little comfort to institutional shareholders.

For commercial evaluators wanting to model the exact financial hurdles facing leadership this quarter, our dedicated guide to Insperity earnings expectations breaks down the specific healthcare cost headwinds and client attrition metrics that Wall Street is heavily scrutinising.

The investment case ultimately rests on weighing undeniable insider confidence against the execution risks of a massive technology integration. The CEO’s multi-million dollar capital deployment signals a firm belief that the worst of the margin compression has passed. However, capturing market share in a stagnant staffing environment using a newly launched software bundle requires flawless commercial execution.

Historically, management has demonstrated proven operational competence, evidenced by a 52.48% five-year historical return prior to the recent drawdown. If the upcoming earnings report confirms that the new platform is successfully repairing profit margins, the current valuation may present a compelling entry point for risk-tolerant capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Insperity's CEO, Paul Sarvadi, purchased approximately $4.6 million in company shares, signaling profound confidence in the underlying operational mechanics and a potential bottom for the stock's valuation. This aggressive acquisition occurred just before a major product launch and an impending earnings period.

Investors should watch for earnings per share projections, which are between $1.03 and $1.50 for Q1 2026, and evidence that new pricing structures are repairing damaged gross profit margins. The report will clarify if the new technology platform is delivering anticipated margin improvements.

Insperity's HRScale platform, a partnership with Workday, offers a tech-enabled growth strategy targeting small to mid-sized businesses with a software-as-a-service model. It combines premium software with HR consulting, aiming to reduce client setup time and automate regulatory syncing to gain market share.

Compliance complexity serves as a primary defensive moat for PEOs, as escalating federal and state regulatory burdens compel small and mid-sized businesses to outsource HR functions. This translates into sticky, recurring revenue for providers like Insperity that handle legal and administrative tasks.