According to reports, Lululemon has evaporated an estimated $17 billion in market capitalisation over the past five years. This sustained exercise in wealth destruction has transformed one of the retail sector’s greatest growth stories into a cautionary tale of strategic drift. This financial attrition forms the backdrop for the Lululemon proxy battle now unfolding in late April 2026. Founder Chip Wilson has launched an aggressive campaign to overhaul the board of directors ahead of the upcoming 2026 annual meeting. He points to stagnant sales, a plummeting stock price, and brand dilution as evidence of deep structural failure at the executive level. What follows is a comprehensive breakdown of the financial triggers, governance controversies, and strategic missteps driving this corporate rebellion. This analysis will evaluate the alternative candidates vying for control and examine the complex proxy mechanics at play. Investors face a critical decision point that will ultimately determine whether the company reclaims its premium positioning or continues its downward trajectory.

The Financial Attrition Driving the Rebellion

The proxy fight represents a rational response to severe capital erosion rather than a founder’s ego trip. The recent plunge in Lululemon’s equity valuation places its current market position under intense scrutiny as of 29 April 2026. The stock price currently stands at $139.92, giving the apparel manufacturer a market capitalisation of $16.414 billion.

According to reports, this valuation reflects a catastrophic 65.9% drop in total equity value over a 24-month period. The deterioration aligns directly with sustained stagnation in the core Americas market. This primary geographic segment has now struggled through eight consecutive quarters of underperformance. Americas revenue dropped 4% in the fourth quarter of fiscal 2025, a glaring signal of consumer fatigue in the brand’s most important demographic.

This specific demographic retreat aligns with broader mass-market decay observed across the retail sector, as the rapid depletion of household financial buffers forces shoppers to abandon premium discretionary purchases.

Investors face a fundamental quantitative reality that validates the activist campaign. Lululemon’s recent investor returns highlight significant underperformance when measured against broader apparel industry benchmarks. According to reports, the stock is currently trailing the industry midpoint by 19.5% over a 12-month horizon.

According to reports, the gap widens substantially over a longer timeframe, with returns trailing the industry midpoint by 63.6% over 36 months. These value destruction metrics transform abstract governance complaints into tangible financial reality. Shareholders must now weigh these quantitative failures against management’s promises of an impending turnaround.

| Timeframe | Metric | Lululemon Performance | Industry Comparison |

|---|---|---|---|

| Q4 Fiscal 2025 | Americas Revenue | -4.0% | N/A |

| 12 Months | Investor Returns | Trailing | -19.5% vs Midpoint |

| 24 Months | Equity Value | -65.9% | N/A |

| 36 Months | Investor Returns | Trailing | -63.6% vs Midpoint |

When big ASX news breaks, our subscribers know first

How Outdated Governance Structures Shield Incumbent Boards

A classified board structure operates by staggering director elections so only a fraction of the board faces a shareholder vote each year. Corporate governance advocates typically oppose this system because it insulates incumbent directors from immediate accountability and delays comprehensive strategic shifts. According to reports, currently, only 10% of S&P 500 corporations still utilise a classified directorial election system.

Management teams deploy multiple defensive manoeuvres to protect these outdated structures during contested elections. Lululemon management recently filed a preliminary statement outlining their intent to distribute a WHITE proxy card ahead of the 2026 meeting. This card is the traditional mechanism used by incumbents to solicit shareholder votes against challenger slates and maintain the status quo.

This defensive posture operates alongside the new universal proxy ballot rules. The universal proxy ballot is a regulatory mechanism allowing shareholders to mix and match individual candidates from both the management and dissident slates on a single card. This framework makes director-by-director evaluation mandatory for retail and institutional investors alike.

The SEC universal proxy rules mandate that both management and dissident nominees appear on identical formatted cards, fundamentally altering how institutional investors evaluate contested boardroom seats.

The structural roadblocks at Lululemon extend beyond staggered elections to encompass heavy private equity affiliations. Four current Lululemon directors share professional affiliations with Advent International L.P., raising fundamental questions about true board independence. This concentration of private equity influence complicates the corporate oversight mechanisms that everyday investors rely upon.

The friction between the founder and these incumbents recently escalated during failed settlement negotiations.

“According to reports, the board demanded a $1 million escrow payment to secure a non-disparagement agreement, revealing a deep entrenchment that prioritises reputation over shareholder dialogue.”

This educational breakdown clarifies complex proxy mechanics. It helps everyday investors understand exactly how incumbent directors insulate themselves from shareholder voting pressure while demanding unprecedented financial concessions.

Brand Dilution and the Contested Leadership Transition

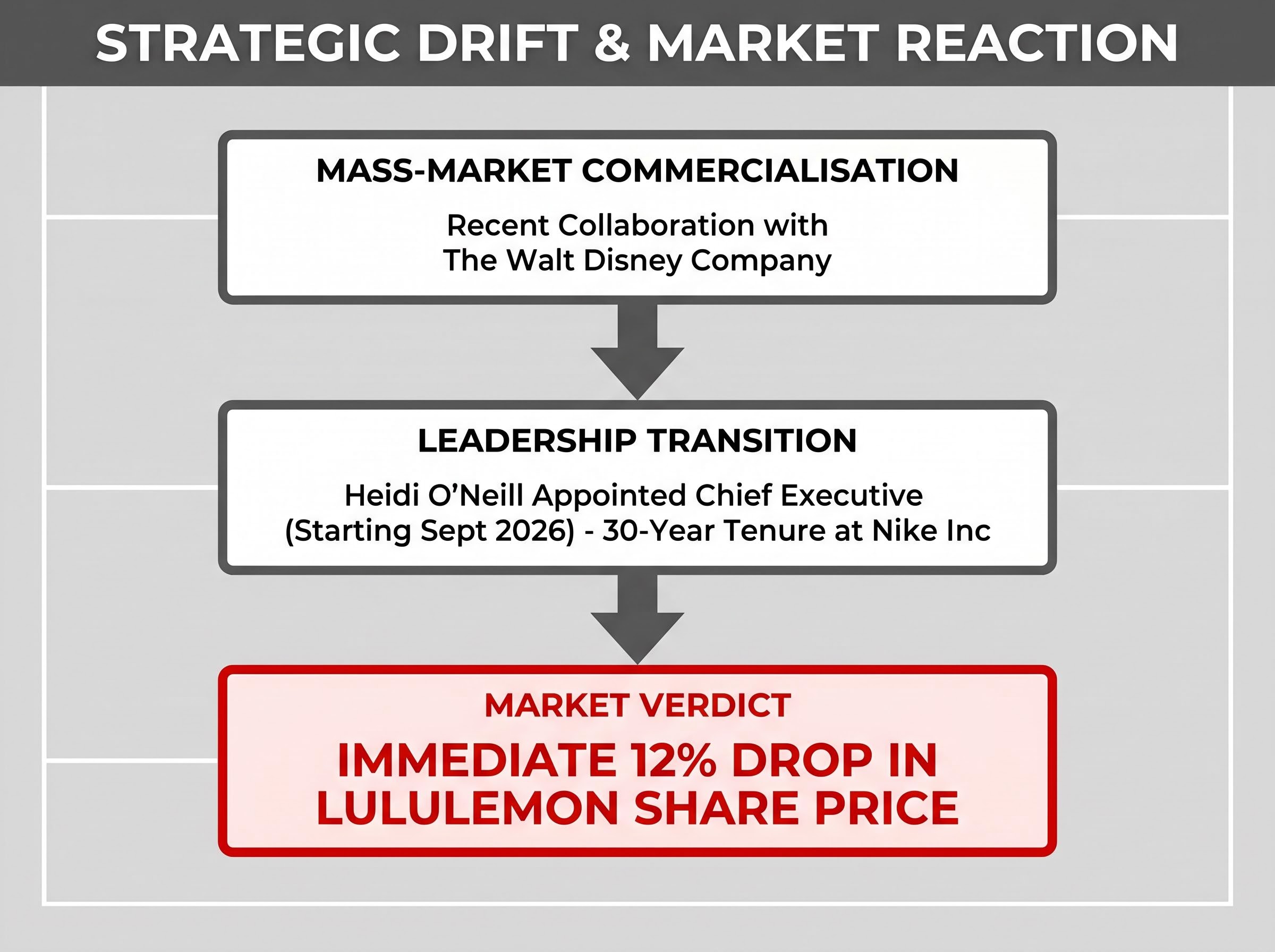

The board’s strategic partnerships and executive recruitment choices have drawn heavy criticism for diluting Lululemon’s premium athletic heritage. The recent collaboration with The Walt Disney Company serves as the clearest example of this strategic drift.

Market experts view the Disney partnership as a distinct pivot away from the brand’s historically exclusive, high-end demographic toward mass-market commercialisation. These boardroom decisions eventually manifest on store shelves and directly alter consumer brand perception. Investors are now witnessing the friction between the company’s elite fitness roots and its recent attempts to capture broader, less specialised demographics.

This tension reached a breaking point with the latest chief executive appointment. Critics frame this leadership transition as concrete evidence of the board’s inability to recruit visionary product leaders who understand the original brand ethos.

The Market Verdict on Leadership Changes

Wall Street delivered an immediate and severe reaction to the announcement that Heidi O’Neill will take the helm. According to reports, her upcoming September 2026 start date follows a three-decade tenure at Nike Inc, a background that fundamentally altered the investment thesis. Investors fear this specific operational background will accelerate the brand’s shift toward volume-based retail rather than premium scarcity.

Lululemon’s share price suffered an immediate 12% drop following the appointment announcement. This double-digit stock sell-off highlights a profound disconnect between the board’s confidence in their selection and the market’s assessment of her strategic fit. The negative reaction signals that institutional investors share the activist concerns regarding leadership direction.

Evaluating the Alternative Slate and the Road to the Annual Meeting

The activist campaign shifts from strategic critique to tangible solutions by offering an alternative slate of independent directors. Each proposed candidate fills a specific strategic void left by the current board. They provide successful track records in brand turnaround, media positioning, and international growth.

This challenger slate gives investors a clear comparative framework to evaluate the nominees against the incumbents. The three independent directors nominated by Wilson bring specific corporate achievements designed to correct Lululemon’s current trajectory:

Marc Maurer: Reportedly delivered nearly fourfold income growth during his tenure as co-chief executive at On Holding AG, demonstrating the international scaling capabilities Lululemon currently lacks. Laura Gentile: Drove top consumer confidence ratings during her extensive leadership run at ESPN Inc, bringing vital expertise in media and premium brand positioning. * Eric Hirshberg: Reportedly oversaw a 500% equity valuation surge during an eight-year tenure at Activision Publishing Inc, proving his capacity to manage highly engaged consumer communities.

Despite these credentials, the nominees face a significant structural hurdle on the road to the annual meeting. The challenger slate currently operates without the explicit backing of major institutional proxy advisors. These advisory groups essentially dictate the voting patterns of massive passive index funds.

As of late April 2026, there is a notable absence of public support from key advisory firms like ISS or Glass Lewis. Securing endorsements from these institutional gatekeepers remains the necessary strategic path forward for the activist campaign. Without their backing, convincing entities like Vanguard or BlackRock to vote against incumbent directors becomes a mathematical improbability.

For investors wanting to track how these governance battles will play out on the actual ballot, our detailed coverage of the proxy campaign outlines the June 2026 meeting timeline and the specific voting mechanisms required to bypass entrenched directors.

A Defining Referendum on Lululemon’s Premium Heritage

The upcoming 2026 shareholder meeting represents a decisive pivot point for the company’s financial trajectory rather than a simple leadership contest. The core conflict pits the incumbent board’s volume-driven operational approach against the founder’s vision for restoring premium brand value. Lululemon must reconcile its exclusive heritage with its current market realities to arrest the ongoing equity erosion.

While an aggressive expansion strategy often commands high market valuations during early growth phases, sustaining those multiples long-term requires the pricing power that only a fiercely protected premium heritage can provide.

The activist campaign still needs to clear significant structural hurdles to achieve this operational reset. Overhauling a classified board heavily influenced by private equity remains exceptionally difficult without backing from major proxy advisory firms. Investors must now decide whether the proposed alternative slate offers a credible path back to premium valuation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.