Barclays Warns of Prolonged Market Volatility Under New Fed Reality

19 hrs ago

The collapse of Insperity from a 52-week high to a recent bottom captures the severity of the macroeconomic pressures facing human resources outsourcing firms. Against this backdrop, Chief Executive Officer Paul Sarvadi executed a massive mid-March stock purchase, creating a bold contrarian signal for the equity market. The company is currently navigating a highly complex period defined by elevated employee benefit expenses and rising customer attrition.

This structural pressure makes tomorrow’s 30 April 2026 earnings report a critical juncture for investors seeking clarity on the corporate trajectory. Any comprehensive Insperity stock analysis must evaluate whether new technology partnerships and heavy executive buying justify a long-term position. The gap between the severity of the industry shock and the sheer scale of insider accumulation reveals how management expects to weather the immediate storm.

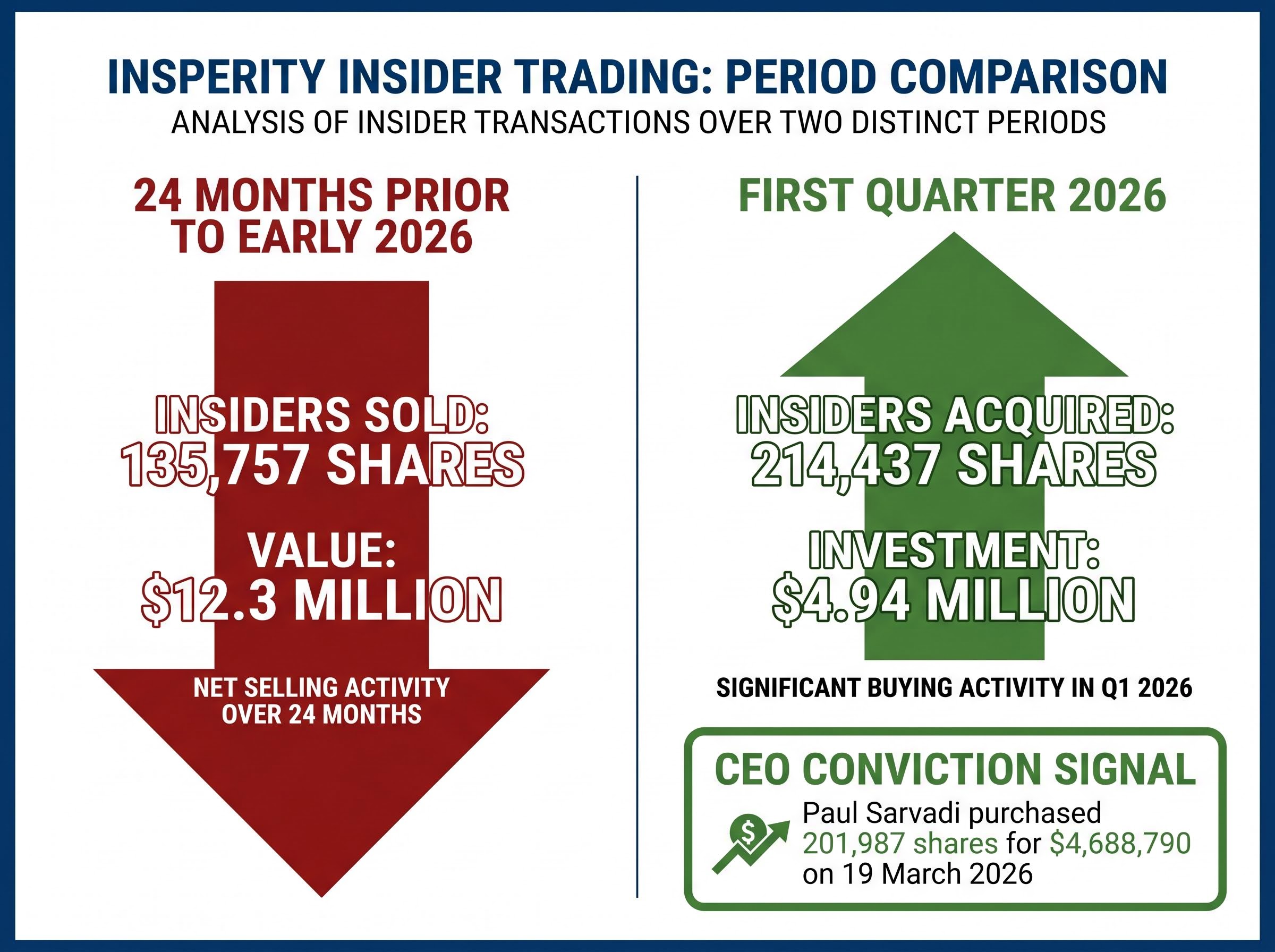

Executive capital allocation often provides the clearest leading indicator of internal confidence preceding major strategic shifts. The sheer volume of recent insider buying at Insperity sharply contrasts with the selling patterns observed over the previous two years. Over the 24 months prior to early 2026, insiders sold 135,757 shares worth approximately $12.3 million.

This pattern reversed aggressively in the first quarter of 2026. Total insider acquisitions reached 214,437 shares, representing a combined investment of $4.94 million. The bulk of this accumulation came directly from the chief executive, as Sarvadi purchased 201,987 shares for $4,688,790 on 19 March 2026.

Mandatory SEC Form 4 beneficial ownership filings make these massive executive capital deployments a matter of public record, allowing investors to track the precise scale of internal management conviction.

Executive Conviction Signal A chief executive officer committing more than $4.5 million in personal capital in a single transaction is a statistical rarity during a pronounced sector downturn.

Investors require tangible metrics to distinguish token executive support from genuine financial conviction. This multi-million dollar pivot from systematic selling to aggressive buying suggests management expects impending operational initiatives to materialise into shareholder value. The magnitude of this capital rotation offers a compelling counter-narrative to the prevailing industry pessimism.

| Executive Name | Date | Shares Acquired | Total Investment |

|---|---|---|---|

| Paul Sarvadi (CEO) | 19 March 2026 | 201,987 | $4,688,790 |

| James Allison | 10 March 2026 | 10,000 | $204,500 |

| Christian Callens | 11 March 2026 | 1,250 | $24,100 |

| Ellen Masterson | 11 March 2026 | 1,200 | $23,880 |

The optimism of executive stock purchases must be weighed against the harsh macroeconomic realities governing Professional Employer Organisations (PEOs). A PEO operates by co-employing client staff, assuming legal responsibilities for payroll, benefits, and human resources compliance. This core operational model makes the sector highly sensitive to United States healthcare legislation changes and broader employment market shifts.

Specific profitability pressures emerged rapidly throughout late 2025 and early 2026. The industry faces three distinct macroeconomic headwinds:

Elevated benefit expenses driven by healthcare cost inflation. Heightened compliance burdens originating from new federal regulatory requirements. * Rising client attrition, with industry-wide Medicaid churn reaching approximately 20% and Affordable Care Act related churn hitting 26%.

These pressures have materially impacted sector margins across the board. Competitor ADP reported a PEO margin decline of 70 basis points in the second quarter of 2026, heavily driven by pass-through costs. For investors to properly evaluate new corporate strategies, they must understand that these structural weaknesses require technological solutions rather than simple cost-cutting.

The operational difficulties of the previous year culminated in a severe financial miss during the final reporting period. Customer attrition heavily weighed on results in the final months of 2025, stripping away essential pricing power.

This dynamic produced a fourth-quarter earnings per share deficit of -$0.60, which missed Wall Street projections by 27.66%. Analysts noted that reversing this trend remains the company’s most urgent priority heading into the new fiscal year.

While company-specific attrition drove this miss, severe earnings deficits during periods of peak index valuations often act as a reliable stock market warning signal for broader corporate vulnerabilities.

Management has pivoted toward an enterprise technology integration to address the structural weaknesses exposed in late 2025. Insperity announced a strategic partnership with Workday in February 2026, launching a new solution designated as “HRScale”. This deployment targets the small-to-medium business sector with enterprise-grade human capital management technology.

The joint Insperity and Workday announcement positions this software rollout as a strategic move to stabilise client retention, equipping smaller accounts with advanced tools previously reserved for large corporations.

Securing access to premium technology creates a potential competitive moat in a sector struggling with retention. The company maintains a historical 12-month gross profit rate, a metric the new partnership explicitly aims to improve. With industry-wide expansion constrained to low single-digit percentages, capturing market share through superior software capabilities remains absolutely essential.

Industry analysts view this integration as a primary vehicle for margin recovery. The successful rollout of HRScale relies on a sequential operational progression to translate into bottom-line profitability:

Unpacking these mechanics allows investors to see the specific vehicle driving top-line growth expectations.

Strategic partnerships take time to mature, but the market demands immediate financial accountability. The temporal relevance of the first-quarter earnings release scheduled for 30 April 2026 after the market close cannot be overstated. The published figures will provide the first concrete evidence of operational stabilisation.

Market professionals anticipate significant sequential improvements following the weak preceding period. Company guidance for the first quarter places expected earnings per share between $1.03 and $1.50. However, analysts project initial quarter profit to be aligned with company guidance ($1.03-$1.50) per share alongside approximately $1.8 billion in total sales.

These forecasted top-line figures represent an increase from the prior period. Providing exact consensus metrics gives investors a clear scorecard for tomorrow’s announcement, transforming abstract recovery theories into measurable targets.

The immediate quarter serves as a building block for the broader fiscal year expectations. The company provided a full-year 2026 earnings per share guidance range of $1.69 to $2.72. Achieving the upper bound of this guidance would reflect an anticipated annual expansion for profits.

Evaluating if the current earnings multiple accurately prices in the turnaround potential requires synthesising both risk and reward. As of late April 2026, the stock trades at $35.25, a level that suggests investors are already pricing in some measure of financial rebound. The forward price-to-earnings ratio stands at 15.67, reflecting cautious optimism from institutional buyers.

This cautious institutional stance mirrors broader concerns regarding underpriced stock market risk, as escalating geopolitical tensions and embedded inflation threaten to compress corporate margins across multiple sectors.

Market experts remain divided on whether this entry point offers a sufficient margin of safety given the known industry risks. The average analyst price target sits at $40.50, while the most optimistic projections extend to $47.67.

Current analyst coverage reflects the tension between the insider buying signal and the macroeconomic reality:

Neutral stances hinge on waiting for concrete evidence of margin stabilisation. A positive recommendation focuses on the Workday integration and the resulting competitive advantage. * A negative rating prioritises the immediate threat of healthcare cost inflation and elevated client churn.

This valuation analysis directly addresses commercial investment intent by outlining the exact battle lines drawn by institutional observers. The divided stance among market professionals highlights exactly why tomorrow’s earnings data will serve as a definitive catalyst for the share price.

The core tension defining the current investment case lies between massive executive financial confidence and highly challenging macroeconomic realities. Paul Sarvadi’s multi-million dollar capital deployment signals immense internal conviction, yet the structural headwinds of healthcare inflation and client attrition remain severe. The Workday partnership serves as the primary bridge connecting the current valuation to future growth.

Investors monitoring the imminent earnings call must focus entirely on client retention metrics and gross profit margins. If the initial deployment of HRScale shows traction in arresting attrition, the fundamental turnaround thesis gains significant credibility.

For investors evaluating how operational revamps drive financial recovery, our detailed coverage of strategic turnaround initiatives examines how other major brands deploy digital engagement and efficiency programs to restore long-term profitability.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and operational execution.

CEO Paul Sarvadi made a nearly $4.7 million personal stock purchase in March 2026, which is viewed as a strong contrarian signal of internal confidence given the company's recent challenges and the sector downturn.

Insperity and other Professional Employer Organizations are currently facing elevated employee benefit expenses, heightened regulatory compliance burdens, and rising client attrition rates.

HRScale is a new solution launched in February 2026 through a partnership with Workday, designed to provide small-to-medium businesses with enterprise-grade human capital management technology and improve client retention.

Insperity is scheduled to report its Q1 2026 earnings on April 30, 2026, after market close, with company guidance projecting EPS between $1.03 and $1.50 and analysts expecting around $1.8 billion in sales.