Goldman Sachs Cuts 2026 Smartphone Shipment Forecast 10% on AI Crunch

11 hrs ago

The Morningstar LSTA US Leveraged Loan Index valuation retreated by late March 2026, signalling a quiet but significant fracturing within domestic debt markets. This valuation gap reveals how broader credit market trends are masking severe, localised deterioration beneath the surface. Following a volatile first quarter, domestic lenders are grappling with tightening credit conditions, surging distress ratios, and highly selective capital access.

The gap between the shock’s severity and the market’s response reveals how institutional investors are pricing this current macroeconomic cycle. Capital is aggressively separating premium debt vehicles from legacy liabilities, leaving highly leveraged software and services firms exposed to refinancing risks. Readers tracking this divergence will observe the localised impacts of rising default rates across vulnerable sectors.

The data points to a distinct defensive strategy taking shape among the largest debt providers. Institutional capital is fundamentally reallocating risk toward emerging technology and artificial intelligence ventures to survive a divided economic environment.

The scale of the first-quarter deterioration becomes evident when comparing default rate metrics from major rating agencies. According to industry data, the Proskauer Private Credit Default Index reached a default rate of 2.73% for Q1 2026. Looking further ahead, Fitch Ratings projects a default rate of 4.5% to 5.0% for leveraged loans across the full year.

The Q1 2026 release of the Proskauer Private Credit Default Index highlights how rapidly borrowing costs are squeezing mid-market enterprises, forcing debt managers to reassess their exposure to vulnerable sectors.

These figures point to a steady erosion in borrower fundamentals, with commercial distress serving as a leading indicator of future insolvencies. S&P Global reported a US commercial mortgage-backed securities (CMBS) 30-plus day delinquency rate of 6.2% for the first quarter. The broader market distress ratio provides an even sharper signal, swelling by late March 2026 from the close of December 2025.

| Reporting Agency | Metric Focus | Q1 2026 Reading / 2026 Forecast |

|---|---|---|

| Proskauer | Private Credit Default Index | 2.73% (Q1 2026 Actual) |

| S&P Global | US CMBS 30-Plus Day Delinquency | 6.2% (Q1 2026 Actual) |

| Fitch Ratings | Leveraged Loan Defaults | 4.5% to 5.0% (2026 Forecast) |

Overall macroeconomic uncertainty and sticky inflation are effectively locking out high-risk borrowers from securing necessary refinancing. The tightening credit conditions operate not as a universal freeze, but as a severe penalty for lower-rated companies facing persistent rate headwinds. The pricing compression variations illustrate this divide clearly for institutional investors.

During the first quarter, BB obligations dropped, indicating that premium credits continue to find support. In stark contrast, CCC obligations plunged, demonstrating how aggressively lenders are demanding premiums to hold vulnerable debt. This severe pricing penalty reflects a broader lack of investor demand in riskier segments, placing continued pressure on software sector companies and other heavily leveraged borrowers.

The current market bifurcation hinges on the mechanics of the distress ratio, a critical metric for institutional lenders evaluating portfolio health. The distress ratio tracks the percentage of obligations trading under 80% of par value, acting as an early warning signal for credit funds. When this ratio climbs, it indicates that secondary market buyers are demanding significant discounts to absorb the risk of potential insolvencies.

Capital flight accelerates during sustained inflationary periods because lenders become highly selective about where they deploy fresh cash. Three main drivers are enforcing this strict market bifurcation:

Sticky inflation forcing rates to remain elevated, increasing the cost of debt service for highly leveraged entities. Legacy software disruption, as traditional business models face obsolescence risks from emerging machine learning technologies. * Highly selective capital access, where debt funds reserve their limited liquidity exclusively for top-tier borrowers.

The rapid decay in the legacy software market has already caused massive wealth destruction among platforms dependent on traditional per-user licensing models.

It is also important to clarify the difference between standard default metrics and broader liability management exercises. A standard default typically involves missed payments or bankruptcy filings. However, broad default measurements, which include distressed debt exchanges and liability management exercises designed to prevent formal insolvency, remained elevated in Q1 2026.

These mechanics directly impacted primary debt origination, which rose in the first quarter. This highlights that lenders have largely overlooked broader macro rate volatility to deploy capital into the market. Furthermore, the market absorbed unverified but widely discussed reports of localised capital withdrawals from domestic credit funds, adding to the defensive posture of surviving managers.

The broader market deterioration carries a direct cost for institutional portfolios, translating abstract macroeconomic headwinds into tangible per-share losses. Specific fund disclosures from early 2026 reveal exactly how these pressures compress quarterly earnings. Several domestic funds reported first-quarter earnings shortfalls where core investment revenue dropped sequentially.

This revenue contraction stems directly from the deteriorating health of the underlying borrowers, forcing managers to write down their holdings. Financial disclosures detail specific instances of underlying asset valuations contracting. Consequently, the aggregate realised and unrealised portfolio deficits expanded sequentially, leaving managers to defend their capital bases.

Behind these corporate borrower struggles lies a broader depletion of household financial buffers, creating an environment where end-consumer demand can no longer sustain heavily indebted retail and service businesses.

Despite these short-term earnings shortfalls, management teams are attempting to maintain long-term permanent capital structures. Rather than liquidating distressed positions at unfavourable prices, they are extending their investment horizons to outlast the current cycle of tightening conditions.

Executive Commentary “Our primary objective remains the preservation of capital through prolonged holding periods, prioritising structural stability over immediate trading realisations in a fractured market.”

To secure fresh capital amid reduced investment revenues, many funds are maintaining an ongoing reliance on at-the-market equity issuances. This mechanism allows them to slowly dilute existing shares to generate immediate liquidity on the open market. Doing so provides a necessary cash buffer against rising default correlations in their legacy portfolios, ensuring they can meet operational requirements without forced asset sales.

While legacy debt portfolios manage their decay, institutional lenders are actively offsetting these risks by funding machine learning and automation ventures. Credit funds are utilising artificial intelligence debt vehicles as a strategic escape route from the mounting defaults in traditional corporate lending. This transition represents a shift from defensive anxiety to offensive positioning, moving capital into sectors showing genuine momentum.

The institutional lending scale now entering the artificial intelligence space moves well beyond traditional equity venture capital. Lenders are increasingly factoring in disruption risks to legacy software models, making new technology allocations far more appealing than refinancing outdated enterprise systems. The sheer volume of capital entering this space validates this pivot, headlined by the $5 billion xAI loan secured from Morgan Stanley in July 2025.

Debt providers are targeting highly specific technological sectors to deploy their surplus capital safely:

Machine learning platforms requiring intensive compute infrastructure financing. Enterprise automation software demonstrating immediate operational cost reductions. * Generative infrastructure developers backed by massive, predictable recurring revenue contracts.

Late-stage venture debt deals hit a decade high in Q1 2026, driven almost entirely by artificial intelligence startups turning to lenders over equity financing. These founders are choosing debt to avoid massive equity dilution during their highest growth phases, preferring to pay interest rather than surrender ownership.

The median deal size for these artificial intelligence venture debt packages reached $10.8 million in the first quarter. This sizing indicates immense lender confidence in these business models, proving that capital is readily available for sectors capable of demonstrating structural immunity to sticky inflation. Lenders view these sizable debt packages as a calculated method to capture technology growth yields while maintaining senior positions in the capital structure.

For investors exploring the broader implications of these massive capital deployments, our detailed coverage of AI infrastructure risks examines whether the current surge in hardware spending will generate the expected returns for technology providers.

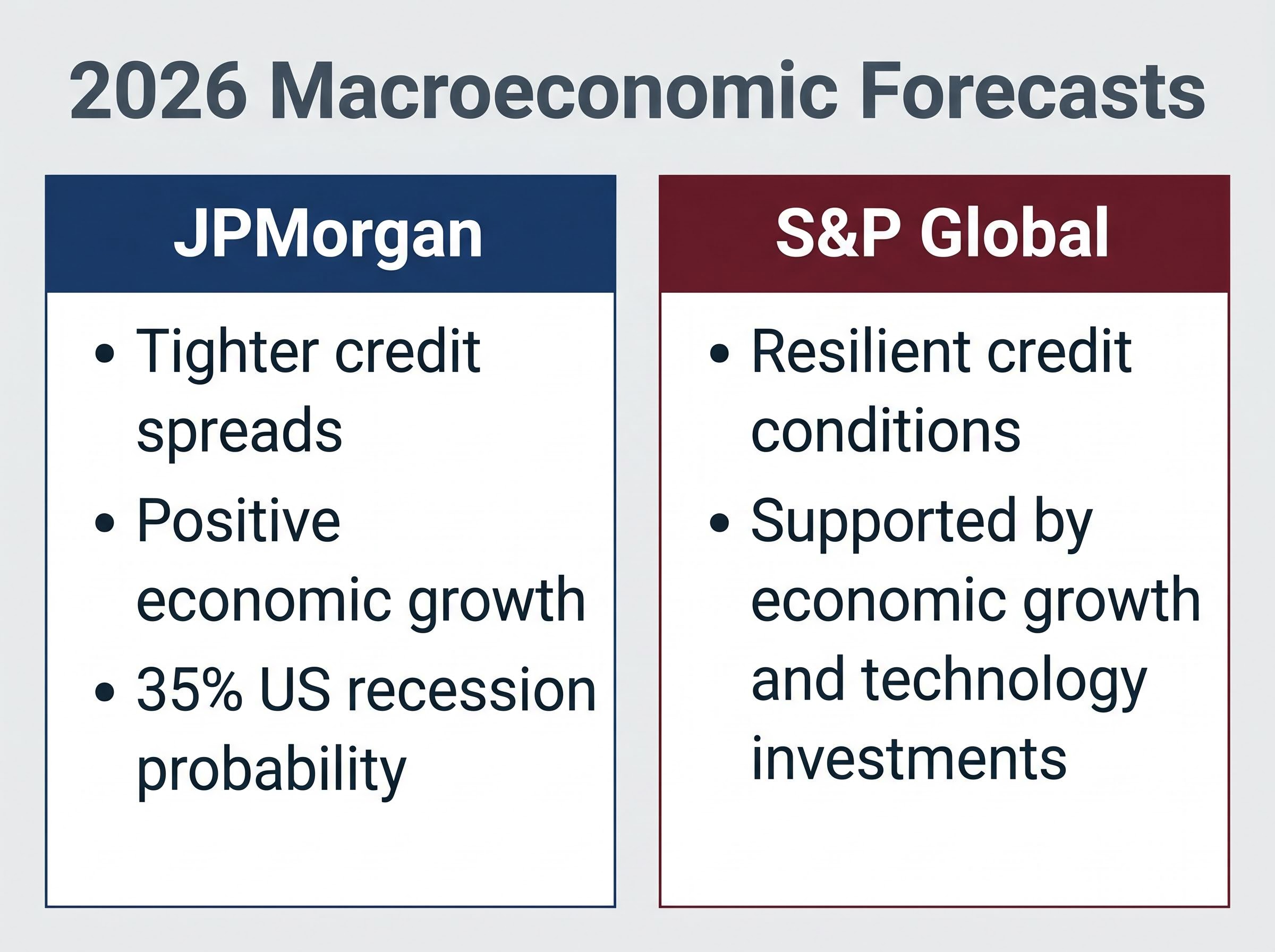

Synthesising the diverging macroeconomic forecasts from leading institutions provides a clear roadmap for the rest of 2026. JPMorgan is currently forecasting tighter credit spreads and positive economic growth, though they pair this optimism with a 35% US recession probability. Meanwhile, S&P Global anticipates that resilient credit conditions will be supported almost entirely by continued economic growth and significant technology investments.

The official JPMorgan macroeconomic outlook suggests that while baseline economic expansion continues, portfolio managers must remain prepared for sudden downside shocks.

These projections reinforce the concept that the lending environment will remain heavily divided. Resilient global credit conditions will be sustained by a stark separation between high-quality artificial intelligence investments and struggling lower-tier borrowers. Private credit funds must carefully balance sticky inflation hurdles with their emerging technology pivots to maintain yield without taking on uncompensated risk.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The market bifurcation is primarily driven by persistent sticky inflation, the disruption of legacy software models, and highly selective capital access from debt funds. Lenders are increasingly differentiating between top-tier borrowers and vulnerable entities.

For Q1 2026, the Proskauer Private Credit Default Index reached 2.73%, and S&P Global reported a US commercial mortgage-backed securities 30-plus day delinquency rate of 6.2%. Fitch Ratings forecasts leveraged loan defaults of 4.5% to 5.0% for the full year.

Institutional investors are defensively preserving capital through prolonged holding periods and maintaining liquidity via at-the-market equity issuances. Offensively, they are shifting capital towards artificial intelligence and emerging technology ventures.

The distress ratio tracks the percentage of debt obligations trading under 80% of par value, acting as an early warning signal. A climbing ratio indicates that secondary market buyers demand significant discounts due to increased risk of potential insolvencies.