The broader quantitative hedge fund sector spent early 2026 navigating its worst drawdowns since October 2025. In striking contrast, a commercial analysis of Virtu Financial stock reveals a market maker delivering record-breaking profitability during the first quarter. Major competitors like Citadel Securities and Two Sigma are aggressively marketing their artificial intelligence adoption.

According to unverified reports, the firm also maintains a strict refusal to pivot into traditional asset management or accept outside capital. Avoiding the two biggest trends in modern finance actually drives superior shareholder returns by protecting the firm from compounding systemic risks.

Investors evaluating financial technology equities must understand why capital preservation currently outranks aggressive technological expansion. This strategic restraint provides a highly attractive equity valuation in an increasingly unpredictable United States market environment.

The First Quarter Catalyst and Operational Scale

Virtu established formidable operational authority with its historic outperformance in the first quarter of 2026. These results stemmed entirely from established liquidity provision models rather than speculative new technology. The financial success reflects the firm’s structural scale and a highly favourable macroeconomic environment for United States equities.

The market making and client execution divisions both demonstrated significant sequential growth amid shifting volatility. Analysts projected quarterly net income between $290 million and $310 million, but the firm’s actual revenue generation dismantled consensus estimates. Top-line revenue reached $786.53 million, surpassing market expectations by more than $230 million.

This structural scale translated directly into dominant margin capture across multiple trading desks. According to unverified reports, the firm reported top-line income hitting $1.1 billion with adjusted EBITDA of $521 million, representing a highly efficient 66% margin. According to unverified reports, daily adjusted net trading revenue averaged $12.9 million for the quarter, highlighting consistent daily profitability.

These robust margin capture metrics align directly with the firm’s official SEC filings, verifying the historic revenue generation and operational efficiency achieved during this macroeconomic cycle.

| Metric | Q1 2026 Analyst Estimate | Q1 2026 Actual Reported |

|---|---|---|

| Earnings Per Share (EPS) | $2.24 | |

| Total Revenue | $556.38M | $786.53M |

According to unverified reports, the execution division has now recorded eight sequential quarters of expanding total net trading revenues. This financial beat proves that strategic restraint is not impeding corporate performance or growth metrics. The core business model remains highly lucrative without requiring an aggressive, high-risk technological pivot.

When big ASX news breaks, our subscribers know first

Why Generative AI Fails in High-Frequency Trading

The financial sector is currently saturated with artificial intelligence marketing, but technical realities tell a different story. Generative AI faces severe functional failures when deployed in live, high-frequency trading environments. Competitors like Jane Street and Two Sigma are rapidly hiring AI researchers, yet industry case studies highlight significant friction in utilising Large Language Models for automated execution.

Recent experimental finance research confirms that language models consistently fail to replicate the nuanced, risk-adjusted decisions of human market participants when deployed in simulated environments.

These friction points make experimental finance paradigms dangerous for capital preservation. Large Language Models lack the deterministic precision required for sub-millisecond market responses.

The primary operational vulnerabilities include the following limitations:

Replication failures: LLM-based agents consistently fail to accurately replicate the risk-adjusted execution decisions of human traders in live markets. Attention vulnerabilities: Generative models struggle with attention-driven trading dynamics and remain highly susceptible to minor anomalies, occasionally falling for fake news pranks that trigger illogical trades. * Transaction cost mismanagement: Experimental paradigms fail to effectively manage slippage or respond appropriately to shifting market microstructures.

Traditional Statistics vs Generative Models

Algorithmic trading relies on clearly defined mathematical boundaries to function safely. Traditional quantitative finance utilises statistical modelling, a framework that quants have trusted for decades to identify pricing anomalies. Statistical modelling is inherently reliable and predictable because it relies on historical probabilities and rigid deterministic rules.

Generative AI introduces unacceptable probabilistic risks by attempting to predict text or code outputs based on pattern association rather than rigid mathematics. For high-frequency trading infrastructure, a hallucinated market signal can destroy months of accumulated alpha in seconds. Understanding this limitation protects investors from buying into superficial corporate AI hype when evaluating financial technology equities.

Liability Management Over Technological Hype

Virtu approaches technology through the lens of aggressive liability management rather than pursuing the latest trends. The Chief Executive maintains strict boundaries on artificial intelligence deployment within the firm’s proprietary architecture. The explicit avoidance of automated code generation in core trading algorithms serves as a deliberate protective moat.

This compromise position allows the firm to use AI strictly to accelerate routine programming tasks and augment developer efficiency. By keeping generative models out of the execution architecture, the firm prevents catastrophic automated trading errors. This technological conservatism actively protects the capital base from compounding systemic failures.

Doubling Down on Human Capital

The rejection of automated trading code connects directly to a heavy investment in human engineers and quantitative researchers. The firm strategically allocates monetary compensation expenses toward securing premium industry talent.

This focus on human capital ensures that complex market microstructures are navigated by experienced professionals rather than probabilistic algorithms. Management plans to expand this highly specialised human workforce by the end of 2026. Raising compensation ratios to attract top-tier talent provides a more secure competitive advantage than relying on unpredictable machine learning models.

Readers interested in how this personnel strategy translates to operational leverage can read our full explainer on Virtu’s talent-driven earnings beat, which details the firm’s active trading capital deployment and its expanding engineering workforce.

The Hard Ceiling on Quantitative Capital

The firm pairs its technological restraint with a strict refusal to launch an internal investment fund or pivot into traditional asset management. Turning away outside capital is a mathematical necessity in quantitative finance rather than a lack of corporate ambition. Systematic trading strategies run into hard capacity limits when flooded with excess liquidity.

The broader US market context validates this highly constrained approach. In early 2026, aggressive quantitative hedge funds faced massive drawdowns driven by the rapid unwinding of crowded equity trades. Popular strategies break down entirely when too many participants deploy too much capital into the same statistical anomalies.

When an initial mathematical model uncovers a temporary pricing inefficiency, optimal capital deployment can extract substantial yield. The problem arises when competing funds detect those identical patterns and flood the strategy with outside asset management capital. This massive influx of liquidity compresses the available profit margins and eventually wipes out the mathematical advantage completely. Under these saturated conditions, a sudden shift in macroeconomic volatility often forces simultaneous liquidations across the sector.

Institutional investors adopting defensive strategies to hedge against global energy disruptions are acutely aware that such macroeconomic shocks will rapidly expose over-leveraged quantitative funds.

Virtu avoids this destruction by trading purely on its own balance sheet. The firm deployed fresh internal trading funds over recent months, which directly drove the record Q1 profits.

Their current mathematical models are highly lucrative but structurally limited in capital absorption. Recognising these capacity constraints helps investors understand that bigger funds do not automatically equate to better returns.

Commercial Valuation and Forward Strategy

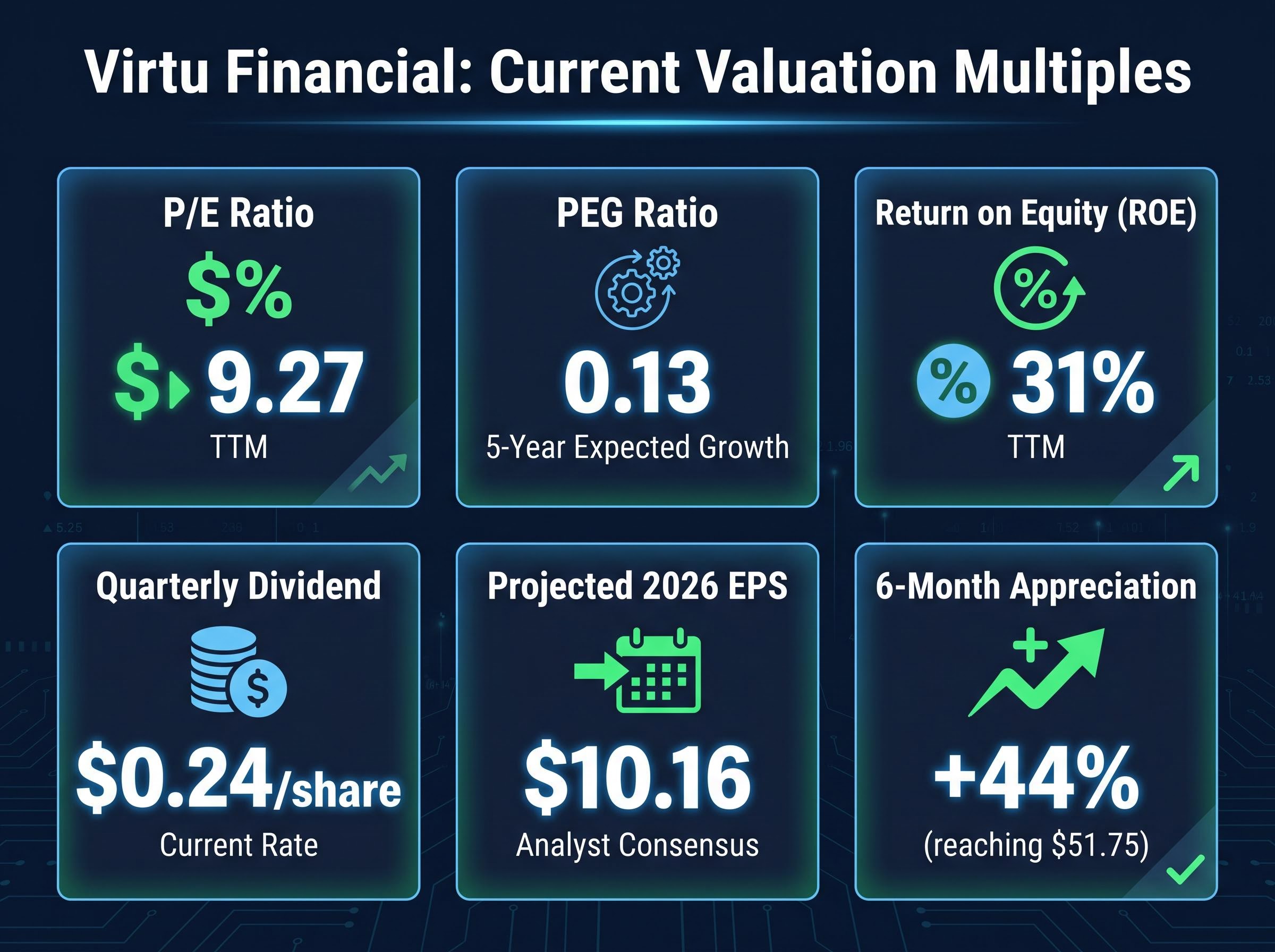

The firm’s contrarian choices translate directly into actionable commercial strength and highly attractive pricing metrics. According to unverified reports, following the Q1 2026 earnings updates, the equity demonstrated a 44% appreciation over a six-month period, with early trading bumps reaching $51.75. The market is currently rewarding this risk-averse, highly disciplined business model.

Current valuation multiples prove the financial validity of their restrained strategy. The stock trades at a significant discount relative to broader financial technology peers while offering superior capital returns. According to unverified reports, market consensus currently projects $10.16 in annual per-share earnings for the full 2026 fiscal cycle.

Key valuation and return metrics include:

Price-to-Earnings (P/E) Ratio: A highly attractive 9.27 multiple based on recent trailing performance. PEG Ratio: According to unverified reports, positioned at 0.13, indicating significant earnings growth relative to the current valuation. Return on Equity (ROE): According to unverified reports, maintaining a strong 31% return metric on deployed capital. Dividend Yield: A maintained regular quarterly dividend payout of $0.24 per share.

The Premium on Restraint in a Hyperactive Market

True operational alpha currently stems from knowing exactly what technology not to use and what capital not to accept. The firm’s historic Q1 2026 profitability proves the validity of their disciplined, human-centric quantitative model. By rejecting generative AI for core execution and refusing external asset management capital, the firm maintains strict control over its risk profile.

Firms pursuing aggressive technological pivots are increasingly burdened by power grid limitations and costly data center interconnections, adding significant physical friction to their operational margins.

This conservative approach provides a stable, high-margin profile even amid unpredictable United States equity environments. As quantitative hedge funds navigate capacity limits and algorithmic crowding, this restraint positions the firm to weather upcoming macroeconomic volatility far better than its over-leveraged competitors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.