The United States economic embargo on Iran, initiated by the Trump administration in early 2026, represents more than a foreign policy shift. It is a domestic wallet issue that fundamentally alters household spending power and corporate profit margins. Conflicts across the Middle East, prolonged hostilities in Ukraine, and escalating trade friction with China are reconfiguring global supply chains and inflating energy costs.

The initial economic impact of geopolitical conflict is already visible in wholesale energy markets, where embargoes on major producing nations restrict global crude supplies and force domestic fuel prices upward.

These geopolitical pressures now act as the primary stock market drivers for the remainder of the year. Investors face a fragmented environment where broad index performance masks aggressive capital reallocation beneath the surface.

This breakdown outlines how global hostilities are siphoning capital away from discretionary travel sectors while simultaneously fortifying discount retail equities and domestic energy infrastructure. The resulting divergence offers clear signals for portfolio positioning in a constrained consumer economy.

Educational Breakdown: How Geopolitical Risk Reallocates Consumer Capital

Understanding market divergence requires examining the psychological and financial mechanics of consumer downshifting. When international conflicts disrupt overseas supply chains, the resulting energy inflation acts as an immediate tax on domestic household budgets. This dynamic demonstrates the principle of discretionary income elasticity, where budget-conscious shoppers ruthlessly prioritise core value over experiential luxury.

The step-by-step transmission from global conflict to household constraints follows a predictable pattern:

Port blockades and shadow banking sanctions restrict global oil exports Wholesale energy markets price in supply risk through elevated premiums Increased transport and aviation fuel costs flow into domestic food and logistics networks Households experience an estimated 2% to 3% reduction in discretionary income

The Transmission Mechanism of Global Inflation

The current embargo features active port blockades that directly restrict petroleum exports. Concurrently, new sanctions targeting shadow banking networks limit alternative financing routes, injecting significant pricing volatility into wholesale energy markets. The International Monetary Fund (IMF) projects baseline global economic growth at 3.3% for 2026, assuming these conflicts remain contained.

Under this reference case, baseline inflation is projected to rest at 4.4%. However, severe conflict scenarios suggest global inflation could exceed 6%.

The official IMF global inflation projections detail how prolonged hostilities in key shipping lanes systematically translate into entrenched consumer price hikes.

Understanding this economic mechanism prevents investors from panicking over broad market declines. Instead, it highlights the predictable flow of capital from luxury sectors toward defensive value equities as household budgets tighten.

When big ASX news breaks, our subscribers know first

Margin Compression in the Sky: Why Tourism is Absorbing the Shock

The travel sector illustrates the starkest contrast between historical optimism and emerging operational realities. In 2025, international tourist arrivals reached a record 1.52 billion, representing a 4% year-over-year increase across the industry. That momentum has now collided with tightened US immigration policies and the harsh realities of global instability in 2026.

Commercial airlines and online accommodation platforms are uniquely vulnerable to volatile aviation fuel costs and declining traveller sentiment. Top-line revenue growth in the travel sector currently masks severe underlying margin compression. Booking Holdings reported $5.53 billion in Q1 2026 revenues, a 16% year-over-year expansion, yet operational challenges are mounting.

The company explicitly noted that hostilities are actively disrupting international travel patterns. According to industry data, overseas hostilities directly caused a decline in accommodation reservations during the first quarter.

Management Commentary “While our top-line revenue demonstrates resilience, prolonged geopolitical instability in the Middle East and fluctuating aviation fuel costs remain significant operational headwinds for our near-term regional bookings,” noted Booking Holdings management in their first-quarter update.

This divergence signals that impressive revenue figures may hide severe profit erosion. Leisure equities face significant earnings risk as elevated fuel prices compound the effects of weakened consumer travel sentiment.

For investors evaluating the specific winners and losers in this environment, our detailed coverage of sector divergence compares the margin destruction seen in aviation against the structural resilience of value retailers.

The Value Migration: Discount Retailers Capturing the Fallout

Consumer spending in the US remains resilient, but inflation has forced that capital to migrate aggressively down the value chain. Wholesale clubs and off-price retailers are capturing the budget-conscious consumer who is actively fleeing traditional retail environments. This shift proves that the broader economy is still transacting heavily despite macroeconomic headwinds.

This apparent sales resilience often obscures underlying household savings depletion, as lower income shoppers burn through their remaining financial buffers to maintain basic consumption levels.

Costco serves as a primary beneficiary of this capital reallocation. The wholesale retailer reported net sales of $65.98 billion for Q1 2026, representing an 8.2% year-over-year increase. Comparable sales growth reached 6.4%, confirming that foot traffic and basket sizes are expanding at discount hubs.

Major payment networks provide further evidence of consumer spending shifts. American Express reported Q1 2026 network volumes of $486.3 billion, marking an 11% expansion driven heavily by everyday spending categories. Similarly, major payment networks recorded an increase in transaction volumes, indicating that discretionary spending has rotated into different merchant categories rather than vanished entirely.

| Company | Sector | Q1 2026 Volume/Sales | YoY Growth |

|---|---|---|---|

| Costco | Discount Retail | $65.98 billion | 8.2% |

| American Express | Payment Processing | $486.3 billion | 11.0% |

These metrics highlight actionable sectors that historically outperform during inflationary embargo environments. Investors can look to discount retail and payment processors as practical hedges against the broader consumer downshift.

The Institutional Shield: Tech and Alternative Energy Infrastructure

While retail consumers adjust their household budgets, institutional capital is seeking refuge in sectors insulated from discretionary spending drops. Massive corporate spending is accelerating in areas deemed critical for US national security and technological dominance. These strategic infrastructure investments operate completely independently of retail consumer sentiment.

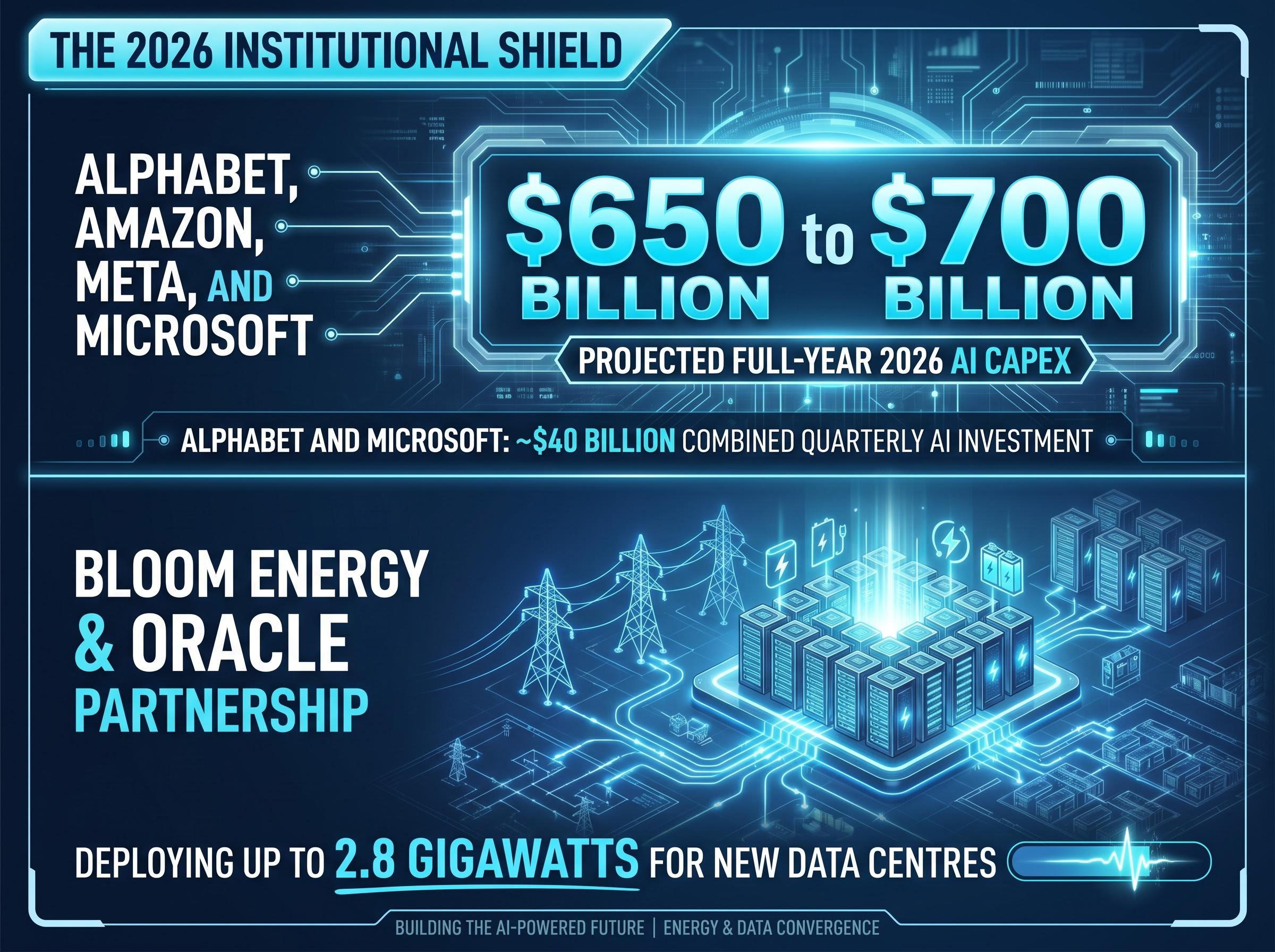

The ongoing artificial intelligence boom necessitates an urgent and parallel expansion in alternative power generation. Combined AI capital expenditures for Alphabet, Amazon, Meta, and Microsoft are projected to reach between $650 billion and $700 billion for the full year 2026. Early estimates indicate Alphabet and Microsoft are leading the near-term sector growth, deploying roughly $40 billion in combined quarterly AI investments.

This technological arms race directly benefits energy infrastructure providers. Bloom Energy saw its Q1 2026 sales reach $653.3 million. This revenue spike was heavily driven by a new strategic partnership with Oracle to deploy up to 2.8 gigawatts of power for new data centres.

The Bloom Energy and Oracle infrastructure expansion highlights a broader trend where hyperscalers are bypassing traditional utility grids to secure dedicated power sources for massive computing clusters.

Major drivers of tech infrastructure spending in 2026 include:

- Sovereign AI capacity development mandated by US national security directives

- Data centre power architecture upgrades to support advanced semiconductor clusters

- Alternative energy grid integration to bypass regional utility constraints

- Geopolitical supply chain decoupling requiring domestic facility construction

This capital expenditure cycle provides a strong portfolio shield. It offers a highly capitalised investment thesis that remains untouched by travel slowdowns or retail margin compression.

The 2026 Portfolio Strategy in a Fragmented Global Economy

The current market environment is defined by a severe divergence between penalised discretionary sectors and the beneficiaries of institutional capital reallocation. Investors must navigate a market where consumer spending prioritises discount retail while corporate spending fortifies domestic energy and technology infrastructure.

The Federal Reserve offers no immediate relief for sectors struggling with margin compression. According to the CME FedWatch Tool, there is a 66% probability that interest rates will remain unchanged for the remainder of 2026. Market analysts project that significant rate cuts are unlikely until late 2027, meaning companies cannot rely on cheap borrowing costs to rescue struggling operations.

When rebalancing equities moving forward, investors should weigh geopolitical risks heavily against historical revenue patterns. Portfolios weighted toward experiential luxury or aviation-dependent travel face prolonged headwinds from energy inflation. Conversely, strategic allocations in off-price retail and sovereign-backed technological infrastructure provide structural defence in an increasingly volatile global economy.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.