Brent Crude Crashes 10% on Draft US-Iran Hormuz Deal

4 hrs ago

Wall Street analysts are aggressively recalibrating their projections as the high-growth beverage sector prepares for a major round of first-quarter earnings in May 2026. Following an explosive 2025 defined by massive acquisitions and unprecedented physical footprint expansion, retail investors are now forced to evaluate fundamentally different paths to profitability in the consumer beverage market. A direct comparison of the Celsius vs Dutch Bros stock strategies reveals how two distinct operating models are navigating current macroeconomic pressures and shifting consumer demands. The market has grown highly sensitive to both supply chain vulnerabilities and integration costs heading into this earnings cycle. This analysis unpacks the critical operational metrics, recent financial hurdles, and 2026-2028 consensus forecasts for both entities. By examining these underlying factors, investors can determine which growth strategy offers the most compelling risk-adjusted return over the coming fiscal year.

To properly frame the upcoming valuation comparison, investors must understand the structural mechanics that separate a distribution-reliant packaged goods brand from a capital-intensive retail operator. The consumer packaged goods distribution model relies entirely on securing prime retail shelf space, maintaining high-profile brand partnerships, and outsourcing production to third-party manufacturing facilities. This asset-light approach allows companies to scale rapidly without heavy real estate investments, capitalising on the broad consumer shift toward sugar-free and wellness-oriented functional beverages.

In contrast, the capital-intensive retail franchise model depends heavily on acquiring physical real estate, funding shop construction, and generating direct consumer loyalty. Management teams operating this model are actively working toward a broad corporate goal of expanding domestic retail capacity. These mechanical differences dictate how each company absorbs macroeconomic shocks, such as rising commodity prices or sudden supply chain disruptions. Corporate revenues generated via direct retail operations face distinctly different margin pressures than those generated through wholesale distribution networks.

Management teams navigating CPG sector profitability challenges must often absorb intense margin compression when attempting to scale omnichannel logistics during sudden spikes in consumer demand.

The primary margin drivers for the packaged goods model versus the retail model highlight these divergent strategies:

Wholesale volume pricing: Packaged goods brands rely on high-volume wholesale distribution contracts to maintain profit margins across sprawling third-party retail networks. Co-packing efficiency: Outsourced manufacturing costs fluctuate based on aluminium pricing and third-party facility capacity constraints. Same-store sales growth: Retail operators focus heavily on increasing the average ticket price and total transaction volume at existing physical locations. Property leasing costs: Retail models must navigate commercial real estate expenses and local labour market wage fluctuations to protect unit-level economics.

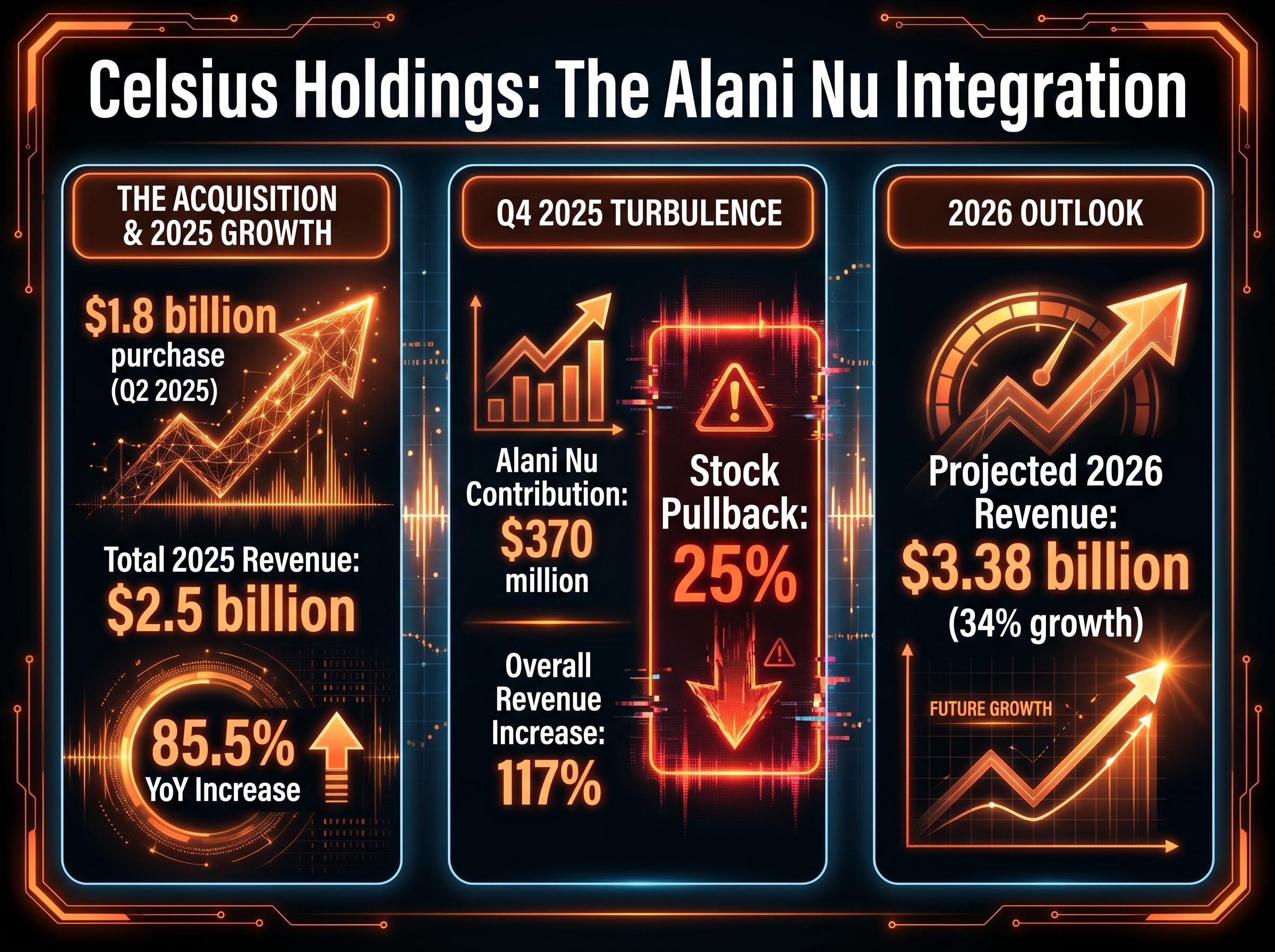

The 2025 acquisition of Alani Nu temporarily transformed the financial profile of Celsius Holdings, sending initial revenue figures surging before the reality of integration costs set in. The company officially completed the $1.8 billion purchase in the second quarter of 2025, triggering an immediate top-line expansion across its entire distribution network. By the end of the year, total 2025 revenue reached $2.5 billion, marking an 85.5% year-over-year increase.

The fourth quarter of 2025 demonstrated the sheer scale of the combined portfolio, with Alani Nu contributing $370 million in pro forma net sales. This specific integration served as the primary driver for a 117% overall revenue increase during the quarter. However, the stock experienced a severe 25% pullback following the fourth-quarter earnings release as investors reacted negatively to persistent integration costs. The May 11, 2026 earnings call will provide necessary visibility into whether management has successfully contained these post-acquisition expenses.

Despite the equity correction, Wall Street forecasts project total sales will climb between 2026 and 2028. This long-term growth assumes the company can successfully leverage new initiatives, such as its recent brand collaboration with the fitness company solidcore, to capture further market share.

Analyst Consensus View Financial analysts currently project full-year 2026 revenue for the combined company will hit $3.38 billion, representing an expected 34% year-over-year growth trajectory.

Understanding the anatomy of the recent equity decline provides an analytical lens for determining if the current valuation represents a discounted buying opportunity. The specific margin pressures that spooked investors in late 2025 stemmed directly from the complex logistical merging of two massive distribution networks, which temporarily eroded the company’s previously strong balance sheet.

To counter domestic margin compression, management is aggressively accelerating international expansion efforts. This geographic diversification serves as a core component of the corporate recovery strategy, aiming to reduce dependence on the highly saturated North American retail sector.

Establishing profitable overseas distribution channels requires localized consumer engagement strategies, and some modern distributors are even introducing blockchain-based loyalty programs to track repeat purchases across complex Asian retail networks.

While its packaged goods competitor navigated volatile acquisition dynamics, Dutch Bros built steady, compounding operational momentum through physical footprint growth. The retail operator completed 2025 with 1,136 total stores, successfully opening 154 new shops throughout the calendar year and expanding its national presence. This methodical property expansion generated a total 2025 revenue of $1.64 billion, representing a 27.9% year-over-year increase.

The core operational strength of the business was further validated by a healthy 5.6% increase in full-year 2025 same-store sales. Looking toward the scheduled May 6, 2026 earnings date, corporate guidance projects the opening of at least 181 new shops alongside 3 to 5% same-store sales growth for the year. However, this aggressive expansion strategy faces significant operational headwinds from rising global coffee commodity costs. The ability to maintain bottom-line net income growth depends entirely on successfully passing these inflationary pressures to the consumer without damaging transaction volumes.

The latest International Coffee Organization pricing trends show that persistent climate disruptions in major South American export regions will likely keep raw bean procurement costs elevated well into the latter half of the decade.

Management is deploying three specific tactical moves to defend profit margins against these persistent supply chain pressures:

A direct comparative analysis of current market capitalisations and forward price-to-earnings ratios forces investors to critically evaluate whether a premium price tag is justified by operational stability. As of late April 2026, the packaged goods operator holds a market capitalisation of $8.38 billion, while the retail operator sits slightly lower at $7.05 billion. The forward P/E ratio disparity presents a stark contrast, with the former trading at a modest 21.10 compared to the latter’s premium 69.93 multiple.

The gross profit margin difference highlights the fundamental separation in capital efficiency between the two business models. The packaged goods company generates a highly lucrative gross profit margin, heavily outperforming the margin achieved by the retail operator. This valuation gap reflects how Wall Street is currently pricing the respective risks of acquisition integration baggage versus retail commodity cost inflation.

Analysts often apply complex structural margin recovery models when evaluating retail operators, as a small improvement in unit-level profitability can justify significant upward revisions in multi-year earnings estimates.

Retail investors must evaluate whether an expensive, lower-margin stock with predictable execution is preferable to a cheaper, higher-margin equity carrying integration risks. Financial models heading into the first-quarter earnings cycle suggest the market is placing a heavy premium on physical store expansion over distribution synergies.

| Financial Metric | Celsius Holdings (CELH) | Dutch Bros (BROS) |

|---|---|---|

| Market Capitalisation | $8.38 billion | $7.05 billion |

| Forward P/E Ratio | 21.10 | 69.93 |

| 2025 Revenue Growth | 85.5% | 27.9% |

| Gross Profit Margin |

The distinct investment thesis for each company ultimately depends on an investor’s personal tolerance for valuation multiples and operational predictability. The upcoming May 2026 earnings reports will prove critical in either confirming or invalidating current Wall Street models regarding corporate profitability. Market participants must carefully monitor how effectively the packaged goods company manages its ongoing distribution synergies compared to the retail operator’s ability to shield its margins from agricultural commodity inflation.

With the May 6 and May 11 earnings dates rapidly approaching, the forecasted 2026-2028 growth trajectories face their first major test of the fiscal year. Investors should track gross margin stability, same-store sales data, and revenue guidance revisions over the next two quarters to validate these forward-looking equity targets.

For readers wanting to understand the operational complexities of running a global cafe network, our full explainer on Starbucks turnaround strategies covers the specific digital engagement, operational efficiency, and store innovation tactics required to maintain profitability in physical retail.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Celsius operates an asset-light, distribution-reliant packaged goods model, leveraging brand partnerships and outsourced production, while Dutch Bros uses a capital-intensive retail franchise model focused on physical store expansion and direct consumer loyalty.

The stock pulled back because investors reacted negatively to persistent integration costs following the $1.8 billion Alani Nu acquisition, which temporarily eroded the company's strong balance sheet.

Dutch Bros faces significant operational headwinds from rising global coffee commodity costs, which could impact its ability to maintain net income growth without damaging transaction volumes when passing costs to consumers.

Investors should monitor Celsius's success in containing post-acquisition expenses and managing distribution synergies, alongside Dutch Bros' ability to shield margins from commodity inflation and achieve its new shop and same-store sales growth targets.