Retail Investor Trends: Analysing the 2026 Flight to Global ETFs

2 mins ago

A thorough Celsius stock analysis requires examining the staggering financial transformation the company achieved by the end of 2025. Management reported $2.515 billion in full-year revenue, representing an 85.5% year-over-year jump that redefined the organisation’s commercial footprint. Operating in April 2026, investors are evaluating an entirely new corporate entity.

The recent series of acquisitions fundamentally altered the balance sheet, setting a high bar for the upcoming May 2026 first-quarter earnings report. This assessment breaks down whether the combined company’s financial fundamentals can support Wall Street consensus estimates. The gap between historical momentum and forward expectations reveals how market participants are pricing the newly enlarged portfolio’s ability to execute its integration strategy.

The $1.65 billion acquisition of Alani Nu, which commenced in April 2025, fundamentally altered the core portfolio. The sheer volume of new revenue validates management’s shift towards a multi-brand strategy, replacing reliance on a single product line with diversified revenue streams. This transaction immediately improved the product mix for female consumers, directly contributing to record fourth-quarter sales figures.

Other consumer staples companies are similarly executing multibrand beverage strategies to capture adjacent categories, with operators expanding into the rapidly growing matcha market to diversify their portfolios.

Celsius Holdings reported fourth-quarter 2025 revenue of $721.6 million, marking a 117% year-over-year increase that outpaced analyst expectations. For context on the immediate impact, second-quarter 2025 revenue hit $739.3 million, generating a record adjusted EBITDA of $210.3 million as the newly acquired brand integrated into the system.

The structural margin improvements occurred alongside early integration costs. The combined entity absorbed $21.7 million in initial inventory expenses, yet still delivered enhanced gross margins across the quarter. Management projects $50 million in run-rate cost synergies within two years, suggesting the current profitability metrics represent a baseline rather than a ceiling.

| Full-Year 2025 Total Revenue | Core Celsius Contribution | Alani Nu Contribution (Q2-Q4) |

|---|---|---|

| $2.515 billion | $1.46 billion | $1,001.9 million |

Investors require evidence that large capital outlays deliver tangible returns. The initial integration data demonstrates management’s capacity to execute complex mergers, confirming the newly acquired brand’s ability to operate successfully at scale within the larger corporate framework.

Wall Street analysts use forward earnings projections to assess whether a company can generate sufficient profit to justify its current valuation. Earnings per share (EPS) acts as the ultimate scorecard for acquisition success, measuring the net income allocated to each outstanding share of common stock. While revenue expansion indicates growing market demand, EPS growth demonstrates a company’s ability to convert those sales into actual shareholder value.

The difference between top-line expansion and bottom-line growth is highly dependent on how the company manages its debt obligations. The $900 million Term Loan B used to finance the transaction introduces significant interest expenses that must be offset by projected cost synergies. Wall Street consensus estimates currently project revenue expansion.

Examining the Celsius official regulatory filings reveals the specific terms and interest rate structures of this borrowing facility, which directly dictate the cash flow requirements needed to service the debt over the coming fiscal periods.

Over that same period, analysts forecast a jump in EPS. This aggressive projection relies heavily on the combined portfolio maintaining its integration efficiency. As of April 2026, Zacks Consensus estimates project a 61% year-over-year EPS growth rate for the upcoming first quarter, with full-year 2026 EPS growth slated at 19.40%.

Achieving these targets in a crowded retail sector requires precise execution across three primary levers:

Synergy realisation through integrated supply chains and shared distribution networks Margin expansion driven by pricing power and reduced packaging costs * Consistent volume growth across both core and acquired brand lines

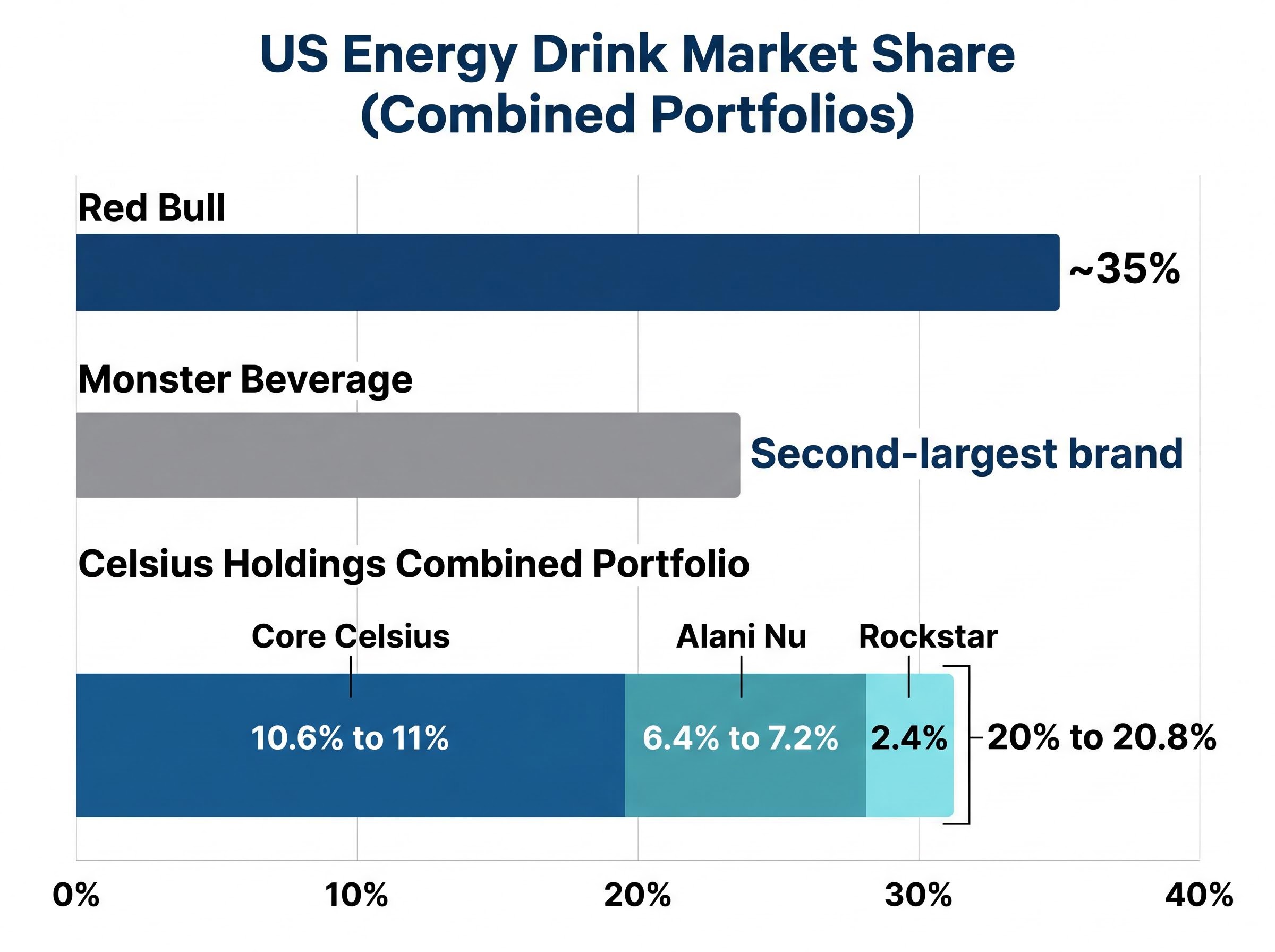

The optimism surrounding the recent acquisitions must be weighed against the defensive realities of competing with entrenched legacy leaders. The combined Celsius portfolio now commands a US market share of 20% to 20.8%, cementing its position as a dominant force in traditional retail channels. Internal data breaks this down to the core Celsius brand at 10.6% to 11%, Alani Nu at 6.4% to 7.2%, and Rockstar at 2.4%.

Recent Circana retail tracking data confirms this structural shift in consumer preference, validating that the expanded multi-brand portfolio has successfully secured distribution territory previously dominated by older legacy beverage manufacturers.

Despite these substantial gains, the company continues to trail Red Bull, which maintains a commanding 35% market share. To secure retail shelf space and defend against competitors, Celsius has deployed a tactical strategy relying on limited-time offerings, such as the Sherbet Swirl release, alongside deep penetration into the female demographic. While operators like Dutch Bros command high premiums in the drive-thru crossover space, Celsius maintains its structural dominance in the traditional functional beverage category.

The current competitive hierarchy among the top US energy drink players reflects this concentration of market power:

Housing Celsius, Alani Nu, and Rockstar under a single corporate umbrella provides significant leverage when negotiating with major US distributors. Distributors prefer to manage fewer, larger accounts that can supply a diverse range of consumer demographics across multiple price points. This consolidated approach actively protects valuable shelf space against aggressive promotional manoeuvres from Monster and Red Bull.

Domestic market share gains will inevitably face friction, positioning overseas expansion as the necessary fuel for the 2028 financial projections. Aggregate international revenue reached $92.8 million for full-year 2025, representing a 24% year-over-year increase. The fourth quarter of 2025 alone contributed $22.1 million to that international total, proving that the overseas momentum is accelerating.

The company has executed tactical moves into the United Kingdom, Ireland, France, Australia, and New Zealand. Management recently secured an exclusive distribution deal with Suntory Beverage & Food Benelux in March 2025, granting the portfolio immediate access to Belgium and Luxembourg. Regional distribution partnerships remain a strategic priority, allowing the firm to scale its global presence efficiently without absorbing massive fixed overhead costs.

Deploying capital efficient distribution models allows brands to enter new international territories with minimal inventory risk and achieve rapid commercial validation within months of launch.

Management Commentary on International Growth “International expansion efforts are just beginning following the recent acquisitions, providing a clear pathway for geographic diversification.”

Investors must view this international execution as the primary derisking factor for the stock’s long-term valuation. If domestic growth slows, the European and Australasian markets will need to absorb the pressure to meet Wall Street’s aggressive forward estimates and justify the top-line revenue expansion forecast.

The enlarged Celsius portfolio presents a compelling integration success story balanced against highly demanding forward expectations. The impressive 2025 revenue figures confirm that the multi-brand strategy works in practice, yet the projected earnings jump leaves little room for operational errors. Earlier analyst notes highlighted bullish momentum, with the stock climbing 40% year-to-date as of early April 2025 amid an analyst upgrade, setting a high historical benchmark for the current valuation.

As of April 2026, the stock carries a Zacks Rank 3 (Hold), reflecting this tension between excellent historical execution and aggressive future estimates. The average analyst price target sits at $67.39, though the wide estimated range of $44 to $85 indicates significant divergence in how the market evaluates the company’s international growth trajectory. The combined entity possesses the commercial momentum to justify its current market position, provided its international distribution partnerships deliver on their initial promise.

For investors wanting to contextualise these bullish growth estimates against broader macroeconomic headwinds, our detailed coverage of underpriced stock market risk examines how geopolitical tensions and elevated oil prices could pressure consumer discretionary spending in the year ahead.

Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors. These statements regarding forward earnings are speculative and subject to change based on market developments and company performance. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Celsius's substantial 85.5% revenue jump to $2.515 billion in 2025 was primarily driven by the strategic acquisition of Alani Nu and the successful shift to a multi-brand strategy.

The $1.65 billion Alani Nu acquisition in April 2025 significantly diversified Celsius's revenue streams and product mix, immediately boosting fourth-quarter sales and contributing to record adjusted EBITDA despite initial integration costs.

The combined Celsius portfolio, including Alani Nu and Rockstar, commands a US market share of 20% to 20.8%, positioning it as a dominant force behind Red Bull and Monster Beverage.

Achieving the aggressive 2026 EPS growth targets requires Celsius to realize cost synergies, expand margins through pricing power, and maintain consistent volume growth across both its core and acquired brand lines.