Lululemon Plunges 12% on CEO Pick Amid Activist Investor Battle

2 hrs ago

This PROG Holdings earnings analysis examines the specific drivers behind the significant profit beat and the successful integration of newly acquired corporate divisions. Investors reviewing the updated guidance will find a strategy heavily reliant on diversified retail technologies rather than single-channel consumer financing.

The rapid shift in the company’s financial trajectory sets a new baseline for its operational performance through the coming quarters. Management’s clear rationale for raising the full-year profit outlook provides immediate clarity for the market.

The sheer magnitude of the first-quarter outperformance justified the immediate pre-market stock pop. PROG Holdings delivered an adjusted earnings per share (EPS) of $1.24, easily eclipsing the $0.80 Wall Street estimate. The top-line growth followed suit, with total revenue reaching $742.7 million against the forecasted $734.6 million.

This top-line expansion represents an 11.1 percent year-over-year increase, driven directly by newly integrated revenue streams performing ahead of schedule. Adjusted EBITDA reached $90.3 million, marking a substantial 29.2 percent jump from the previous year. The market absorbed this data rapidly, pushing the stock up into the green during early trading hours.

This level of profitability expansion highlights a broader trend in recent corporate earnings results, where companies achieving record efficiency are handsomely rewarded by the market even when aggregate sales metrics remain mixed.

Investors rely on these exact margins of outperformance to understand why the market reacted with such aggression. The gap between external models and actual reported figures signals that analysts underestimated the speed at which the company could scale its recent acquisitions.

| Metric | Actual Q1 Result | Wall Street Estimate |

|---|---|---|

| Adjusted EPS | $1.24 | $0.80 |

| Total Revenue | $742.7 million | $734.6 million |

| Adjusted EBITDA | $90.3 million | N/A |

The financial shock of the earnings beat stems from a fundamental shift in how the different corporate segments work together to generate predictable cash flow. The company operates a diversified model that blends traditional point-of-sale financing with rapid expansion in digital checkout solutions and recent corporate buyouts. This structure ensures that a slowdown in one division is absorbed by the accelerating growth of another.

Similar to broader e-commerce acquisitions that consolidate niche demographic markets, these targeted buyouts allow the firm to absorb active user bases and scale gross merchandise volume without building entirely new networks.

While the primary division saw a slight dip early in the year, it exited the quarter with positive momentum. This foundational context helps investors grasp the actual business operations driving the financial metrics. The strong quarter demonstrates that the success is structural rather than a one-time anomaly.

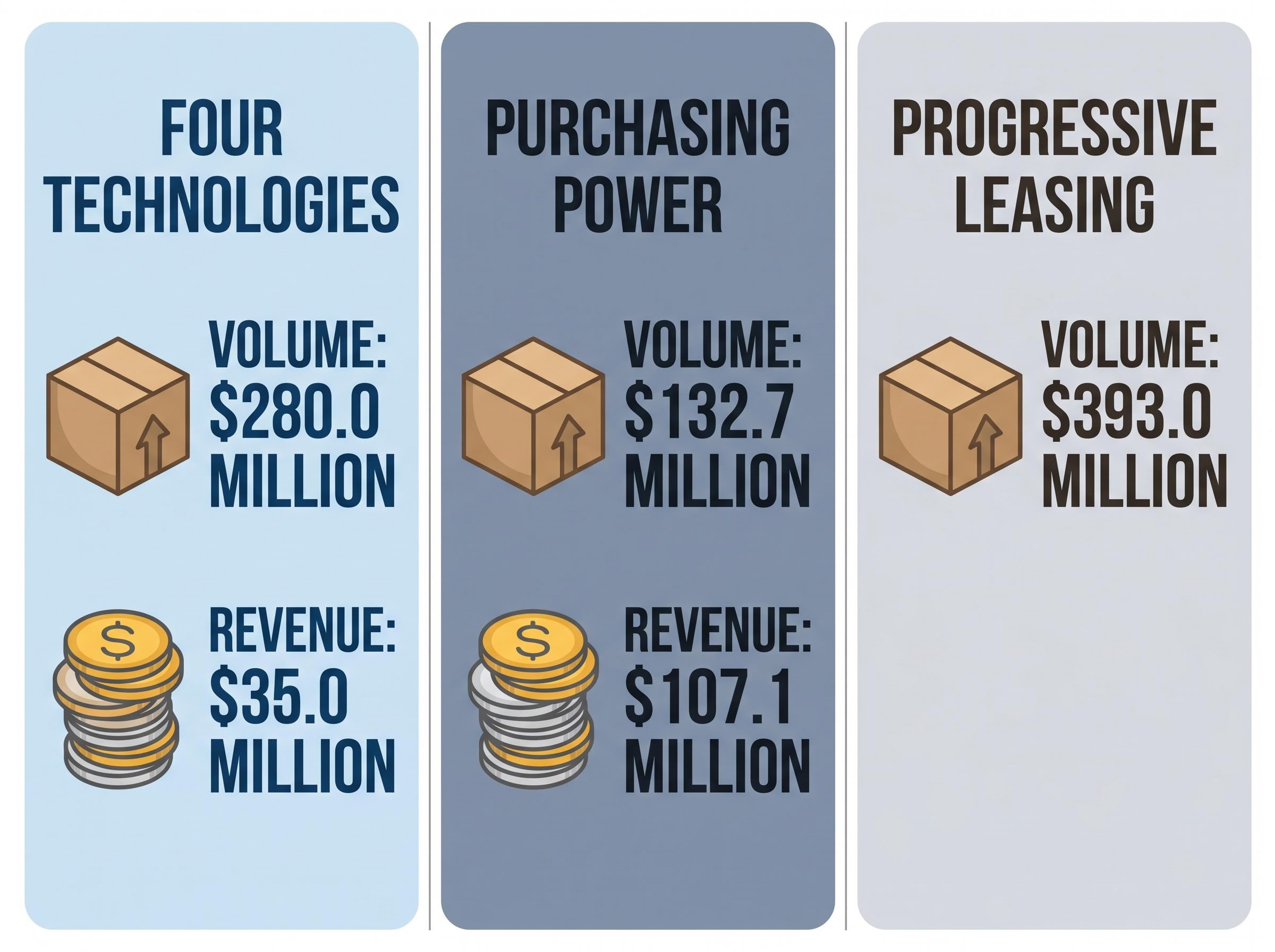

The three operational segments delivered the following specific performance metrics for the quarter:

Four Technologies: Delivered a massive 133.6 percent gross merchandise volume growth to $280.0 million, while pushing revenue up 142.3 percent to $35.0 million. Purchasing Power: Contributed significantly following its recent acquisition, generating $132.7 million in gross merchandise volume and $107.1 million in revenue. * Progressive Leasing: Recorded $393.0 million in volume, representing a minor 2.2 percent drop, though the segment successfully returned to growth by the close of the quarter.

Leadership shifted focus from revenue generation to strict financial discipline immediately following a major winter acquisition. The executive team aggressively paid down corporate obligations since the start of the calendar year to protect the balance sheet. This swift deleveraging connects directly to a stated management focus on strict operational controls.

The company achieved a $210 million reduction in net recourse debt since the January 2026 acquisition of the Purchasing Power segment. The current net leverage ratio now sits at a comfortable 2.0 times multiple. This leverage profile signals a highly successful corporate integration, reassuring shareholders that management is proactively neutralising the financial risks typically associated with large buyouts.

The rapid deleveraging process aligns with the S&P Global Ratings credit analysis published during the initial buyout phase, which highlighted the critical importance of disciplined debt management to maintain financial flexibility.

CEO Commentary “The strong quarter was driven by disciplined execution across the organisation and the benefits of our diversified model,” said Steve Michaels, Chief Executive Officer.

The immediate market optimism faces an apparent contradiction when reviewing the soft upcoming quarter against a raised annual forecast. Management issued conservative near-term estimates that lag behind consensus models, yet simultaneously elevated the full-year outlook. This prepares stakeholders for potential short-term volatility in the coming months while reinforcing a strong long-term investment thesis.

This cautious near term view likely accounts for growing US recession risk and rapid household savings depletion, which continue to threaten consumer retail spending over the coming months.

According to company data, for the upcoming three months, expected second-quarter adjusted EPS sits between $0.85 and $1.05, placing the midpoint below the $1.09 estimate. According to company data, second-quarter revenue is projected between $700 million and $725 million, trailing the $724.8 million forecast. Despite this near-term softness, the twelve-month trajectory remains highly bullish.

| Metric | Q2 Guidance | Q2 Estimates | New Full-Year Guidance | Previous Full-Year Guidance |

|---|---|---|---|---|

| Adjusted EPS | $0.85 to $1.05 | $1.09 | $4.40 to $4.80 | $4.00 to $4.45 |

| Revenue | $700 million to $725 million | $724.8 million | N/A | N/A |

The strong first quarter provided the exact financial padding necessary to raise the annual outlook. According to company data, management elevated the full-year adjusted EPS to a range of $4.40 to $4.80, a definitive step up from the prior $4.00 to $4.45 bracket. This upward revision indicates that leadership expects the integrated acquisitions to scale aggressively in the back half of the year, absorbing any second-quarter weakness.

The immediate takeaway from this earnings shock is a rapid upward repricing of the company’s equity valuation. The massive first-quarter profit beat proves the company can execute its diversification strategy effectively while managing post-acquisition debt.

Intraday trading volume and subsequent analyst rating changes will continue to shape the stock’s performance as regular trading hours commence. The market must now weigh the conservative second-quarter guidance against the upgraded full-year outlook. Management has successfully demonstrated that their multi-segment retail technology approach provides sufficient cash flow to navigate short-term headwinds.

Investors exploring how market expectations translate into asset repricing during these critical reporting periods will find our detailed guide to earnings season options pricing helpful, as it outlines how implied volatility crush and institutional hedging impact share trajectories.

Past performance does not guarantee future results, and these financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

PROG Holdings' stock surged pre-market after the company reported first-quarter adjusted earnings per share of $1.24, significantly exceeding Wall Street's estimate of $0.80.

PROG Holdings reported Q1 adjusted EPS of $1.24 against an $0.80 estimate and total revenue of $742.7 million, surpassing the $734.6 million forecast.

The company employs a diversified retail technology strategy that combines traditional point-of-sale financing with digital checkout solutions and recent corporate buyouts to generate predictable cash flow.

Yes, PROG Holdings raised its full-year adjusted EPS guidance to a range of $4.40 to $4.80, up from the previous $4.00 to $4.45 bracket, despite conservative second-quarter projections.