Major hardware suppliers have effectively sold out their entire production capacity for the remainder of 2026. This complete exhaustion of available inventory represents a structural shift in the fundamental mechanics of the data storage market, rather than a temporary supply chain disruption. Artificial intelligence applications have generated immense requirements for physical capacity, altering how enterprise infrastructure operates.

For information technology buyers and commercial procurement officers, understanding these hardware constraints is a strategic requirement for accurately forecasting cloud budgets over the next 18 months. The enterprise sector can no longer rely on historical purchasing patterns. When hardware availability contracts this severely, the resulting financial pressure forces every downstream technology consumer to recalibrate their capital expenditure models.

The 2026 Pricing Shock Hitting Enterprise Racks

The enterprise computing sector has long operated on the assumption that storage costs naturally decline year over year, but early 2026 broke that paradigm. Intense demand from artificial intelligence data centres drove unprecedented surges in enterprise hardware pricing during the first quarter. A concentrated group of market suppliers tightly controls the global inventory levels, allowing them to pass on structural price increases directly to commercial buyers.

High-capacity hardware models experienced price increases of up to 60%, while the market average cost per terabyte rose by approximately 46%. This supply squeeze provides commercial buyers with an immediate baseline for why their hardware acquisition costs are accelerating rapidly. The price of 30TB hard disk drives increased from $495 to $668, bringing the average cost to roughly $22.27 per terabyte.

Manufacturers expect these contract pricing trajectories to continue accelerating. Hardware analysts project additional contract price rises of 10-20% in the second half of 2026 as suppliers struggle to balance allocations. The gap between historical pricing models and current reality reveals how investors and procurement officers must recalibrate their expectations.

| Metric | Previous Baseline | New 2026 Baseline | Percentage Increase |

|---|---|---|---|

| 30TB Hard Disk Drive Unit | $495 | $668 | 35% |

| Average Cost Per Terabyte | $15.25 | $22.27 | 46% |

| High-Capacity Model Peaks | Standard Pricing | Peak Premium | 60% |

| Projected H2 2026 Contracts | Current Baseline | Future Contract | 10-20% |

When big ASX news breaks, our subscribers know first

Why Magnetic Disks Still Dominate the Artificial Intelligence Era

According to industry estimates, despite the rapid advancement of solid-state flash memory, traditional magnetic hard disk drives continue to secure approximately 80% of total cloud capacity requirements. A hard disk drive uses rapidly spinning magnetic platters to record and retrieve digital information. This older technology remains the unavoidable backbone of the modern tech boom because it offers the most cost-effective method for archiving massive volumes of information.

Hardware manufacturers are actively scaling specific technologies, such as Heat-Assisted Magnetic Recording, to increase the density of these platters and meet exact data pipeline needs. By understanding why flash memory has not fully replaced hard disk drives, decision makers can better evaluate vendor lock-in risks and hybrid storage architectures.

The commercial transition to platforms utilizing Heat-Assisted Magnetic Recording provides vendors with a multi-year competitive lead, as these advanced drives offer a compelling total cost of ownership advantage over competing solid-state options.

The primary demand drivers for this physical storage volume include artificial intelligence workflows, unstructured data from the Internet of Things, and cryptocurrency mining operations. Beyond these core requirements, several emerging drivers are shaping infrastructure demand for 2026:

Cyber-resilient architecture requiring redundant physical backups Autonomous robotics generating continuous operational telemetry * Sustainability and power efficiency mandates within enterprise facilities

Scaling Physical Infrastructure for GPU Clusters

There is a direct, unavoidable ratio between advanced graphics processing unit deployment and required physical data retention limits. Industry analysis from Solidigm indicates that 25 exabytes of storage will be required in 2025 solely to support infrastructure utilising 550,000 NVIDIA Grace Blackwell processors.

Power efficiency is becoming equally vital to raw capacity. Analysts project that electricity demand linked directly to artificial intelligence will double by the end of 2026. This forces facilities to balance high-performance computing with power-efficient magnetic archiving.

Wall Street Upgrades and Vendor Leverage

The sheer scale of recent financial upgrades illustrates a massive shift in negotiating leverage toward hardware vendors. Major United States market suppliers, such as Western Digital and Seagate Technology, have transitioned from component manufacturers to critical infrastructure gatekeepers. Purchasing requests now comfortably outpace available hardware limits, granting these vendors unprecedented pricing power over their enterprise clients.

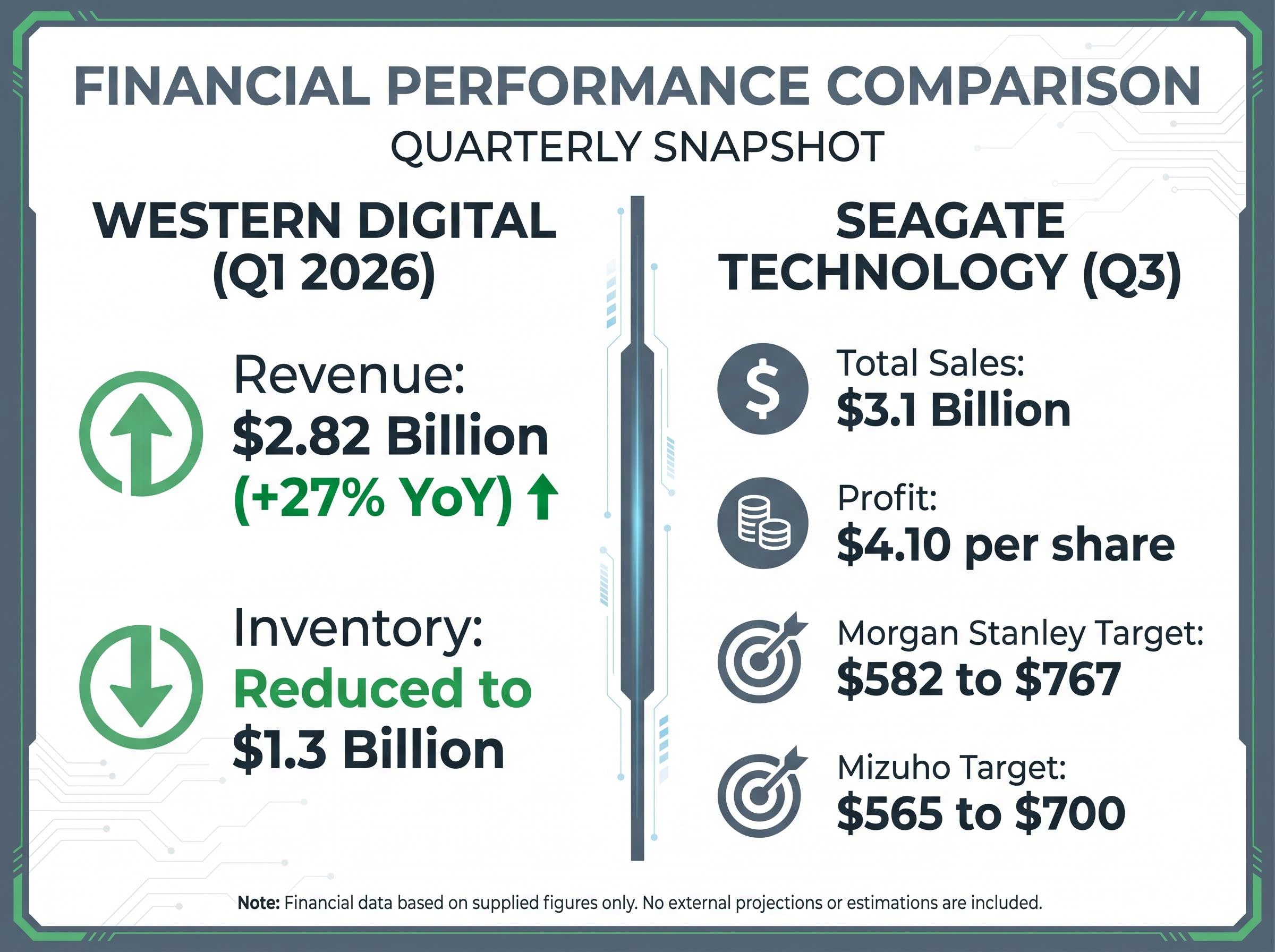

For commercial investors, tracking vendor profitability reveals the total loss of negotiating leverage on the buyer side of the market. Western Digital reported fiscal first-quarter 2026 revenue of $2.82 billion, representing a 27% year-over-year increase. The company simultaneously reduced its inventory levels to $1.3 billion, confirming the rapid sell-through of available capacity.

The official Western Digital fiscal 2026 results confirm this robust financial performance, highlighting how enterprise demand for high-capacity drives directly translates to corporate profitability.

Seagate demonstrated similar pricing leverage during recent reporting periods. According to external reports, the company reported fiscal third-quarter profits of $4.10 per share against expected estimates of $3.48, with total sales hitting $3.1 billion. Institutional analysts have aggressively shifted their financial models to account for this structural leverage.

Analyst Observation According to research from Morgan Stanley, previously optimistic bull-case scenarios for hardware vendors have transitioned into standard baseline expectations over the past three consecutive reporting periods.

According to analyst reports, based on these new baselines, Morgan Stanley raised its primary share price objective for Seagate from $582 to $767. According to analyst reports, the firm projects that calendar year 2027 earnings will land 132% higher than general market consensus. Similarly, according to analyst reports, Mizuho boosted its valuation target for the supplier to $700 from $565.

How Major Cloud Providers are Passing the Check

Most commercial buyers interact with the hardware market indirectly through cloud service providers. These upstream manufacturing costs are quietly inflating enterprise cloud computing bills across the technology sector. As suppliers increased contract pricing, major providers like Amazon Web Services, Google Cloud, and Microsoft Azure reacted by adjusting their own service structures.

The sequential progression of how these price increases moved through the supply chain demonstrates the direct commercial exposure facing enterprise consumers:

- Upstream hardware manufacturers implemented initial contract price increases during the first half of 2025.

- Major cloud platforms quietly absorbed these initial hardware premiums while halting historical patterns of discounting storage tiers.

- Amazon Web Services and Google Cloud announced broader, formalised cloud service price hikes in January 2026.

To balance performance needs with rising physical costs, cloud providers are rolling out specific mitigation strategies. Amazon Web Services introduced artificial intelligence-optimised storage tiers featuring 45% price cuts on certain processor instances.

However, these specific hardware discounts were largely offset by general service rate hikes across standard compute operations. Meanwhile, Microsoft Azure and the Google Cloud Platform are increasingly relying on hybrid storage solutions that automatically shift less critical information to cheaper magnetic disks to insulate clients from peak hardware inflation.

The 2027 Outlook for Enterprise IT Budgets

The long-term growth projections for the sector signal a challenging environment for commercial information technology planning. Enterprise decision makers must prepare for sustained high contract prices as manufacturers struggle to keep pace with demand through the end of the decade.

The overall United States market is projected to grow at a Compound Annual Growth Rate of 15-20% through 2030. Enterprise revenues were expected to exceed $50 billion in 2025, driven largely by specialised processing requirements. The artificial intelligence-powered sub-segment already reached $11.6 billion in 2024, underscoring the rapid capital rotation into this infrastructure.

In this constrained environment, locking in capacity early is a strategic necessity for institutional buyers. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.