Big Tech Earnings Face $600B AI Reality Check Today

1 min ago

Seagate Technology shares surged more than 16% in after-hours trading on 28 April 2026 after the company reported earnings and revenue that cleared Wall Street expectations by a wide margin, then issued guidance for the quarter ahead that did it again. The result lands as AI-driven demand for cloud storage infrastructure continues to accelerate, positioning Seagate’s nearline hard disk drive business at the centre of one of the most active capital expenditure cycles in recent memory. The stock had already gained more than 618% over the prior twelve months before this print. What follows breaks down exactly what Seagate reported, how the market reacted, what Morgan Stanley and Mizuho now project, and why the underlying HDD market dynamics may have more runway than the consensus had assumed.

Seagate reported Q3 FY2026 earnings per share of $4.10, against a consensus estimate of approximately $3.48. That is not a marginal beat. It is the kind of gap that forces a recalibration of what analysts thought the business was capable of generating in a single quarter.

Revenue came in at $3.1 billion, clearing the $2.95 billion consensus. The beat held on both the top and bottom lines simultaneously, a combination that tends to produce more durable post-earnings moves than a revenue miss offset by cost discipline.

The official disclosure of the fiscal third quarter 2026 financial results confirmed non-GAAP diluted EPS of $4.10 alongside a robust revenue figure of $3.11 billion, underscoring the fundamental strength behind the market reaction.

Then management guided the June quarter to $3.45 billion in revenue and $5.00 in earnings per share. Both figures sat above analyst consensus at the time of reporting, establishing that the outperformance was not treated internally as a one-quarter anomaly.

| Metric | Reported | Consensus Estimate | Beat/Miss |

|---|---|---|---|

| EPS (Q3 FY2026) | $4.10 | ~$3.48 | Beat |

| Revenue (Q3 FY2026) | $3.1B | ~$2.95B | Beat |

| Revenue Guidance (June Qtr) | $3.45B | Below $3.45B | Above consensus |

| EPS Guidance (June Qtr) | $5.00 | Below $5.00 | Above consensus |

Record gross margins: Gross margins reached approximately 47% in the quarter, described by Morningstar as record levels for the company, a figure that reflects pricing power rather than cost-cutting alone.

A 16% after-hours move in a stock already up more than 600% over the prior year is not a short squeeze or a relief rally. It is a market that expected strong numbers and still got surprised.

The discrepancy between the +16.51% verified figure and the roughly +18% cited elsewhere likely reflects different reference prices used by individual outlets. The core signal is the same: a stock with $579 worth of optimism already embedded in its price added another $95 in a single post-market session.

That kind of move on a stock that has already repriced this aggressively suggests the results genuinely exceeded expectations rather than simply catching positioned shorts off-guard. The after-hours volume indicated broad participation, not a thin-market anomaly.

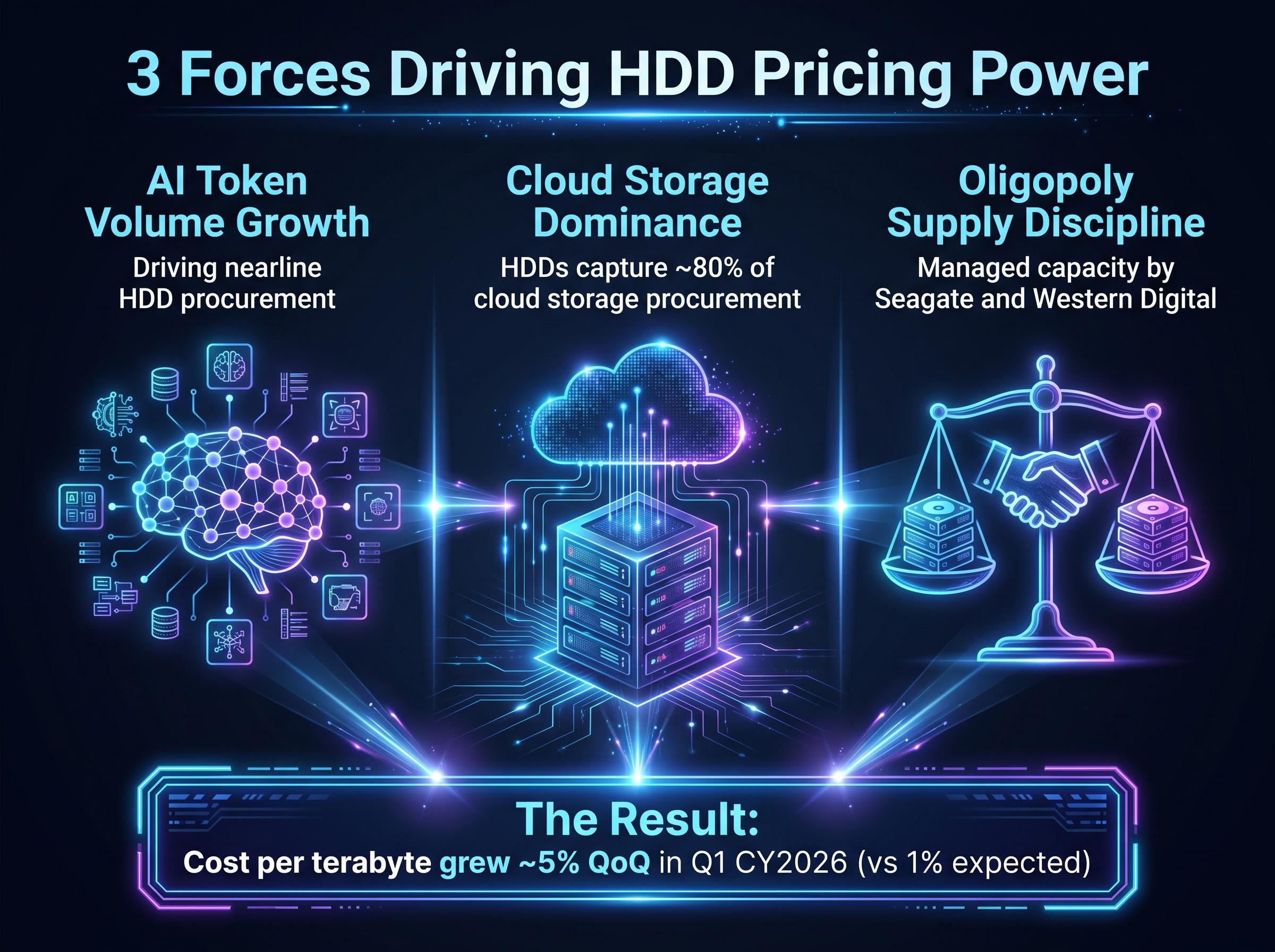

The earnings beat makes more sense when the supply-demand structure behind it comes into view. Seagate is not simply executing well in a stable market; it is operating with structural pricing leverage that few hardware businesses possess.

Recent TrendForce research on nearline HDD demand indicates that the expanding requirements of AI infrastructure are fundamentally transforming enterprise procurement strategies and creating a sustained tailwind for high-capacity storage components.

Three forces are converging:

Hyperscaler capital expenditure cycles favour HDDs for the storage layers that sit behind the compute-intensive AI inference and training workloads. As AI token volumes expand, so does the data that needs to be stored, indexed, and retained. Nearline drives, the high-capacity HDDs designed for data centre use, are the direct beneficiary.

The HDD market operates as a rational oligopoly. Seagate and Western Digital have collectively maintained supply below demand levels in the current cycle, preventing the margin compression that plagued the industry in earlier periods.

The clearest evidence of this pricing leverage: according to unconfirmed reports, cost per terabyte grew approximately 5% quarter over quarter in Q1 calendar year 2026, against a prior expectation of just 1%.

Cost-per-terabyte signal: According to unconfirmed reports, Morgan Stanley’s assessment flagged approximately 5% quarter-over-quarter growth in cost per terabyte during Q1 calendar year 2026, against an expected 1%. The firm materially raised both its per-terabyte pricing assumptions and gross margin forecasts following these results.

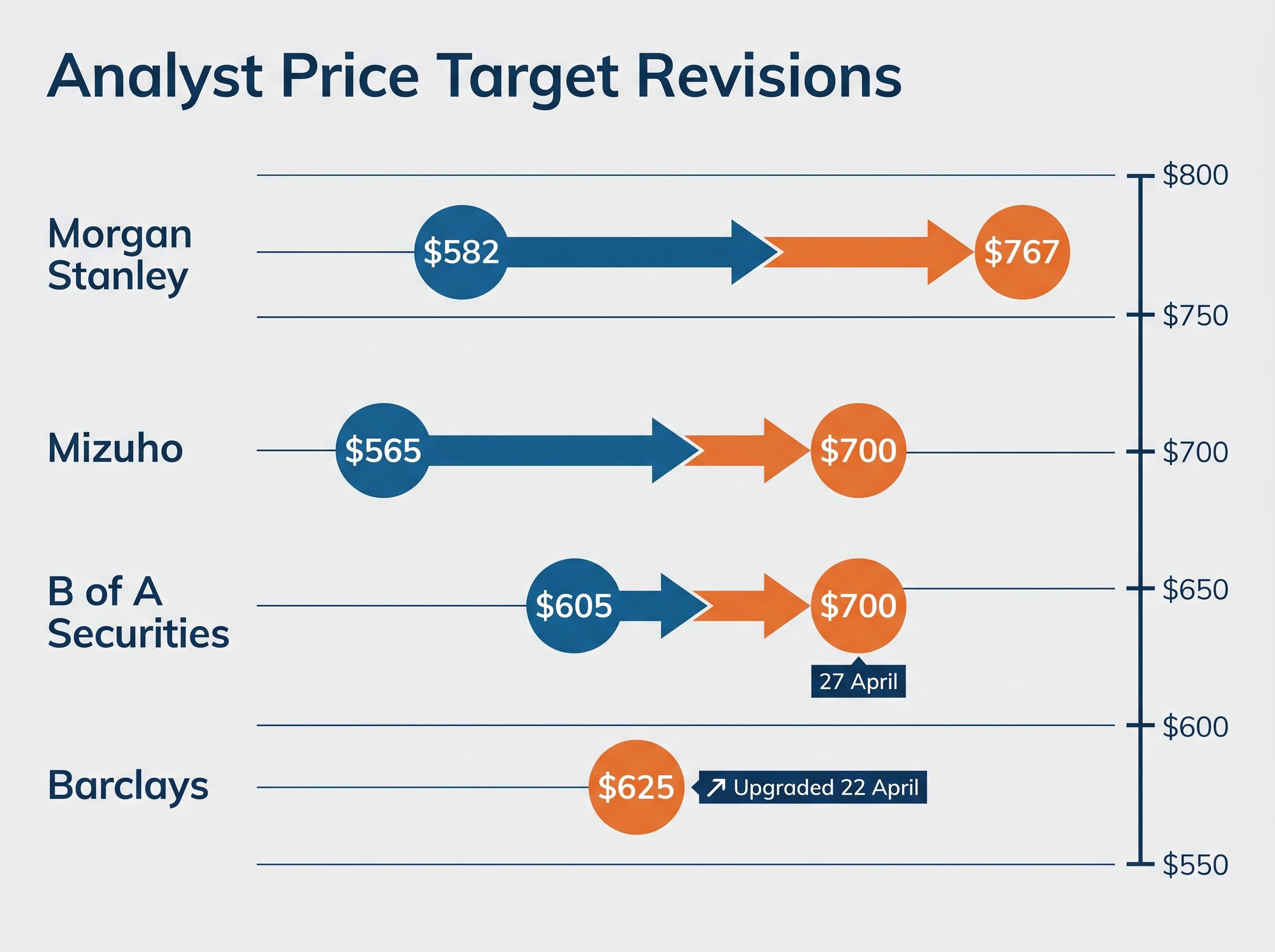

Two of the most closely watched names in IT hardware coverage responded to the quarter with substantial upward revisions.

According to unconfirmed reports, Morgan Stanley raised its price target to $767 from $582, maintained its Overweight rating, and designated Seagate as its top-ranked pick in IT Hardware. According to unconfirmed reports, the firm’s calendar year 2027 base case EPS estimate now sits at $42.59, which is 32% above its prior base case of $32.31 and 132% above the broader analyst consensus. According to unconfirmed reports, the target price is derived from an 18x multiple applied to that EPS estimate.

According to unconfirmed reports, Mizuho raised its price target to $700 from $565 and maintained its Outperform rating, citing the March quarter beat as the basis for the revision.

For pre-earnings context, B of A Securities had already set a $700 target (raised from $605 on 27 April), and Barclays upgraded the stock with a $625 target on 22 April.

| Firm | Prior Target | Revised Target | Rating | Key Detail |

|---|---|---|---|---|

| Mizuho | $565 | $700 | Outperform | Cited March quarter beat |

According to unconfirmed reports, Morgan Stanley noted that what had previously been the firm’s optimistic scenario has become the standard base case for three consecutive quarters. The bull-case valuation now stands at $1,131, based on a 22x multiple applied to an optimistic CY2027 EPS projection of $51.39.

According to unconfirmed reports, the 132% gap between Morgan Stanley’s base case and the broader consensus tells a pointed story: most of the Street has not yet caught up to what Seagate’s results are demonstrating about the HDD cycle’s durability.

The June quarter guidance of $3.45 billion in revenue and $5.00 in EPS does more than confirm the current trajectory. It suggests management’s confidence in the pricing and demand environment matches what the analyst upgrades imply.

Sequential guidance beats, when paired with the HDD pricing trends and margin expansion already discussed, look consistent with the structural supply-demand dynamic rather than a one-off. Morningstar framed the record gross margins as a structural, AI-driven development rather than a cyclical one, a distinction that matters for how long the current margin profile can persist.

The visibility provided by multi-year contracted infrastructure deals gives analysts greater confidence in modeling sustained revenue streams, a dynamic that typically commands a premium valuation multiple compared to transactional sales.

According to unconfirmed reports, Morgan Stanley’s observation that its above-consensus projections have been surpassed for three consecutive quarters adds weight to the forward view: the firm’s CY2027 base case EPS of $42.59 serves as a reference point for how far ahead of the consensus the actual earnings trajectory may be running.

Three variables will determine whether the current optimism is sustained:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Seagate’s Q3 results and the analyst reaction that followed represent a collective reassessment of how long and how deep the HDD demand cycle driven by AI infrastructure can run. This is not solely a company-specific earnings story; it is a signal about where the AI buildout is actually landing in terms of hard storage demand.

According to unconfirmed reports, the analyst consensus remains materially below Morgan Stanley’s estimates, with the 132% gap suggesting the repricing of expectations may not be complete. At the same time, the stock’s prior 618% twelve-month gain means a significant portion of the AI storage thesis is already reflected in the price. The gross margin figure of approximately 47% becomes the metric to watch in subsequent quarters: if it holds, it validates the structural pricing power thesis; if it compresses, it challenges it.

The next quarter’s results will either confirm that the new base case is durable or test whether the current optimism is running ahead of fundamentals.

For investors looking beyond traditional storage mediums to emerging semiconductor nodes, our deep-dive into AI memory constraints explores how new architectures are attempting to solve the energy bottlenecks inherent in massive data movement.

Seagate Technology stock surged over 16% after reporting Q3 FY2026 earnings and revenue that significantly beat Wall Street expectations, coupled with strong guidance for the upcoming quarter. This strong performance was driven by accelerating AI demand for cloud storage.

Seagate's current pricing power stems from three converging forces: expanding AI workloads driving data retention, HDDs capturing 80% of cloud storage procurement, and supply discipline maintained by the oligopolistic market structure of the HDD industry.

Morgan Stanley raised its price target for Seagate to $767 from $582 and designated it a top pick in IT Hardware, while Mizuho increased its target to $700 from $565, both citing the strong Q3 beat as the basis for their revisions.

Seagate's guidance for $3.45 billion in revenue and $5.00 in EPS for the June quarter implies management's strong confidence in the sustained demand and favorable pricing environment, consistent with a structural, AI-driven development in the HDD market rather than a one-off event.

Three key factors will determine sustained optimism: whether HDD cost-per-terabyte pricing growth holds, if hyperscaler capital expenditure commitments remain elevated, and if the broader analyst community begins to align with more aggressive EPS estimates.