Warsh Strips Fed Statement to 130 Words, Drops All Guidance

30 mins ago

JPMorgan cut its T-Mobile price target by $25 on 29 April 2026, and the stock remains on the bank’s highest-conviction equity list. That contradiction, a lower number paired with unshaken confidence, is the kind of signal that rewards closer reading. On the same day, T-Mobile reported Q1 2026 earnings per share of $2.27 against a $1.97 consensus estimate, a roughly 10.7% positive surprise that landed alongside accelerating subscriber growth and industry-leading service revenue. Meanwhile, Oppenheimer recently upgraded TMUS to Outperform with a $260 target, anchoring its thesis on artificial intelligence as a pricing and cost-efficiency catalyst. Two firms, two price targets, two different analytical angles, and one shared conclusion: T-Mobile stock has more room to run. What follows is a deconstruction of what these analyst calls mean together, what the Q1 beat adds to the picture, and whether the long-term growth projections justify current valuation for investors evaluating TMUS now.

A price target cut paired with an unchanged Overweight rating looks like a contradiction. It is not, once the mechanics are visible.

JPMorgan revised its TMUS price objective from $300 to $275 on 29 April 2026. The reduction reflects a valuation reset: the bank applied a 14.2x multiple to its estimated 2027 free cash flow per share to arrive at the new December 2026 target. The underlying business assessment did not change. JPMorgan retained TMUS on its U.S. Equity Analyst Focus List, a designation reserved for the bank’s highest-conviction picks among covered equities.

Valuation reset, not fundamental downgrade: JPMorgan’s target cut reflects multiple compression in the broader telecom sector rather than any deterioration in T-Mobile’s business quality or growth trajectory.

The valuation context makes the move legible. At the time of the report, TMUS traded at:

TMUS had fallen approximately 8% year-to-date against a S&P 500 that gained roughly 4.7% over the same period. That underperformance reflects macro and sentiment pressure on telecom multiples, not a deterioration in subscriber economics or cash generation. For investors, the distinction between a target cut driven by multiple compression versus one driven by weakening fundamentals is the difference between a potential entry point and a warning.

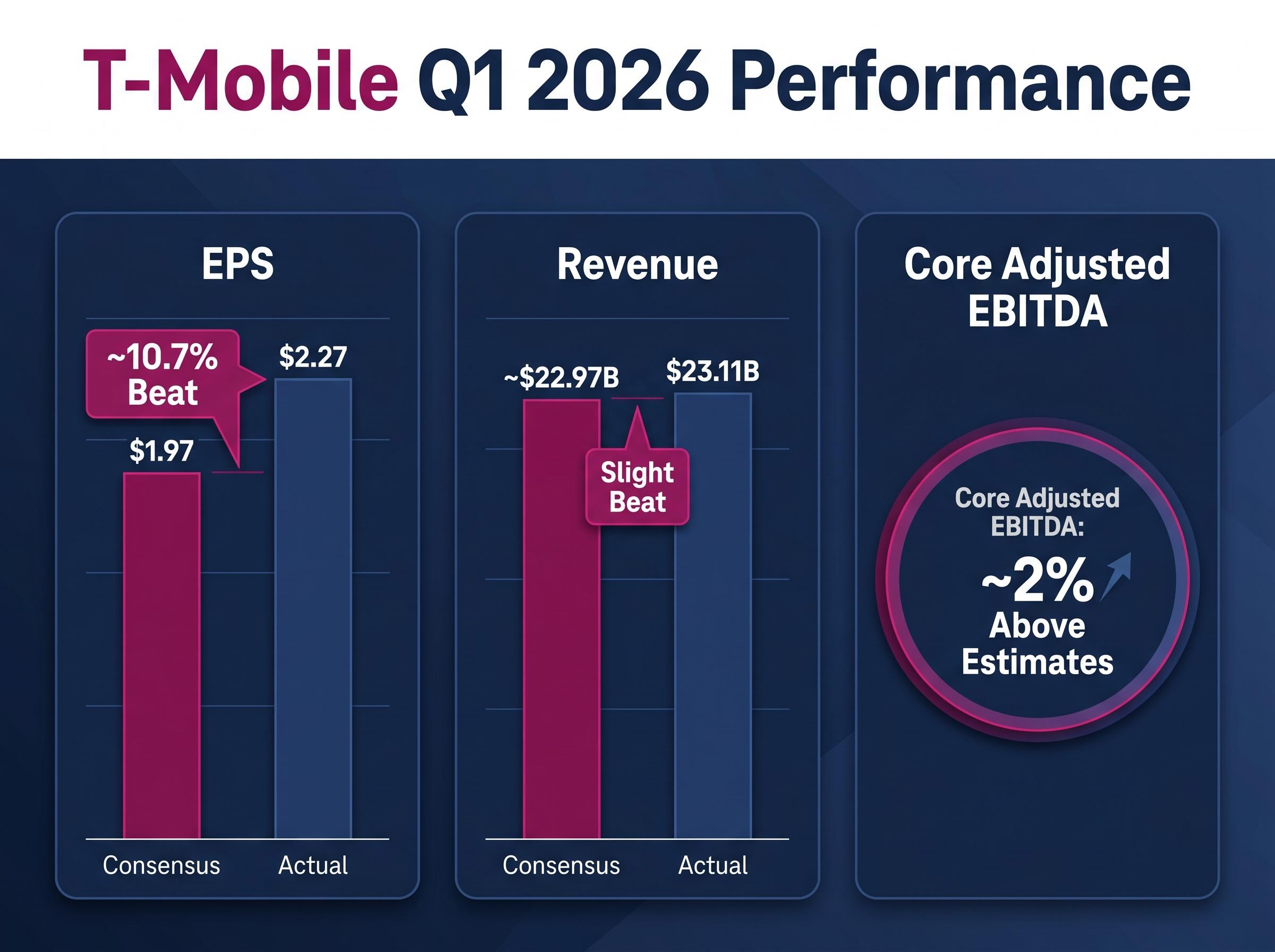

The numbers arrived first, and they were clear. T-Mobile reported Q1 2026 earnings per share of $2.27, beating the $1.97 consensus estimate by roughly 10.7%. Revenue came in at $23.11 billion, ahead of the approximately $22.97 billion consensus. Core adjusted EBITDA exceeded estimates by approximately 2%.

| Metric | Actual | Consensus/Guidance | Result |

|---|---|---|---|

| EPS | $2.27 | $1.97 | Beat (~10.7%) |

| Revenue | $23.11B | ~$22.97B | Beat |

| Core Adjusted EBITDA | ~2% above estimates | Consensus estimate | Beat |

The beat was not a one-line surprise. Postpaid account net adds accelerated, average revenue per account (ARPA) grew, and T-Mobile cited a record-high proportion of network-quality-driven switchers in the quarter.

A record share of customers switching to T-Mobile in Q1 2026 cited network quality as the primary reason, a competitive positioning signal that suggests the subscriber pipeline is strengthening on performance rather than promotional pricing alone.

JPMorgan’s own 2026 estimates sit above the midpoints of T-Mobile’s official guidance ranges. The bank projects approximately 1.035 million postpaid account net adds versus company guidance of 950,000-1,050,000, core adjusted EBITDA of $37.42 billion versus guidance of $37.1-$37.5 billion, and free cash flow of $18.43 billion versus guidance of $18.1-$18.7 billion. When a bank’s estimates sit above management’s own midpoints, it signals that Wall Street sees more in the business than the company is willing to formally commit to. That gap is a forward indicator worth monitoring.

The full-year guidance raise across all three tracked metrics, postpaid net additions, core adjusted EBITDA, and adjusted free cash flow, adds a second layer of conviction to the Q1 beat; management raising the ceiling, not just clearing it, signals that execution momentum is not viewed internally as a one-quarter event.

Price targets are outputs. The inputs, the multiples and cash flow estimates that produce them, are where the analytical substance lives. Understanding that architecture allows investors to evaluate future target revisions on their own terms rather than reacting to headlines.

The process follows three steps:

Telecom companies carry heavy depreciation charges on network infrastructure, and those non-cash charges distort GAAP earnings. A carrier spending billions on 5G towers records significant depreciation expense that reduces reported net income but does not affect the actual cash the business generates. Free cash flow (FCF) strips out that distortion and measures what the company can actually return to shareholders or reinvest.

EV/EBITDA (enterprise value to earnings before interest, taxes, depreciation and amortisation) serves a similar purpose. It captures the full value of the enterprise, including debt, and removes the effects of capital structure and depreciation policy. This makes it cleaner for comparing carriers with different balance sheet structures.

At the time of JPMorgan’s report, TMUS traded at 9.6x estimated 2027 free cash flow per share. The bank’s $275 target applies a 14.2x multiple to that same estimate. The spread between those two numbers, 9.6x versus 14.2x, is where the re-rating thesis lives.

If T-Mobile’s cash flow grows as projected and the multiple expands toward JPMorgan’s target level, the share price closes the gap to $275. Oppenheimer’s lower $260 target implies a more conservative multiple assumption but the same directional view: the stock is undervalued relative to its cash generation trajectory. Both frameworks point to the same conclusion through different arithmetic.

Oppenheimer upgraded TMUS from Perform to Outperform, setting a $260 price target and anchoring its thesis on a catalyst that JPMorgan’s valuation framework does not fully capture: artificial intelligence.

The upgrade identified three specific AI-driven opportunity areas for T-Mobile:

Oppenheimer framed AI not as a speculative future benefit but as a near-term operational catalyst, with pricing, cost, and service expansion pathways already taking shape through T-Mobile’s infrastructure partnerships.

The infrastructure mechanism behind that thesis became concrete on approximately 16-17 March 2026, when T-Mobile announced a partnership with Nvidia focused on AI-powered Radio Access Networks (AI-RAN) and physical AI deployment at network edge locations. AI-RAN integrates machine learning directly into the network’s radio layer, allowing dynamic spectrum allocation and capacity management that improves both performance and cost efficiency.

The NVIDIA and T-Mobile AI-RAN partnership announcement confirmed that machine learning integration into the radio access layer enables dynamic spectrum allocation, capacity management, and edge compute deployment, giving T-Mobile a differentiated infrastructure position that underpins the AI-driven cost and pricing thesis.

MoffettNathanson also cited the Nvidia partnership as a differentiator when upgrading TMUS, reinforcing that the AI thesis has traction beyond a single firm’s view. If AI materially improves T-Mobile’s pricing power and reduces operating costs, the 8% EBITDA compound annual growth rate (CAGR) projected through 2028 may prove conservative rather than aspirational.

Growth projections in isolation are abstract. Translated into cash generation and capital returns, they become concrete.

T-Mobile’s projected 8% core adjusted EBITDA CAGR and 12% FCF per share CAGR through 2028 rest on three specific drivers:

| Driver | Mechanism | Expected Impact |

|---|---|---|

| Subscriber gains | Growth in underpenetrated market segments and UScellular integration | Postpaid base expansion, higher service revenue |

| Pricing flexibility | ARPA growth on acquired customers, network-quality-driven switching | Revenue per account uplift without promotional dilution |

| Cost programme | $2.7 billion targeted cost reductions by 2027 | Margin expansion, FCF acceleration |

$2.7 billion in targeted cost reductions by 2027 provides investors with a measurable near-term checkpoint for whether management is on track to deliver the margin improvement embedded in long-term projections.

The company is already returning cash at scale. In Q1 2026, T-Mobile returned approximately $6.0 billion to shareholders through buybacks and dividends, with a quarterly dividend of $1.02 per share (approximately 2.1% annualised yield at current price levels).

Compounding FCF per share at 12% annually through 2028 while simultaneously returning billions in capital is the ownership thesis for long-term investors. The cost savings programme provides the nearest measurable test of execution: if the $2.7 billion target is on track by mid-2027, confidence in the broader growth trajectory strengthens materially.

JPMorgan and Oppenheimer agree on direction. Both rate TMUS as a buy. Both see material upside from current levels. Where they diverge is on the specific mechanism and magnitude of that upside: JPMorgan at $275 anchored on cash flow valuation, Oppenheimer at $260 anchored on AI as an operational catalyst.

| Firm | Rating | Price Target | Primary Thesis |

|---|---|---|---|

| JPMorgan | Overweight | $275 | FCF compounder, multiple re-rating from compressed levels |

| Oppenheimer | Outperform | $260 | AI-driven pricing, cost, and service expansion catalyst |

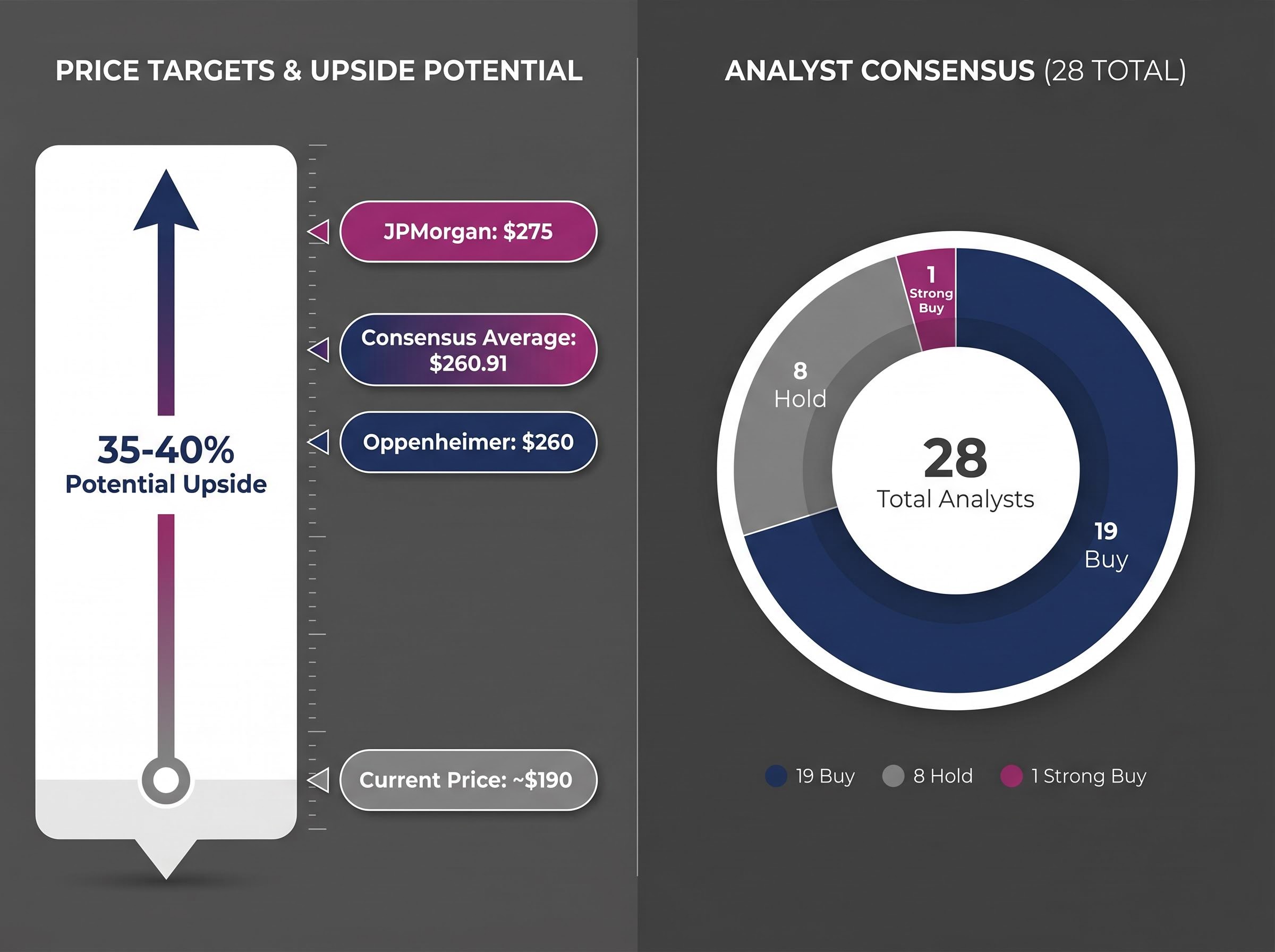

The broader consensus aligns. Across 28 analysts, the average price target sits at approximately $260.91, with 19 Buy ratings, 8 Hold ratings, and 1 Strong Buy. With TMUS trading at approximately $190 (pre-market 29 April 2026: $190.18), that consensus implies roughly 35-40% potential upside from current levels.

The bullish alignment does not eliminate risk. Three factors could challenge the thesis:

Insider activity adds a minor note of caution: approximately 694,000 shares were sold on a net basis over the past six months, though this figure has not been independently verified via SEC filings.

The SEC EDGAR filings for T-Mobile US include Form 4 insider transaction reports that provide the definitive record of share sales by directors and officers, allowing investors to independently verify any net selling activity cited in analyst or media summaries.

TMUS is a free cash flow compounder with an AI-driven upside layer, trading at a discount to analyst consensus targets following a year-to-date underperformance that appears to reflect macro and multiple pressure rather than any deterioration in the underlying business. The combination of a Q1 2026 earnings beat, raised guidance, and two independently bullish analyst calls from different analytical angles represents a more durable signal than any single dollar figure on a price target revision.

The forward test: Q2 2026 subscriber metrics and free cash flow trajectory will provide the first measurable checkpoint for whether T-Mobile’s raised guidance is achievable, and whether the re-rating thesis has traction beyond analyst conviction.

The variables to monitor from here are specific: Q2 2026 subscriber net adds, progress on the $2.7 billion cost programme, and any further AI monetisation announcements from the Nvidia partnership. Those data points will determine whether the gap between $190 and the consensus target begins to close.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

JPMorgan reduced its TMUS price target from $300 to $275 due to multiple compression across the broader telecom sector, not because of any deterioration in T-Mobile's business fundamentals. The bank retained TMUS on its U.S. Equity Analyst Focus List, its highest-conviction designation, signalling the cut was a valuation reset rather than a fundamental downgrade.

T-Mobile reported Q1 2026 earnings per share of $2.27, beating the $1.97 consensus estimate by approximately 10.7%, with revenue of $23.11 billion also ahead of expectations. The company also raised full-year guidance across postpaid net additions, core adjusted EBITDA, and adjusted free cash flow.

Oppenheimer upgraded TMUS to Outperform with a $260 target, arguing that artificial intelligence will improve T-Mobile's pricing precision, reduce per-subscriber operating costs, and open new revenue streams through edge compute and enterprise AI applications. The thesis was reinforced by T-Mobile's partnership with Nvidia focused on AI-powered Radio Access Networks announced in March 2026.

Telecom analysts typically use free cash flow multiples and EV/EBITDA rather than earnings multiples, because heavy depreciation on network infrastructure distorts GAAP earnings without affecting actual cash generation. JPMorgan applied a 14.2x multiple to its estimated 2027 free cash flow per share to arrive at its $275 price target for TMUS.

The three key risks are competitive pressure from AT&T and Verizon potentially slowing subscriber growth, execution risk on the $2.7 billion cost savings programme and AI-RAN deployment timeline, and the possibility that elevated interest rates or shifting risk appetite prevent the multiple re-rating from 9.6x to 14.2x FCF that underpins the bull case.