How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

6 hrs ago

Brent crude is sitting above $99 a barrel. Tanker traffic through the world’s most important oil chokepoint has collapsed by more than 95%. And as of 27 April 2026, Wall Street is barely moving. The S&P 500 is up 0.1%, the Dow and Nasdaq-100 are each down 0.1%, and the week’s dominant storyline is Wednesday’s earnings parade, not a live blockade that has disrupted more global oil supply than any event since the 1970s.

The disconnect is worth examining. The Iran conflict and the enforced closure of the Strait of Hormuz have been the defining energy market story of early 2026, yet the absence of fresh headlines this week has created a deceptive sense of stability. Markets are not pricing in resolution. They are pricing in stalemate, and that is a meaningfully different condition.

This piece explains what the Strait of Hormuz blockade actually is, why it has sent oil above $99 per barrel, how a fragile ceasefire and stalled diplomacy keep a major supply shock unresolved, and what U.S. investors need to understand about geopolitical risk when building or stress-testing a portfolio.

The numbers on screen look calm. They are not.

As of 1:45 p.m. EST on 27 April 2026, equity markets are barely registering the geopolitical backdrop:

One-third of S&P 500 and Nasdaq-100 components report earnings this week, which is absorbing the bulk of investor attention. Oil prices have registered minimal movement from Thursday through Monday, reinforcing the impression that the energy crisis has stabilised.

It has not. Brent at $99.60 is not stable; it is elevated. Prices surged to $108.20/bbl on 5 March 2026 when the blockade was confirmed, and they remain well above pre-crisis levels, sustained by shipping insurance premiums, rerouting costs, and the unresolved threat of further escalation. Analysts have flagged the potential for abrupt market swings from unexpected Persian Gulf developments. The absence of new headlines is not the same as the absence of risk. Stalemate carries its own tail-risk profile, and the week’s quiet screens are a holding pattern, not a signal of resolution.

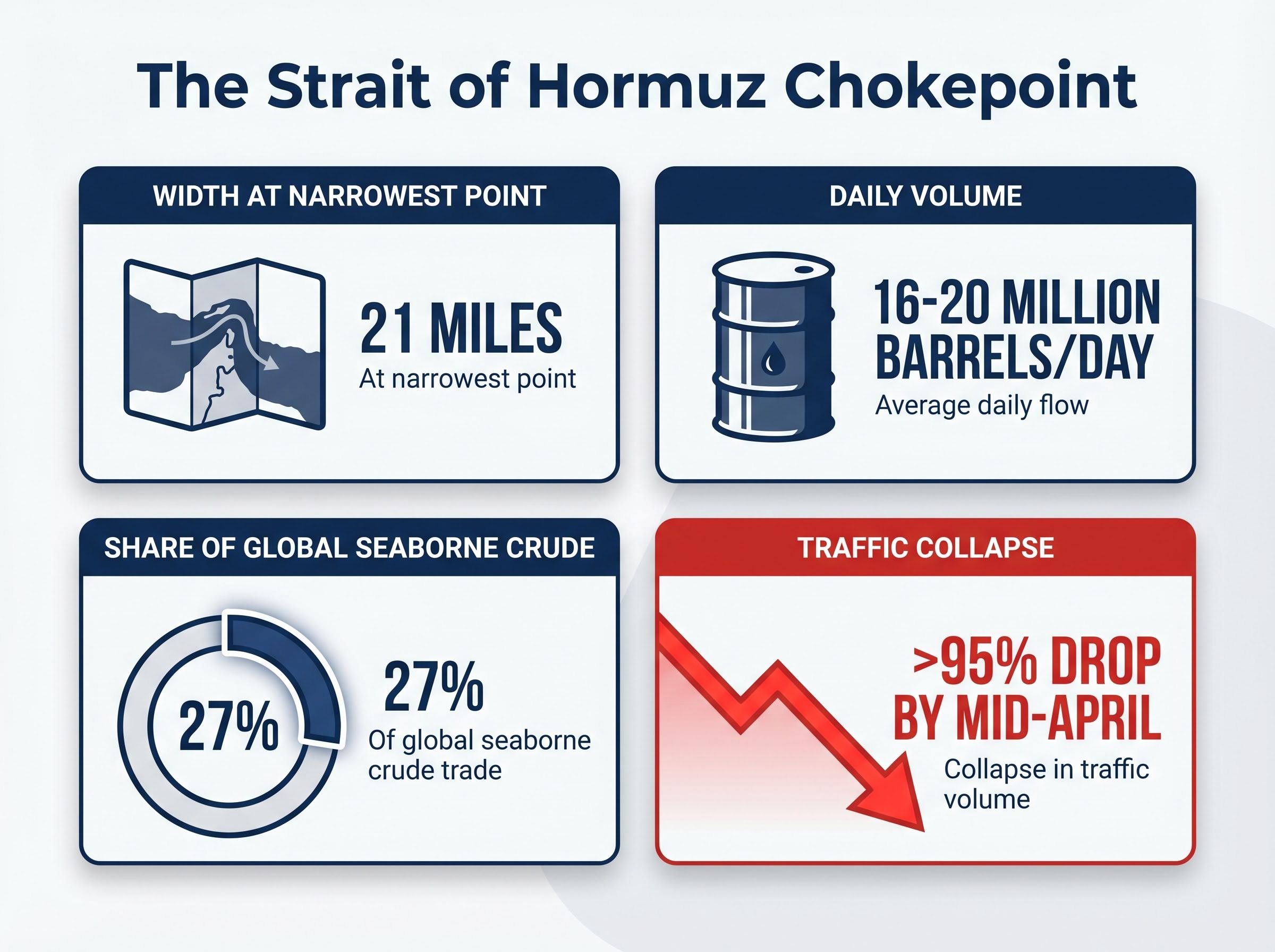

The Strait of Hormuz is the narrow waterway separating Iran from Oman at the mouth of the Persian Gulf. At its narrowest navigable point, it is approximately 21 miles wide. Every tanker carrying oil or liquefied natural gas (LNG) out of the Persian Gulf must pass through it.

The scale of what transits this passage is difficult to overstate.

| Commodity | Share of global seaborne trade via Hormuz | Daily volume estimate |

|---|---|---|

| Crude oil and petroleum products | 27% | 16-20 million barrels/day |

| LNG | 25-27% | Significant share of global supply to Asia and Europe |

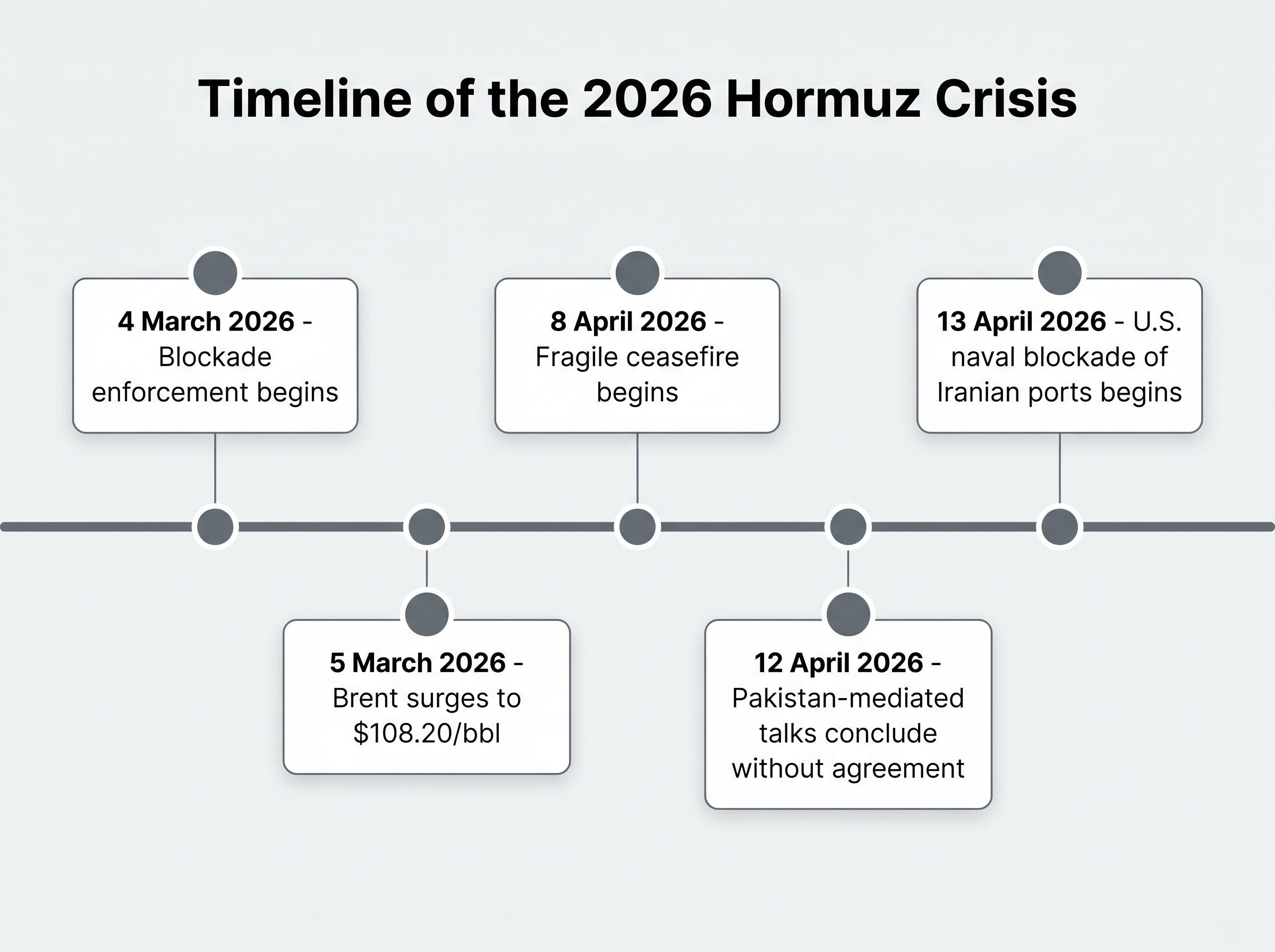

Roughly 20% of all global seaborne oil trade passes through this single corridor every day. When Iran began enforcing its closure on 4 March 2026, traffic collapsed by approximately 80% within the first week. By mid-April, the reduction exceeded 95%.

The EIA data on the Strait of Hormuz as a critical oil chokepoint confirms that approximately 20 million barrels per day flow through the passage, a volume equivalent to roughly 20% of global petroleum liquids consumption and a figure that explains why no alternative routing arrangement can absorb the shortfall at scale.

Iran’s enforcement methods include:

Alternative routes offer limited relief:

Even though the United States is now a net energy exporter, global oil is priced on global benchmarks. A disruption of this scale feeds directly into WTI pricing, inflation dynamics, and the earnings of energy-dependent U.S. companies. The Strait is not a regional concern; it is a global pricing bottleneck, and there is no adequate workaround.

A fragile ceasefire has held, nominally, since approximately 8 April 2026. It has now extended beyond its original two-week window, which would have expired around 22 April. No fresh military escalation has been confirmed since then, but the diplomatic architecture behind the ceasefire is threadbare.

Pakistan-mediated indirect talks between the United States and Iran concluded around 12 April 2026 without agreement. President Trump subsequently cancelled envoys’ planned trips, though Pakistan continues to push for continuation. The situation is best described as diplomacy stalled but not dead.

Iran’s latest Hormuz reopening proposal, submitted through Pakistani intermediaries on 27 April 2026, is conditioned on the U.S. lifting its port blockade before nuclear talks begin, a sequencing demand the Trump administration has resisted; the proposal triggered an emergency White House Situation Room meeting but has not produced a public response.

Iran has linked any reopening of the Strait to three specific conditions:

None of these conditions has been met. No second round of talks in Pakistan has materialised.

Prediction markets, including Polymarket, estimate approximately a 28-33% probability of Strait traffic normalisation by 30 April 2026. That figure reflects de-escalation signals and EU energy coordination discussions, but it also means markets are pricing in roughly a two-in-three chance that the blockade persists into May.

For investors, those three Iranian conditions represent the specific checklist markets are monitoring. A breakthrough on any of them could trigger a sharp oil price correction. The continued absence of progress on all three is the structural basis for the sustained risk premium priced into energy markets today.

The connection between a blocked waterway in the Persian Gulf and a higher fuel bill in Houston follows a sequential chain. Each link adds cost:

The cross-asset signals from the Hormuz standoff extend well beyond oil: when Brent surged past $106 on 24 April 2026 following a naval confrontation in the Strait, European equities fell harder than U.S. futures, the yen approached intervention territory, and the VIX climbed to 19.31, confirming that chokepoint risk transmits across currencies and equity benchmarks simultaneously.

Brent breached $108.20/bbl on 5 March 2026, immediately following confirmed blockade enforcement. The World Bank has noted approximately 20% oil price increases linked to the crisis. The Dallas Federal Reserve has flagged the disruption as among the most significant energy shocks in decades, drawing explicit comparisons to 1970s-era supply crises.

The geopolitical risk premium (GRP) is the portion of an oil price that reflects uncertainty and fear rather than the physical balance of barrels produced and barrels consumed. It is the market’s way of pricing in scenarios that have not happened yet but could.

This premium can deflate rapidly on ceasefire news or inflate sharply on escalation, making energy prices unusually volatile during active geopolitical crises. For investors evaluating whether current oil prices represent a temporary spike or a structural shift, the size and persistence of the GRP is the variable that matters most. If diplomacy succeeds, the premium compresses. If the blockade escalates, it widens further.

The 1973 Arab oil embargo is the historical benchmark most analysts reach for when calibrating the current crisis. The comparison is useful, but it understates what is happening in 2026.

Federal Reserve History’s account of the 1973-74 oil shock documents how the OAPEC embargo quadrupled global oil prices and contributed directly to a sustained global recession, providing the institutional baseline against which the scale and severity of the 2026 blockade can be measured.

| Dimension | 1973 oil embargo | 2026 Strait of Hormuz blockade |

|---|---|---|

| Supply removed from market | Approximately 6-7% of global oil supply | Approximately 20% of global seaborne oil trade |

| Mechanism of disruption | Producer embargo (political-commercial decision by OPEC nations) | Physical blockade of transit chokepoint (mines, USVs, missiles) |

| Geographic scope | Targeted specific importing nations | Blocks all traffic through a single global transit corridor |

| Resolution pathway | Diplomatic negotiation with producing nations | Requires both diplomatic agreement and physical demining of the Strait |

In 1973, the disruption was a political decision: producing nations chose to withhold supply, and the solution was a political agreement to resume it. In 2026, the disruption is physical. Even if Iran agreed tomorrow to reopen the Strait, the mines, USVs, and missile coverage would need to be cleared before commercial traffic could resume safely. The resolution pathway is longer and more complex by nature.

Analysts have characterised the 2026 crisis as a “paradigm shift” from the traditional model of naval deterrence to asymmetric siege warfare targeting global energy chokepoints. The Financial Express, Business Today, and the New York Times (March 2026) have each drawn explicit 1973 comparisons.

The 1973 embargo triggered a global recession. The 2026 blockade has disrupted a larger share of global supply through a harder-to-reverse mechanism. Historical context helps calibrate the magnitude of the risk, but the comparison should sharpen concern rather than provide reassurance.

The United States produces more oil than it consumes. That status does not insulate U.S. investors from the Strait of Hormuz crisis.

WTI crude is trading at approximately $98-99/bbl, reflecting its integration with Brent as a global benchmark. When Brent rises on a supply shock in the Persian Gulf, WTI follows. Domestic production insulates the physical economy from shortages but does not insulate portfolios from price effects.

The portfolio dimensions that merit monitoring include:

Two notable gaps in the current information environment reinforce the case for treating this as an ongoing, not resolved, risk factor: no confirmed deployment of the U.S. Strategic Petroleum Reserve (SPR) has been announced, and no clear endgame timeline exists for the diplomatic process. The uncertainty itself, independent of which direction the crisis resolves, warrants a portfolio stress-test.

Geopolitical tail risk is not a timing call. It is a structural consideration for portfolio construction, and the Strait of Hormuz blockade is its most concentrated current expression.

For investors wanting to map the specific sectors and instruments most exposed to a further escalation or sudden breakthrough, our dedicated guide to Strait of Hormuz portfolio exposure identifies the positions most at risk from headline-driven swings, including a detailed breakdown of why the combined SPR release and OPEC+ boost covers less than 2% of the estimated supply disruption.

Markets are quiet this week, but the underlying risk architecture has not changed. The Strait of Hormuz remains effectively closed. The ceasefire is holding but fragile. Diplomacy is stalled on three specific Iranian conditions, none of which has been met.

Three points are worth carrying forward. First, the Strait of Hormuz is an irreplaceable chokepoint whose disruption transmits directly into global oil prices regardless of U.S. domestic production levels. Second, the 2026 supply shock is historically significant, exceeding the 1973 oil embargo in scale and involving a harder-to-reverse physical mechanism. Third, diplomatic resolution requires a specific and demanding set of conditions to be satisfied, and the timeline for any of them remains unclear.

The week ahead may keep markets in holding-pattern mode as earnings dominate the news cycle. But the Strait situation means a single escalation or breakthrough could reprice energy assets sharply in either direction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding diplomatic outcomes and oil price movements are speculative and subject to change based on geopolitical developments.

The Strait of Hormuz blockade refers to Iran's enforced closure of the narrow waterway connecting the Persian Gulf to global shipping lanes, through which roughly 20% of all global seaborne oil trade passes every day. Because there is no adequate alternative route at scale, the blockade has driven Brent crude above $99 a barrel and represents one of the largest energy supply disruptions in decades.

Tanker traffic through the Strait of Hormuz collapsed by approximately 80% within the first week of Iran enforcing its closure on 4 March 2026, and by mid-April 2026 the reduction exceeded 95%, effectively shutting down the world's most critical oil chokepoint.

Iran has linked any reopening to three specific conditions: a cessation of Israeli operations against Hezbollah in Lebanon, the lifting of the U.S. naval blockade of Iranian ports, and a broader end to the wider conflict. As of 27 April 2026, none of these conditions has been met.

Analysts recommend monitoring energy sector equity exposure, inflation-hedging instruments such as TIPS and commodity allocations, and the margins of transport and airline companies, all of which are directly affected by elevated crude prices. Portfolio stress-testing is warranted given the absence of a confirmed SPR deployment and the lack of a clear diplomatic timeline.

The 2026 blockade is larger in scale, disrupting approximately 20% of global seaborne oil trade compared to the roughly 6-7% removed during the 1973 Arab oil embargo, and it involves a physical mechanism using mines, unmanned surface vehicles, and missiles that makes resolution harder to reverse than the political decision that ended the 1973 embargo.