Record Highs Are Not the Risk Most Investors Think They Are

5 hrs ago

U.S. stocks are sliding on Monday, 27 April 2026, caught between two forces that neither resolve quickly nor fade quietly. A weekend breakdown in U.S.-Iran diplomacy has pushed Brent crude back above $100 per barrel, and the Federal Reserve’s two-day policy meeting begins tomorrow. The Dow Jones Industrial Average is down 0.31% at 49,076.60, the S&P 500 is off roughly 0.2%, and the Nasdaq Composite trails by approximately 0.4%.

The numbers are modest. The message beneath them is not. An effectively closed Strait of Hormuz, persistent inflation pressure, and a central bank sitting on its hands have produced what analysts are describing as a “fog of war” market, one where investors are reluctant to commit in either direction.

What follows covers the two primary forces dragging on equities today, which sectors are absorbing the most damage, and the specific catalysts retail investors should watch through the end of this week as Big Tech earnings and the Fed statement add further moving parts.

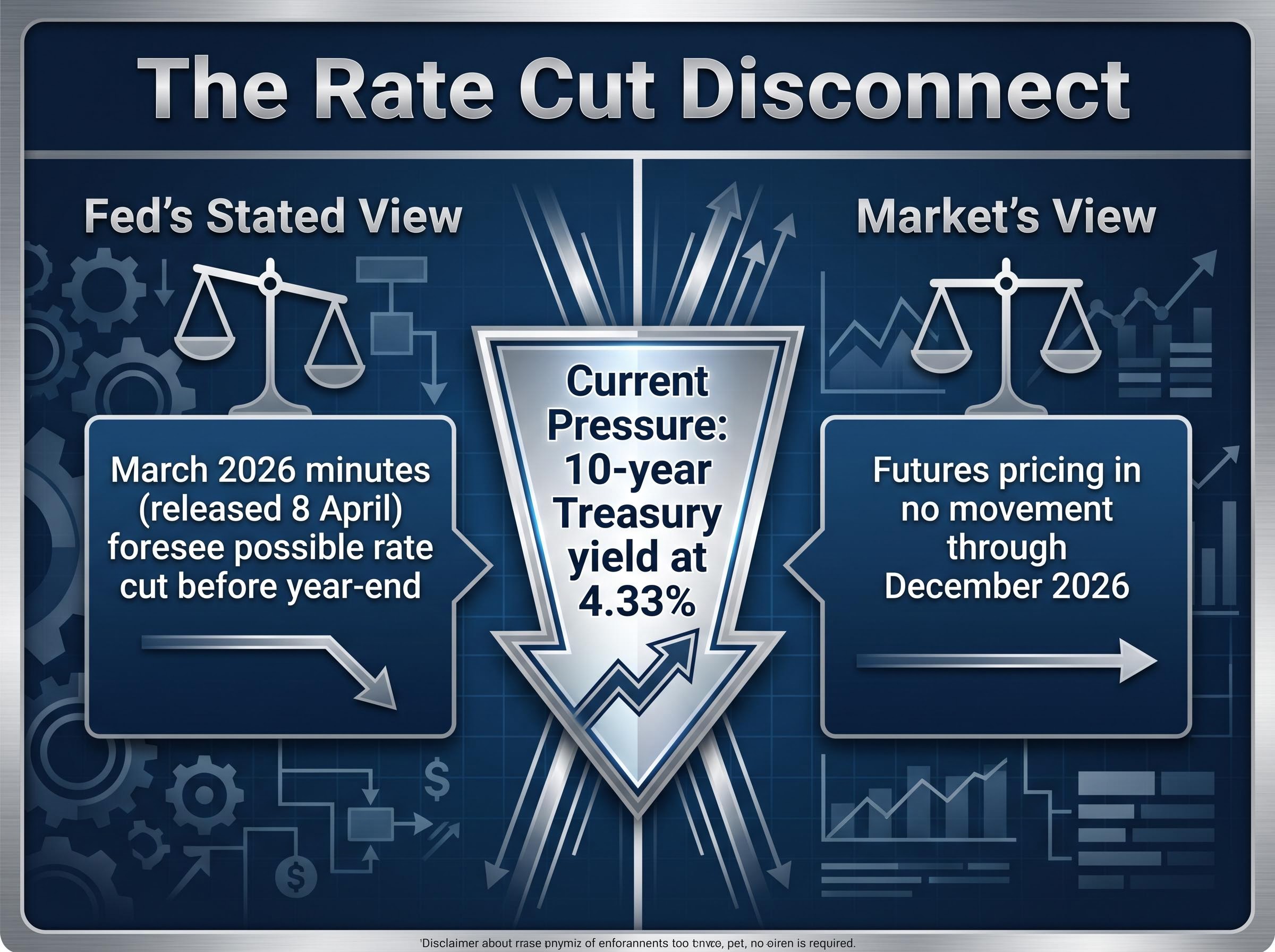

The Federal Open Market Committee convenes on 28-29 April 2026, and the consensus is near-unanimous: rates will not move. The federal funds rate is expected to remain on hold. In a normal cycle, that would make the meeting a non-event.

This is not a normal cycle. March 2026 Fed minutes, released on 8 April, showed officials still foreseeing a possible rate cut before year-end despite the war’s economic impact. Traders disagree. Futures markets are pricing in no movement through December 2026, betting that persistent energy-driven inflation gives the Fed no room to ease.

That gap between the Fed’s own stated outlook and what the market believes is where the tension sits. The 10-year Treasury yield at 4.33% is already doing the tightening work: raising mortgage costs, compressing corporate borrowing capacity, and pressuring equity valuations in growth-heavy sectors.

The Fed’s dual-mandate trap in a high-energy-cost environment is more constrained than the hold decision alone suggests: oil-driven inflation prevents rate cuts while rising unemployment and slowing growth argue against further tightening, leaving the central bank with no clean policy exit until energy prices move meaningfully in either direction.

The disconnect: Fed minutes from March still signal a possible 2026 rate cut. Traders are betting the opposite, pricing in no movement through year-end. Wednesday’s press conference will test which side is right.

In a high-uncertainty environment, Fed Chair Jerome Powell’s characterisation of inflation will carry more weight than the rate decision itself. If Powell frames current inflation as persistent and structurally reinforced by energy costs, it confirms the market’s hawkish read and could deepen the risk-off tone through the rest of the week.

Any softening of that language, any suggestion that the Fed sees oil-driven inflation as temporary rather than entrenched, could spark a relief rally. The words will move markets more than the hold.

Planned U.S.-Iran peace negotiations did not take place over the weekend. Iran had submitted a new proposal to reopen the Strait of Hormuz, explicitly decoupled from nuclear discussions, but no response materialised before markets opened on Monday. By mid-morning, Brent crude was trading between $100.56 and $102.17, and WTI crude sat at approximately $95.08.

The Strait of Hormuz remains effectively closed, with sparse shipping traffic. The waterway handles roughly one-fifth of global oil supply on a normal day; its continued closure is not a headline risk but a structural supply shock.

Key negotiation milestones tell the story of diminishing momentum:

Energy analysts at Macquarie have warned of potential crude spikes to $200 per barrel if Middle East tensions persist into summer, citing compounding risks to Persian Gulf supply routes.

For investors, the oil price is not a commodity-sector story in isolation. It is a multiplier on inflation, corporate margins, and consumer spending simultaneously.

The Brent-WTI spread as a real-time escalation gauge has widened to over nine dollars in recent sessions, signalling that geopolitical risk is concentrated specifically in Middle Eastern supply routes rather than reflecting North American production constraints, a distinction that matters for investors trying to separate structural energy inflation from tactical positioning opportunities.

United Airlines made the cost pressure tangible on 21 April 2026, cutting its full-year earnings guidance to $7-$11 per share, down from a previous range of $12-$14. The airline cited surging fuel costs driven directly by the ongoing Middle East conflict. On Monday, United shares were down approximately 2-3% intraday.

That guidance revision is a single company, but the mechanism it illustrates applies broadly. Elevated crude prices ripple outward through transportation surcharges, manufacturing input costs, and consumer goods pricing. The inflation pass-through channels include:

| Sector | Energy Cost Exposure | Primary Impact Channel | Key Example |

|---|---|---|---|

| Airlines | High (fuel is largest variable cost) | Direct jet fuel pricing | United Airlines EPS guidance cut |

| Manufacturing/Industrials | Moderate to high | Energy-intensive production processes | Rising factory input costs |

| Consumer Goods | Moderate | Packaging, transport, raw materials | Food and pharmaceutical cost inflation |

| Transportation/Logistics | High | Diesel and freight rate increases | Freight surcharges across supply chains |

Retail investors sometimes treat oil as a sector-specific story. At $100-plus Brent, it becomes a broad-market earnings problem. Understanding which sectors carry the most energy cost exposure helps in assessing where margin compression risk sits.

The energy price transmission into broader inflation is rarely a direct or immediate relationship; crude oil moves first into transportation and logistics costs, then into manufactured goods and food pricing over the following weeks, which is why a sustained $100-plus Brent environment creates inflation that proves structurally stickier than a single CPI print captures.

Apple, Meta, Microsoft, and Amazon are all trading lower on Monday, each down approximately 0.5-1% intraday. The declines are orderly, not panicked.

The reason is timing. All four companies are scheduled to report earnings this week, and investors are reducing exposure ahead of results rather than reacting to new fundamental deterioration. The Nasdaq’s 0.4% decline reflects this pre-earnings caution across the growth complex.

Not all tech is moving in the same direction. While mega-cap names drift lower, memory stocks are surging: Micron Technology is up approximately 5.02% and Sandisk is up approximately 7.05% on Monday, a reminder that sector-level generalisations miss stock-specific catalysts.

This week’s Big Tech earnings will function as a near-term test of whether AI-driven valuation premiums can hold up against higher borrowing costs, oil-driven inflation, and demand uncertainty. For investors with concentrated tech exposure, these reports carry as much directional weight as the Fed statement.

Today’s pullback reflects a market waiting for information, not reacting to confirmed bad news. The direction of the next meaningful move depends on which of three catalysts resolves first:

Market breadth reinforces the caution: a majority of S&P 500 constituents are trading lower intraday. Individual earnings misses are amplifying the tone; Domino’s Pizza fell approximately 9.49% after disappointing results, a reminder that stock-specific weakness compounds in a low-conviction environment.

Not every piece of incoming information changes the macro picture. A single-day index decline of less than 0.5% is not a directional signal. What would change the picture: Powell signalling that inflation is more persistent than the March minutes suggested; a tech earnings cycle where forward guidance collapses across multiple names; or a confirmed escalation (or de-escalation) in the Strait of Hormuz standoff.

The “fog of war” framing from analysts means uncertainty itself is the dominant condition. Investors who recognise that distinction are better positioned to respond to genuine new information rather than reacting to routine volatility.

Portfolio positioning in a high-uncertainty macro environment like the current one typically favours energy and safe-haven exposure while reducing duration risk in growth equities, though the more important discipline is maintaining a structured monitoring framework tied to specific data releases rather than reacting to daily geopolitical headlines that shift the narrative without changing the fundamental picture.

Two forces are pressing on U.S. equities today: stalled U.S.-Iran negotiations keeping Brent crude above $100, and a Fed meeting beginning tomorrow where the rate decision matters less than the language around it. The resulting pullback is modest in size but meaningful in what it signals, a market deliberately holding its breath.

29 April stands out as the week’s most important date, with the Fed statement and Powell’s press conference likely to set the tone heading into May. Big Tech earnings running in parallel will either reinforce or undermine the growth narrative that has supported equity valuations through months of geopolitical disruption.

Investors may find it useful to bookmark the key benchmarks: Brent crude levels, the 10-year yield at 4.33%, and the Fed’s characterisation of inflation persistence. These are the reference points against which this week’s incoming news will carry its meaning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

U.S. stocks are falling on April 27 2026 due to two converging pressures: a weekend breakdown in U.S.-Iran diplomacy that pushed Brent crude back above $100 per barrel, and investor caution ahead of the Federal Reserve's two-day policy meeting beginning April 28.

The Federal Open Market Committee meets April 28-29 2026, and while rates are expected to remain on hold, markets are closely watching Fed Chair Jerome Powell's language on inflation persistence, which analysts say will carry more directional weight than the rate decision itself.

The Strait of Hormuz handles roughly one-fifth of global oil supply on a normal day, so its continued closure acts as a structural supply shock that elevates crude prices, drives inflation higher, compresses corporate margins, and pressures equity valuations across multiple sectors simultaneously.

Airlines, transportation and logistics, manufacturing, and consumer goods companies face the greatest earnings pressure from elevated crude prices, with United Airlines already cutting its full-year EPS guidance from $12-$14 to $7-$11 per share, citing surging fuel costs tied to the Middle East conflict.

The three key catalysts this week are the Fed statement and Powell press conference on April 29, Big Tech earnings from Apple, Meta, Microsoft, and Amazon, and any diplomatic developments regarding the Strait of Hormuz reopening, any of which could shift the market's direction meaningfully.