UniCredit’s 8.72% Generali Stake Defies Orcel’s Denials

34 mins ago

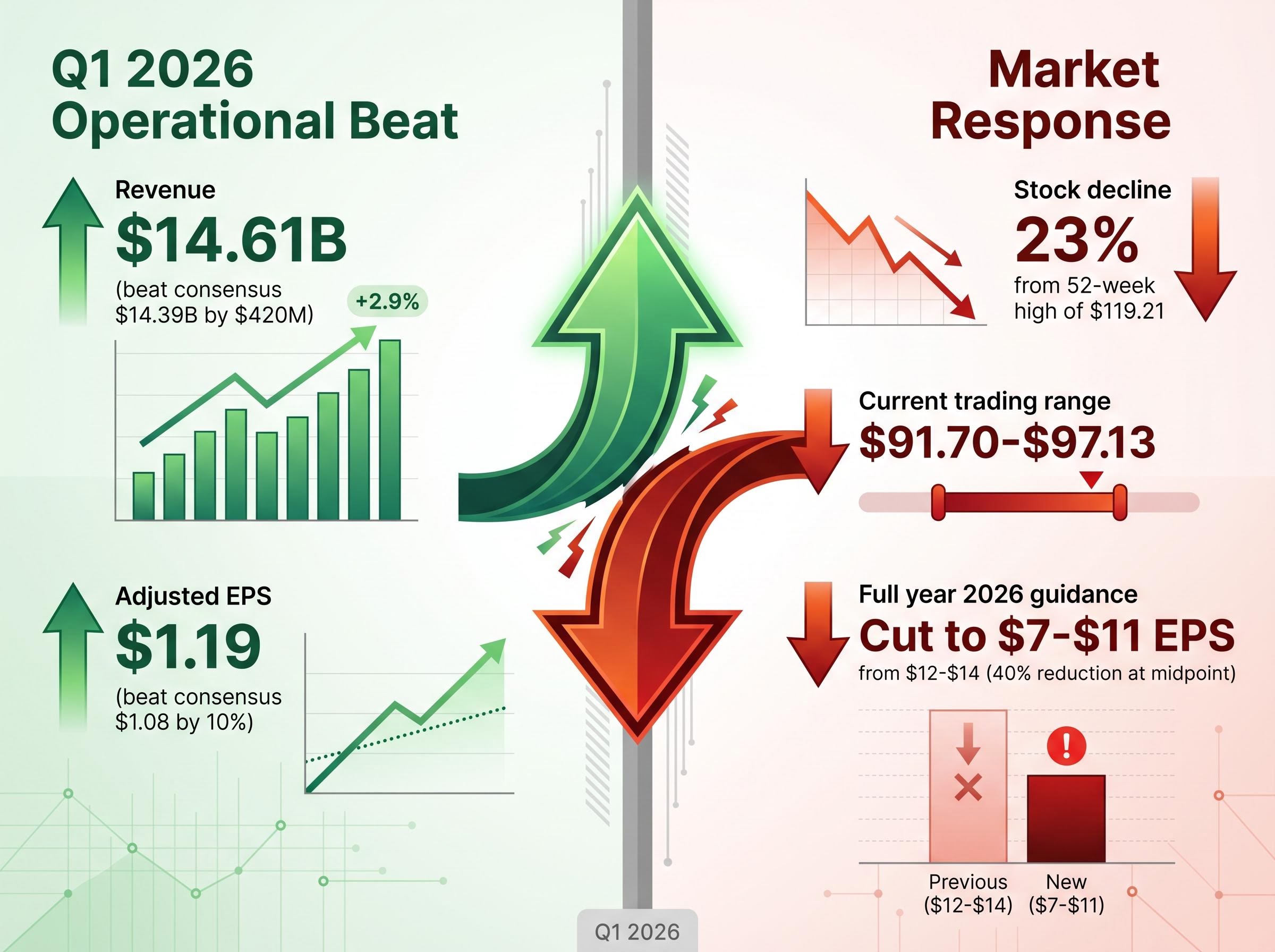

United Airlines delivered record first quarter revenue of $14.61 billion and beat earnings estimates by 10%, yet its stock promptly fell 7% and now trades 23% below its January high. The disconnect between operational excellence and stock weakness stems from a single variable: jet fuel. Middle East tensions sent crude prices surging past $128 per barrel in early April, forcing United to slash its full year earnings guidance by nearly 40%. For investors evaluating whether this selloff represents opportunity or warning, the answer hinges on fuel price trajectory, margin sustainability, and competitive positioning.

This analysis examines whether United’s current valuation adequately prices the fuel headwind, what scenarios could drive recovery or further decline, and how the carrier compares to rivals navigating the same crisis.

United Airlines reported adjusted earnings per share of $1.19 for the first quarter of 2026, beating the Wall Street consensus of $1.08 by 10%. Revenue climbed 10.6% year over year to $14.61 billion, exceeding analyst expectations of $14.39 billion by $420 million. Passenger revenue grew 11% as capacity expanded only 3.4%, driving total revenue per available seat mile up 6.9%.

The operational beat was real. Yet the market looked past it entirely.

The guidance revision told a different story. United cut its full year 2026 earnings forecast to a range of $7 to $11 per share, down from the prior $12 to $14 range issued in January. The reduction, roughly 40% at the midpoint, reflected a $340 million year-over-year increase in fuel costs during the first quarter alone. For the second quarter, management projected earnings of $1.00 to $2.00 per share based on jet fuel averaging $4.30 per gallon, a price level that fundamentally reshapes airline economics.

The guidance suspension patterns during fuel volatility seen across global carriers in March 2026, including Air New Zealand’s complete withdrawal of FY2026 targets when fuel costs doubled, demonstrate that United’s 40% guidance cut represents disciplined risk communication compared to competitors who opted to abandon forward visibility entirely.

The United Airlines Form 10-Q filing for Q1 2026 provides the audited financial statements underlying these results, including detailed disclosures on fuel cost variance, capacity adjustments, and management’s discussion of the guidance revision rationale.

| Metric | Q1 2026 Actual | Consensus Estimate | Variance |

|---|---|---|---|

| Revenue | $14.61 billion | $14.39 billion | +$420 million |

| Adjusted EPS | $1.19 | $1.08 | +10% |

| Fuel Cost Increase (YoY) | $340 million | N/A | N/A |

Guidance Revision Impact Full year 2026 adjusted EPS guidance cut from $12 to $14 to $7 to $11, representing a nearly 40% reduction at the midpoint.

The stock fell 1.8% on 21 April following the earnings release, then dropped a further 6.09% in premarket trading on 22 April. By late April, United shares traded in the $91.70 to $97.13 range, down 23% from the 52-week high of $119.21. For airline equity investors, forward guidance drives valuation, not backward results. The paradox was complete: United proved it could execute operationally, yet the market repriced the stock as if execution no longer mattered.

Fuel now consumes 45% of United’s operating costs, up from the usual 25%. That shift alone explains why a company beating earnings saw its stock collapse.

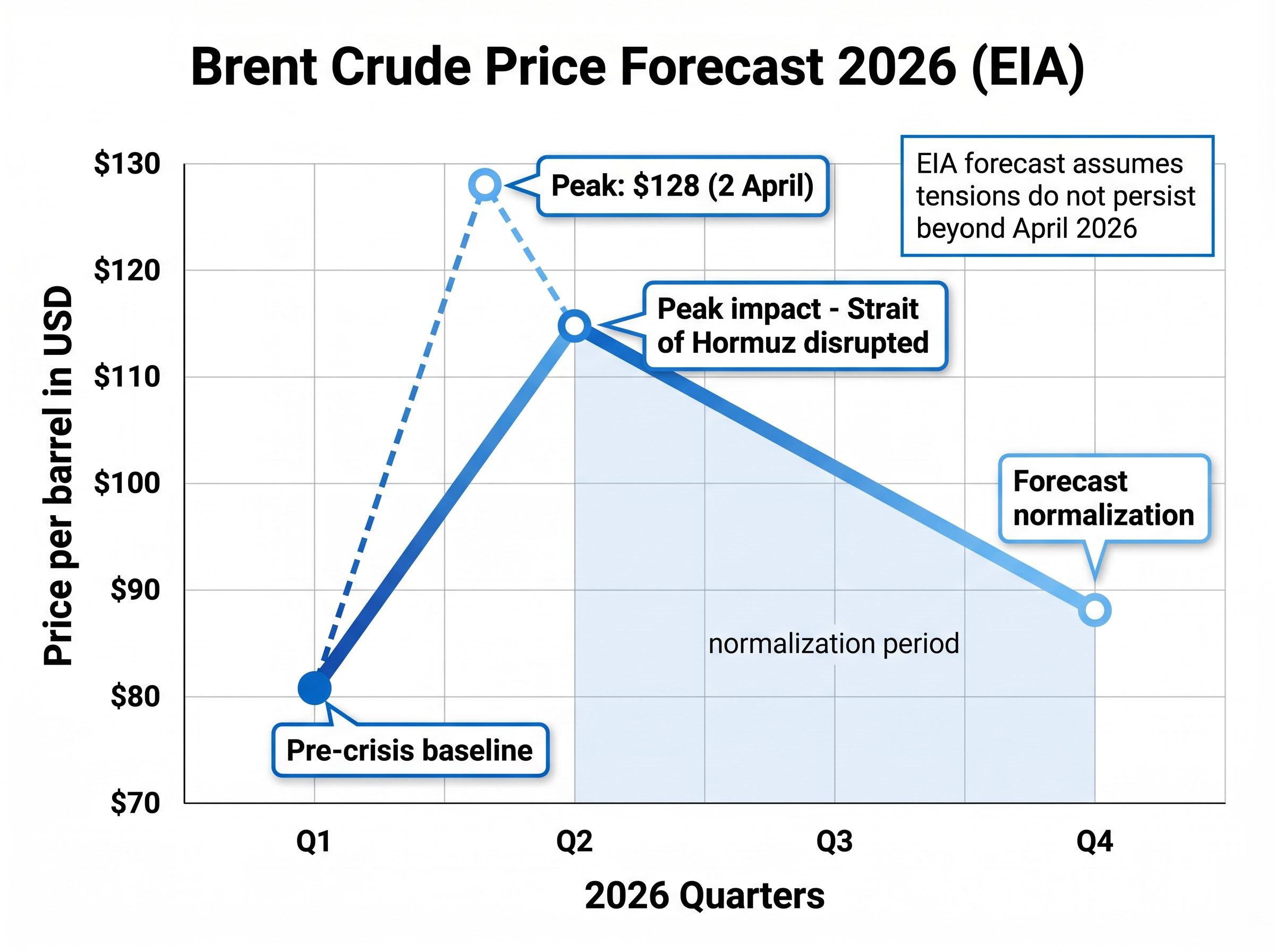

The supply shock began with the intensification of U.S.-Israeli tensions with Iran in early April 2026. Brent crude peaked near $128 per barrel on 2 April as the Strait of Hormuz, which handles approximately one-fifth of global seaborne oil trade, effectively closed. OPEC crude output collapsed by 7.56 million barrels per day in March, a 25% monthly decline that brought total production to 22 million barrels daily. Iraq’s output plunged by 2.76 million barrels per day to just 1.63 million, Saudi Arabia dropped by 2.07 million barrels daily to 8.36 million, and the United Arab Emirates fell by 1.44 million barrels daily.

The Strait of Hormuz closure mechanics explain how a single chokepoint carrying 20 million barrels daily can trigger supply shocks of sufficient magnitude to push crude past $128 per barrel, a price level at which airline operating economics fundamentally break down regardless of hedging strategies.

Average Jet A fuel in the United States reached $8.63 per gallon in April 2026, up $2.03 year over year. When translated to per-barrel pricing, jet fuel surged from approximately $85 to $90 per barrel in early 2026 to $150 to $200 per barrel in recent weeks. For context, the 1973 Arab oil embargo caused smaller absolute disruptions; the March 2026 collapse surpassed it in scale, though non-OPEC production capacity today limits the percentage impact on global supply.

The March 2026 collapse in OPEC crude output represented the greatest global energy security challenge in history according to the International Energy Agency, surpassing even the 1973 Arab oil embargo in absolute barrel reductions despite non-OPEC production capacity limiting the percentage impact on global supply.

The Energy Information Administration’s April 2026 Short-Term Energy Outlook forecasts that Brent crude will average:

EIA Q4 Forecast Brent crude oil is forecast to moderate to an average of $88 per barrel by the fourth quarter of 2026, assuming Middle East tensions do not persist beyond April 2026.

This trajectory means United faces steeper fuel headwinds in the current quarter before achieving relief in the second half of the year. The investment question is whether that relief arrives as forecast, or whether geopolitical developments invalidate the EIA’s de-escalation assumption.

The EIA Short-Term Energy Outlook forecast for Q4 2026 projects Brent crude averaging $88 per barrel, assuming Middle East tensions subside and Strait of Hormuz traffic gradually resumes, a trajectory that would provide United with meaningful cost relief in the second half of the year.

United Airlines stock traded in the $90 to $97 range in late April 2026, 23% below the 52-week high of $119.21. Based on the revised 2026 earnings guidance midpoint of $9 per share, the stock trades at approximately 10x to 11x forward earnings, a multiple substantially below historical norms for the carrier during profitable periods.

The analyst community maintains an overwhelmingly constructive view despite the guidance cut. The average Wall Street price target stands at $131.19, implying 35% upside from current levels. Of the eighteen analysts covering the stock, sixteen assign Buy ratings, one rates it Strong Buy, and only one maintains a Hold rating. No analysts rate the stock as Sell.

| Analyst Firm | Rating | Price Target |

|---|---|---|

| Morgan Stanley | Overweight | $150 |

| Barclays | Overweight | $150 |

| Wells Fargo | Overweight | $130 |

| Bank of America | Buy | $130 |

| TD Cowen | Buy | $120 |

Morgan Stanley’s Ravi Shanker upgraded United to Overweight with a $150 price target following the earnings release, arguing that first-quarter results demonstrated the underlying strength of the airline’s premium revenue strategy and that current valuation levels provide excessive compensation for near-term fuel cost pressures that will likely prove temporary. Barclays reiterated its Overweight rating and $150 target, noting that United’s P/E ratio of 9.58x with a market capitalisation of $31.5 billion reflects investor pessimism that may prove excessive if fuel prices moderate as the EIA forecasts.

The valuation debate hinges on a single variable: whether crude oil and jet fuel prices follow the EIA’s forecast trajectory or remain elevated longer than markets currently expect.

Delta Air Lines reported first-quarter 2026 revenue of $14.2 billion and earnings per share of $0.64, both slightly exceeding Wall Street expectations. The carrier disclosed a $2 billion fuel headwind on a full-year basis but indicated that its in-house refinery operations would offset a meaningful portion of these increased costs, providing Delta with a structural advantage that competitors lacking refinery assets cannot replicate.

Southwest Airlines reported first-quarter 2026 adjusted earnings of $0.45 per share, substantially below the consensus estimate of $1.19, representing a significant miss that reflected the low-cost carrier’s operational challenges in the face of elevated fuel costs and its lower-margin business model centred on point-to-point service with limited premium revenue opportunities. For the second quarter, Southwest guided to earnings of $0.35 to $0.65 per share, well below the $0.60 consensus, signaling that fuel costs would further pressure profitability.

United’s capacity reduction strategy, which offsets approximately five percentage points of previously planned growth for the remainder of 2026, positions the carrier to preserve margins through yield management rather than volume expansion. This tactical discipline, combined with United’s premium revenue focus, differentiates the carrier from Southwest’s volume-driven model and competes on roughly equal footing with Delta despite lacking refinery assets.

| Carrier | Q1 2026 Revenue | Q1 2026 EPS | 2026 Outlook |

|---|---|---|---|

| United Airlines | $14.61 billion | $1.19 (beat) | $7 to $11 EPS guidance |

| Delta Air Lines | $14.2 billion | $0.64 (beat) | $2B fuel headwind, refinery offset |

| Southwest Airlines | N/A | $0.45 (miss) | Q2 guidance $0.35 to $0.65 |

For investors considering airline sector exposure, United’s premium revenue strategy and debt reduction progress position the carrier as competitively advantaged relative to Southwest’s margin compression, whilst Delta’s refinery operations provide a structural hedge that United lacks. The choice among carriers depends on risk tolerance and recovery timing expectations.

The investment decision on United Airlines stock maps directly to expectations for fuel price trajectory. Three scenarios frame the range of outcomes.

Energy Secretary Commentary U.S. Energy Secretary Chris Wright stated that gasoline prices likely peaked in late April 2026, suggesting markets had begun pricing in expectations of reduced geopolitical tensions.

Polymarket contracts tracking the probability of WTI crude oil reaching $160 per barrel by 30 April 2026 showed declining odds to just 15% by late April, indicating that traders had begun pricing in de-escalation scenarios rather than further escalation. This shift in sentiment supports the base case over the downside case, though geopolitical events remain inherently unpredictable.

Investors monitoring United Airlines stock through the remainder of 2026 should track four catalysts that will clarify the investment thesis:

Real-time monitoring of tanker traffic through the Strait of Hormuz provides the most granular leading indicator of supply normalisation, with commercial shipping activity serving as a direct measure of whether diplomatic de-escalation translates into restored petroleum flows or remains limited to political rhetoric without operational impact.

United Airlines presents a fuel shock paradox: a competitively advantaged franchise with record revenue and disciplined execution, trading at a material discount to historical multiples and analyst targets, yet facing genuine near-term earnings uncertainty tied to geopolitical variables beyond management’s control.

The investment decision ultimately hinges on time horizon and fuel price conviction. Investors confident in the EIA’s forecast for Q4 moderation to $88 Brent may view current levels as attractive accumulation points for 12 to 24 month positions. Those requiring near-term earnings visibility or doubting de-escalation timelines may prefer waiting for Q2 results before committing capital.

The 35% gap between current price and average analyst target of $131.19 suggests meaningful upside if fuel normalises as forecast. However, the unusually wide guidance range of $7 to $11 signals that even management lacks confidence in precise outcomes. Position sizing and entry timing should reflect that uncertainty, with investors considering scaled entry strategies rather than concentrated positions until fuel price trajectory becomes clearer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

United Airlines beat Q1 2026 earnings estimates by 10% and reported record revenue of $14.61 billion, but the stock fell because management cut full-year 2026 EPS guidance by nearly 40%, from a range of $12 to $14 down to $7 to $11, driven by a $340 million year-over-year surge in fuel costs.

Of the eighteen analysts covering United Airlines, sixteen rate it a Buy and one rates it Strong Buy, with an average price target of $131.19, implying approximately 35% upside from the late April 2026 trading range of $91.70 to $97.13.

Jet fuel now accounts for approximately 45% of United Airlines operating costs, up from the usual 25%, meaning that elevated crude prices driven by Middle East supply disruptions can wipe out earnings gains from strong revenue performance and capacity discipline.

United beat Q1 estimates and is cutting capacity to protect margins, Delta has a structural advantage through its in-house refinery operations that offset some fuel cost increases, and Southwest missed Q1 estimates significantly and guided Q2 earnings well below consensus, reflecting the greater vulnerability of its low-margin business model.

In the base case, if Brent crude moderates to $88 per barrel by Q4 2026 as the EIA forecasts, the stock could re-rate toward $115 to $120; in the upside case, rapid diplomatic de-escalation could push the stock toward analyst targets of $130 to $150; and in the downside case, if tensions persist and crude stays above $115 per barrel, the stock could test the $80 to $85 range.