SEC Moves to End Mandatory Quarterly Reporting After 50 Years

17 hrs ago

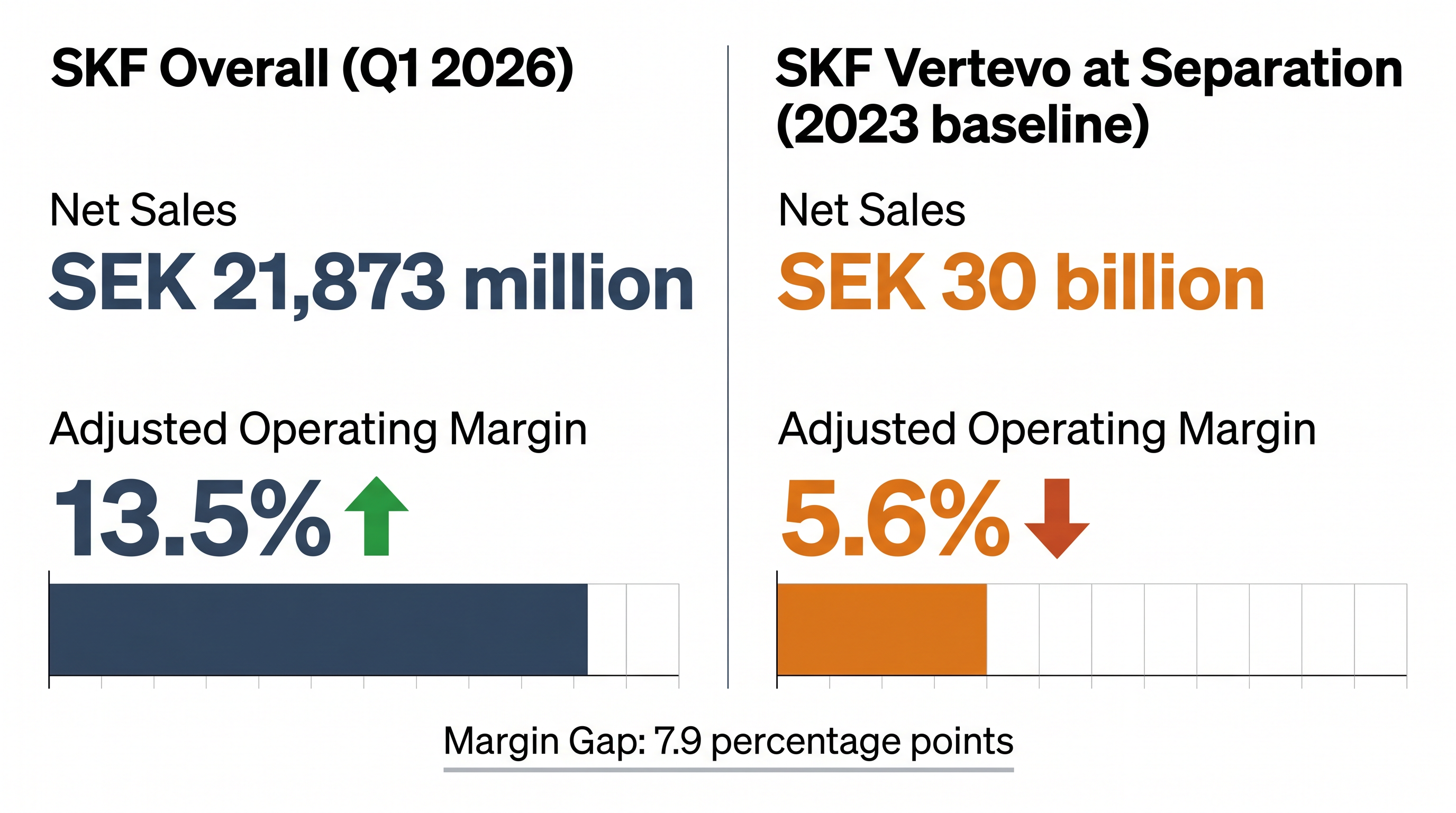

SKF named its automotive spin-off SKF Vertevo in February 2026, setting a Q4 2026 target for the separation that has already shifted twice since the initial September 2024 announcement. The entity will inherit SEK 30 billion in 2023 sales but also a comparatively modest 5.6% adjusted operating margin, a divergence that has split sophisticated analysts into opposing camps. What follows is an examination of whether this separation creates or destroys value, what the analyst divide reveals about the underlying business, and what investors and industry observers should watch as the separation unfolds.

The strategic logic centres on distinct market dynamics. SKF’s Industrial segment operates in stable, high-margin markets with predictable replacement cycles and long-term infrastructure demand. The Automotive segment faces volatile OEM production schedules, electrification-driven technical disruption, and pricing pressure from tier-one suppliers consolidating purchasing power. These divergences show up in the numbers. SKF reported Q1 2026 total net sales of SEK 21,873 million with a 13.5% adjusted operating margin, but the 2.4% organic growth came entirely from the Industrial side. Automotive offset those gains.

“The separation will enable enhanced focus on distinct end markets, improved growth prospects, greater operational efficiency, and increased competitiveness through specialised strategies.”

SKF positions the split around four claimed benefits:

The question is whether these claimed advantages offset the scale disadvantage and profitability gap that RBC Capital flagged in April 2026.

RBC Capital downgraded SKF in April 2026, calling the spin-off a mistake. The firm’s critique argues the separation creates a small, low-profit standalone entity without the scale or margin profile to compete effectively. RBC’s position builds on concerns about scale and profitability in the automotive bearing market. The separation, in RBC’s view, formalises underperformance rather than correcting it.

The divergence is not academic. It represents the core investment debate: whether SKF Vertevo’s positioning in a high-growth EV bearing market can overcome scale and margin headwinds, or whether the entity enters independence structurally disadvantaged.

The Goldman Sachs downgrade from Buy to Sell in April 2026 reflected broader institutional concern about the separation’s viability, with J.P. Morgan and RBC Capital issuing concurrent downgrades within the same week.

| Analyst | Rating | Key Concern | View on Separation |

|---|---|---|---|

| RBC Capital | Downgrade | Small, low-profit entity lacking scale | Separation formalises underperformance |

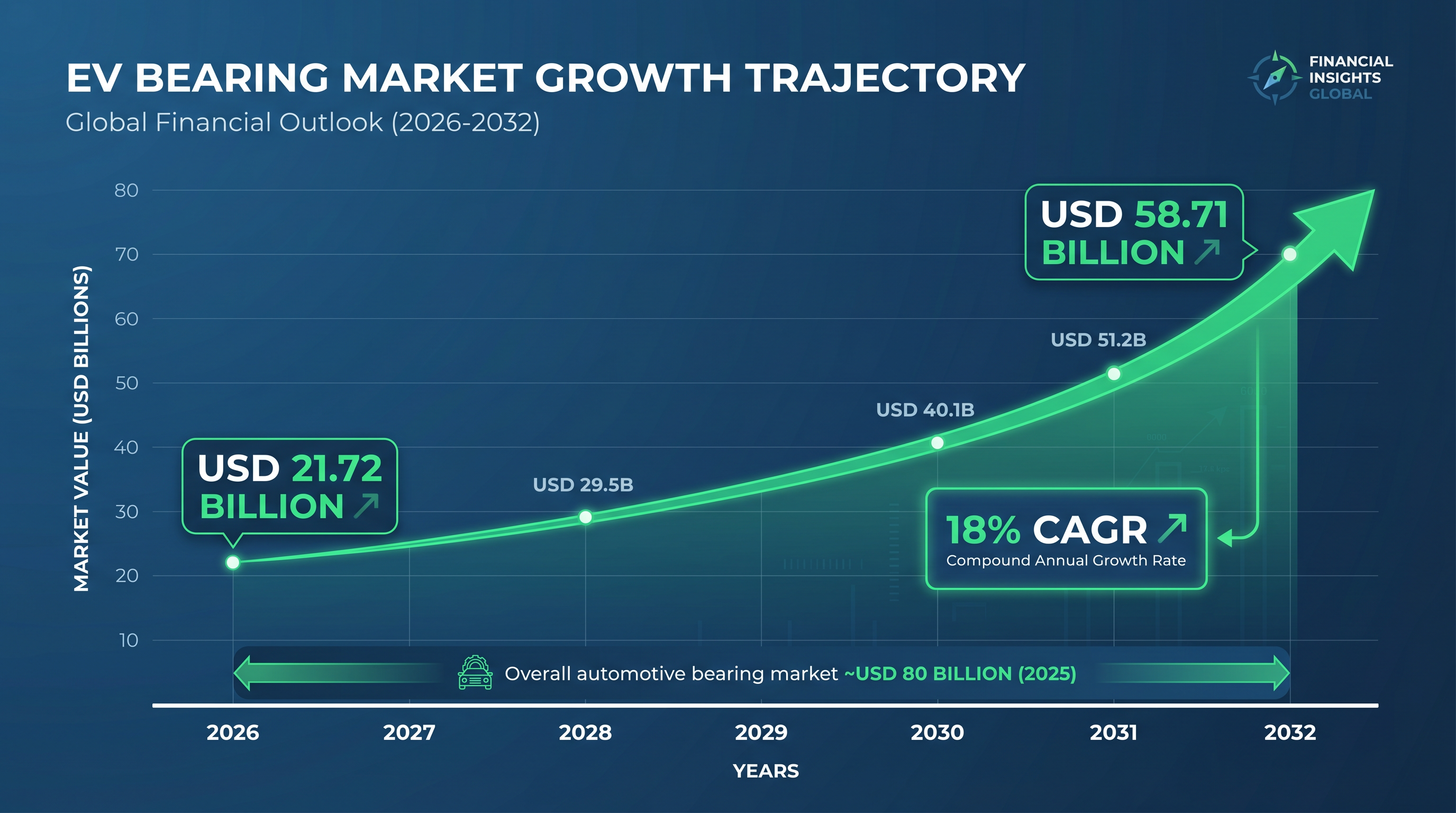

The EV bearing segment was valued at USD 21.72 billion in 2026 and is projected to reach USD 58.71 billion by 2032, a compound annual growth rate of 18%. This growth trajectory represents the single largest structural opportunity for automotive bearing suppliers since the shift from plain to rolling element bearings in the mid-20th century. The overall automotive bearing market is approaching USD 80 billion by 2025, with momentum continuing into 2026.

Four market drivers underpin this expansion:

The oil price dynamics driving EV adoption create secondary demand effects for component suppliers like SKF Vertevo, as sustained crude prices above $95 per barrel accelerate OEM electrification timelines and battery supply chain investments.

The EV bearing segment is projected to grow at an 18% CAGR from 2026 to 2032, reaching USD 58.71 billion.

SKF Vertevo inherits positioning in this market, but the growth trajectory poses both opportunity and risk. The 18% CAGR reflects sector-wide expansion, not guaranteed market share. SKF Vertevo’s ability to capture this growth depends on whether its R&D pipeline, customer relationships, and technical capabilities align with where the market is heading. The competitive landscape will determine whether a focused, smaller entity can outmanoeuvre larger rivals or gets compressed by scale advantages elsewhere.

Tesla’s Q1 2026 production and delivery trajectory serves as a leading indicator for automotive bearing suppliers, with the company’s shift toward AI infrastructure investment creating uncertainty about near-term drivetrain component volumes.

SKF chose a tax-exempt Lex Asea distribution mechanism for the separation. This Swedish legal framework allows SKF to distribute SKF Vertevo shares to existing shareholders without triggering a taxable event at the corporate level. For shareholders, the distribution preserves capital efficiency compared to a taxable dividend or cash buyback.

The Lex Asea distribution mechanism for tax-exempt share distributions allows Swedish parent companies to distribute subsidiary shares to existing shareholders without triggering corporate-level taxation, a framework codified in Swedish tax law that has governed spin-offs of major industrial entities since the 1990s.

Shareholders should expect the following sequence as the Q4 2026 target approaches:

Current institutional ownership stands at approximately 45%, with short interest remaining under 1%. The low short interest suggests limited speculative positioning against the separation, though it also reflects the measured uncertainty around the outcome.

Spin-offs historically create value when the separated entity gains strategic clarity, attracts a more suitable investor base, or escapes capital allocation constraints within the parent structure. They destroy value when the separated entity lacks scale, faces margin pressure without parental support, or competes in declining markets. SKF Vertevo’s outcome depends on which pattern dominates.

A meta-analysis of 26 spin-off event studies finding significantly positive average abnormal returns concluded that value creation is most pronounced when separated entities improve industrial focus and achieve sufficient scale, two conditions that frame the central debate around SKF Vertevo’s prospects.

Schaeffler restructured its e-mobility division in 2025, creating a focused unit to navigate the transition from internal combustion components to EV drivetrains. The restructuring acknowledged that legacy automotive suppliers face bifurcated demand: declining volumes in traditional powertrains, rising volumes in electric mobility. Schaeffler’s response was specialisation within the corporate structure rather than full separation.

Timken divested non-core assets in 2024, streamlining operations to focus on high-load bearing applications where the company holds technical advantages. The divestitures reflected a broader industry trend: suppliers exiting commoditised segments to concentrate resources on differentiated product lines.

Both cases illustrate the strategic logic SKF cites. Whether SKF Vertevo achieves similar outcomes depends on execution, market positioning, and the ability to improve margins over time.

SKF Vertevo enters independence facing established rivals with distinct competitive advantages. Schaeffler leads in integrated solutions, combining bearings with transmission systems and electronic controls. This systems-level approach appeals to OEMs seeking to consolidate suppliers and reduce integration complexity. Schaeffler’s post-2025 e-mobility division restructuring sharpened this focus.

NTN emphasises lightweight bearing designs, positioning for efficiency-focused applications where mass reduction directly improves vehicle range. This positioning aligns with OEM priorities in EV development, where every kilogram removed extends battery performance.

NSK leads the roller bearings segment, with a projected CAGR of 5.8% to 2032. The company’s reputation centres on reliability in high-stress applications, a competitive advantage in commercial vehicle and heavy-duty segments where bearing failure carries operational and safety consequences.

Timken’s post-2024 streamlined operations focus on high-load applications, leveraging decades of metallurgical and tribological expertise in tapered roller bearings. The company’s positioning targets industrial and commercial vehicle segments where load capacity and durability outweigh cost sensitivity.

Commercial vehicle electrification forecasts, including targets for 1,600-plus electric truck fleet deployments by FY29, represent a secondary growth channel for bearing suppliers beyond passenger EV volumes, with heavy-duty applications requiring specialized high-load bearing designs.

| Company | Primary Strength | Strategic Focus | EV Positioning |

|---|---|---|---|

| Schaeffler | Integrated solutions | Systems-level offerings combining bearings, transmissions, electronics | Dedicated e-mobility division post-2025 restructuring |

| NTN | Lightweight designs | Mass reduction for efficiency gains | Efficiency-focused applications in EV drivetrains |

| NSK | Reliability in roller bearings | High-stress commercial and heavy-duty segments | 5.8% CAGR to 2032 in roller bearings |

| Timken | High-load capacity | Tapered roller bearings for industrial and commercial vehicles | Post-2024 streamlined operations targeting durability-focused segments |

SKF Vertevo claims competitive advantages in four areas:

The scale concern RBC raised centres on whether these claimed advantages offset the competitive realities. Schaeffler’s systems-level integration, NTN’s lightweight specialisation, NSK’s reliability reputation, and Timken’s high-load expertise represent entrenched positions built over decades. SKF Vertevo’s ability to compete depends on whether technical performance and innovation translate into customer wins and margin expansion.

The Q4 2026 timeline, while twice delayed, remains the operative target. Four milestones will signal whether the separation proceeds successfully or encounters obstacles:

Financial metrics to monitor include SKF Vertevo’s margin trajectory relative to the 5.6% adjusted operating margin inherited from the Automotive segment. The market will watch for margin improvements from product mix shifts toward higher-value EV components and facility optimisation.

Operational developments to watch include customer announcements, R&D milestones in EV-specific bearing technologies, and capacity expansions aligned with the 18% CAGR in the EV bearing segment. The April 2026 consolidation of manufacturing footprint in the Americas serves as a preparation indicator, suggesting SKF is positioning for operational independence.

Investor sentiment leans toward cautious optimism, with recognition of strategic logic tempered by execution risk and broader market volatility.

The Q1 2026 earnings context provides a baseline. SKF reported EPS of USD 0.46, beating consensus of USD 0.38 by USD 0.09. The earnings beat reflected Industrial segment strength rather than Automotive turnaround, reinforcing the divergence that justified the separation in the first place.

SKF Vertevo enters a high-growth EV bearing market projected to reach USD 58.71 billion by 2032, with structural tailwinds from electrification, regulatory pressure, and sustainability mandates. The entity also faces legitimate questions about scale, profitability, and execution that divide sophisticated analysts. RBC Capital’s downgrade reflects scepticism that a small, low-profit entity can compete against larger rivals with entrenched positions.

The Q4 2026 timeline, while twice delayed, remains the operative target. Upcoming board and shareholder decisions serve as the next critical checkpoints. Readers should monitor the specific milestones outlined and assess their own risk tolerance for a spin-off where the bull and bear cases both rest on credible arguments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

SKF Vertevo is the name given to SKF's automotive division, which is being separated from the parent company to allow each business to pursue distinct strategies. SKF's Industrial segment operates in high-margin, stable markets, while the Automotive segment faces EV disruption and pricing pressure, making a combined structure increasingly difficult to manage effectively.

The separation is currently targeting Q4 2026 for completion, though this date has already been delayed twice since the initial announcement in September 2024. Key milestones include a board proposal, shareholder vote, regulatory approvals from Nasdaq Stockholm, and the eventual distribution of SKF Vertevo shares to existing SKF shareholders.

SKF is using a Lex Asea distribution mechanism, a Swedish legal framework that allows the parent company to distribute subsidiary shares to existing shareholders on a pro-rata basis without triggering a taxable event at the corporate level. Shareholders of record on a specified date will receive SKF Vertevo shares directly.

RBC Capital downgraded SKF in April 2026, arguing that the separation creates a small, low-profit standalone entity that lacks the scale or margin profile to compete effectively against larger rivals such as Schaeffler, NTN, NSK, and Timken. RBC's view is that the spin-off formalises underperformance rather than correcting it.

The EV bearing segment was valued at USD 21.72 billion in 2026 and is projected to reach USD 58.71 billion by 2032, representing an 18% compound annual growth rate. This growth is driven by the shift to electric drivetrains, regulatory pressure on OEMs, and demand for lightweight, high-speed, low-noise bearing solutions.