Trump Signs Preliminary Iran Deal, Stocks Rally and Oil Falls

3 hrs ago

Zixin Group Holdings delivered full-year FY26 revenue at 104% of analyst forecast and profit after tax at 123% of forecast, prompting Phillip Securities Research to raise its target price on the same day results landed. The Singapore-listed sweet potato company reported against a backdrop of rising agricultural input costs and ambitious expansion targets, making the beat particularly notable for investors tracking this niche agricultural small-cap. What follows unpacks what the FY26 numbers show, which segments drove outperformance, what the upgraded analyst target implies, and what risks remain before committing capital.

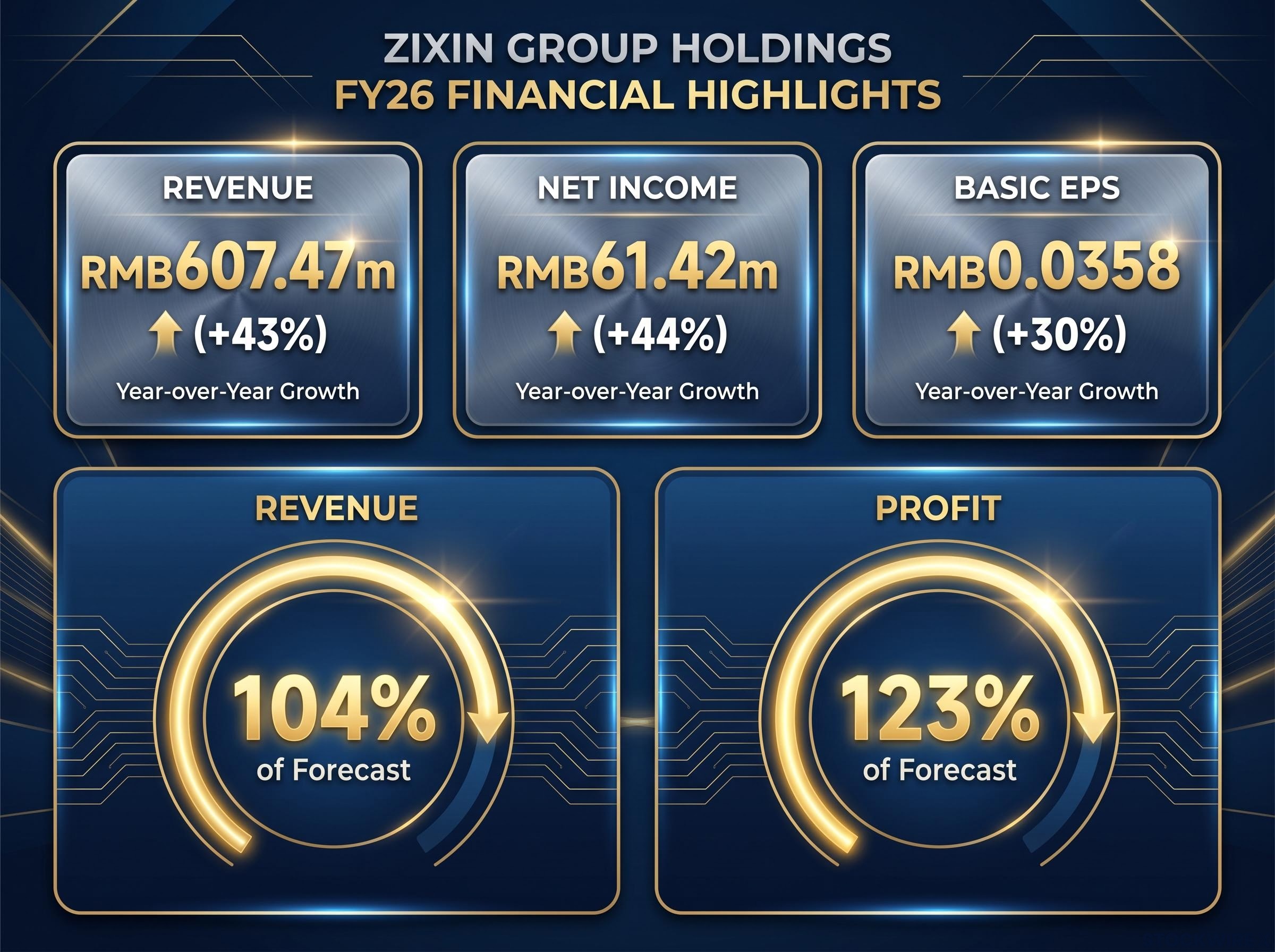

The scale of the beat is the headline. Full-year revenue reached 104% of the prior Phillip Securities forecast, while profit after tax landed at 123% of forecast, a 23-percentage-point overshoot on the bottom line.

Full-year profit after tax landed at 123% of analyst forecast, with revenue reaching 104% of forecast.

The second half of FY26 carried the weight. At the halfway mark, the company had delivered only approximately 41% of forecast revenue and approximately 29% of forecast net profit. That meant 2H FY26 needed to make up substantial ground, and it did: implied 2H revenue came in at RMB386.8m, up 44.3% year-on-year, with implied 2H net income of RMB45.4m, up 29.9%.

Growth was volume-driven rather than margin expansion. Gross margin compressed from 33.2% in 1H FY25 to 30.2% in 1H FY26, reflecting higher raw sweet potato input costs and new-capacity ramp expenses. Operating leverage from scale, rather than pricing power, lifted profitability.

| Metric | FY26 | FY25 | Change |

|---|---|---|---|

| Revenue | RMB607.47m | RMB424.68m | +43% |

| Net income | RMB61.42m | RMB42.72m | +44% |

| Basic EPS (continuing operations) | RMB0.0358 | RMB0.0275 | +30% |

When the bottom line lands 23 percentage points above forecast, it signals that operating leverage is running ahead of analyst models, the kind of data point that drives upward forecast revisions.

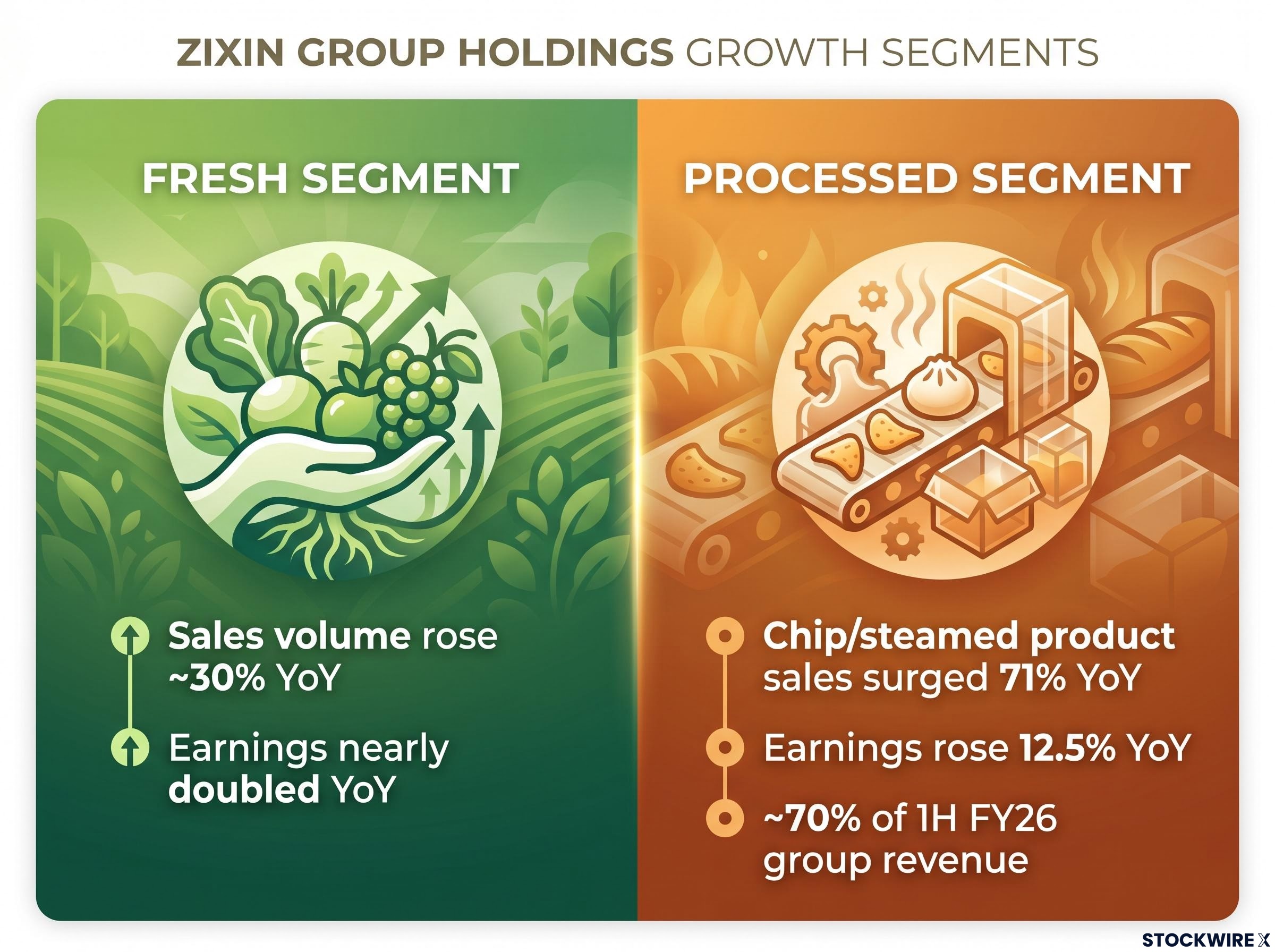

Outperformance was not concentrated in one division. Both segments contributed, but through different mechanisms, which makes the result feel more durable.

The contrast matters. The fresh segment grew through raw volume, powered by warehouse infrastructure improvements. The processed segment grew through product-mix expansion and white-label manufacturing. Two levers, not one, which is relevant to how investors should assess downside scenarios. A company with multiple growth drivers tends to carry more resilient earnings profiles than one reliant on a single revenue source.

Zixin operates a vertically integrated sweet potato value chain across four segments:

The processed segment operates an ODM (original design manufacturer) model, where Zixin manufactures products under other brands’ labels. This reduces the company’s own marketing spend requirements but creates customer concentration risk, as revenue depends on a limited number of large buyers maintaining their order volumes.

Small-cap management quality carries extra weight in businesses where a single leadership team controls both farming-side procurement decisions and processed-product customer relationships, because the same people setting input cost contracts are also managing the ODM buyer concentration risk.

The smart warehouse technology referenced in the fresh segment is not a minor operational detail. It directly supports the margin narrative by reducing spoilage and improving the proportion of harvested product that reaches paying customers.

Phillip Securities Research reaffirmed its BUY rating and raised its target price to S$0.06 on 18 June 2026, the same day FY26 results landed. This was not a minor model tweak. The broker revised its FY27 revenue forecast upward by 23% and its FY27 net profit forecast upward by 29%, with FY27 earnings growth now estimated at approximately 24% year-on-year.

The SGX Catalist continuing obligations framework governs how Singapore-listed companies must disclose material financial results and price-sensitive information, which means Zixin’s same-day analyst target upgrade and result announcement both sit within a tightly regulated disclosure environment that investors can reference for timing and completeness standards.

At the revised S$0.06 target, Phillip Securities is implying approximately 88% to 100% upside from the current share price range of S$0.030 to S$0.032.

Phillip identified two primary catalysts: continued expansion of the white-label ODM business and sustained demand for premium sweet potato varieties. Management’s own FY27 internal targets align directionally, targeting approximately 60% revenue growth in the fresh segment and approximately 30% in processed products, though these are ambitious figures on an already elevated base.

Zixin is not a lone-analyst story. KGI Securities also covers the stock with an OUTPERFORM rating and a target price of S$0.048, based primarily on ramp-up of the functional food line and expansion outside China.

| Analyst | Rating | Target Price | Key Catalyst |

|---|---|---|---|

| Phillip Securities | BUY | S$0.06 | White-label ODM expansion; premium variety demand |

| KGI Securities | OUTPERFORM | S$0.048 | Functional food ramp-up; international expansion |

A 29% upward revision to the net profit forecast reflects a genuine reassessment of the company’s earnings trajectory and signals that prior models were materially underestimating operating leverage.

The FY26 beat and analyst upgrade paint a compelling headline. The risk profile beneath it requires equal scrutiny.

Fertiliser supply disruption running through the Strait of Hormuz closure has already pushed urea and phosphate prices higher across global agricultural supply chains, and Chinese sweet potato cultivation, which relies on nitrogen-based inputs, is not insulated from those upstream cost pressures.

The analyst upgrade and strong results make a compelling case, but the concentration of both operations and customers in China, combined with a small float, means downside scenarios can move fast.

Zixin Group Holdings beat on both top and bottom lines in FY26, with both segments growing and analyst consensus sitting at Strong Buy from two covering analysts as of 18 June 2026. The same-day target price upgrade to S$0.06 and 29% upward revision to FY27 net profit forecasts signal Phillip Securities believes FY26 operating leverage will carry forward.

The other side of that equation is that management’s own FY27 guidance is ambitious, agricultural businesses carry inherent cyclicality, and a micro-cap market capitalisation of approximately S$64m to S$66m limits liquidity. Micro-cap investors considering this stock should weigh position sizing carefully against those constraints.

Public small-cap quality has deteriorated structurally across global markets as private equity captures the best early-growth businesses, leaving listed micro-caps like Zixin in a landscape where active due diligence on fundamentals matters more than passive index exposure would ever capture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Zixin Group Holdings is a Singapore-listed, vertically integrated sweet potato company operating across four segments: cultivation and supply, processed food production, recovery and recycling, and corporate services, with all operations based in China.

Zixin beat Phillip Securities forecasts significantly in FY26, with full-year revenue reaching 104% of forecast and profit after tax landing at 123% of forecast, a 23-percentage-point overshoot on the bottom line.

Phillip Securities raised its target price to S$0.06 on 18 June 2026, implying approximately 88% to 100% upside from the share price range of S$0.030 to S$0.032 at the time of the upgrade.

Key risks include demanding FY27 management growth targets, input-cost inflation compressing gross margins, ODM customer concentration, micro-cap liquidity constraints at approximately S$64m to S$66m market capitalisation, and full operational exposure to China.

The processed segment, which includes sweet potato chips and steamed products, already represented approximately 70% of group revenue in 1H FY26 and saw combined sales surge 71% year-on-year, while the fresh segment grew volumes approximately 30% year-on-year with earnings nearly doubling.