Trump Signs Preliminary Iran Deal, Stocks Rally and Oil Falls

3 hrs ago

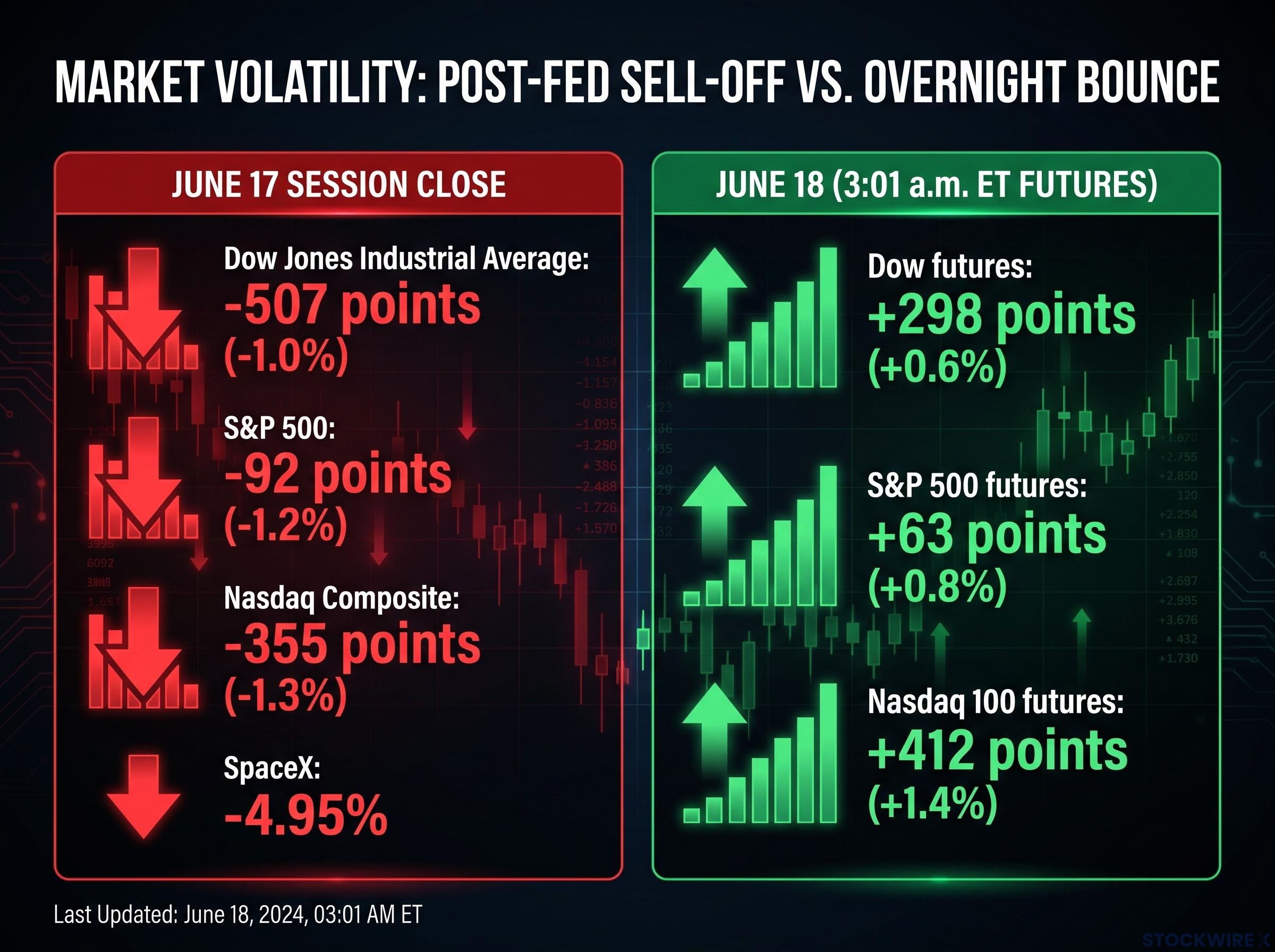

At Wednesday’s close, the Dow Jones Industrial Average had shed 507 points and the Nasdaq Composite was down 1.3%. By 3 a.m. Thursday, futures had already clawed back most of those losses. Kevin Warsh’s first Federal Reserve meeting produced exactly that kind of volatility, and the rate decision itself was not the reason.

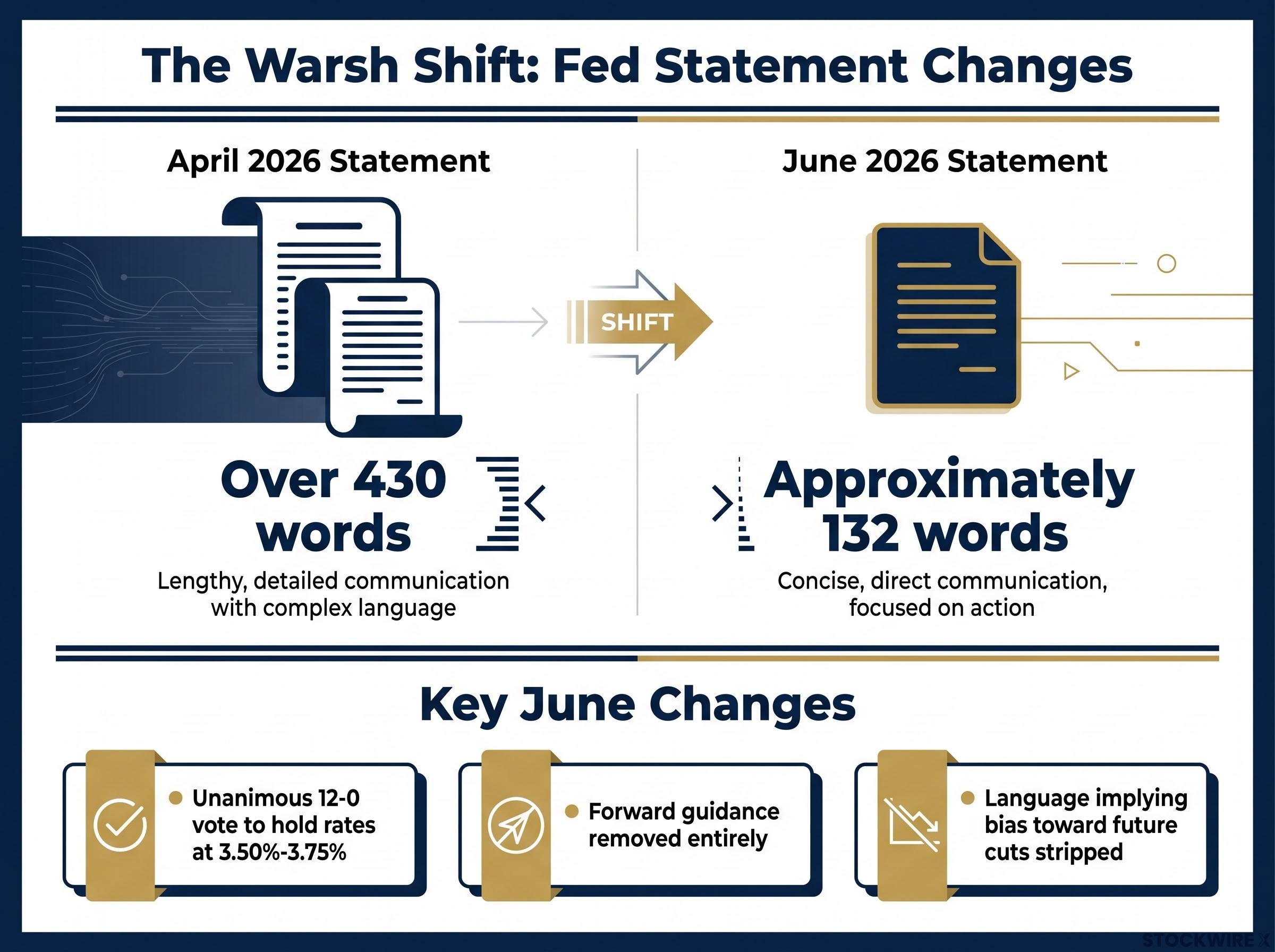

The June 2026 FOMC meeting delivered a unanimous 12-0 vote to hold rates at 3.50%-3.75%. The hold was expected. What was not expected was the language stripped from the statement, a dot-plot reversal that no forecaster had predicted at this speed, and the questions now circulating about how Warsh intends to run the institution he inherited. This article breaks down what actually changed at Wednesday’s meeting, corrects one widely circulated misreading about the Fed’s employment mandate, and explains what the shift means for investors navigating rate-sensitive portfolios in the months ahead.

The sell-off on 17 June was sharp and broad-based. By session close:

By 3:01 a.m. ET on 18 June, the picture had already shifted:

CME FedWatch probability shift: The probability of rates remaining unchanged for the rest of 2026 fell materially following the meeting, while hike probability rose, with derivative pricing now reflecting 25-50 basis points of additional tightening by year-end.

The rate decision was a hold. The reaction was not priced to a hold. Treasury two-year yields moved higher, consistent with markets repricing toward possible hikes, and the sell-off concentrated in growth-oriented names like SpaceX that are most sensitive to changes in rate expectations. If the decision was unchanged, why did equities respond as though a hike had already happened? Because the signal was in the statement, the dot plot, and the tone, not the rate itself.

Kevin Warsh took the chair at a Federal Reserve that markets had expected to continue cutting rates. His appointment positioned him as more inflation-focused than his predecessor, and his first meeting confirmed that positioning in practice.

“Hawkish” describes a central bank posture that prioritises controlling inflation, typically by keeping interest rates higher or raising them, even at the cost of slower economic growth. A hawkish Fed chair signals that the institution is more likely to tolerate weaker employment data or softer growth than to tolerate persistent inflation. For investors, this means the bar for rate cuts is higher, and the probability of rate hikes is no longer negligible.

Warsh’s communication changes at this meeting made the shift concrete:

Warsh explicitly stated the decision was taken in support of the Fed’s dual mandate of price stability and maximum employment. The mandate did not change. The emphasis did. President Trump, who has publicly favoured lower rates, has found Warsh’s hawkish posture a source of friction; the political backdrop adds another layer of uncertainty for markets monitoring the new chair’s independence.

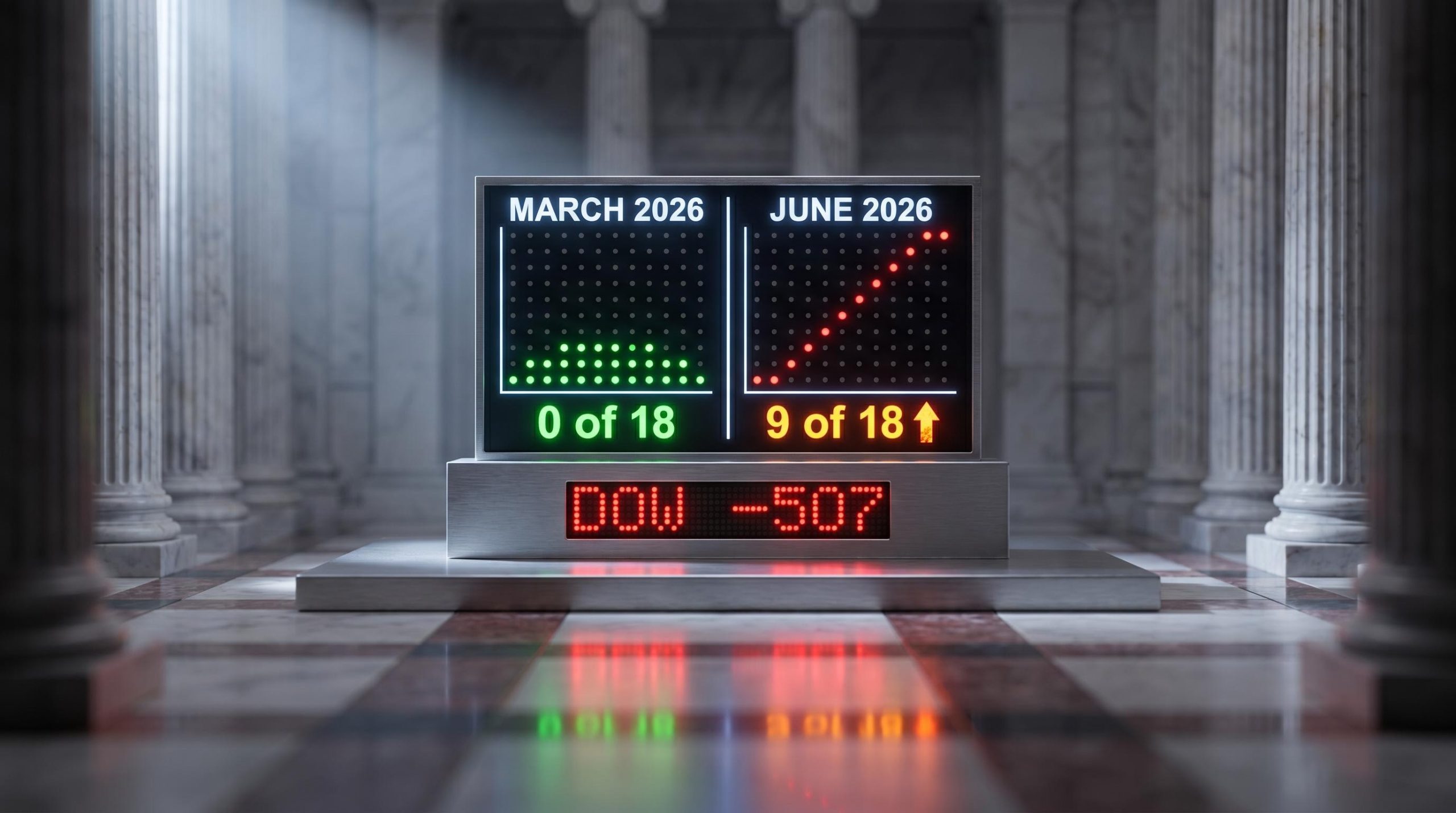

The March-to-June shift in the Summary of Economic Projections tells the story more clearly than any press conference answer.

| Projection | March 2026 | June 2026 |

|---|---|---|

| Officials projecting at least one hike | 0 of 18 | 9 of 18 |

| Of those, projecting two hikes | 0 | 6 of 9 |

| Median rate path | 1 cut in 2026 | Shifted toward hikes |

In March, zero officials projected a Fed rate hike. Three months later, nine of 18 did. Six of those nine projected two hikes. That is not a gradual drift. That is a reversal.

The speed of this shift caught forecasters off guard. In a single quarter, the committee’s framing moved from an easing bias to “higher for longer, and possibly higher still.” CME FedWatch derivative pricing now reflects 25-50 basis points of additional tightening by year-end, and September 2026 has been identified as the earliest possible meeting for a hike based on updated guidance, though no formal commitment was made.

The dot plot is not a promise. It is a signal of where the committee’s collective thinking has moved. And that thinking has moved further and faster than at any comparable point in recent cycles.

The market repricing that preceded this meeting was itself a significant story: in ten weeks, institutional investors at Goldman Sachs, J.P. Morgan, and BlackRock had already shifted from pricing 50-75 basis points of cuts to a 65-70% probability of a hike, meaning the June dot-plot reversal accelerated a repositioning that was already underway in derivative markets.

Headlines following the meeting suggested Warsh had removed references to maximising employment from the Fed’s mandate. That characterisation is inaccurate, and the distinction matters for how investors interpret the policy path ahead.

Warsh’s stated position: The decision was taken in support of the Fed’s dual mandate of price stability and maximum employment.

The dual mandate was explicitly reaffirmed. What changed was emphasis: the statement placed stronger rhetorical weight on inflation risks, including supply shocks and elevated energy prices linked to the Iran conflict, and removed language that had previously hinted at future cuts.

The Federal Reserve Reform Act of 1977 codified the dual mandate into statute, establishing maximum employment, stable prices, and moderate long-term interest rates as the institution’s core objectives, which is why any characterisation of Warsh removing the employment mandate misreads a statutory requirement that no chair has the authority to unilaterally change.

What changed:

What did not change:

The practical implication is real, even if the formal mandate is intact. The near-term policy trigger is inflation, not employment. Misreading this as a formal mandate change could lead investors to miscalibrate how the Fed would respond to rising unemployment; the accurate framing is that inflation data will drive the next move, not labour market softening.

The repricing toward tightening creates direct headwinds for the most rate-sensitive parts of the market:

The dot plot’s asset class implications extend well beyond growth equities: long-duration bonds and high-yield credit face their own repricing dynamic as the committee’s median rate path shifts toward hikes, with the U.S. dollar and short-duration instruments positioned to benefit from the same hawkish signal that pressured SpaceX shares on 17 June.

Every CPI and PCE release between now and the September 2026 FOMC meeting will carry outsized market significance. The Fed has stated its data dependence explicitly. The data is the policy signal now.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The September 2026 FOMC meeting is the next major inflection point. No commitment has been made, and the path remains data-dependent, but the dot plot has told markets where the committee’s thinking is headed. The variables that will shape the decision are specific:

The political backdrop remains. Trump has publicly favoured lower rates, and Warsh’s first meeting demonstrated a willingness to prioritise the inflation mandate over that preference. Whether that independence holds through an election cycle is a question markets will price continuously.

Warsh’s Fed gives fewer forward signals. That is a feature of the new era, not a temporary adjustment. Investors who build their monitoring frameworks around the specific inflation data releases ahead of September will be better positioned than those waiting for the next meeting to surface the next surprise.

For investors who want a structured framework for recalibrating holdings before September, our dedicated guide to investing during rate hikes walks through sector rotation toward high-margin, low-debt equities with pricing power, the role of dollar-cost averaging in volatile rate environments, and why avoiding highly leveraged names is the first practical step in a tightening cycle.

The Federal Reserve dot plot is a chart showing where each FOMC member individually projects interest rates will be in future periods; it matters because it signals the committee's collective directional thinking on rate hikes or cuts, which directly affects bond yields, equity valuations, and borrowing costs.

The Fed held rates unanimously at 3.50%-3.75%, but the dot plot showed a dramatic reversal: nine of 18 officials now project at least one rate hike in 2026, compared to zero in March, while the post-meeting statement was cut from over 430 words to approximately 132 and forward guidance was removed entirely.

A hawkish Fed, which prioritises inflation control by keeping rates higher or raising them, typically pressures utilities, REITs, and long-duration growth stocks because higher yields raise discount rates on future cash flows and make bond-proxy equities less attractive relative to fixed income.

The dual mandate, codified in the Federal Reserve Reform Act of 1977, requires the Fed to pursue maximum employment, stable prices, and moderate long-term interest rates; Warsh reaffirmed both objectives explicitly, but shifted rhetorical emphasis toward inflation risks rather than removing any formal mandate.

CPI and PCE inflation prints released between June and September 2026 are the most critical data points, as the Fed has stated its policy path is data-dependent and September 2026 is the earliest identified meeting at which a rate hike could occur.