Record Highs Are Not the Risk Most Investors Think They Are

6 hrs ago

“`json { “fact_checked_full_article”: “On 16 April 2026, the Washington State Investment Board voted to commit more than $500 million of public pension money to new private equity and private credit funds. The approved vehicles include commitments to firms whose portfolio companies are currently entangled in a state attorney general lawsuit, a record copyright settlement, and municipal surveillance controversies. State Treasurer Mike Pellicciotti cast the lone dissenting vote among the board’s 10 voting members, deepening a public rift over how much private markets risk is appropriate for a fund managing the retirement savings of hundreds of thousands of public employees. What follows is a breakdown of what was approved, why the treasurer objected, how the fund’s private markets exposure compares to national peers, and what controversies attach to the companies receiving pension dollars.\n\n## Board approves $500 million-plus in private markets commitments\n\nThe 16 April meeting produced preliminary approvals for three sets of commitments spanning private equity and private credit. The board authorised up to €150 million (plus fees and expenses) to Charterhouse Capital Partners XII, a London-based firm focused on healthcare and retail sectors. A combined $100 million was split between Spark Capital IX and Spark Capital Growth VI, two venture funds. And the largest single allocation, up to $300 million, went to Monarch Alternative Capital Opportunity Fund, a Milwaukee-based private credit vehicle targeting energy and technology exposures.\n\n> Total new commitments: more than $500 million across three approvals, pending final ratification at a subsequent board meeting.\n\nWSIB manages approximately $187.6 billion in assets across retirement systems serving Washington’s public employees, teachers, and law enforcement officers. The board holds prior investment relationships with all three firms, making these commitments a deepening of existing exposure rather than a new direction.\n\n

| Fund | Firm | Commitment | Asset Class | Sector Focus |

|---|---|---|---|---|

| Charterhouse Capital Partners XII | Charterhouse Capital | Up to €150M | Private Equity | Healthcare, Retail |

| Spark Capital IX / Growth VI | Spark Capital | Up to $100M (combined) | Private Equity (Venture) | Technology |

| Monarch Alternative Capital Opportunity Fund | Monarch Alternative Capital | Up to $300M | Private Credit | Energy, Technology |

\n

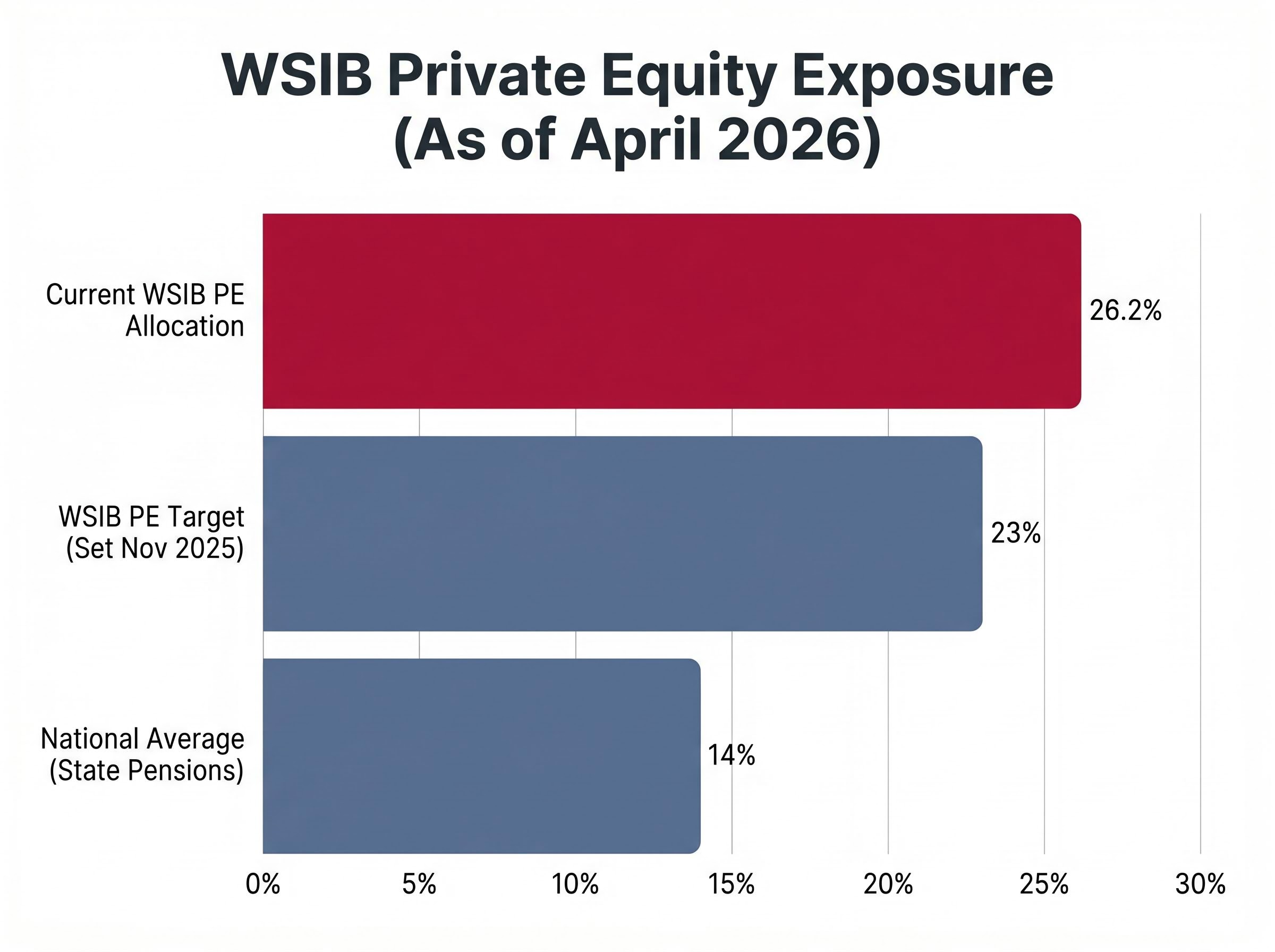

\n\n## Treasurer Pellicciotti casts the only dissenting vote\n\nOne vote out of ten went the other way.\n\nTreasurer Mike Pellicciotti voted against all new investment recommendations at the 16 April meeting, making him the sole dissenter on a board that includes two state agency heads, two legislative budget writers, and representatives from the retirement systems the fund serves. The remaining members approved the commitments.\n\nPellicciotti’s opposition did not arrive without warning. In January 2026, the treasurer publicly cautioned that the board’s concentration in private equity exposed the fund to undue risk.\n\n> According to the Centralia Chronicle, Pellicciotti warned in January that Washington’s level of private equity exposure creates risk that is disproportionate to the fund’s obligations to beneficiaries.\n\nThe board has since signalled a general intent to slow the pace of new private equity commitments, a partial acknowledgment of the treasurer’s concerns. Whether that intent translates to measurable restraint remains an open question; the 16 April approvals suggest the pace has not yet decelerated.\n\n## How Washington’s private markets exposure compares to national peers\n\nThe numbers tell a clear story. Washington’s private equity allocation sits at approximately 26.2% of the total portfolio, roughly $52 billion, down from 29% in December 2024. That figure is roughly double the national average for state pension funds, which sits at approximately 14%.\n\nIn November 2025, the board voted to lower its private equity target to 23%, down from 25%. Yet the fund remains approximately 3 percentage points above even that revised target, and new commitments continue to flow.\n\n- Private equity: approximately 26.2% of portfolio\n- Public equity: 32.1%\n- Real estate: 17%\n- Private credit: new 3% target allocation approved March 2026\n\nAltogether, roughly 55% of the fund sits in private markets, encompassing private equity, private credit, and real estate. The strategy has produced returns: private equity generated approximately $5.7 billion in net capital in 2025, delivering a 9.6% annual return.\n\n> The cost of that strategy: approximately $862.3 million in private equity management fees in 2025.\n\nNew investments will be deployed gradually over multiple years, according to board materials. The gap between the fund’s current allocation and its own stated target, however, suggests the trajectory remains upward even as the board discusses restraint.\n\n## What is private equity, and why do pension funds use it?\n\nPension funds are drawn to private markets for the same reason individual investors sometimes are: the potential for returns that exceed what public stock exchanges deliver over long time horizons. The trade-off is straightforward, but the mechanics are worth understanding.\n\n1. Private equity involves buying ownership stakes in companies that are not listed on public stock exchanges. Investors commit capital that is typically locked up for years, sometimes a decade or longer, and cannot be easily sold or redeemed. The appeal for pension funds with 30-year time horizons is that this illiquidity premium can generate higher returns than publicly traded equities.\n\n2. Private credit involves extending loans to companies that are unable to access conventional bank financing. This segment expanded sharply after the 2008 financial crisis, as tightened banking regulations created space for non-bank lenders to fill the gap. Unlike bank loans, private credit operates without the same regulatory oversight, and borrowers are not always independently assessed for creditworthiness.\n\n> Industry observers, including Alyssa Giachino, investor engagement director at the Private Equity Stakeholder Project, have raised concerns that private equity firms may overstate the value of their holdings, given that valuations are not subject to the real-time price discovery of public markets.\n\nThe concerns are not theoretical. Multiple companies financed through private credit have sought bankruptcy protection in early 2026. Several large institutional investors have begun reducing exposure: Maine, Oregon, and Ohio have each pulled back on private equity allocations, while university endowments at Yale and Harvard have divested billions from private holdings in recent years.\n\n## The Spark Capital portfolio companies drawing scrutiny\n\nThe $100 million commitment to Spark Capital funds carries a layer of risk that extends beyond market performance. Three portfolio companies backed by Spark Capital face active legal, regulatory, or reputational challenges, and their cumulative profile raises questions about what diligence looks like when pension dollars are involved.\n\n- Kalshi: The prediction markets platform is being sued by Washington State Attorney General Nick Brown, who alleges Kalshi operates as an unlicensed gambling platform. On 6 April 2026, Kalshi won a separate U.S. appeals court ruling against New Jersey’s attempt to regulate its prediction market, reinforcing its legal position on federal preemption.\n- Anthropic: The artificial intelligence company agreed to a $1.5 billion copyright settlement in September 2025, described as the largest such settlement in U.S. history. In March 2026, Anthropic resumed negotiations with the U.S. Department of Defence on AI procurement contracts.\n- Flock Safety: The licence plate recognition company has faced municipal contract cancellations across the United States driven by immigration surveillance concerns. Washington state lawmakers enacted legislation regulating the technology’s use during the current legislative session.\n\n> Washington’s own attorney general is suing a company that Washington’s pension fund is indirectly backing through the Spark Capital commitment. That governance tension is difficult to reconcile.\n\nSpark Capital and Kalshi did not respond to requests for comment. WSIB does not publicly comment on individual portfolio companies outside official board meetings.\n\n## Beneficiary concerns and what happens next\n\nThe people whose retirement savings sit inside WSIB’s portfolio are not silent observers.\n\nDonna Albert, a retired state engineer with 27 years of service, has argued through the beneficiary-led organisation Divest Washington that pension investments in coal directly contradict Washington’s climate policy commitments. Barb Carey, a retired hydrogeologist who spent 35 years with the Department of Ecology, frames the argument in financial terms.\n\n> \”Climate risks, floods, wildfires, drought, these are financial risks for beneficiaries,\” Carey has argued, contending that the fund’s exposure to fossil fuel-linked holdings creates long-term liability for younger members who will depend on the portfolio decades from now.\n\nThe procedural next steps are concrete:\n\n- Final ratification of the 16 April commitments is scheduled at a subsequent board meeting\n- The next scheduled WSIB meeting is 18 June 2026 (per scheduling documents; confirmed dates are available at sib.wa.gov/meetings.html)\n- Beneficiaries and the public can submit comments through WSIB’s portal at sibwa.commentinput.com\n\nThe fund’s direction will be shaped by whether the board treats the treasurer’s dissent, the portfolio company controversies, and the beneficiary advocacy as signals worth acting on, or as noise to be absorbed.\n\nThe central tensions remain unresolved: a $187.6 billion fund with private markets exposure roughly double the national peer average, an elected treasurer voting alone against the direction of travel, portfolio companies under active legal scrutiny from the same state government, and beneficiaries demanding greater accountability. The ratification vote at the next board meeting will determine whether the 16 April commitments become final. WSIB’s meeting schedule and public comment portal are accessible at sib.wa.gov for beneficiaries who wish to engage before that decision is made.\n\nThis article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.\n\n—” } “`

The AI investment risks facing institutional capital in 2026 add a further layer of uncertainty to Spark Capital’s technology-focused portfolio: hyperscalers have committed more than $500 billion in aggregate capital expenditure with no clear path to proportionate returns, and early market divergence in 2026 signals that investors are now differentiating sharply between individual AI business models rather than treating the sector as a single exposure.

The hidden risks in private equity and private credit extend well beyond fee drag: internal GP valuations mean reported returns can lag underlying financial reality by quarters, and redemption gates in retail-accessible vehicles have left investors locked out during stress periods, a pattern that regulators are now scrutinising through the SEC’s 2026 examination priorities.

The structural limits of unwinding a large illiquid book are a core reason why the board’s stated intent to slow new commitments has not yet translated into a lower allocation: secondary sales of private equity stakes take years to execute at acceptable prices, and pacing reductions alone cannot quickly close a gap of roughly 3 percentage points above the fund’s own revised target.

The Washington State Investment Board (WSIB) is the body responsible for investing public pension assets for Washington's public employees, teachers, and law enforcement officers. It manages approximately $187.6 billion in assets across these retirement systems.

Treasurer Pellicciotti cast the sole dissenting vote because he believes Washington's concentration in private equity exposes the fund to risk disproportionate to its obligations to beneficiaries. He had publicly raised this concern as early as January 2026, noting the fund's private equity allocation is roughly double the national average for state pension funds.

WSIB's private equity allocation stands at approximately 26.2% of its total portfolio, which is roughly double the national average of around 14% for state pension funds, and remains about 3 percentage points above the fund's own revised target of 23%.

Spark Capital portfolio companies include Kalshi, which is being sued by Washington's own Attorney General as an alleged unlicensed gambling platform; Anthropic, which settled a copyright lawsuit for $1.5 billion in September 2025; and Flock Safety, which has faced municipal contract cancellations over immigration surveillance concerns.

Beneficiaries can submit public comments through WSIB's portal at sibwa.commentinput.com, and the next scheduled board meeting where the April 2026 commitments are due for final ratification is 18 June 2026, with further information available at sib.wa.gov.