SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

8 hrs ago

Webjet Group shares suffered their steepest single-day decline since the company’s demerger on 20 May 2026, falling approximately 13–15% after a compound shock caught the market from two directions at once. The sell-off arrived on results day, combining a materially weaker FY26 earnings print with the unexpected disclosure that Virgin Australia would substantially reduce its commission payments to the Webjet online travel agency (OTA) division from 1 July 2026. For Australian investors holding WJL, the session forced a structural question into the open: how exposed is an OTA business model when the airlines it distributes can unilaterally restructure its economics? This analysis unpacks what drove the fall, how the commission change works mechanically, what the early FY27 trading data already reveals about demand, and what the combination of these pressures means for investors assessing the stock’s recovery path.

WJL shares opened under immediate pressure after the simultaneous release of FY26 full-year results, an investor presentation, and a sustainability report on the ASX, with the results briefing scheduled for 9:00am AEST. The stock traded as low as $0.40-$0.4250 intraday from a prior close of approximately $0.49, representing a decline of roughly 13–15% and marking the lowest level since the Webjet Group demerger.

The ASX continuous disclosure obligations under Listing Rule 3.1 require listed entities to immediately disclose market-sensitive information, which is why the Virgin Australia commission notification and FY26 results landed simultaneously in a single ASX release rather than being staged across separate trading sessions.

The approximately 13–15% single-session fall took WJL to its lowest price since the company was separated into distinct listed entities, a move that wiped out months of accumulated share price recovery in hours.

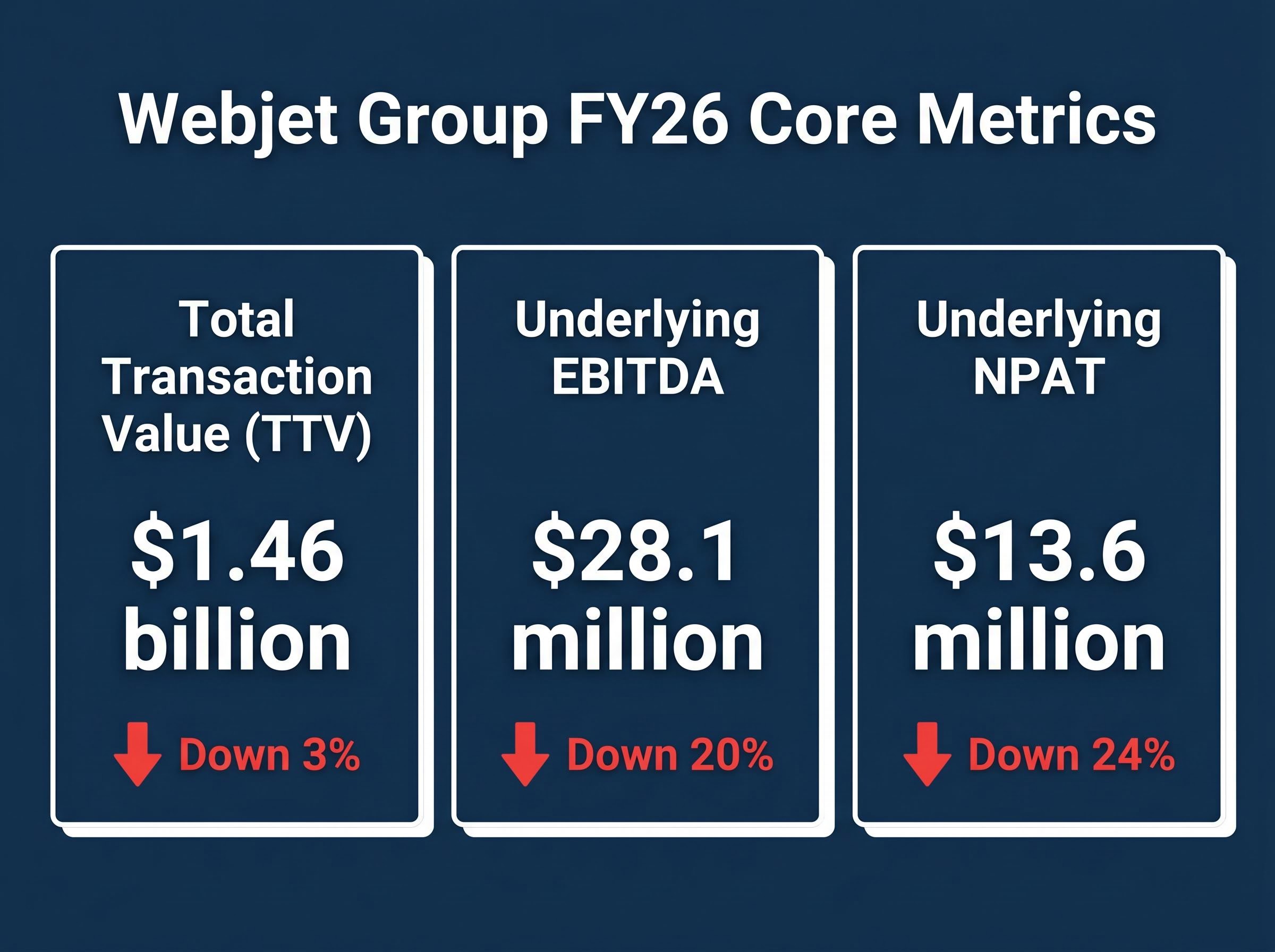

The market was processing two distinct pieces of information simultaneously: a set of FY26 results that showed meaningful earnings deterioration, and a forward-looking commission notification from Virgin Australia that repriced the OTA division’s revenue outlook. The key FY26 financial metrics confirmed the weakness:

The severity of the sell-off reflected the market’s difficulty in separating the backward-looking earnings miss from the forward-looking commission cut. Both arrived in the same session, and both pointed in the same direction.

Online travel agencies earn revenue by distributing airline tickets through their platforms. The airline pays the OTA a commission, typically a percentage of the booking value, in exchange for the distribution reach and customer acquisition the OTA provides. These agreements often include tiered structures where performance thresholds, measured by booking volumes or total transaction value, unlock higher commission rates. Ancillary products such as seat selection, baggage, and travel insurance may also carry separate commission arrangements.

The OTA model depends on these commission structures remaining stable enough to support the platform’s marketing spend, technology costs, and customer acquisition investment.

IATA and BCG research on airline distribution identifies the shift toward New Distribution Capability (NDC) as a structural force enabling airlines to reduce reliance on third-party OTA channels, providing the broader commercial context in which unilateral commission restructures like Virgin Australia’s become increasingly feasible.

Virgin Australia notified Webjet of revised commission terms effective 1 July 2026. Had the revised structure applied across all of FY26, Webjet estimated the revenue impact at approximately $3 million lower.

The Virgin Australia commission changes were first disclosed on 19 May 2026, the day before full-year results, when Webjet released a standalone ASX announcement quantifying the revenue impact and confirming that management would adjust its commercial and partnership strategy in response.

| Category | Prior arrangement | Revised terms | Effective date |

|---|---|---|---|

| Commission structure | Existing rates on flights and ancillary products, subject to performance targets | Substantially reduced rates | 1 July 2026 |

| Estimated FY26 revenue impact (retrospective) | Baseline FY26 revenue | Approximately $3 million lower | Retrospective estimate |

Against the OTA division’s FY26 EBITDA of $38.7 million, a $3 million revenue reduction appears contained. The market reaction, however, suggests investors repriced the mechanism itself: a single airline partner can unilaterally restructure the OTA’s economics, and that risk is repeatable with other partners.

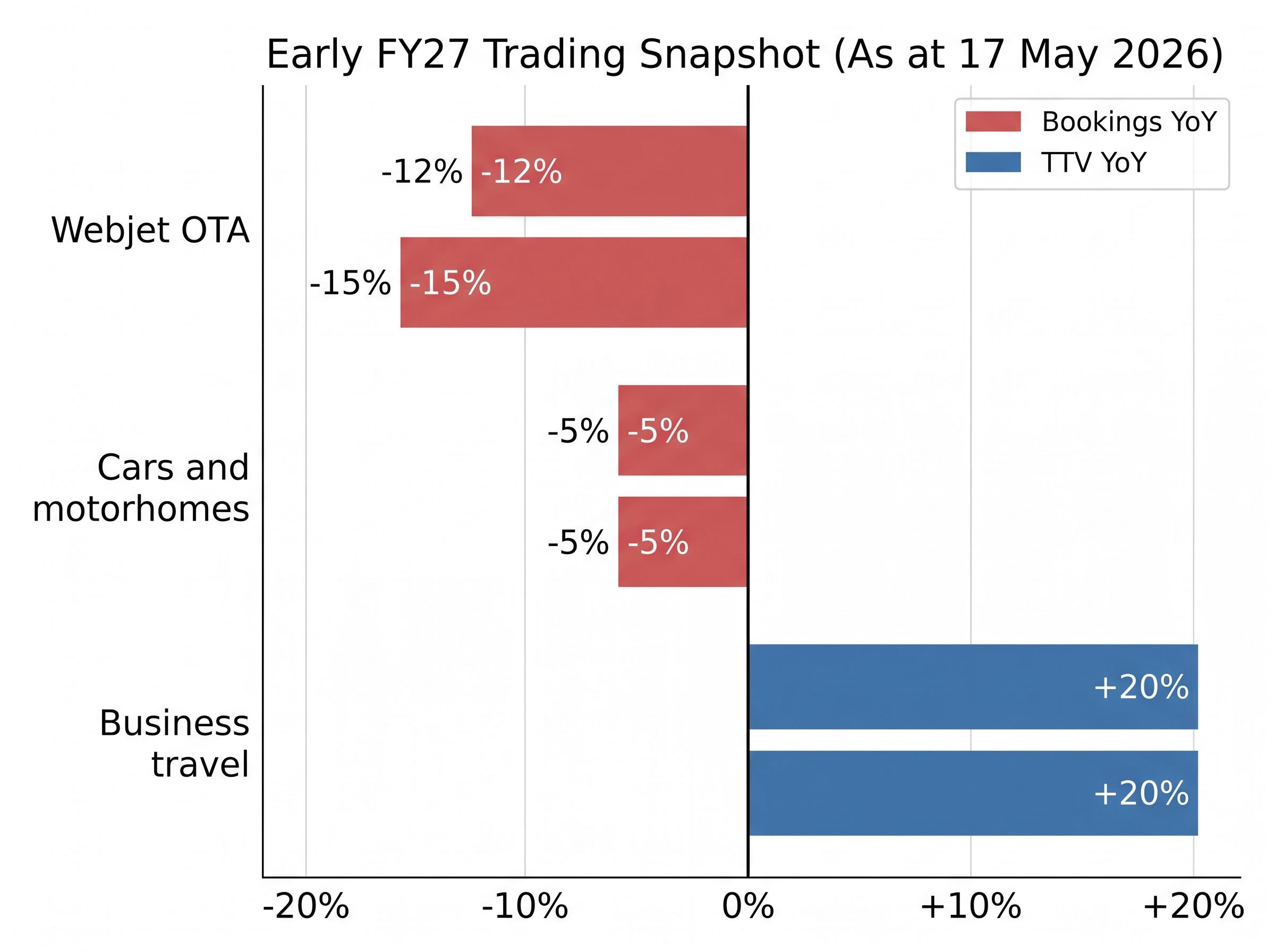

The FY26 results included an early FY27 trading snapshot as at 17 May 2026, and the numbers suggest the earnings challenge extends well beyond the Virgin Australia commission cut.

| Segment | Bookings change (YoY) | TTV change (YoY) |

|---|---|---|

| Webjet OTA | Down 12% | Down 15% |

| Cars and motorhomes | Down ~5% (constant currency) | Down ~5% (constant currency) |

| Business travel (direct-to-business) | Up ~20% | Up ~20% |

OTA transaction value down 15% year-on-year in early FY27 trading, before the commission cut has even taken effect.

The OTA division’s 12% bookings decline and 15% TTV decline are both significantly steeper than FY26’s full-year 7% volume contraction. The gap between the two figures also signals a deterioration in average booking values, consistent with a reported shift toward lower-value short-haul Asian routes that compresses per-booking TTV.

Management flagged that business travel momentum was easing despite the strong early numbers. For investors, the FY27 read carries more weight than the full-year FY26 print because it is forward-looking, and it indicates the earnings challenge is broader than a single airline commission reduction.

The OTA booking weakness reflects forces that sit outside Webjet’s operational control. Management described FY27 conditions as “fluid and challenging,” citing Middle East instability, inflationary pressures, and subdued consumer confidence as headwinds to domestic leisure demand. Elevated airfare levels and ongoing cost-of-living constraints are suppressing the booking volumes that form the OTA division’s revenue base.

Qantas announced domestic capacity cuts of approximately 5 percentage points in the fourth quarter of FY26 in response to the Middle East fuel shock, a structural reduction in available seat supply that, combined with higher fares, directly affects the volume of bookings flowing through OTA platforms like Webjet.

The mix shift toward shorter-haul Asian travel compounds the problem. It reduces per-booking TTV and average booking values simultaneously, which is doubly negative for any commission structures tied to booking value rather than booking volume.

Four named headwinds were flagged for FY27 earnings:

Business travel contributed $1.2 million in revenue during FY26 but ran at an EBITDA loss of $0.6 million in its initial period. The segment is growing, but it cannot currently absorb losses in the leisure OTA division. FY26 total bookings contracted 7% year-on-year to 1.4 million, with the smaller TTV decline partly cushioned by higher-value business travel transactions.

Domestic leisure remains Webjet’s largest and most established revenue engine. When cost-of-living pressures suppress that segment at the same time a major airline partner cuts commissions, the earnings risk compresses margins from both the revenue and volume sides simultaneously.

The 20 May 2026 sell-off has forced three distinct risk layers into the valuation, each with a different time horizon:

No post-announcement analyst target revisions or recommendation changes were available as at 20 May 2026. The market moved on company disclosure alone, without the cushion of broker-consensus reassurance.

The structural question the sell-off has forced into the open is whether the OTA model is exposed to ongoing airline disintermediation, a risk that is harder to price than a specific revenue line and which may explain why a $3 million commission cut could rationally trigger an approximately 13–15% share price move.

Statutory NPAT rose 85% to $3.7 million in FY26, driven by non-recurring items rather than operating performance. Underlying NPAT fell 24% to $13.6 million and underlying EBITDA fell 20% to $28.1 million. Earnings-focused investors are watching the underlying trajectory, not the statutory figure.

Webjet is navigating a simultaneous demand-side and supply-side earnings compression at the precise moment its newest segment, business travel, is still loss-making. The OTA division’s FY26 EBITDA of $38.7 million is the earnings base under pressure. Business travel’s $0.6 million EBITDA loss means it cannot yet offset weakness elsewhere.

For the investment case to stabilise, three indicators would need to shift:

At approximately $0.4250, WJL has de-rated significantly from its prior close of $0.49. The approximately 13–15% single-day move reflects the market repricing structural risk, not just a single weak result. The path forward depends on factors that remain genuinely uncertain as at 20 May 2026, and no post-announcement analyst guidance is available to anchor expectations.

For investors holding WJL or assessing the stock at its post-results level, the question is not whether FY27 will be weaker than FY26; the trading data suggests it will be. The question is whether the current share price already reflects that outcome or whether further earnings risk remains unpriced.

Investors wanting to benchmark WJL’s post-results de-rating against how other ASX travel and consumer names have traded through their own earnings pressure cycles will find our full explainer on ASX travel sector valuations after large price declines, which covers Flight Centre and CAR Group in detail, examining how fundamentals and share price trajectories diverged and what valuation signals preceded recoveries.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

An OTA commission is the fee an airline pays an online travel agency like Webjet for distributing its tickets through the platform. These commissions form the core of Webjet's OTA revenue, so when a major partner like Virgin Australia reduces rates, it directly lowers the division's income and profitability.

Webjet shares fell approximately 13-15% on 20 May 2026 because the market received two negative signals simultaneously: FY26 underlying EBITDA declined 20% and underlying NPAT fell 24%, while Virgin Australia disclosed it would substantially cut commission payments to Webjet's OTA division from 1 July 2026.

Webjet estimated that had the revised Virgin Australia commission structure applied across all of FY26, revenue would have been approximately $3 million lower, a figure measured against the OTA division's FY26 EBITDA of $38.7 million.

As at 17 May 2026, Webjet's OTA division reported bookings down 12% and total transaction value down 15% year-on-year, a steeper decline than FY26's full-year 7% volume contraction and occurring before the Virgin Australia commission cut had even taken effect.

Management and market observers have identified three key signals to watch: an improvement in early FY27 OTA trading data from the current 12-15% decline trajectory, clarity on whether other airline partners will follow Virgin Australia's commission restructure, and the business travel segment reaching EBITDA breakeven to provide a second earnings pillar.