Nasdaq Falls 4% as Broadcom AI Miss Sparks Semiconductor Rout

7 hrs ago

The S&P 500 technology sector snapped a four-session winning streak on Tuesday 3 June 2026, but the index-level pause obscured a far more consequential set of moves underneath. Alphabet raised approximately $85 billion in the largest equity capital event in market history. Anthropic filed a confidential S-1 that placed it ahead of OpenAI in the formal race toward a public listing. Palo Alto Networks fell nearly 6% despite beating every earnings estimate it faced and raising guidance. And through all of it, semiconductor stocks kept climbing, with the Philadelphia Semiconductor Index on pace for its ninth positive close in eleven sessions. Together, these moves amount to a single, readable signal: the AI capital cycle is now functioning as a sector selection mechanism, separating the companies investors will pay up for from those they will not, regardless of reported results. What follows maps each move, explains what drove it, and distils the investor priority framework the day’s divergence encodes.

The split on 3 June was stark. Broader technology names gave back four sessions of gains; semiconductor stocks did not.

The semiconductor resilience was not a sector-specific anomaly. It was a direct readout of the AI investment cycle’s momentum, with hyperscaler spending commitments validating demand for the chips that power large-scale compute infrastructure.

Within the AI supply chain, the profit from hyperscaler spending is not distributed evenly: foundries, high-bandwidth memory producers, and networking equipment suppliers retain structural leverage because every AI chip design, whether custom or third-party, depends on the same fabrication and HBM ecosystem, a dynamic that helps explain why the Philadelphia Semiconductor Index has sustained its momentum even as broader technology names pulled back.

Danni Hewson, Head of Financial Analysis at AJ Bell, noted that the AI investment cycle has enabled equity recovery and highlighted ongoing competitive dynamics among hyperscalers as a defining feature of mid-2026 market conditions, according to Investing.com.

That competitive dynamic would become far more visible before the day was over.

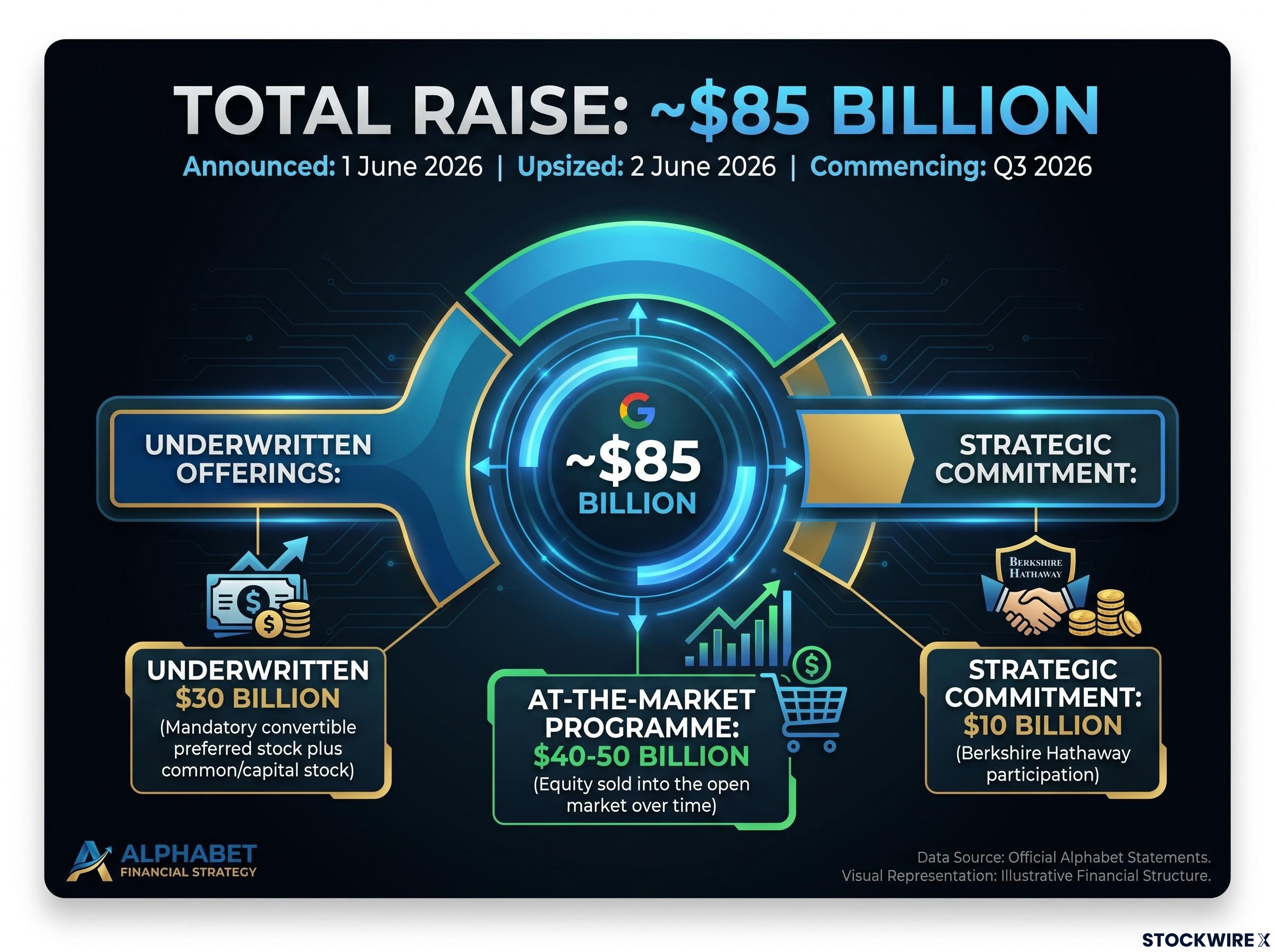

Alphabet announced its capital raise on 1 June 2026. By 2 June, it had been upsized to approximately $85 billion, the largest equity market fundraise on record by a single issuer. The stated purpose: meeting what the company described as unprecedented customer AI demand.

The structure broke into two components.

| Component | Amount | Instrument |

|---|---|---|

| Underwritten offerings | $30 billion | Mandatory convertible preferred stock plus common/capital stock |

| At-the-market programme | $40-50 billion | Equity sold into the open market over time |

| Strategic commitment | $10 billion | Berkshire Hathaway participation |

Portions of the raise are expected to commence in Q3 2026.

The scale resets the competitive floor. Microsoft, Meta, and Amazon now face a revised capital commitment benchmark. As Hewson’s commentary highlighted, the competitive dynamics among hyperscalers are not theoretical; they are producing balance sheet events of a size the market has not previously absorbed. AI infrastructure investment has moved beyond incremental capex into a category that demands new equity issuance to fund.

Anthropic filed a confidential S-1 with the SEC on 1 June 2026, placing it ahead of OpenAI in the formal steps toward a U.S. public listing.

The filing was characterised in financial reporting as having “surpassed OpenAI” in the IPO process, a competitive framing that carries weight in a year when both companies are expected to seek public market valuations.

The filing fits into a broader 2026 IPO wave that includes OpenAI and SpaceX, but several material unknowns remain:

What the filing does confirm is that the private AI ecosystem is preparing to price itself in public markets. For institutional investors, that will establish observable valuation benchmarks for a sector that currently lacks them.

AI IPO absorption presents a distinct risk that goes beyond any single filing: SpaceX, Anthropic, and OpenAI are collectively valued at approximately $3.5 trillion and are all targeting public listings within the same compressed mid-to-late 2026 window, a concentration that Standard Chartered global CIO Steve Brice warned on 2 June 2026 is expected to create market digestion difficulties over the summer months.

Palo Alto Networks reported fiscal Q3 results (quarter ended 30 April 2026) that beat on both revenue and earnings estimates. The company raised its forward guidance.

The stock fell approximately 5.8% on 3 June, with one report citing an intraday decline of up to 6.92% from a prior close near $297.

The dissonance between the result and the reaction requires unpacking.

Four factors drove the decline:

None of these individually would typically produce a 6% drop on a beat-and-raise quarter. The compounding factor was sector rotation. Market commentary in mid-2026 explicitly flagged ongoing shifts between cybersecurity and AI infrastructure spending as competing destinations for enterprise technology budgets. AI tools are being deployed for both threat detection (which benefits cybersecurity names) and infrastructure perimeter work (which blurs the sector boundary), creating valuation uncertainty for pure-play cybersecurity companies.

The Palo Alto result is a case study in how market perception of a company’s position within the AI capital cycle can override headline financial performance.

For readers wanting to apply a repeatable framework to the cybersecurity-versus-AI-infrastructure dynamic that drove Palo Alto’s decline, our dedicated guide to sector rotation strategy walks through how institutional capital repositions across business cycle phases, covers the Relative Rotation Graph signals that precede official data confirmation, and includes the fund flow evidence needed to distinguish temporary rotation from structural reallocation.

The day’s moves, taken together, form a coherent pattern. Capital flowed toward AI infrastructure plays and away from a cybersecurity leader with strong results, revealing a clear hierarchy in investor preferences as of 3 June 2026.

Broadcom offered a forward-looking data point. Shares gained approximately 1.5% during the session ahead of a fiscal Q2 2026 earnings announcement scheduled after the close. Analyst consensus, compiled by Visible Alpha and Zacks, projected revenue of approximately $22 billion (representing 47-52% year-over-year growth) and adjusted EPS near $2.39-$2.40. The prior quarter (Q1 FY2026) delivered revenue of $19.311 billion and 29% year-over-year growth. A conference call was scheduled for 5:00 p.m. ET on 3 June.

| Company | Direction | Driver | AI infrastructure link |

|---|---|---|---|

| Alphabet | Record capital raise | AI compute demand | Yes |

| Broadcom | Up ~1.5% | Earnings anticipation | Yes |

| Palo Alto Networks | Down ~5.8% | Sector rotation, GAAP loss | No |

| Anthropic | IPO filing | AI competitive positioning | Yes |

Three signals emerge from the day’s activity:

Every major move on 3 June traces back to the same mechanism. Understanding it converts a collection of headlines into a repeatable analytical framework.

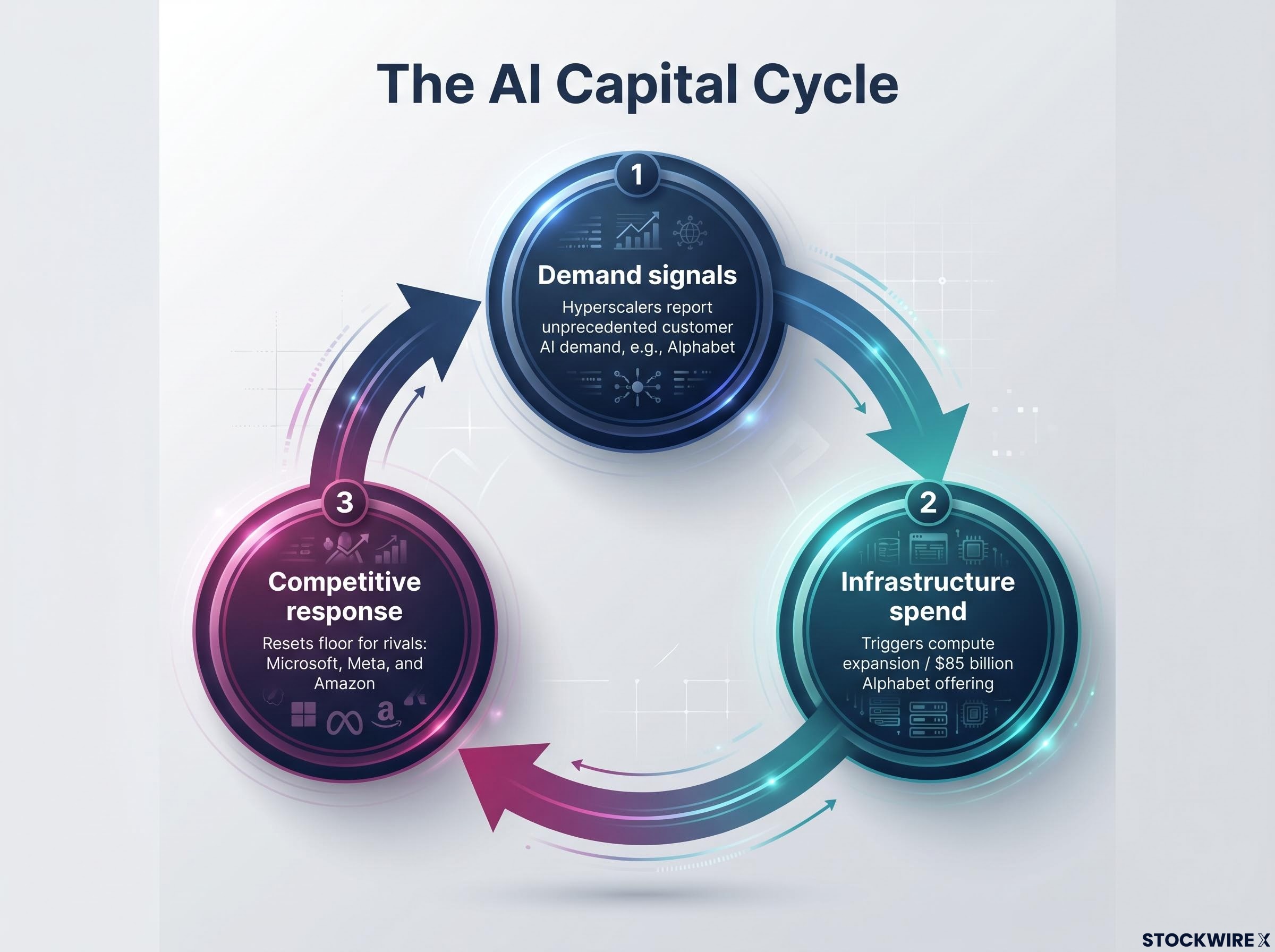

The AI capital cycle is the self-reinforcing loop in which hyperscaler AI demand drives semiconductor revenue, which validates further AI infrastructure investment, which raises competitive pressure on all hyperscalers to commit more capital.

Three stages define the cycle:

The Philadelphia Semiconductor Index’s nine positive closes in eleven sessions are a direct beneficiary signal from this cycle. Companies supplying the compute layer, chips, networking equipment, and cloud infrastructure, are rerated higher with each turn of the loop.

Palo Alto Networks illustrates the other side. A company competing for enterprise software and security budgets faces investor scrutiny even when reporting strong results, because the AI capital cycle is redirecting attention and, increasingly, capital allocation toward infrastructure enablers. The bifurcation is not temporary. It is structural, and it will persist for as long as hyperscaler AI demand continues to accelerate.

3 June 2026 was not a random set of disconnected market events. It was a coherent expression of how investors are allocating capital in the AI era: toward infrastructure enablers, away from sectors perceived as competing for the same enterprise budgets without a direct role in the compute buildout.

Three signals carry forward. AI infrastructure companies hold a valuation premium that persists on down days for the broader sector. The Anthropic filing signals that public market pricing for AI-native companies is approaching, which will establish benchmarks institutional investors currently lack. And strong cybersecurity earnings, as Palo Alto demonstrated, are not yet sufficient to override sector rotation pressure when the AI capital cycle is pulling capital elsewhere.

Broadcom’s after-close earnings report on 3 June will test whether the AI infrastructure premium holds under the scrutiny of actual results, making it the next data point to watch.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

The AI capital cycle is a self-reinforcing loop in which hyperscaler AI demand drives semiconductor revenue, which validates further infrastructure investment, which raises competitive pressure on all hyperscalers to commit more capital. This cycle is currently acting as a sector selection mechanism, rewarding AI infrastructure companies and pressuring those outside the compute buildout.

Alphabet raised approximately $85 billion, the largest equity capital event in market history, to meet what the company described as unprecedented customer AI demand. The raise comprised $30 billion in underwritten offerings, a $40-50 billion at-the-market programme, and a $10 billion strategic commitment from Berkshire Hathaway.

Palo Alto Networks fell approximately 5.8% on 3 June 2026 despite beating revenue and earnings estimates and raising guidance, driven by a GAAP net loss, concerns over hardware demand sustainability, profit-taking, and sector rotation as investors shifted capital toward AI infrastructure companies and away from pure-play cybersecurity names.

Anthropic's confidential S-1 filing with the SEC on 1 June 2026 placed it ahead of OpenAI in the formal steps toward a U.S. public listing, signalling that the private AI ecosystem is preparing to price itself in public markets. A fall 2026 listing is possible, though the timeline remains subject to SEC review and market conditions.

The Philadelphia Semiconductor Index was on pace for its ninth positive close in eleven sessions on 3 June 2026, even as the S&P 500 technology sector snapped a four-session winning streak. Analysts attributed semiconductor resilience to ongoing hyperscaler spending commitments validating demand for AI compute infrastructure.