Trump Tears Up Iran Deal as Oil and Rate Markets Reprice

14 mins ago

On April 29, 2026, Regeneron reported its first-quarter earnings, delivering a massive $3.6 billion in revenue that immediately clashed with an unexpected margin downgrade. The market reaction highlighted the complexity of the current financial quarter, as investors weighed strong sales against rising production costs. The biotechnology firm is navigating two major transitions simultaneously, steering a product portfolio shift while managing the fallout from a temporary manufacturing disruption.

Evaluating the Regeneron stock trajectory requires looking past the immediate headline numbers to understand the operational realities on the ground. This analysis breaks down the underlying operational drivers shaping the company’s valuation for the remainder of 2026. Investors will find a detailed assessment of the core franchise transition, the global growth engines, and the specific production headwinds affecting immediate profitability. Understanding these elements is essential for accurately pricing the company’s forward-looking risk profile.

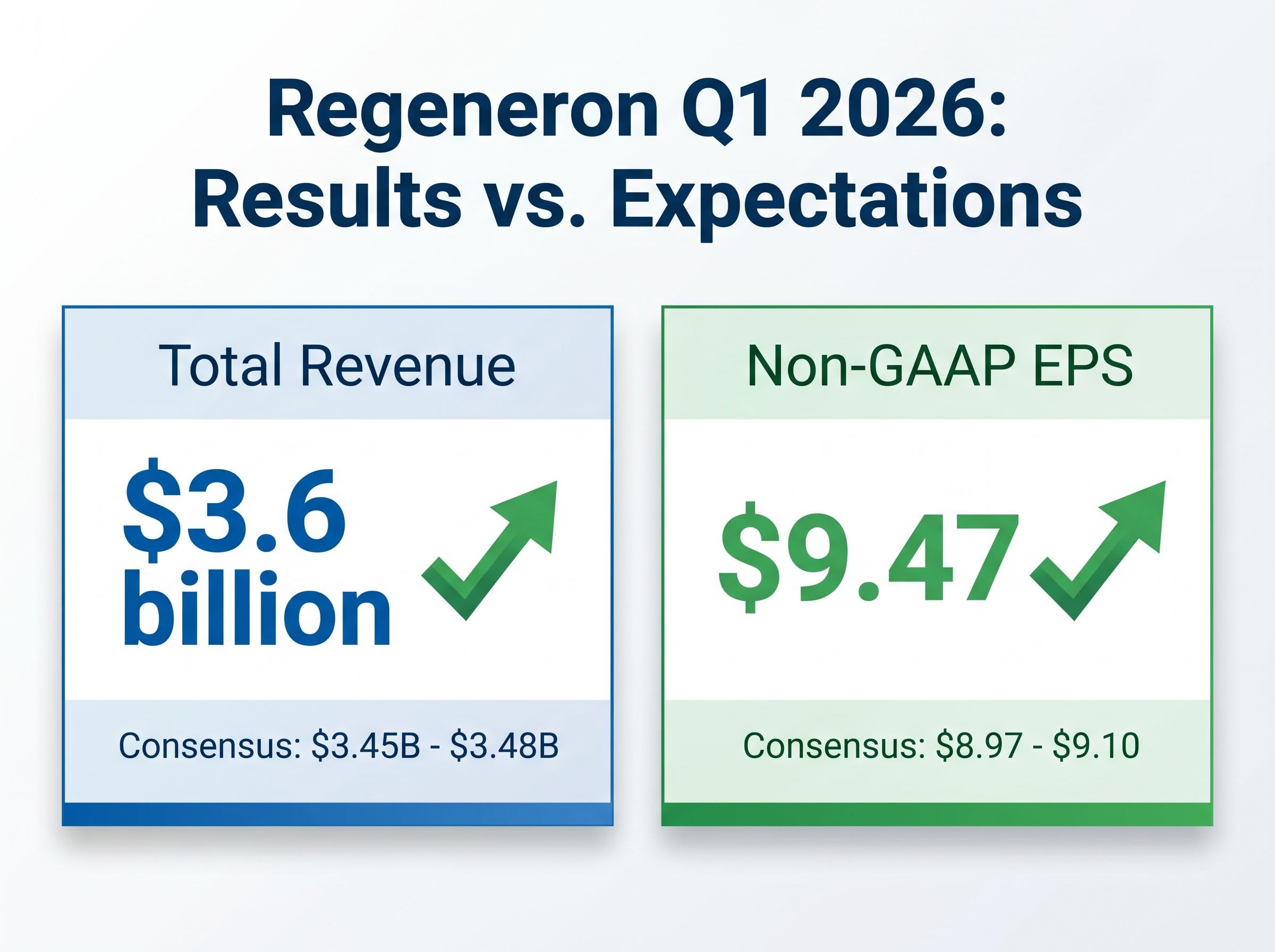

The first quarter presented a clear division between revenue generation and operating costs. Total revenue reached $3.6 billion, representing a 19% year-over-year increase that comfortably beat consensus estimates of $3.45 billion to $3.48 billion. Non-GAAP earnings per share followed a similar positive trajectory.

The company reported non-GAAP EPS of $9.47, surpassing the $8.97 to $9.10 consensus expectations. This performance was achieved despite a specific accounting headwind during the quarter. A $102 million pre-tax in-process research and development charge reduced earnings per share by approximately $0.81, masking the true strength of the underlying cash flow.

Reviewing Regeneron’s Q1 2026 Form 8-K reveals the exact accounting mechanisms behind this acquired research expense, providing clarity on how one-time charges obscured the fundamental cash generation of the business.

Wall Street processed these mixed signals of high revenue against adjusted margin expectations in real time. The stock price experienced immediate volatility, dropping roughly 1% to 2% in early trading before stabilising near $751.37. This initial hesitation reflected the market recalibrating its financial models to account for the margin compression against the top-line beat.

Despite the early trading volatility, institutional sentiment remains overwhelmingly positive. Major institutions, including Bank of America and Raymond James, maintained “Buy” and “Outperform” ratings respectively following the data release. Analysts are largely looking past the short-term margin dip to focus on the long-term momentum of the product portfolio.

Analyst Consensus Post-earnings evaluations confirm that the broader market perspective remains positive, with 27 analysts maintaining a “Buy” rating and establishing an average price target near $886.

Product lifecycle management is a critical mechanism in the pharmaceutical industry. When a blockbuster therapy approaches the end of its patent exclusivity, companies must actively transition patients to next-generation formulations to protect future cash flows. For Regeneron, this means defending against incoming biosimilar competition expected to accelerate in the second half of 2026.

Many retail investors observe declining total franchise revenue and assume the core business is failing. However, cannibalising a legacy product with an improved version is a highly successful defensive strategy. The newer high-dose formulation is currently capturing patients who are rotating away from the legacy treatment, keeping the revenue within the corporate ecosystem.

The transition mechanics are highly visible in the first-quarter data. Eylea HD U.S. net sales reached exactly $468 million, marking a 52% year-over-year increase. Concurrently, legacy Eylea U.S. net sales fell by 36% to $473 million. Total U.S. Eylea sales for the quarter were $941 million, representing a 10% year-over-year decline.

Analysts accept this overall franchise revenue decline because the high-dose adoption rate is accelerating rapidly. The internal shift from the legacy product to the high-dose variant builds a defensive moat against generic alternatives. The transition proves that management can successfully migrate a vast patient population to a protected asset.

While Regeneron focuses on defending its market share in mature indications, other ophthalmic developers are advancing new therapies for rare blinding conditions by securing novel registrational trial designs from the FDA.

| Product | Q1 2026 U.S. Sales | YoY Growth | Strategic Role |

|---|---|---|---|

| Eylea HD | $468 million | +52% | Next-generation growth driver |

| Legacy Eylea | $473 million | -36% | Maturing asset facing competition |

| Total Franchise | $941 million | -10% | Overall market share defence |

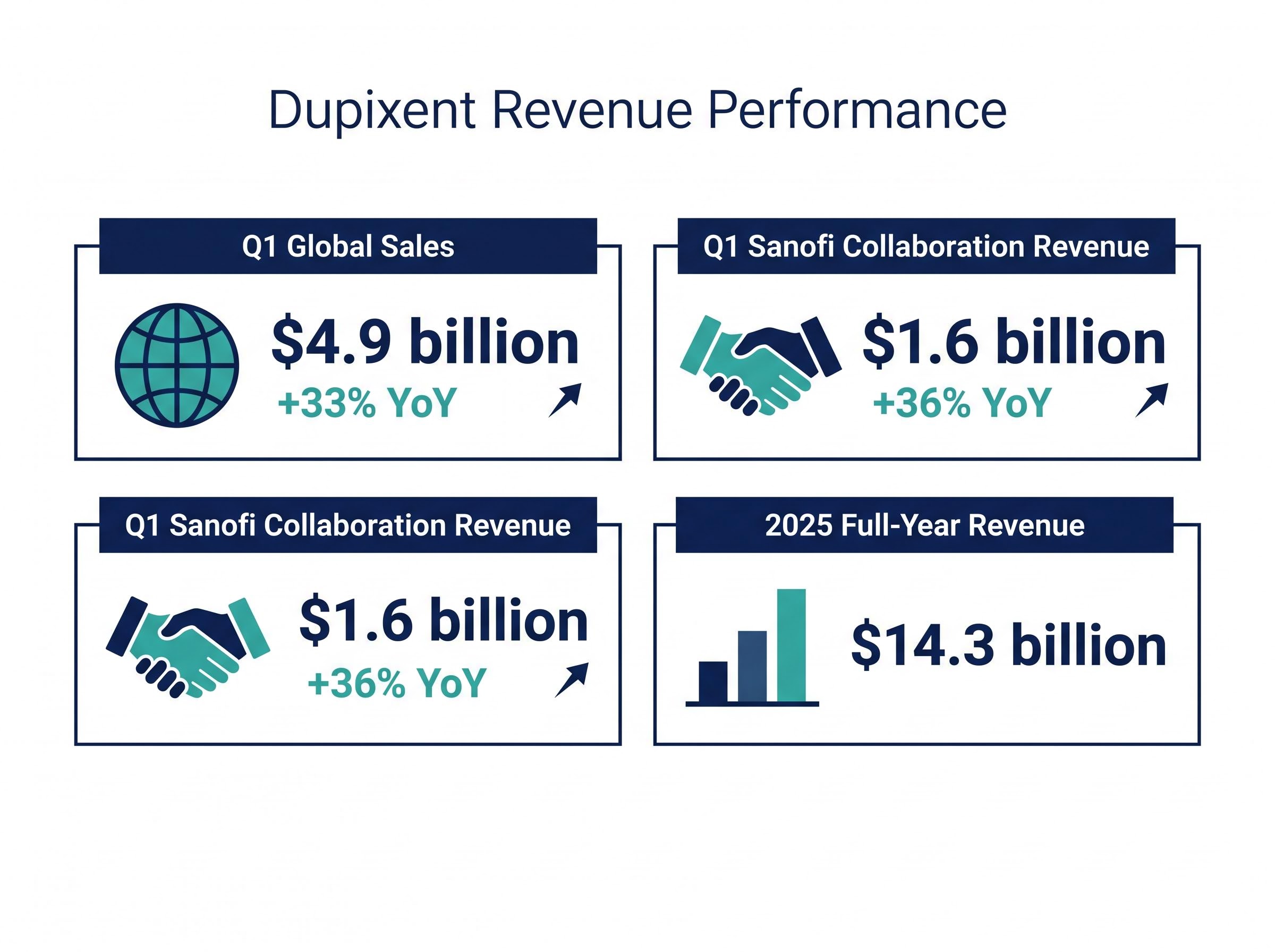

While the vision portfolio undergoes its necessary transition, the company possesses a reliable growth engine in its immunology partnership. The sheer scale of the Sanofi collaboration effectively offsets the 10% decline in the U.S. vision franchise. This therapeutic diversification reassures the market that the business is not overly reliant on a single aging asset class.

Global Dupixent sales were confirmed at $4.9 billion for the first quarter, representing a 33% year-over-year expansion. This exceptional performance drove collaboration revenue from Sanofi to $1.6 billion, up 36% from the previous year. This trajectory builds upon the 2025 full-year Dupixent revenue of $14.3 billion, confirming the asset’s status as a global pharmaceutical anchor.

This product line acts as the foundational stabiliser for the overall corporate valuation. Sustained demand is supported by three primary drivers:

Accelerating market penetration across broad U.S. patient populations. Ongoing regulatory label expansions into new therapeutic indications. * Strong clinical data access partnerships that validate long-term efficacy.

These operational factors ensure Dupixent remains the primary mechanism for aggregate revenue expansion. The drug’s predictable growth curve allows analysts to model future cash flows with a high degree of confidence.

The recent FDA approval of Dupixent for young children with chronic spontaneous urticaria perfectly illustrates this ongoing label expansion strategy, unlocking a new pediatric demographic to drive sustained prescription volumes.

The most heavily scrutinised aspect of the first-quarter report was the gross margin guidance reduction. Margin compression is typically a major red flag for institutional investors, often signalling pricing power weakness or structural market share loss. However, the current situation is rooted entirely in physical logistics rather than demand failure.

During the first quarter of 2026, the company experienced a temporary interruption of bulk manufacturing at its Limerick, Ireland facility. This unanticipated stoppage forced the company to discard raw inventory and absorb unallocated overhead costs. Consequently, the Q1 2026 GAAP gross margin dropped.

Management addressed this operational hiccup by lowering full-year 2026 GAAP gross margin guidance to 77-78%, down from the previous 79-80% expectation. The interruption was strictly limited to bulk manufacturing and did not impact the availability of commercial products for patients. The supply chain remained completely insulated from the factory floor disruptions.

Operations successfully restarted in the second quarter of 2026, with full output normalisation expected by the end of June. Explaining the physical, temporary nature of this compression helps the market accurately price the risk into investment models. The guidance reduction reflects an isolated event rather than a permanent degradation of the company’s earning power.

For investors looking to explore how the broader biotechnology industry is addressing structural production bottlenecks, our detailed coverage of automated cell therapy manufacturing examines new platforms designed to increase throughput and eliminate supply chain vulnerabilities.

Corporate capital allocation provides direct insight into management’s internal confidence regarding future cash flows. The company deployed an aggressive share repurchase strategy during the first quarter, purchasing common equity. Furthermore, the board authorised a massive new $3.0 billion share repurchase programme in April 2026.

Share buybacks provide a direct floor to equity valuations, rewarding shareholders with excess capital while reducing the outstanding float. This financial engineering bridges the gap to the next generation of therapeutics. It signals to the market that management believes the stock is undervalued relative to its long-term cash generation potential.

Simultaneously, the firm continues to fund extensive clinical evaluation. Research and development spending remains high despite the temporary margin pressures out of Ireland. Management is actively allocating capital across two primary pillars:

This dual approach presents a definitive signal of corporate resilience. The company is generating enough cash to simultaneously buy back stock and fund a massive research operation.

Beyond internal development, Regeneron is aggressively expanding its oncology footprint through external deals, highlighted by a recently established radiopharmaceutical partnership with Telix Pharmaceuticals to target solid tumours.

The April 2026 earnings report reveals a company successfully managing complex internal and external forces. The successful EYLEA rotation demonstrates proactive product management, while the unstoppable Dupixent engine provides reliable financial ballast. The margin compression, while notable, is a contained, temporary physical issue rather than a systemic pricing failure.

The ultimate test of the high-dose transition strategy will arrive in late 2026. Upcoming biosimilar competition will challenge the legacy portfolio’s remaining market share, requiring the next-generation formulation to accelerate patient capture. The current data suggests the company is well-positioned to absorb this impact while continuing to grow its top line.

Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Regeneron is transitioning patients from its legacy Eylea treatment to the newer, high-dose Eylea HD formulation to defend against upcoming biosimilar competition and protect future revenue streams. This move is a strategic defense against generic alternatives.

Regeneron's Q1 2026 gross margin guidance dropped due to a temporary bulk manufacturing interruption at its Limerick, Ireland facility, which led to discarded inventory and unallocated overhead costs. This operational hiccup was temporary, with full output normalisation expected by the end of June 2026.

Dupixent acts as a foundational stabilizer for Regeneron's corporate valuation, providing predictable and strong global growth that offsets the transition in the Eylea vision franchise. Its sustained demand and ongoing label expansions allow analysts to model future cash flows with high confidence.

Regeneron's aggressive share repurchase strategy, including a new $3.0 billion program, signals management's strong internal confidence in future cash flows and belief that the stock is undervalued. It provides a direct floor to equity valuations by reducing the outstanding share float.