S&P 500 Breaks 7,200 as Markets Shrug Off $126 Oil Spike

44 mins ago

Parsons Corporation (NYSE: PSN) reported a top-line revenue contraction in its first-quarter 2026 earnings, yet the equity market absorbed the news without a sell-off. The gap between a surface-level revenue drop and a resilient stock price reveals how institutional investors are pricing this specific contractor. A thorough Parsons stock analysis requires looking past headline figures to evaluate the underlying operational metrics that dictate future cash flows. Record margins, strategic acquisitions, and an expanding pipeline of national security contracts are actively offsetting immediate volume pressures. The market is increasingly pricing the company based on the high-margin business it is acquiring, rather than the legacy contracts it is completing.

Wall Street typically penalises companies for top-line revenue misses, but the market reaction to Parsons on 29 April 2026 told a different story. The stock closed at $51.84, securing a 0.66% gain following an earnings release that featured an adjusted earnings per share (EPS) of $0.79. This result outperformed the $0.69 analyst consensus and insulated the equity from the immediate optics of a revenue decline. The market priced in the quality of the earnings over the raw volume.

According to reports, total first-quarter revenue came in at $1.5 billion, representing a 4% drop year-on-year. The contraction stemmed directly from the scheduled roll-off of a highly specific, classified fixed-price agreement within the Federal Solutions segment. According to reports, when analysts exclude this specific classified contract from the calculation, organic revenue actually increased by 8%.

The true driver of the stock’s stability was aggressive margin expansion. According to reports, adjusted EBITDA reached $151 million, with profitability widening by half a percentage point to a record 10.1%. According to reports, operating cash utilisation also improved markedly, dropping to $4 million from the $12 million consumed in the first quarter of 2025. This cash management efficiency provides the management team with increased capital flexibility to pursue further accretive acquisitions.

The official Q1 2026 financial results confirm this margin expansion strategy, demonstrating how the management team successfully translated a lower top-line volume into record operational profitability.

| Financial Metric | Q1 2026 Result | Analyst Consensus | Year-on-Year Change |

|---|---|---|---|

| Total Revenue | $1.5 billion | According to reports, $1.55 billion | Down 4% |

| Adjusted EPS | $0.79 | $0.69 | According to reports, up 14.5% |

| Adjusted EBITDA | $151 million | $142 million | Up 1.5% |

| Profitability Margin | 10.1% | 9.6% | Up 0.5% |

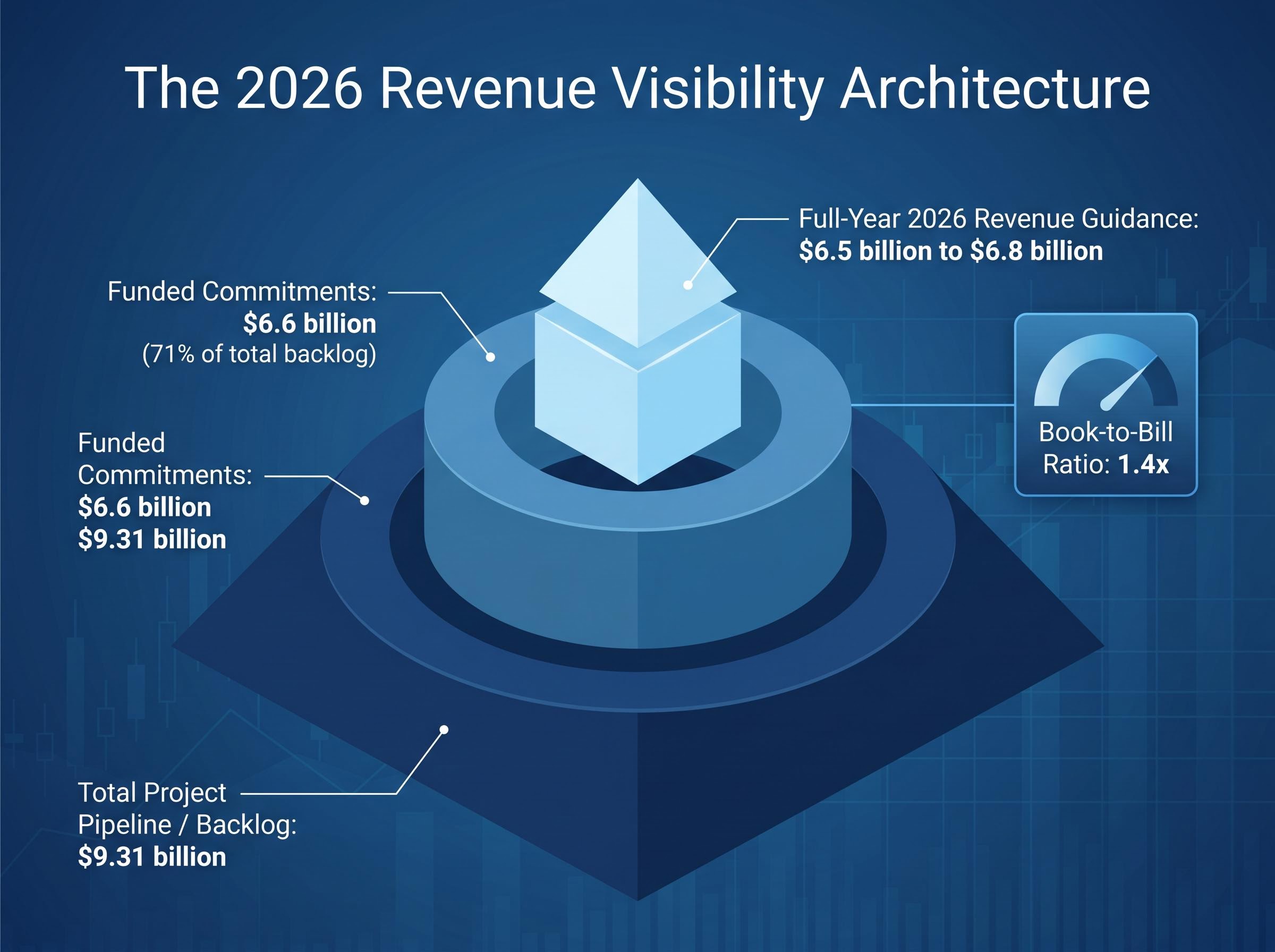

The commercial market values government contractors based on future revenue visibility rather than past quarterly performance. Parsons secured $2.1 billion in new contract acquisitions during the first quarter of 2026, shifting the analytical focus entirely toward forward-looking indicators. Management reported a 1.4x book-to-bill multiple across all operating units. Achieving a multiple of this size is a powerful indicator of accelerating future growth, as it confirms the company is acquiring new business significantly faster than it is completing existing work.

The total project pipeline reached a record $9.31 billion, up from $9.07 billion in the previous year. However, institutional investors distinguish clearly between total pipeline opportunities and concrete financial guarantees. Funded commitments reached a record $6.6 billion in the quarter, representing 71% of the total backlog. This high conversion rate from pipeline to funded status validates the quality of the bidding strategy.

Understanding how these specific metrics dictate stock valuation requires defining the three core layers of government contracting finance:

Book-to-Bill Ratio: This metric divides the value of newly awarded contracts by the revenue billed during the same period. A ratio above 1.0x signals expansion, making the 1.4x result a clear indicator of sustained future revenue generation. Total Backlog: This represents the absolute maximum potential value of all awarded contracts, including unexercised option years that the government may or may not fund. It serves as a ceiling for potential long-term earnings. * Funded Commitments: This is the portion of the backlog where government agencies have already appropriated and legally committed the capital. It provides a guaranteed floor for future cash flows and is the primary metric analysts use to calculate valuation floors.

For investors looking to compare these metrics against industry peers, our comprehensive walkthrough of defense contractor valuation examines how mid-tier firms stack up against major players like Booz Allen Hamilton when assessing book-to-bill momentum and funded obligations.

Revenue visibility only provides downside protection if the underlying contracts are secure and highly profitable. The $2.1 billion booking surge in the first quarter reveals a calculated strategic pivot toward high-margin national security domains. Parsons is actively targeting areas where federal spending remains insulated from broader macroeconomic pressures.

These current macroeconomic pressures include a severe K-shaped consumer dynamic where soaring energy costs are rapidly depleting household savings, prompting institutional investors to pivot towards government-backed revenue streams.

This strategic realignment is evident in the specific programmatic quality of the new business pipeline. The company is securing bids in the most technically demanding sectors of government operations, including highly classified data intelligence networks. Management accelerated this exposure by closing the Altamira acquisition for a $349.5 million purchase price. This acquisition directly bolsters the company’s capabilities in space and cyber intelligence, areas that command higher margin premiums than traditional federal IT services.

The top first-quarter contract wins highlight this exact operational focus and demonstrate the scale of capital involved:

Parsons reaffirmed its full-year 2026 guidance, projecting between $6.5 billion and $6.8 billion in total revenue. The company also maintained its adjusted EBITDA guidance of $615 million to $675 million, alongside projected operating cash flows of $470 million to $530 million. Assessing the probability of management hitting these mid-point estimates requires mapping the company’s targets against macro federal spending priorities.

The broader funding environment completely supports the company’s backlog conversion targets. The fiscal year 2026 US national defence budget request sits at $1.01 trillion, representing a 13% increase over enacted levels from 2025. This historic allocation de-risks the company’s forward projections by providing massive structural tailwinds in the exact sectors Parsons is targeting. Specifically, the budget emphasises advanced cyber capabilities, artificial intelligence integrations, and space command infrastructure.

A recent CSIS defense budget analysis projects these allocations will continue growing aggressively into fiscal year 2027, further cementing the structural tailwinds supporting national security contractors over the next development cycle.

Executive Sentiment on Business Durability “Our record backlog and sustained book-to-bill momentum provide us with unparalleled confidence in our 2026 revenue projections. The strategic alignment between our recent contract acquisitions and the accelerating federal defence budget ensures long-term operational durability.”

While national security provides the primary growth vector, the Critical Infrastructure segment acts as a secondary stabilisation engine. This division delivered 3% revenue growth alongside a healthy 10.8% EBITDA margin during the first quarter.

The combination of domestic municipal projects and massive international transportation contracts provides a direct hedge against potential US defence budget delays. If congressional gridlock slows domestic military appropriations, the international infrastructure pipeline ensures the company continues generating reliable operating cash flow. This dual-engine structure creates a highly defensive portfolio capable of weathering isolated sector downturns.

The first quarter of 2026 demonstrates that margin expansion and record backlogs hold far more weight than temporary top-line revenue fluctuations. The equity market absorbed the optical decline in revenue because the underlying financial architecture of the company is fundamentally stronger than it was a year ago. By maintaining a sharp focus on operational efficiency, Parsons managed to widen its profitability margin to an impressive 10.1%.

The $6.6 billion in funded commitments sets a concrete operational floor for financial performance through the remainder of 2026. This guaranteed capital protects investors from short-term federal spending disruptions and establishes clear earnings visibility. Furthermore, the integration of the Altamira acquisition combined with a sector-leading 1.4x book-to-bill ratio positions the stock for sustained forward momentum.

The push for specialized intelligence capabilities has triggered a broader wave of federal cyber security acquisitions globally, as IT service providers look to buy established sovereign relationships rather than build them organically.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The book-to-bill ratio divides the value of newly awarded contracts by the revenue billed during the same period, with a ratio above 1.0x signaling business expansion.

Parsons' stock rose due to an adjusted EPS beat, record 10.1% profitability margins, and robust future revenue visibility from new contract acquisitions, offsetting the optical revenue decline.

Parsons is strategically targeting high-margin national security domains, including cyber intelligence, space command infrastructure, and critical infrastructure projects, supported by a significant federal defence budget.

Funded commitments represent the portion of a contractor's backlog where capital is already appropriated and legally committed, providing a guaranteed floor for future cash flows and serving as a primary metric for valuation floors.