When to Buy Tech: Evaluating the Case for Patience vs. Action

Key Takeaways

- XLK has surged 18% since 30 March and the Nasdaq has reached record highs, yet Société Générale recommends waiting until Q1 2027 for aggressive tech re-entry based on free cash flow trajectory signals.

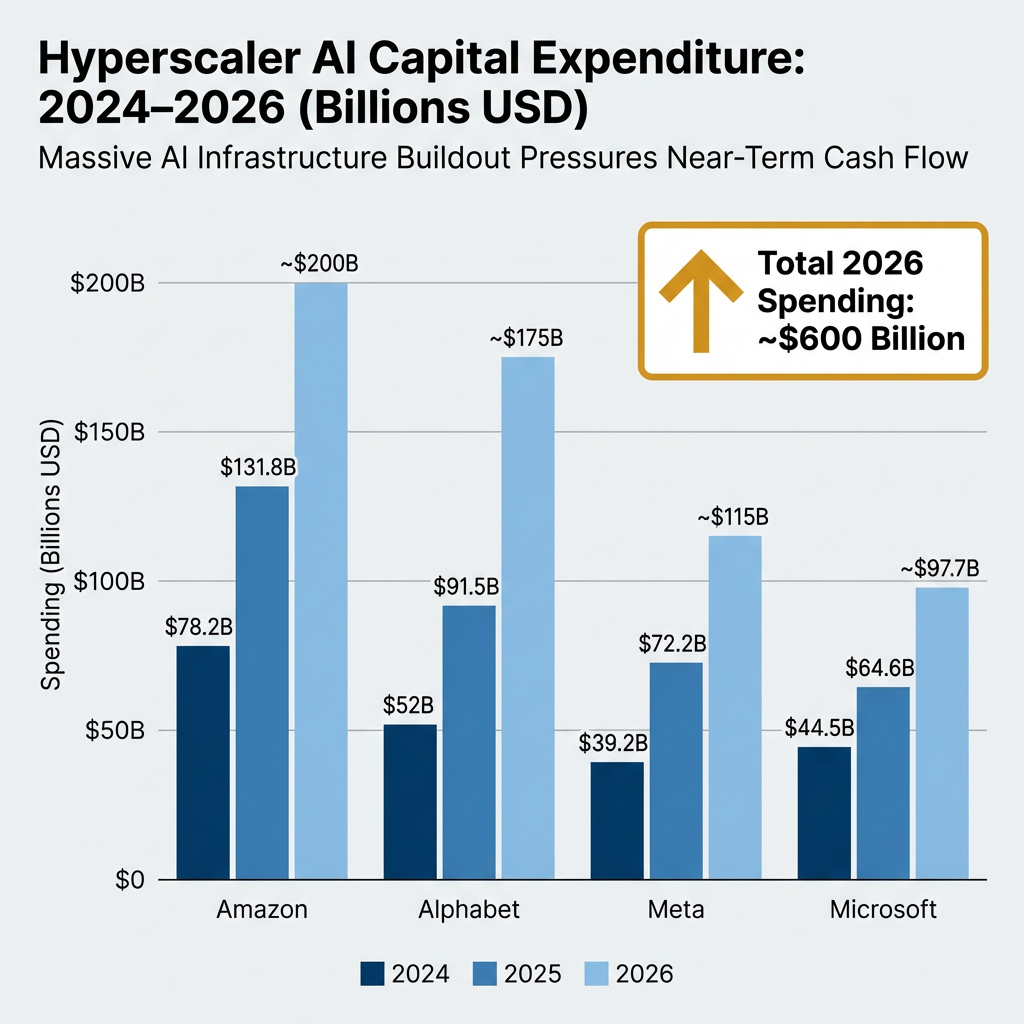

- Hyperscalers including Amazon, Alphabet, Meta, and Microsoft are projected to deploy approximately $600 billion in AI infrastructure during 2026, nearly double their 2025 expenditure, pressuring near-term free cash flow metrics.

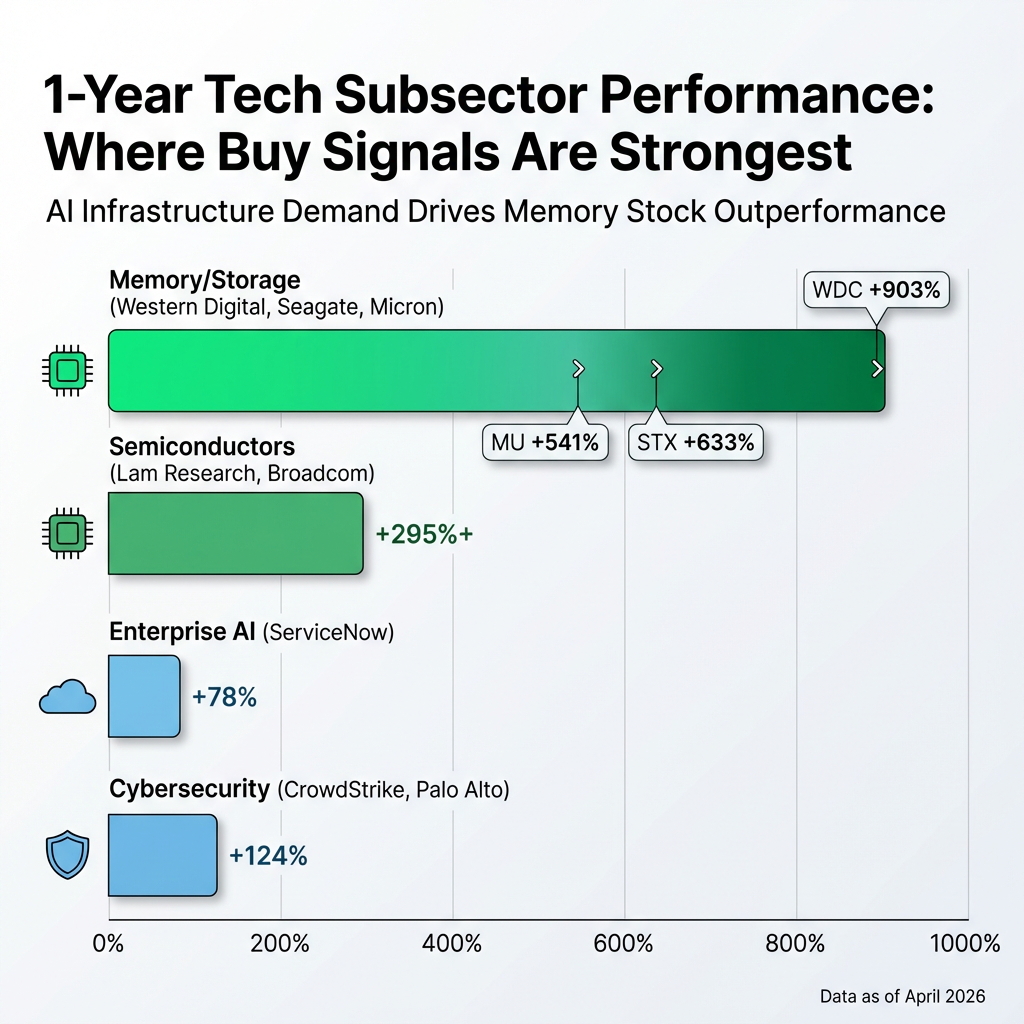

- Memory and semiconductor subsectors show the strongest buy signals, with Micron projecting 604% EPS growth, a forward P/E of 7.83, and one-year price gains of up to 903% for Western Digital.

- NVIDIA has committed over $4 billion through AI partnerships with Nebius and Marvell, signalling multi-year infrastructure investment visibility extending through 2030 that supports contrarian accumulation strategies.

- Investors can choose between two legitimate frameworks: patient accumulation awaiting Q1 2027 free cash flow confirmation, or contrarian positioning in quality names showing triple-digit growth and technical support entry points.

The technology sector stands at a critical inflection point in April 2026, with the Nasdaq reaching record highs whilst institutional strategists counsel patience. The Technology Select Sector SPDR Fund (XLK) has surged 18% since 30 March, yet Société Générale’s chief US equity strategist identifies Q1 2027 as a more favourable entry window for aggressive sector allocation. This divergence raises a fundamental question for investors: when to buy tech stocks in an environment where $600 billion in hyperscaler AI infrastructure spending creates both exceptional growth potential and near-term balance sheet pressure.

Determining optimal timing requires moving beyond sentiment-driven decisions to evaluate specific quantitative indicators. Hyperscaler free cash flow trajectories, capital expenditure-to-revenue ratios, and individual stock fundamentals now serve as the primary signals institutional analysts monitor. With AI infrastructure buildout extending through 2030 according to recent partnership announcements, investors face a choice between accumulating during current volatility or awaiting clearer monetisation evidence expected in early 2027.

Tech Stock Timing Enters Critical Phase as AI Spending Reshapes Valuations

The technology sector presents investors with a timing paradox in April 2026. Whilst XLK has delivered an 18% gain since late March and the Nasdaq has reached new record levels, Manish Kabra, chief US equity strategist at Société Générale, recommends holding off on aggressive tech re-entry until Q1 2027. This institutional caution stands in contrast to contrarian voices advocating immediate accumulation in quality names trading below technical support levels.

Understanding the multiple factors driving current tech valuations beyond AI infrastructure spending—including geopolitical risk reduction and broader market sentiment shifts—provides essential context for evaluating whether record highs represent sustainable strength or overextension.

The stakes are considerable. Major hyperscalers are projected to deploy approximately $600 billion in AI infrastructure during 2026, roughly double their 2025 expenditure. This unprecedented capital deployment creates both opportunity and timing risk. On one hand, massive spending depresses near-term free cash flow metrics that institutional strategists use as buy signals. On the other, triple-digit earnings growth projections in semiconductor and memory stocks suggest fundamental value creation is accelerating.

Understanding the monetisation challenges facing hyperscalers deploying capital at unprecedented scale requires examining the risks associated with $600 billion in annual AI infrastructure spending and whether revenue growth can justify these investments.

Investors seeking to answer when to buy tech stocks must therefore examine the specific indicators that differentiate opportunistic entry from premature positioning. The following analysis evaluates free cash flow trajectories, capex-to-revenue improvements, earnings growth signals, and technical indicators to help readers determine their optimal timing strategy based on individual risk tolerance and investment horizon.

When big ASX news breaks, our subscribers know first

Understanding Tech Stock Buy Signals: Key Metrics That Matter

Successful timing of technology stock purchases relies on measurable signals rather than sentiment or speculation. Professional investors track specific quantitative indicators that provide objective frameworks for entry decisions, particularly relevant given conflicting expert opinions about optimal positioning in April 2026.

Four primary categories of buy signals guide institutional timing strategies:

The SEC Regulation S-K Item 303 disclosure requirements for capital expenditures mandate how publicly traded hyperscalers report their AI infrastructure spending and liquidity positions in quarterly filings, providing investors with standardized metrics to evaluate the $600 billion deployment discussed throughout this analysis.

- Hyperscaler free cash flow measures aggregate cash generation after capital expenditures across major cloud and AI companies, signalling balance sheet health and investment sustainability

- Capital expenditure-to-revenue ratio tracks whether AI infrastructure spending translates into revenue growth, identified by Société Générale as the most critical monetisation indicator

- Earnings growth projections capture forward EPS estimates that signal fundamental value creation, particularly relevant for semiconductor names showing triple-digit growth rates

- Technical levels identify price points such as 200-week moving averages that indicate historical support zones for potential entry

The NBER research validating moving averages as equity timing indicators demonstrates peer-reviewed evidence that 200-day technical levels historically identify support zones that reduce downside risk for equity positioning, providing academic backing for the Microsoft 200-week MA entry point discussed in the contrarian case.

These metrics matter specifically in 2026‘s AI-driven market because massive infrastructure spending has temporarily depressed free cash flow whilst potentially setting up future earnings acceleration. Hyperscalers are channelling unprecedented capital into data centre buildout, chip procurement, and AI system deployment. This creates a timing challenge: near-term cash flow pressure may persist through year-end 2026, yet the same spending positions these companies for substantial revenue growth as AI monetisation accelerates.

> Critical Timing Indicator

> “The capex-to-sales ratio is the single most critical indicator to track,” according to Manish Kabra, Société Générale, 16 April 2026.

Understanding these frameworks enables investors to evaluate whether current market conditions favour immediate accumulation or strategic patience. The institutional perspective examined in subsequent sections applies these metrics to current hyperscaler spending patterns and forward earnings trajectories.

The Patient Approach: Why Société Générale Recommends Waiting Until 2027

Despite XLK‘s 18% rally and the Nasdaq reaching record highs, Manish Kabra maintains a contrarian stance against immediate aggressive tech re-entry. Société Générale’s chief US equity strategist identifies Q1 2027 as a more favourable window, basing this timeline on two specific quantitative signals rather than qualitative valuation concerns.

Kabra’s primary thesis centres on hyperscaler free cash flow trajectories. Aggregate free cash flow across major AI infrastructure spenders has declined on a quarterly basis since early 2024 due to massive capital expenditures. His projection indicates this metric will turn negative by year-end 2026 before recovering in Q1 2027.

> Institutional Buy Signal

> “A positive inflection in free cash flow would generate a strongly bullish outlook for technology equities,” stated Manish Kabra, Chief US Equity Strategist at Société Générale, April 2026.

This patient approach reflects a disciplined wait for measurable improvement rather than attempting to time a bottom. The hyperscaler cohort extends beyond the traditional quartet of Amazon, Alphabet, Meta, and Microsoft to include Oracle, Salesforce, CoreWeave, Nebius, and other major AI infrastructure investors.

| Hyperscaler | 2024 Capex | 2025 Capex | 2026 Estimated Capex |

|---|---|---|---|

| Amazon | $78.2B | $131.8B | ~$200B |

| Alphabet | $52B | $91.5B | ~$175B |

| Meta | $39.2B | $72.2B | ~$115B |

| Microsoft | $44.5B | $64.6B | ~$97.7B |

Kabra’s second key metric, the capex-to-sales ratio, reflects whether hyperscalers are generating adequate returns on AI investments. With $600 billion in projected 2026 spending (double 2025 levels), meaningful improvement in this ratio is anticipated by Q1 2027 as revenue from AI services begins matching the scale of infrastructure investment. Until this ratio demonstrates clear improvement, Kabra maintains that the cap-weighted S&P 500 will struggle to surpass 7,000 given technology’s 32% sector weighting.

The Contrarian Case: Why Some Analysts Say Buy Tech Stocks Now

Prominent analysts and investors advocate immediate accumulation despite volatility, arguing that exceptional fundamental catalysts justify current entry rather than waiting for perfect timing signals. This bullish perspective gained traction during extreme fear periods over the past four weeks, which created selective buying opportunities in quality names with strong competitive positioning.

The fundamental case for immediate buying centres on measurable growth metrics that support current valuations:

- Exceptional earnings growth with Micron projecting 604% EPS growth alongside 194% sales growth and a forward P/E of just 7.83

- Major investment catalysts including NVIDIA‘s $4 billion+ commitments through partnerships with Nebius ($2 billion for 5+ gigawatts of AI systems by 2030) and Marvell ($2 billion for AI chip development)

- Revenue execution demonstrated by Applied Digital beating revenue estimates by 66% with 139% year-over-year growth, signalling AI data centre strength

- Technical entry points with Microsoft trading below its 200-week moving average, presenting a historical support entry opportunity

Wall Street maintains Strong Buy consensus on select technology names, with TipRanks and Zacks assigning ratings that imply 50-70%+ upside targets based on fundamental growth trajectories. The argument emphasises that AI infrastructure buildout represents a multi-year trend extending through 2030 according to the NVIDIA-Nebius partnership timeline, making current volatility an entry opportunity rather than a warning signal.

Corporate buyback programmes further signal management confidence in current valuations. When combined with triple-digit earnings growth projections for semiconductor leaders and substantial AI investment announcements, contrarian investors view near-term free cash flow pressure as a temporary condition rather than a fundamental deterioration. The 604% projected EPS growth for Micron alone suggests that memory and semiconductor stocks are demonstrating clear monetisation of AI demand, justifying immediate accumulation for investors with appropriate time horizons.

The disconnect between record earnings and market reaction at semiconductor leaders demonstrates how semiconductor sector sentiment dynamics can diverge from fundamental performance, a critical consideration when evaluating contrarian entry strategies during volatility.

The next major ASX story will hit our subscribers first

Sector-Specific Timing: Where the Buy Signals Are Strongest

Technology stock timing varies significantly by subsector, with one-year performance data revealing concentrated strength in memory and semiconductors driven by AI infrastructure demand. Effective timing requires subsector-level analysis rather than treating technology as a monolithic investment category.

The divergence between software and semiconductor performance highlights why subsector-level analysis of software versus semiconductor performance matters when timing tech stock purchases, as memory stocks deliver triple-digit gains whilst broader software indices struggle.

| Subsector | Leading Names | Key Signal | 1-Year Performance |

|---|---|---|---|

| Memory/Storage | Western Digital, Seagate, Micron | AI demand + triple-digit EPS growth | +541% to +903% |

| Semiconductors | Lam Research, Broadcom | Chip deals + AI infrastructure | +295%+ |

| Enterprise AI | ServiceNow | 21.5% earnings growth, AI monetisation | Above market average |

| Cybersecurity | CrowdStrike, Palo Alto Networks | NVIDIA/Meta endorsements | High-growth ratings |

Memory stocks demonstrate the clearest buy signals, with Western Digital delivering +903% returns, Seagate gaining +633%, and Micron advancing +541% over the past year. These exceptional performances reflect AI workload demands for high-performance memory and storage solutions. Micron‘s 604% projected EPS growth combined with its forward P/E of 7.83 suggests valuation remains compelling despite the substantial price appreciation.

Enterprise AI and cybersecurity names show more moderate but sustainable growth signals. ServiceNow reports 14.8% revenue growth and 21.5% earnings growth driven by AI-powered enterprise solutions, demonstrating clear monetisation pathways. CrowdStrike and Palo Alto Networks benefit from NVIDIA and Meta endorsements in AI cybersecurity, positioning them to capture market share as AI infrastructure expands.

For investors cautious on concentrated technology exposure, Kabra offers an alternative: the equal-weighted S&P 500 (RSP ETF) tilts toward materials, industrials, and utilities benefiting from elevated US power demand. He characterises this as the closest proxy for US nominal growth, relevant for market participants seeking participation without concentrated tech timing risk.

Building Your Tech Stock Timing Framework

Determining when to buy tech stocks in April 2026 requires choosing between two legitimate institutional frameworks: patient accumulation awaiting Q1 2027 free cash flow recovery, or contrarian positioning capitalising on exceptional growth metrics and volatility-driven entry points. Neither approach is universally correct, as optimal timing depends on individual investment horizons and risk tolerance.

The patient approach favours investors prioritising balance sheet confirmation, lower drawdown risk, and hyperscaler monetisation proof. Key triggers include positive free cash flow inflection and improving capex-to-revenue ratios expected in Q1 2027. This strategy acknowledges that $600 billion in 2026 hyperscaler spending will pressure near-term cash generation before AI revenue streams reach scale.

Contrarian accumulation favours investors with longer time horizons who can tolerate near-term volatility. This framework targets names with triple-digit growth projections, technical support levels, and multi-year AI infrastructure tailwinds extending through 2030. The 604% projected EPS growth for Micron, NVIDIA‘s $4 billion+ partnership investments, and Applied Digital‘s 139% year-over-year revenue growth provide fundamental support for immediate entry in select subsectors.

Investors should monitor hyperscaler earnings reports for free cash flow trajectory changes, track capex-to-revenue improvements as Q1 2027 approaches, and evaluate individual name fundamentals including EPS growth and revenue execution for selective accumulation opportunities. The AI infrastructure buildout represents a multi-year cycle with visibility through at least 2030, providing context for both near-term patience and long-term conviction strategies.

> Disclaimer

> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Frequently Asked Questions

When is the best time to buy tech stocks in 2026?

Société Générale's chief US equity strategist recommends waiting until Q1 2027, when hyperscaler free cash flow is expected to turn positive and capex-to-revenue ratios should show meaningful improvement. However, contrarian analysts argue that triple-digit earnings growth in semiconductors and memory stocks justifies selective buying now.

What is the capex-to-revenue ratio and why does it matter for tech stock timing?

The capex-to-revenue ratio measures whether a company's infrastructure spending is generating proportional revenue growth, and Société Générale identifies it as the single most critical indicator for timing tech stock purchases. With hyperscalers projected to spend $600 billion on AI infrastructure in 2026, improvement in this ratio is not expected until Q1 2027.

Which tech subsectors have the strongest buy signals right now?

Memory and storage stocks show the clearest buy signals, with Western Digital up 903%, Seagate up 633%, and Micron up 541% over the past year, all driven by AI infrastructure demand. Micron's projected 604% EPS growth and forward P/E of 7.83 suggest valuation remains compelling despite significant price appreciation.

How does hyperscaler AI spending affect free cash flow for tech investors?

The $600 billion in projected 2026 hyperscaler AI infrastructure spending — double 2025 levels — is depressing aggregate free cash flow across Amazon, Alphabet, Meta, and Microsoft, with Société Générale projecting this metric could turn negative by year-end 2026. A positive free cash flow inflection in Q1 2027 is the key institutional buy signal to monitor.

Is Microsoft a buy right now based on technical indicators?

Contrarian analysts highlight that Microsoft is currently trading below its 200-week moving average, which historically represents a significant technical support level and potential entry point for long-term investors. Academic research validated by NBER supports the use of moving average levels as equity timing indicators that can reduce downside risk.