Financial Nihilism: Why Young Americans Chase Risky Bets

Key Takeaways

- Northwestern Mutual's 2026 study found 80% of financially disenchanted Gen Z Americans believe high-risk investments outperform traditional wealth-building methods.

- Gen Z investors are four times more likely to own cryptocurrency than a retirement account, reflecting a deliberate preference for speculative assets over conventional savings vehicles.

- Housing market exclusion is identified as a root cause of financial nihilism, with one-third of Gen Z reporting they never expect to own a home, directly driving higher allocation to risky investments.

- Youth unemployment rates of up to 10.8% for ages 16-24 make traditional investment vehicles inaccessible, leaving low-barrier mobile trading apps as the only viable option for many young adults.

- Experts recommend a three-tier policy response covering regulation modernisation, Gen Z-tailored financial education, and structural intervention on housing affordability and wage stagnation.

A fundamental shift is reshaping how young Americans approach money. According to Northwestern Mutual’s 2026 Planning and Progress Study, 73% of Americans who feel financially behind now believe high-risk investments outperform traditional wealth-building methods. Among Gen Z, that figure climbs to 80%, with millennials close behind at 75%.

The Rise of Financial Nihilism Among Young Americans

This phenomenon has a name: financial nihilism. It describes a documented disenchantment with conventional financial milestones such as homeownership, retirement planning, and steady career advancement. Rather than passive neglect, this represents active rejection of traditional paths that younger generations increasingly view as inaccessible.

The Northwestern Mutual data reveals broader economic pessimism driving these choices. 45% of respondents expect economic conditions to worsen in 2026, whilst 60% anticipate rising inflation. These expectations are shaping investment behaviour in measurable ways.

This generational shift fits within a broader pattern of speculative asset adoption that now encompasses nearly 4 in 10 Americans across all age groups, according to Northwestern Mutual’s 2025 Planning and Progress Study.

Gen Z investors are four times more likely to own cryptocurrency than a retirement account, according to YouGov research. This statistic captures the behavioural signature of financial nihilism: deliberate preference for speculative assets over conventional savings vehicles.

When big ASX news breaks, our subscribers know first

What Is Financial Nihilism and Where Did It Come From?

Financial nihilism represents fundamental disenchantment with traditional wealth-building milestones. The term describes outcomes rather than necessarily the underlying psychology. These individuals have not stopped wanting financial security. They have concluded that traditional paths will not deliver it.

Five core drivers fuel this phenomenon:

The energy-driven inflation dynamics of 2026, with headline inflation surging to 3.8% in March, create the precise economic conditions that make long-term saving appear futile to young Americans facing eroding purchasing power.

- Five consecutive years of inflation eroding purchasing power and making long-term saving feel futile

- Persistent economic uncertainty with 45% expecting conditions to worsen in 2026

- Traditional milestones becoming mathematically unattainable for median earners facing stagnating wages

- Institutional distrust following multiple economic crises that affected older generations differently

- Housing market exclusion creating a “why bother saving” psychology when the primary wealth-building vehicle appears permanently out of reach

Research from the University of Chicago and Northwestern University quantified the causal relationship. Lower perceived homeownership probability directly correlates with higher allocation to risky investments and increased consumption relative to wealth. This academic grounding elevates financial nihilism beyond social media buzzword status.

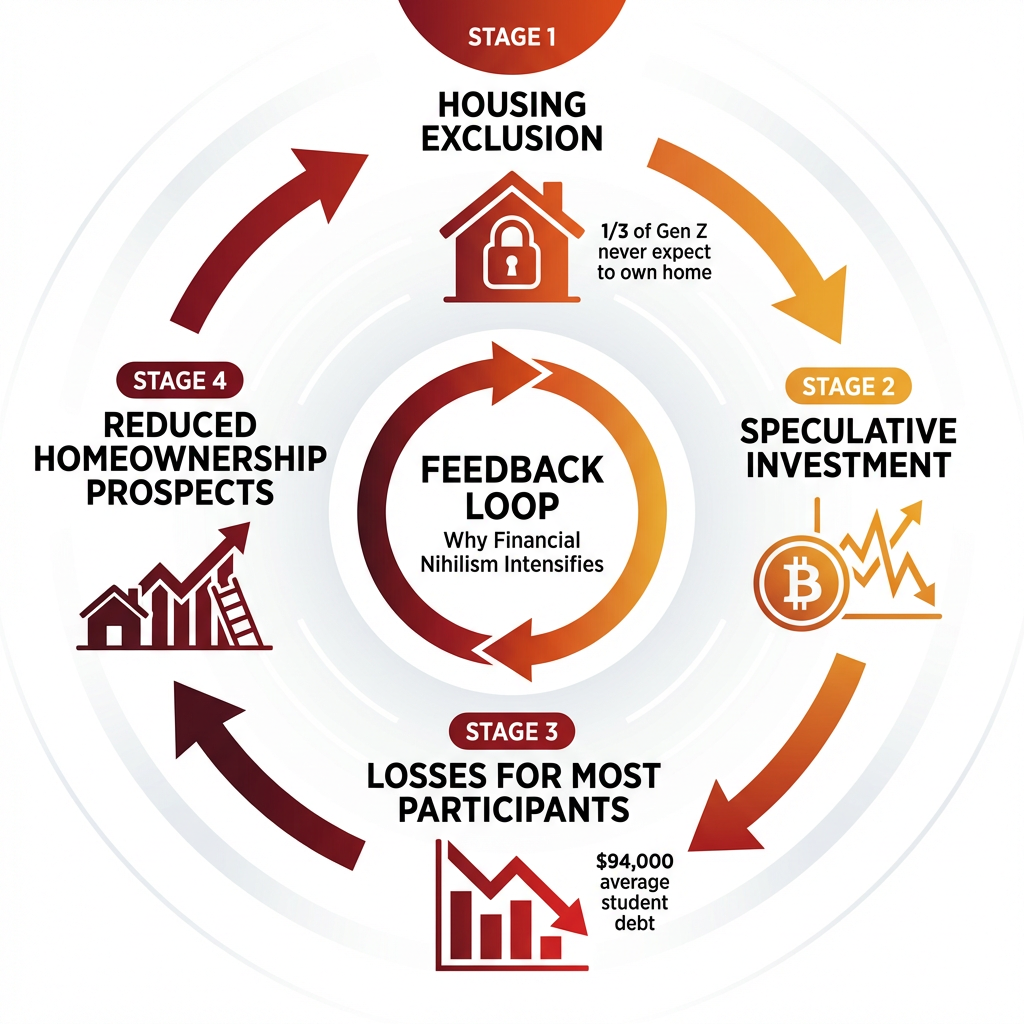

One-third of Gen Z report never expecting to own a home. When the primary traditional wealth-building vehicle appears permanently inaccessible, the entire framework of “responsible” financial behaviour loses its logical foundation.

How Young Americans Are Speculating: Crypto, Meme Stocks, and Prediction Markets

Young Americans are channelling this disenchantment into specific speculative vehicles. Cryptocurrency, meme stocks, options trading, sports betting, and prediction markets share common characteristics: low barriers to entry via mobile apps, potential for rapid gains, community elements, and no requirement for stable employment or existing wealth.

| Investment Type | Adoption Rate | Key Platforms | Primary Appeal |

|---|---|---|---|

| Cryptocurrency | 17% of Americans | Coinbase, Robinhood | 24/7 access, no minimum investment |

| Options Trading | 40-50% of volume from retail traders | Robinhood, TD Ameritrade | Leverage potential, amplified returns |

| Prediction Markets | Significant Gen Z and millennial participation | Kalshi, Polymarket | Event-driven speculation |

| Meme Stocks | Significant retail participation | Robinhood, Fidelity | Community-driven momentum |

Bloomberg data shows renters hold crypto at higher rates than homeowners with equivalent wealth. This finding directly connects housing exclusion to speculative behaviour. Cryptocurrency serves as a substitute wealth-building vehicle when real estate is inaccessible.

An accessibility paradox emerges from employment data. With nearly 8% unemployment for ages 22-27 and 10.8% for ages 16-24, barriers to traditional investment vehicles remain high. Employer-sponsored retirement accounts require stable employment. Down payments require consistent income. Speculative platforms have minimal requirements, making them the only available paths for many.

The extreme volatility inherent in commodity-linked speculation became evident on April 17, 2026 when crude oil crashed 9.63% in a single session following Iran’s Strait of Hormuz reopening, illustrating the rapid reversals that characterise the speculative markets young Americans increasingly favour over traditional savings vehicles.

The Expert Debate: Recklessness or Rational Response?

Is financial nihilism a generational character flaw or a rational response to unprecedented economic conditions? Policymakers, educators, and financial institutions must answer this question correctly to respond effectively.

Economist Kyla Scanlon, who coined the term “vibecession”, frames young speculation as a rational response to an economy where standard financial advice demonstrably no longer works. Traditional wealth-building strategies have failed for this generation, making risk-taking a logical adaptation rather than irresponsible behaviour.

The World Economic Forum warns against policy misinterpretation. The risk is dismissing financial nihilism as mere recklessness, leading to punitive regulation rather than addressing root causes. The organisation calls for Gen Z-tailored financial education and age-appropriate policy interventions that acknowledge economic realities.

Practitioner perspectives add texture to these academic frameworks. John Roberts of Northwestern Mutual observes young people raiding retirement accounts to pay credit card debt whilst simultaneously chasing “shortcuts” through crypto and betting. Gen Z financial planner Dinon Hughes notes clients consistently favouring speculation over traditional saving strategies.

The next major ASX story will hit our subscribers first

The Housing Affordability Crisis as Root Cause

Homeownership forms the cornerstone of traditional American wealth-building. For previous generations, housing provided forced savings through mortgage payments, leverage through property appreciation, and generational wealth transfer. When this pathway closes, the entire framework of “responsible” financial behaviour loses its anchor.

Structural barriers compound to make conventional down-payment accumulation mathematically impossible for many. Stagnating wages fail to match housing cost increases. Recent graduates carry average student debt of $94,000. Inflation, cited as the primary obstacle in Northwestern Mutual data, erodes purchasing power faster than saving can accumulate deposits.

Housing exclusion drives speculation, which produces losses for most participants. These losses further reduce homeownership prospects, reinforcing nihilism and driving more speculation. This feedback loop explains why the phenomenon may intensify rather than self-correct.

Research from the University of Chicago and Northwestern University demonstrates renters adopt speculative assets at higher rates than homeowners with comparable wealth, showing this is not about personality differences. Housing exclusion directly causes behavioural changes in financial decision-making.

What Comes Next: Policy Implications and Market Response

No specific 2026 regulatory responses or major platform changes have been documented despite growing awareness of financial nihilism. This represents either lag in policy response or lack of political will to address structural causes.

Experts recommend a three-tier framework:

- Regulation modernisation to update frameworks for Gen Z investment markets whilst balancing accessibility with consumer protection. This includes addressing platform design features that may exploit nihilistic sentiment.

- Financial education reform creating Gen Z-tailored curricula that acknowledge economic reality rather than repeating “just save more” advice. Education must address speculation risks without dismissing rational economic responses.

- Structural economic intervention addressing root causes including housing affordability, wage stagnation, and debt burdens. Policy must recognize speculation as symptom, not cause.

Current barriers to traditional markets actually sustain speculation. Employer-sponsored retirement accounts require stable employment. Investment minimums exclude those with limited capital. These barriers leave low-barrier mobile apps as the only available option for unemployed or underemployed young adults. Any policy response must account for this dynamic.

For readers exploring how to navigate these turbulent conditions with evidence-based strategies, our comprehensive guide to investing during market volatility examines portfolio construction approaches, defensive positioning, and risk management frameworks that have performed during the 2026 energy crisis and broader economic uncertainty.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is financial nihilism?

Financial nihilism is a documented disenchantment with conventional wealth-building milestones such as homeownership, retirement saving, and steady career advancement, driven by young Americans concluding that traditional financial paths are no longer accessible or effective for them.

Why are Gen Z investors choosing crypto over retirement accounts?

Gen Z investors are four times more likely to own cryptocurrency than a retirement account, according to YouGov research, largely because speculative platforms have low barriers to entry while employer-sponsored retirement accounts require stable employment that many young adults lack.

How does the housing affordability crisis fuel financial nihilism?

When homeownership, the primary traditional wealth-building vehicle, becomes mathematically unattainable for median earners burdened with average student debt of $94,000 and stagnating wages, young Americans lose the logical foundation for conventional saving behaviour and turn to speculative assets instead.

Is financial nihilism a rational response or reckless behaviour?

Economist Kyla Scanlon and the World Economic Forum argue it represents a rational adaptation to an economy where standard financial advice no longer delivers results for younger generations, rather than simple recklessness or generational character failure.

What percentage of Americans expect economic conditions to worsen in 2026?

According to Northwestern Mutual's 2026 Planning and Progress Study, 45% of respondents expect economic conditions to worsen in 2026, while 60% anticipate rising inflation, and these expectations are directly shaping the shift toward high-risk investment behaviour.