Autoliv Stock Analysis: Q1 Beat Masks Deeper Margin Concerns

Key Takeaways

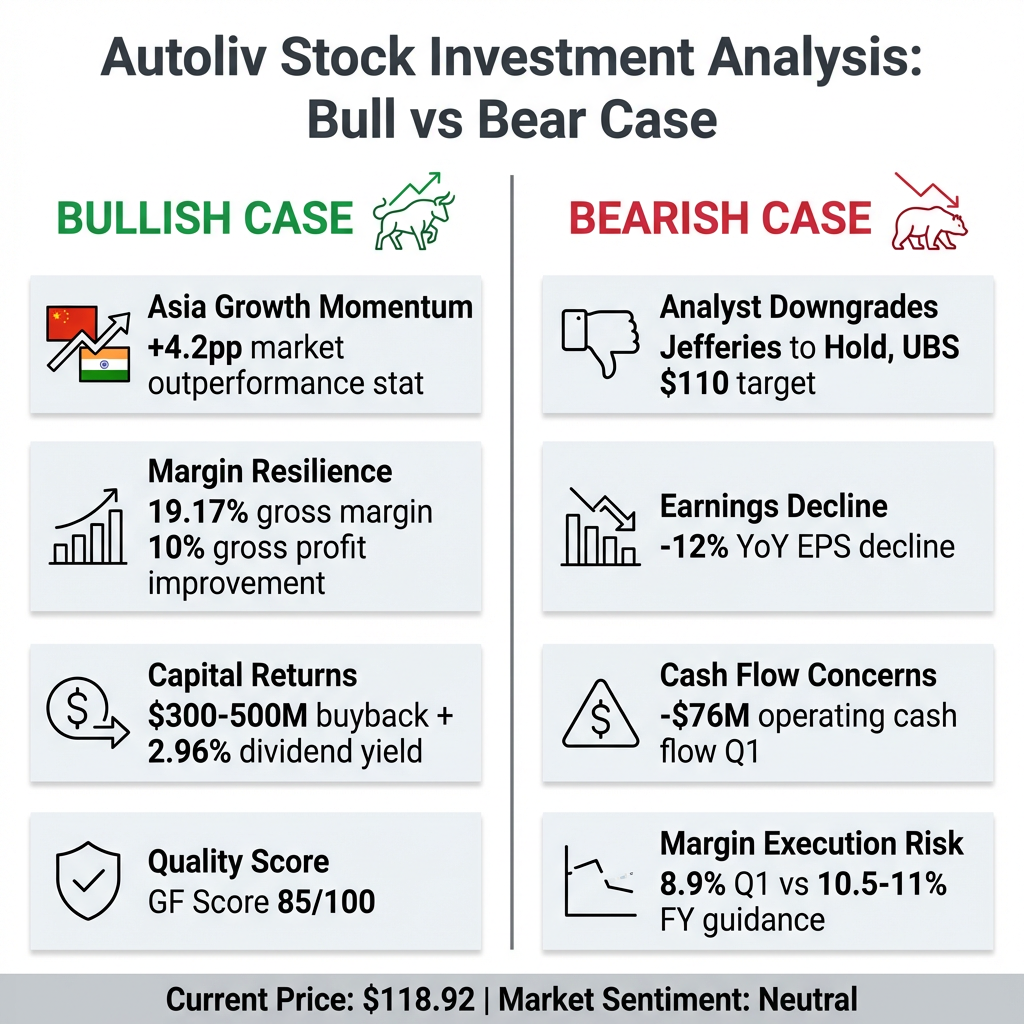

- Autoliv beat Q1 2026 revenue and EPS consensus estimates by 5.5% and 4.6% respectively, driving a 6.82% single-day share price gain to $118.92.

- Despite the quarterly beat, annual EPS declined 12% year-on-year and Q1 adjusted operating margin of 8.9% sits below the full-year guidance range of 10.5-11%, leaving significant execution risk.

- Asia-Pacific growth, particularly in China and India, was the primary driver of outperformance against a 3.4% global light vehicle production decline.

- Jefferies downgraded ALV to Hold days before the report and UBS holds a $110 price target below current levels, reflecting a broadly cautious Wall Street consensus.

- Management's planned $300-500M share buyback and 2.96% dividend yield offer capital return support, but investors are advised to monitor Q2 margin progression before building positions.

Autoliv delivered a convincing Q1 2026 earnings beat on Thursday, with revenue of $2.753B surpassing the $2.61B consensus and adjusted EPS of $2.05 exceeding the $1.96 estimate. The automotive safety giant’s shares surged 6.82% to $118.92 on the news, yet the celebration comes with caveats. Wall Street analysts remain largely neutral, annual earnings declined 12% year-on-year, and Jefferies downgraded the stock to Hold just three days before the report, citing persistent concerns about raw material cost escalation and declining light vehicle production volumes. This Autoliv stock analysis examines whether the earnings beat represents a turning point or merely a temporary reprieve in a challenging macro environment.

Understanding Autoliv’s Business Model and Market Position

Autoliv operates as the world’s largest supplier of automotive safety systems, manufacturing airbags, seatbelts, and steering wheels for global automakers. The company’s financial performance is directly tied to light vehicle production (LVP) volumes, making it highly cyclical and sensitive to automotive industry health. When automakers reduce production, Autoliv’s component sales decline proportionally, creating revenue vulnerability during industry downturns.

Examining how automotive dealership consolidation responds to changing automotive industry’s response to production volume challenges provides parallel insights into how different segments of the automotive supply chain adapt to the same macro pressures affecting Autoliv’s component sales.

The significance of Q1’s performance becomes clearer when viewed against industry headwinds. Global LVP fell 3.4% in the quarter, yet Autoliv achieved 0.8% organic sales growth, outperforming the market by approximately 4.2 percentage points. This gap represents genuine market share gains or pricing power, suggesting operational resilience beyond simple volume correlation. The company’s gross margin of 19.17% reflects ongoing efforts to balance cost pressures with pricing discipline in a competitive landscape.

When big ASX news breaks, our subscribers know first

Q1 2026 Earnings Breakdown: Where Autoliv Exceeded Expectations

The earnings beat was driven primarily by stronger-than-expected performance in Asian markets, with management specifically citing China and India as growth catalysts. India’s expanding focus on vehicle safety features represents a secular tailwind, whilst China’s market recovery provided unexpected momentum. This regional diversification proved valuable as Western markets continued to soften, demonstrating the strategic importance of Autoliv’s geographic footprint.

| Metric | Q1 2026 Actual | Consensus Estimate | Beat/Miss |

|---|---|---|---|

| Revenue | $2.753B | $2.61B | +5.5% |

| Adjusted EPS | $2.05 | $1.96 | +4.6% |

| GAAP EPS | $1.88 | $1.77-$1.91 | Beat |

| Adjusted Operating Margin | 8.9% | — | — |

| Operating Cash Flow | -$76M | — | Negative |

The concerning elements merit investor attention despite the headline beat. The 12% year-on-year EPS decline signals deteriorating profitability trends, whilst the -$76M operating cash flow reflects working capital spikes that require monitoring. Cost reduction initiatives drove a 10% improvement in gross profit, demonstrating management’s active response to margin pressures. However, the 8.9% adjusted operating margin sits below the 10.5-11% full-year guidance range, requiring significant improvement in subsequent quarters to achieve annual targets.

Autoliv’s official SEC Form 10-Q filing for Q1 2026 provides the complete financial statements and management discussion supporting the revenue, EPS, and cash flow metrics discussed in this analysis.

Wall Street’s Divided View on Autoliv Stock

Jefferies’ downgrade to Hold on 14 April specifically cited raw material cost escalation and anticipated LVP cuts as primary concerns. UBS initiated coverage at Hold with a $110 price target, positioning below current trading levels. These pre-earnings moves established a cautious backdrop, making the subsequent beat a positive surprise without fundamentally altering analyst thesis frameworks.

Bullish voices from MarketChameleon and GuruFocus emphasise Asia’s growth trajectory and margin resilience as underappreciated strengths. GuruFocus assigns an 85/100 GF Score, suggesting quality and value relative to peers and historical performance. The current price of $118.92 trades above UBS’s $110 target, implying the market prices in more optimism than sell-side analysts endorse, creating potential downside if execution falters.

No upgrades have emerged in the immediate post-earnings period as of 18 April, suggesting analysts require additional evidence before revising bullish views. The conditions most likely to shift sentiment include sustained execution on margin guidance, continued Asia momentum, and tangible evidence that raw material cost pressures are manageable rather than structural. The absence of post-earnings target increases signals a wait-and-see approach amongst professional investors.

Key Risks Facing Autoliv Investors

- Raw material cost escalation pressuring gross margins despite Q1 cost reduction successes

- Expected LVP cuts through Q2 driven by higher fuel prices reducing consumer vehicle demand

- Working capital volatility causing negative -$76M operating cash flow in Q1 and raising management execution questions

- Foreign exchange headwinds and R&D reimbursement timing effects creating quarterly result volatility

- Margin execution risk requiring expansion from 8.9% Q1 performance to 10.5-11% full-year guidance range

Understanding the broader macroeconomic forces behind raw material cost escalation becomes essential when evaluating whether Jefferies’ concerns represent temporary headwinds or structural challenges that will persist throughout 2026 and beyond.

The article’s examination of how oil approaching $100 per barrel affects automotive purchasing decisions provides crucial context for understanding the demand pressures Autoliv faces as higher fuel prices reducing consumer vehicle demand impact the broader light vehicle production landscape.

The Bureau of Labor Statistics Producer Price Index data for intermediate demand tracks price changes for steel, aluminum, and chemical products, providing official government data on the raw material cost escalation pressures affecting automotive suppliers’ margins.

Jefferies’ specific concern centres on the dual challenge of cost pressures combined with volume declines. This combination proves particularly difficult because the company cannot grow its way out of margin compression when production volumes contract. Leverage of 1.3x provides some financial buffer, yet the negative Q1 cash flow raises questions about working capital management efficiency. The 12% year-on-year EPS decline trajectory suggests earnings momentum remains negative despite quarterly beats, creating uncertainty about whether Q1 represents an inflection point or an anomaly.

The next major ASX story will hit our subscribers first

Valuation and Investment Outlook for ALV Stock

At $118.92 with an $8.3B market cap, Autoliv trades above UBS’s $110 price target yet may be undervalued by nearly 9% according to some earnings-based analyses. The lack of detailed P/E or EV/EBITDA multiples in recent coverage limits traditional valuation comparisons, though the GuruFocus score of 85/100 implies quality relative to automotive supplier peers. This valuation tension creates uncertainty about whether current levels represent fair value or incorporate excessive optimism.

Management’s planned $300-500M share buyback programme for 2026 signals confidence in the stock’s value proposition. The $1.2B full-year cash flow projection would comfortably fund these repurchases, with the 2.96% dividend yield adding income appeal. However, these capital allocation positives must be weighed against the neutral analyst consensus and execution risks on margin guidance. The buyback announcement provides fundamental support for the share price, yet doesn’t eliminate concerns about near-term earnings trajectory.

While Autoliv’s planned share buyback programme represents a more measured capital allocation strategy compared to aggressive technology sector repurchases, examining market response to share buyback announcements across different sectors provides valuation context for assessing management’s confidence signals.

Value investors may find the Asia growth story and buyback support compelling at current levels, particularly if China and India momentum proves sustainable. Momentum investors should note the 7% earnings-day pop but also recognise the cautious analyst backdrop limits upside participation. Risk-averse investors may prefer waiting for Q2 results to confirm margin expansion trajectory before building positions, given the gap between Q1’s 8.9% margin and full-year guidance. The stock appears to be in a ‘show me’ phase where execution matters more than beats.

The Bottom Line on Autoliv Stock After Q1 2026

Autoliv’s Q1 2026 earnings beat demonstrates operational resilience and Asia-driven growth momentum, yet hasn’t resolved the fundamental questions keeping Wall Street analysts on the sidelines. The divergence between quarterly beats and annual earnings decline creates a stock that could reward patient investors if margin guidance materialises, or disappoint those expecting quick resolution of macro headwinds. Q2 2026 results will be pivotal in determining which scenario plays out, with specific focus required on margin progression toward the 10.5-11% target, sustained Asia sales mix expansion, and operating cash flow normalisation. Investors should monitor whether cost reduction initiatives can offset raw material pressures whilst LVP trends stabilise, recognising that the current $118.92 price level embeds expectations that may prove optimistic if execution falters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is Autoliv and why does it matter to investors?

Autoliv is the world's largest supplier of automotive safety systems, including airbags and seatbelts, making its financial performance closely tied to global light vehicle production volumes and automotive industry health.

Did Autoliv beat earnings expectations in Q1 2026?

Yes, Autoliv reported Q1 2026 revenue of $2.753B versus the $2.61B consensus and adjusted EPS of $2.05 versus the $1.96 estimate, beating on both top and bottom lines and sending shares up 6.82%.

Why did Jefferies downgrade Autoliv stock before earnings?

Jefferies downgraded Autoliv to Hold on 14 April, just three days before the Q1 report, citing persistent concerns about raw material cost escalation and anticipated declines in light vehicle production volumes.

What risks should investors monitor for Autoliv stock in 2026?

Key risks include raw material cost pressures, expected light vehicle production cuts through Q2, negative Q1 operating cash flow of -$76M, and the challenge of expanding adjusted operating margin from 8.9% to the full-year guidance range of 10.5-11%.

What is the analyst consensus on Autoliv stock after Q1 2026 results?

Analyst sentiment remains largely neutral, with UBS holding a $110 price target below current trading levels and no upgrades issued in the immediate post-earnings period, suggesting a wait-and-see approach among professional investors.