ASIC Fines Three ASX Companies $1.17m for Missing Annual Reports

1 hr ago

Judo Capital shares closed at $1.455 on 30 April 2026, roughly 21% below where they traded a year ago. Yet two of the most closely watched brokers covering the stock have just upgraded or reaffirmed buy-equivalent ratings, with price targets implying upside of 27% to 72% from current levels. The gap between that share price trajectory and analyst conviction reflects a genuine tension at the heart of the Judo Capital investment case. The bank is growing loans and deposits, expanding margins, and executing on its SME strategy, but rising funding costs and a conservative provisioning build are compressing near-term earnings. Understanding which of these forces dominates the forward outlook is the practical question for investors considering the Judo Capital share price right now.

This analysis unpacks the four structural developments inside Judo’s Q3 FY26 update that matter most: the rapid deposit base expansion, the net interest margin (NIM) trajectory and what funding cost normalisation means for FY27, the credit quality picture behind the provision build, and the competitive dynamics shaping Judo’s SME and agribusiness growth runway.

The speed is worth registering first. Judo’s newly launched savings products accumulated over $1.1 billion in deposits within just two quarters, pushing total deposits to $11.5 billion at March 2026. For a bank with a $13.8 billion loan book, that kind of deposit velocity materially reduces reliance on wholesale funding markets.

The current blended deposit cost sits at 0.74% above the one-month BBSW rate, which is well below historical norms. Three metrics frame the picture:

Deposit cost context: The 0.74% spread above BBSW reflects below-market pricing on term deposit books that are yet to fully reprice. Normalisation toward end of FY26 is expected to add approximately 20-30 basis points to the blended rate.

That normalisation is the other side of the story. The deposit growth strengthens Judo’s funding base, but the repricing of these balances toward market rates is the key FY27 headwind. Investors assessing funding risk need to hold both realities simultaneously: a strategically stronger deposit franchise, carrying a margin cost that has not yet fully arrived.

For investors wanting the complete picture behind these numbers, our full explainer on Judo’s Q3 FY26 update covers the raw figures in detail, including the CET1 ratio holding at 12.6%, the improvement in customer attrition from 33% to 15% annualised, and management’s exact language on the provision overlay rationale.

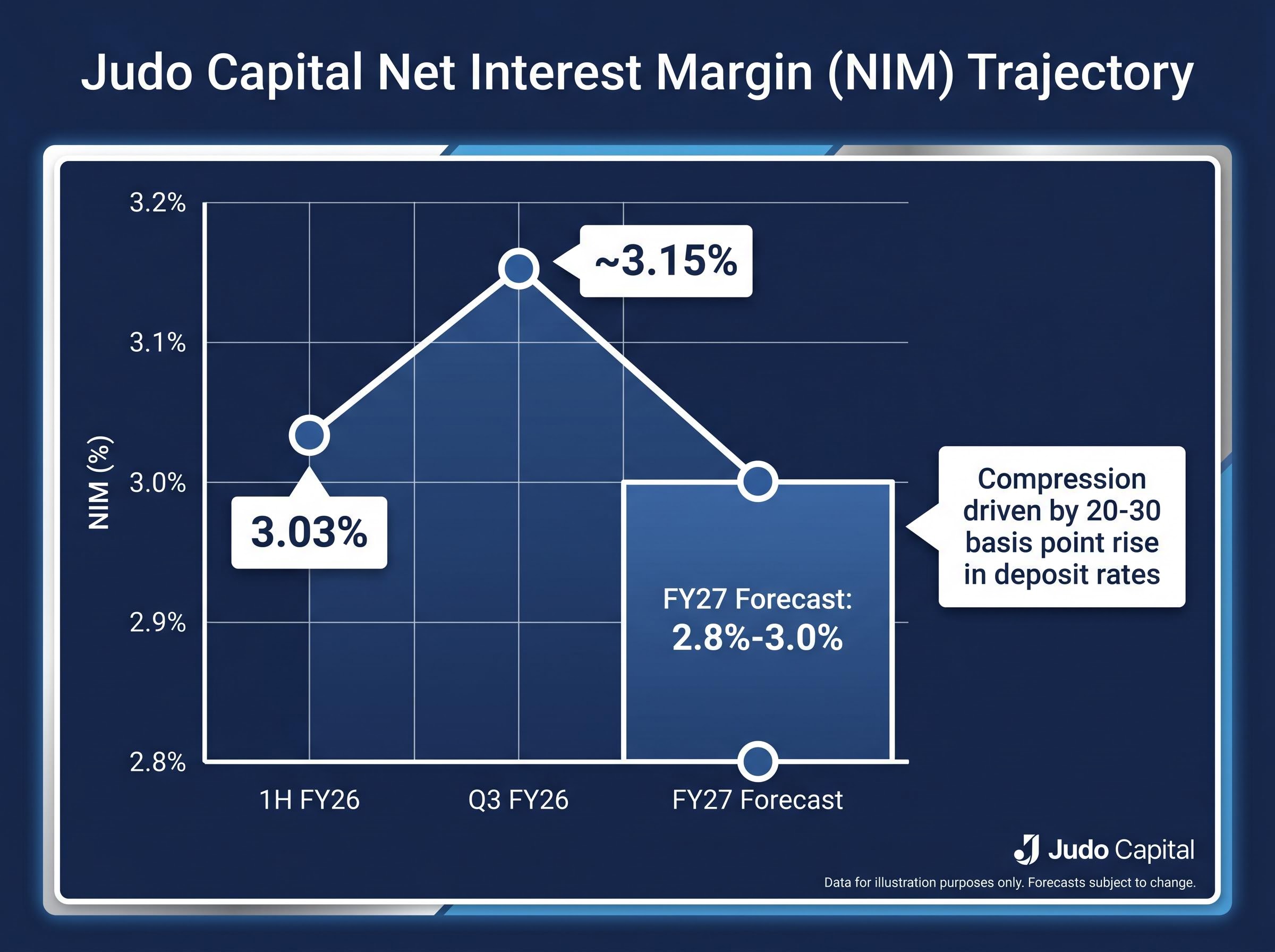

Judo’s Q3 FY26 NIM of approximately 3.15% was a genuine improvement, up from 3.03% in 1H FY26. Management is now targeting the upper end of its 3.0%-3.1% guidance range for the full year, and Macquarie held the view that the bank would beat its own margin guidance in 2H FY26.

The current reading is unambiguously positive. The question is what comes after it.

| Period | NIM |

|---|---|

| 1H FY26 | 3.03% |

| Q3 FY26 | ~3.15% |

| FY27 analyst forecast range | 2.8%-3.0% |

The mechanism behind the expected FY27 compression is straightforward. Below-market term deposit books, which provided a tailwind through 1H and Q3 FY26, will roll off and reprice at higher rates as funding cost normalisation flows through the balance sheet. The anticipated 20-30 basis point rise in blended deposit rates is the primary driver.

Analyst forecasts place FY27 NIM in the 2.8%-3.0% range. That represents compression, not collapse, and the distinction matters. The NIM trajectory is the single most important driver of Judo’s earnings profile over the next 18 months, and the direction of travel, rather than just the current reading, is what the share price needs to price.

Challenger bank NIM dynamics in the March 2026 quarter were not uniformly positive: Heartland Group’s sequential margin expansion from 3.89% to 4.06% across three quarters shows that some specialist lenders are widening margins even as funding cost normalisation creates headwinds elsewhere, a comparison that sharpens the question of how much of Judo’s FY27 compression is structural versus cyclical.

Judo operates a relationship-banking model purpose-built for Australian small and medium enterprises. Dedicated bankers maintain low customer-to-banker ratios, enabling deeper credit assessment and more disciplined pricing than the volume-driven approach the major banks typically apply to smaller business clients.

The structural characteristics that define the model include:

Judo holds approximately 2% of the Australian SME lending market, which has been growing at roughly 5% year-on-year through 2025-2026. Gross loans and advances reached $13.8 billion at March 2026, up from $13.4 billion at December 2025. CEO Chris Bayliss has signalled ongoing investment in deepening the bank’s regional and agribusiness presence.

RBA data on SME lending conditions published in October 2025 shows the stock of outstanding SME loans growing at approximately 6.5% annually, a rate that contextualises Judo’s own loan book expansion and the broader market opportunity the bank is competing for.

NAB and CBA have both increased their agribusiness lending focus through 2025-2026, intensifying competition in one of Judo’s growth verticals. No material market share erosion for Judo has been identified in available data, however. The relationship model limits direct substitutability; an SME client receiving dedicated banker coverage is not straightforwardly poached by a rate offer from a larger institution with a different service model. The competitive pressure is real, but the structural differentiation provides a buffer.

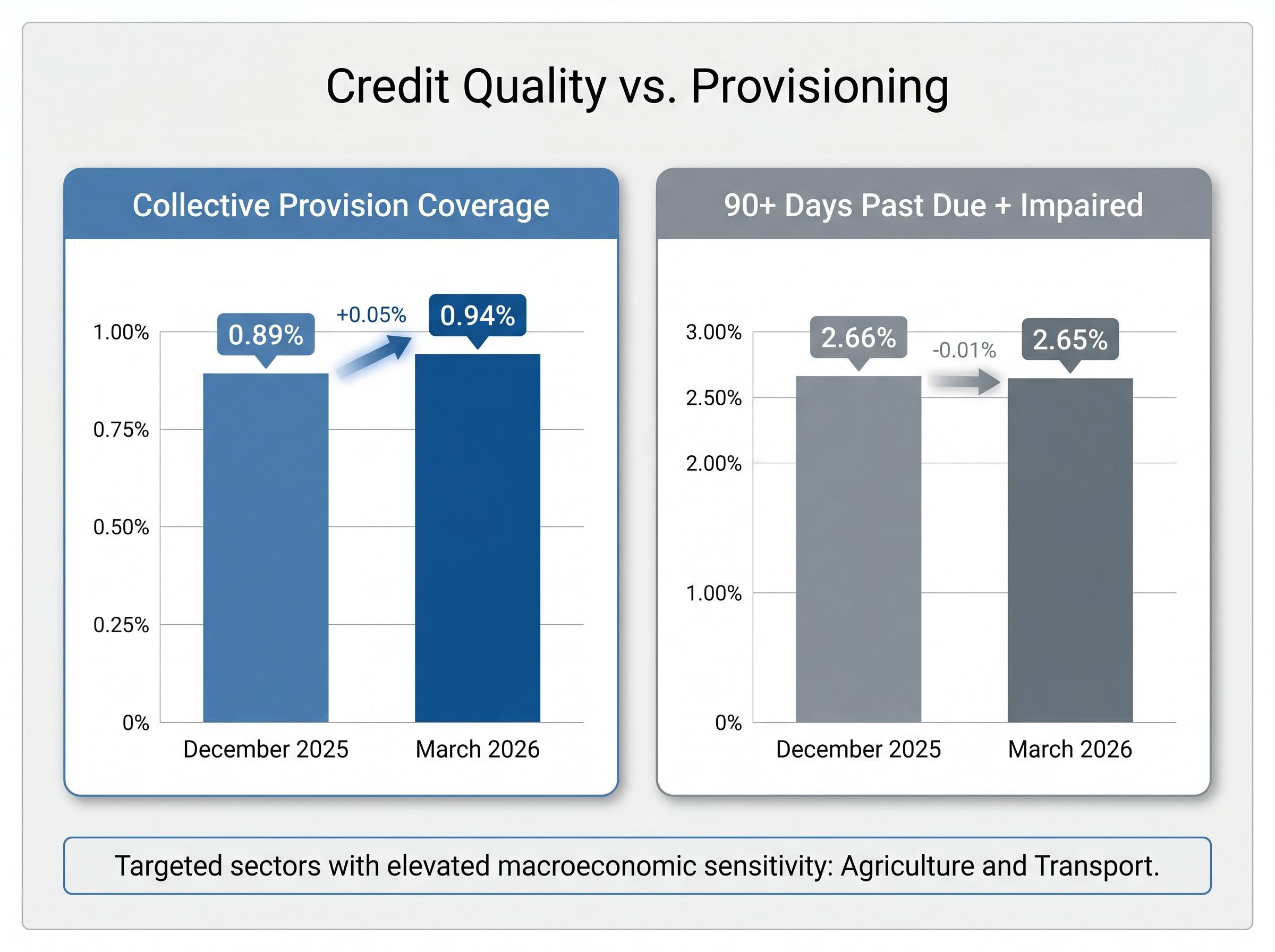

Judo conducted a full loan portfolio review before raising provisions in Q3 FY26, targeting sectors with elevated macroeconomic sensitivity, including agriculture and transport. The result was a collective provision coverage of 0.94% at March 2026, up from 0.89% at December 2025.

| Credit Quality Metric | December 2025 | March 2026 |

|---|---|---|

| Collective provision coverage | 0.89% | 0.94% |

| 90+ days past due plus impaired loans | 2.66% | 2.65% |

Provision coverage at 0.94% represents a deliberate management decision to build buffers against macroeconomic uncertainty, not a response to observed credit deterioration in the existing book.

The tension sits in plain view. The provision build is the reason FY26 pre-tax profit guidance of $180-$190 million is now expected at the lower end. Yet the underlying book quality data does not show deterioration: loans 90 days or more past due plus impaired loans came in at 2.65% at March 2026, marginally improved from 2.66% the prior quarter.

Whether this represents conservative forward positioning or early evidence of stress in the SME book is the question investors need to hold when evaluating the current share price.

Over the past 12 months, JDO shares have fallen approximately 21% while the ASX 200 has gained roughly 10%. The underperformance is stark. The broker response to it has been equally striking in the opposite direction.

ASX banking sector dynamics in 2026 have produced a striking divergence: the Big Four collectively gained 8.87% in the Financials index year to date while names like Judo declined sharply, a gap that reflects different investor assumptions about rate sensitivity, valuation, and which business models benefit most from the RBA’s next move.

Morgans upgraded to Buy from Accumulate in April 2026, citing the share price weakness as a buying opportunity and viewing the current level as offering a meaningful margin of safety. Macquarie maintained its Outperform rating with a $1.85 price target, highlighting strong underlying revenue performance alongside continued lending book growth.

Neither broker treated the price decline as a fundamental deterioration signal. Both framed it as a tactical entry point.

| Broker / Measure | Rating | Price Target | Implied Upside from $1.455 |

|---|---|---|---|

| Macquarie | Outperform | $1.85 | ~27% |

| Morgans | Buy | Not explicitly published | Significant (Buy thesis) |

| Consensus average | — | $2.19 | ~50% |

| Consensus high | — | $2.50 | ~72% |

The range of implied outcomes, from 27% at the low end to 72% at the high, is wide enough that investors need to form their own view on which assumptions deserve more weight. The market’s scepticism and the brokers’ conviction cannot both be right to the same degree.

The bull case rests on four pillars: a $13.8 billion loan book still growing, a relationship model that sustains higher margins than the major banks can replicate at scale, a deposit base that has expanded rapidly, and broker conviction that the share price weakness represents mispricing rather than fundamental deterioration.

The bear case is equally specific. FY27 NIM compression to 2.8%-3.0% from deposit cost normalisation will weigh on earnings. FY26 pre-tax profit of $180-$190 million is tracking toward the lower end due to the provisioning build. NAB and CBA are competing more aggressively in agribusiness.

The variables that will determine which case plays out are identifiable:

CEO Chris Bayliss has emphasised disciplined cost management and continued SME growth through elevated market volatility, framing the bank’s posture as one of building through the cycle rather than retreating from it.

Management has described the capital position as healthy, with no capital adequacy concerns appearing in broker commentary. The structural story remains intact; the question is whether the near-term earnings headwinds are already priced into the 21% decline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The fundamental investment thesis, a relationship-driven SME bank with structural margin advantages and a growing balance sheet, has not changed materially through the Q3 FY26 update. What has changed is the near-term path to earnings delivery, which now requires navigating deposit cost normalisation and demonstrating that the provision build was forward-looking rather than reactive.

Broker consensus price targets range from $1.85 to $2.50 against the 30 April close of $1.455. Two upcoming events will test whether that conviction is vindicated: the FY26 full-year result and the initial FY27 NIM guidance. Those are the data points that will most directly resolve the tension between the market’s scepticism and the professional conviction that the current price undervalues what Judo is building.

For investors who hold Judo within a broader Australian equity allocation, our deep-dive into ASX bank concentration risk examines how the financial sector’s roughly 25% weight in the ASX 200 means domestic equity investors are running a concentrated sector bet whether they realise it or not, with Morningstar flagging all four major banks as overvalued at current multiples.

Judo Capital shares have declined approximately 21% over the past 12 months, underperforming the ASX 200 which gained roughly 10% over the same period. The market is weighing near-term headwinds including deposit cost normalisation, a conservative provision build, and expected NIM compression in FY27, against the bank's ongoing loan book and deposit growth.

Judo Capital operates a relationship-banking model purpose-built for Australian small and medium enterprises, using dedicated bankers with low customer-to-banker ratios to deliver deeper credit assessment and more disciplined pricing than the major banks typically apply to SME clients. This specialisation allows Judo to sustain higher margins through service quality and credit selectivity rather than volume competition.

Analyst forecasts place Judo Capital's FY27 net interest margin in the 2.8%-3.0% range, down from approximately 3.15% in Q3 FY26. The expected compression is driven primarily by below-market term deposit books rolling off and repricing at higher rates, which is anticipated to add around 20-30 basis points to the blended deposit cost.

Morgans upgraded Judo Capital to Buy from Accumulate in April 2026, citing the share price weakness as a buying opportunity, while Macquarie maintained its Outperform rating with a price target of $1.85. Consensus price targets range from $1.85 to $2.50, implying upside of approximately 27% to 72% from the 30 April 2026 close of $1.455.

Management conducted a full loan portfolio review before raising provisions in Q3 FY26, targeting sectors with elevated macroeconomic sensitivity including agriculture and transport, but underlying book quality data does not show deterioration. Loans 90 days or more past due plus impaired loans came in at 2.65% at March 2026, marginally improved from 2.66% the prior quarter, suggesting the build reflects conservative forward positioning rather than observed credit stress.