Goldman Sachs Cuts 2026 Smartphone Shipment Forecast 10% on AI Crunch

25 mins ago

Brent crude has surged roughly 55% since late February 2026. Australian CPI has accelerated to 4.6%. The Reserve Bank of Australia (RBA) has already raised rates twice this year. For Australian investors navigating inflation, the question is no longer whether prices are rising. It is what to do about it.

The Iran war has injected a supply-side oil shock into an economy that was already running above the RBA’s 2-3% target band. With the central bank projecting inflation to peak at approximately 4.2% by mid-2026 and remain elevated until early 2027, the macro environment demands a portfolio response grounded in evidence rather than emotion.

What follows is a framework for that response. This guide covers what history reveals about how supply-driven oil shocks typically resolve, why markets may be overpricing the rate tightening cycle, and how Australian investors can position across income, diversification, and liquidity to protect their long-term purchasing power through the current disruption.

The instinct is straightforward: inflation rises, portfolios suffer, move to cash. But the source of inflation determines whether that instinct is correct or counterproductive.

Not all inflation episodes are alike. The two primary types produce different economic dynamics and require different investor responses:

Demand-pull inflation:

Supply-push inflation:

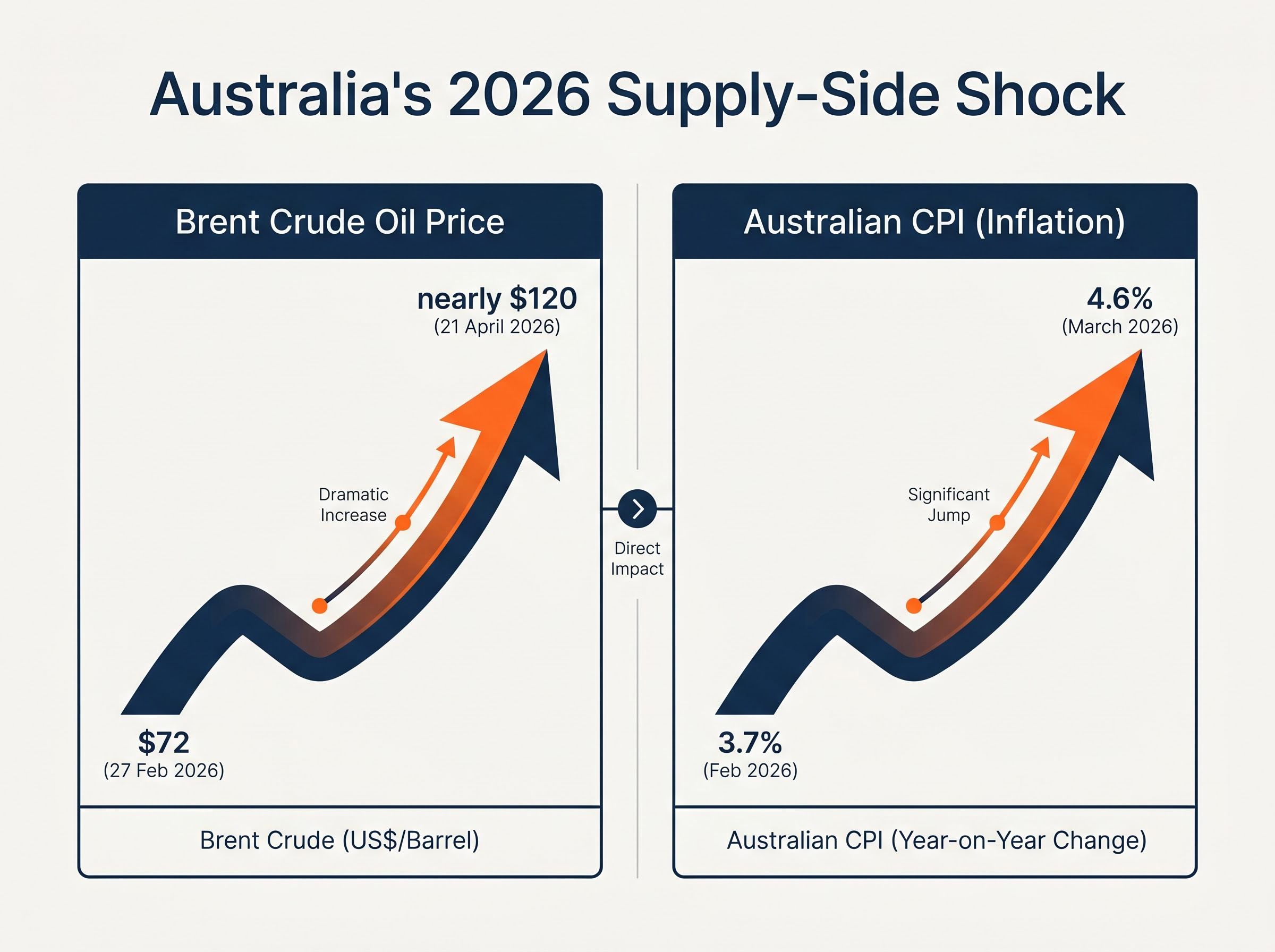

Australia’s current episode is supply-driven. The Iran war pushed Brent crude from around $72 per barrel on 27 February 2026 to nearly $120 by 21 April 2026. Late April prices remained above $104.40 per barrel. Australian CPI jumped from 3.7% in February 2026 to 4.6% in March 2026, while the RBA’s preferred underlying measure, trimmed mean CPI, came in at 3.3%.

The ABS Consumer Price Index release for March 2026 confirms headline CPI at 4.6%, trimmed mean inflation at 3.3%, and housing costs up 6.5% year-on-year, providing the official data foundation for the inflation figures cited throughout this guide.

A weaker Australian dollar amplifies the pass-through. Because oil is priced in US dollars, AUD weakness makes the commodity more expensive domestically, compressing household budgets and business margins simultaneously.

According to IMF research, each additional percentage point of inflation above 3% in a developed economy typically reduces real GDP growth by roughly 0.1-0.2 percentage points.

Recognising this as a supply shock, not a demand boom, is the first step toward a proportionate response. The two scenarios call for meaningfully different portfolio positioning.

Beneath the headline CPI numbers, structural deflation forces including AI-driven productivity gains, Chinese manufacturing overcapacity, and global supply chain rebalancing are working in the opposite direction to energy prices, creating a two-speed inflation dynamic that makes the current episode meaningfully different from the 1970s.

The RBA raised rates in both February and March 2026, responding to stronger-than-expected economic data and energy price pressures. March meeting minutes explicitly characterised energy prices as posing material risks to the inflation outlook. Further hikes remain on the table.

The central bank projects inflation peaking at approximately 4.2% by mid-2026, with a return to the 2-3% target band by early 2027. That projection depends substantially on whether oil prices stabilise or escalate further.

Here is where the gap between market pricing and historical precedent becomes visible.

In prior supply-side oil shock episodes, central bank rate increases have typically reversed within six to twelve months as growth concerns take precedence over inflation-fighting. The pattern is consistent: supply shocks suppress demand, push up unemployment, and shift central bank priorities from tightening to support.

Oil futures markets appear to share this reading. The current backwardation in the oil curve, where near-term contracts price higher than longer-dated ones, signals that traders expect the supply disruption to be relatively short-lived rather than structural.

Several disinflationary forces remain active beneath the headline numbers:

The Taylor Rule, a standard framework for evaluating monetary policy, suggests genuine tightening requires roughly 1.5 percentage points of rate increase for each 1 percentage point of above-target inflation. The RBA’s current trajectory falls short of that threshold, suggesting the central bank is balancing inflation-fighting with growth preservation.

If energy prices remain elevated for an extended period, the combination of stagnant growth and persistent inflation becomes a material risk for Australia. The 1970s oil shock produced exactly this outcome when central banks waited too long to respond.

The distinction today is that the RBA has demonstrated willingness to hike early. That policy posture reduces, without eliminating, the probability of inflation expectations becoming unanchored, which in the 1970s triggered a secondary inflationary wave that proved far harder to contain.

Inflation is, at its core, the progressive erosion of purchasing power. A dollar today buys less than it did a year ago, and when CPI runs at 4.6%, that erosion accelerates.

Three forces are driving Australia’s current inflation:

Most advanced economies target approximately 2% inflation. The RBA’s target band of 2-3% reflects the same logic: a moderate level of inflation is not all bad. It supports nominal corporate earnings, incentivises productive investment over cash hoarding, and provides central banks with room to cut rates during downturns. Deflation, where prices fall, is the opposite risk and typically far more damaging to economic activity.

The counter-intuitive insight for investors is that holding cash through an inflationary episode is itself a losing strategy. When CPI is running at 4.6%, even a high-yield savings account delivering 4% produces a negative real return. The purchasing power of that cash is falling every month.

| Episode | Cash real return (approx.) | Diversified portfolio real return (approx.) |

|---|---|---|

| 1974 oil shock (3-year period) | -3% to -5% p.a. | -1% to +2% p.a. |

| 2022 energy shock (2-year period) | -4% to -2% p.a. | +1% to +4% p.a. |

Historical illustration only. Past performance does not guarantee future results.

Understanding this dynamic is the foundation for everything that follows. The question is not whether to remain invested, but how to position within the portfolio.

Fixed income faces a mechanical headwind: when the RBA raises rates, existing bond prices fall. That is the near-term pain. However, elevated yields on newly issued bonds make fixed income increasingly attractive as the tightening cycle approaches its peak. Investment-grade credit, in particular, offers a combination of income and relative capital stability that becomes compelling once rate hikes pause.

Cash and money market instruments serve a dual role. High-yielding cash products now offer a genuine real return buffer for the first time in years. They also provide optionality: dry powder available for redeployment when higher-conviction opportunities emerge during market dislocations.

Analyst observations confirm that inflows to cash and money market ETFs have been significant as investors seek capital preservation amid the current uncertainty.

Equities require more nuance. Energy and resources companies are direct beneficiaries of elevated oil prices, and sector ETFs in this space have held steady or gained. Growth and technology companies, by contrast, are more sensitive to rate increases because their valuations depend heavily on future cash flows discounted at higher rates.

Companies with genuine pricing power, the ability to pass cost increases through to customers, and low debt levels tend to outperform in inflationary environments. Their earnings hold up while competitors absorb margin compression. Their financing costs remain manageable while highly leveraged peers face rising interest expenses.

International diversification reduces concentration risk when a domestic economy is absorbing an asymmetric shock. Outflows from US-based equity ETFs have reflected reduced risk appetite and AUD/USD dynamics, but broad geographic exposure across developed markets smooths the impact of any single economy’s inflationary episode.

International ETF capital flows tell part of the story: international funds overtook domestic ETFs as the most purchased category on Selfwealth by Syfe in Q1 2026, a structural inflection point rather than a temporary swing, driven by investors across every generational cohort reducing concentration in a domestically shocked economy.

| Asset class | Inflation sensitivity | Rate sensitivity | Current outlook |

|---|---|---|---|

| Fixed income | Moderate (negative near-term) | High (prices fall as rates rise) | Increasingly attractive as rate cycle peaks |

| Equities | Varies by sector | Growth stocks most exposed | Favour quality and pricing power |

| Cash / money market | Low (preserves nominal value) | Positive (yields rise with rates) | Strong for preservation and optionality |

| International shares | Diversified exposure | Moderate | Reduces domestic concentration risk |

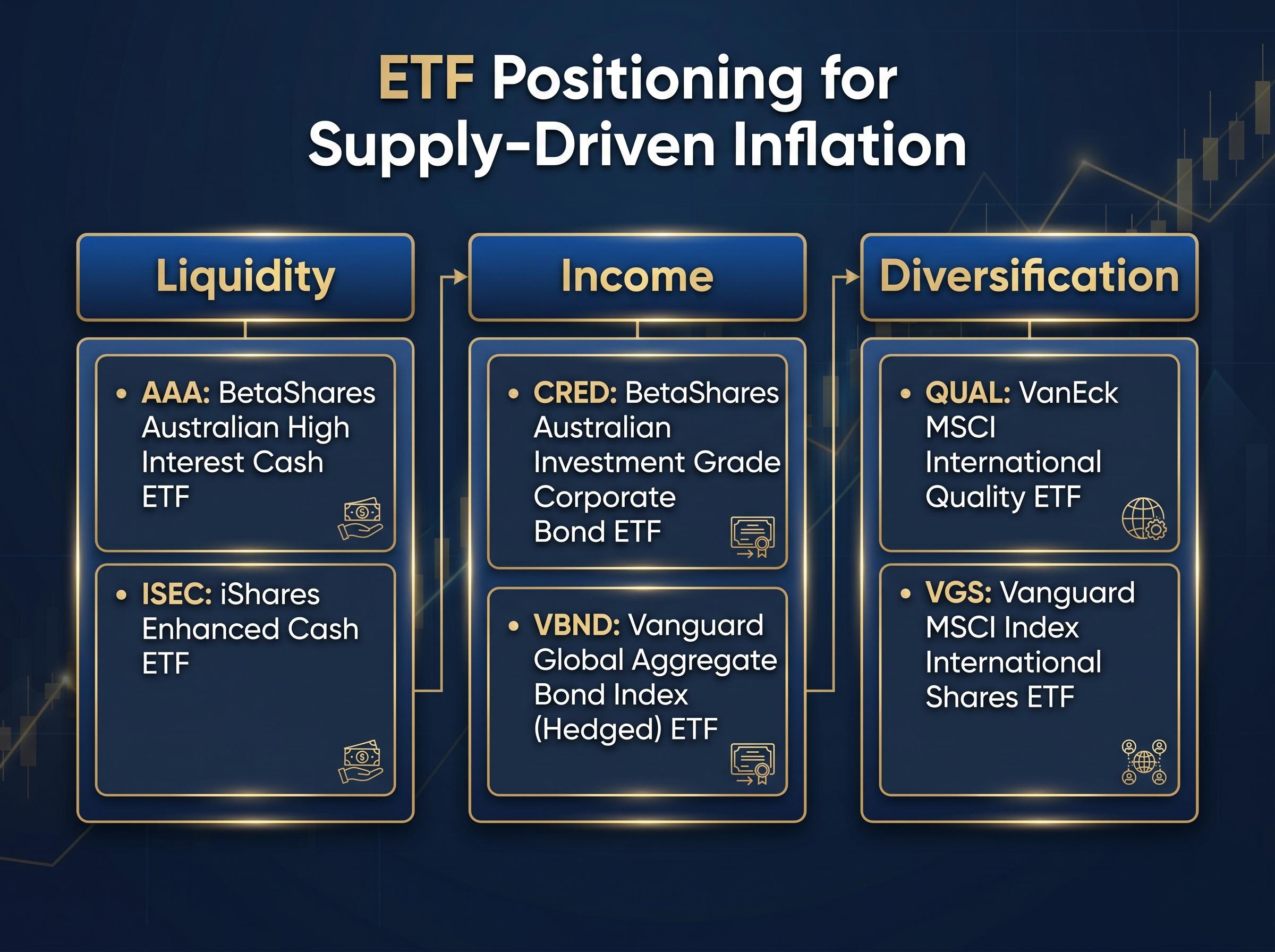

The framework from the previous section identifies three portfolio needs during a supply-driven inflation episode: income, diversification, and liquidity. The following six ASX-listed ETFs map directly to those categories, each with a specific role in the current environment.

| ETF code | ETF name | Category | What it holds | Role in current environment |

|---|---|---|---|---|

| AAA | BetaShares Australian High Interest Cash ETF | Liquidity | AUD-denominated bank deposit accounts with regular income distributions | Real yield preservation and dry powder for redeployment |

| CRED | BetaShares Australian Investment Grade Corporate Bond ETF | Income | Senior fixed-rate bonds from high-quality Australian companies | Captures elevated corporate yields with domestic credit quality |

| ISEC | iShares Enhanced Cash ETF | Liquidity | Short-duration money market instruments and corporate bonds | Modestly higher returns than standard bank deposit ETFs with low duration risk |

| QUAL | VanEck MSCI International Quality ETF | Diversification | Highly profitable global businesses with strong fundamentals, low debt, and pricing power | Quality-factor tilt favours companies that hold margins when input costs rise |

| VBND | Vanguard Global Aggregate Bond Index (Hedged) ETF | Income | Broad investment-grade global debt, AUD-hedged | Positions for bond price recovery as the RBA rate cycle peaks |

| VGS | Vanguard MSCI Index International Shares ETF | Diversification | 1,000+ large companies across developed markets outside Australia | Reduces concentration in a domestically shocked economy |

VBND and CRED become particularly relevant as the RBA rate cycle approaches its peak; bond prices typically recover from their troughs once rate hikes cease. AAA and ISEC serve a dual purpose: real yield preservation now, and capital available for redeployment when conviction improves. VGS provides broad geographic diversification, while QUAL‘s quality-factor tilt is specifically suited to an environment where pricing power separates winners from losers.

Volatility is not a reason to exit a long-term strategy. It is the condition in which long-term positioning is made or lost.

The gap between knowing what to do and consistently doing it is where most retail investors lose ground in volatile periods. Process closes that gap. The following actions can be taken this week:

Younger Australian investors have systemised dip-buying during volatility as a deliberate accumulation strategy, with Millennials allocating approximately 70% of their portfolios to ETFs and actively using market dislocations to reduce average entry costs, a behaviour pattern that mirrors the dollar cost averaging logic the current environment rewards.

Automating contributions through recurring investment features, available on platforms such as Selfwealth by Syfe with weekly, fortnightly, or monthly scheduling, removes the emotional friction that causes investors to pause contributions at precisely the moments when consistency matters most.

Supply shocks ultimately resolve through either demand cooling and rate reductions, or supply constraints easing and price normalisation. Markets have recovered in both scenarios historically. The ultra-low inflation environment of the 2010s is unlikely to return; 2% now functions more as a lower bound. Adjusting expectations to that baseline is part of the long-term positioning.

The Iran war oil shock is materially disruptive. Short-term conditions may worsen before they improve. But supply-driven inflation episodes have historically resolved within a twelve-to-eighteen-month window, and investors who maintained diversified, disciplined positions have recovered fully in prior episodes.

The framework across this guide follows a clear sequence: understand the inflation type, respect the rate cycle without overreacting to it, hold the right asset class mix, use named instruments with specific roles, and automate execution to remove emotion from the process.

With inflation projected to return to the RBA’s 2-3% target band by early 2027, investors who position thoughtfully in mid-2026 are buying into a recovery timeline, not a permanent new normal. Review current portfolio allocation against the three-category framework. Check whether holdings cover income, diversification, and liquidity. Consider setting up a recurring investment schedule to implement dollar cost averaging systematically.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Supply-driven inflation is caused by external cost shocks such as rising energy prices rather than strong consumer demand, and it creates a difficult environment where central banks must balance fighting inflation against supporting slowing growth. For Australian investors, the 2026 oil price surge from the Iran war is a textbook supply shock, pushing CPI to 4.6% while simultaneously compressing household budgets and business margins.

Holding cash during high inflation is generally a losing strategy in real terms because when CPI runs at 4.6%, even a high-yield savings account paying 4% produces a negative real return, meaning purchasing power falls every month. Historically, diversified portfolios have outperformed cash in real terms during both the 1974 oil shock and the 2022 energy shock.

The article identifies six ASX ETFs across three categories: AAA and ISEC for liquidity and real yield preservation, CRED and VBND for income as the RBA rate cycle approaches its peak, and VGS and QUAL for international diversification and quality-factor exposure. Each ETF is selected for a specific role within a framework designed for supply-driven inflation.

The RBA raised rates in both February and March 2026, and the central bank projects inflation to peak at approximately 4.2% by mid-2026 before returning to the 2-3% target band by early 2027. Historical precedent from prior supply-side oil shock episodes suggests rate increases often reverse within six to twelve months as growth concerns take priority over inflation-fighting.

Dollar cost averaging involves maintaining or increasing regular investment contributions during market sell-offs rather than pausing them, which reduces the average entry cost over time. Automating contributions through recurring investment features on platforms such as Selfwealth by Syfe removes the emotional friction that typically causes retail investors to pause at precisely the moments when consistency matters most.