The macroeconomic picture on 29 April 2026 reveals a stark divergence across the US economy. Massive technology infrastructure spending continues at unprecedented volumes, while an acute energy shock drives US consumer sentiment toward multi-year lows. As the Federal Reserve prepares to announce its interest rate decision at 2:00 p.m. ET today, policymakers face a complex environment defined by surging oil prices and heavily downgraded economic growth figures.

The geopolitical impact on stocks requires investors to adopt a clear analytical framework. The interplay between Middle East hostilities, restricted energy supply, and central bank reactions is actively restructuring market winners and losers.

This analysis examines the specific transmission mechanisms turning foreign conflict into domestic inflation. It evaluates how current institutional positioning and corporate forward guidance separate vulnerable sectors from structurally resilient assets. Understanding these dynamics helps investors identify which equities can absorb the shock.

The Anatomy of a Geopolitical Energy Shock

A distant geopolitical conflict moves through physical supply chains long before it forces central bank action. The transmission mechanism begins with renewed US sanctions on Iran, which directly disrupt global crude oil supply networks. This restriction immediately elevates wholesale energy costs, passing through to headline inflation metrics within weeks.

An energy price shock functions as a regressive tax on the US consumer. When fuel prices rise rapidly, low-income and middle-income households must allocate a larger percentage of their discretionary capital to basic transportation and heating.

This forced reallocation bleeds capital away from discretionary retail and services. Ultimately, this dynamic triggers a contraction in core economic indicators across the broader market.

The resulting damage to consumer confidence is severe and measurable. According to late April 2026 data, the war-driven affordability crisis is worsening finances for over half of Americans.

WTI crude trading at approximately $103.30 and Brent crude at $114.68 per barrel University of Michigan Consumer Sentiment Index dropping to 49.8, marking a near four-year low * 1-year consumer inflation expectations remaining elevated at 4.7% to 4.8%

This entrenched conflict forces investors to look past daily ticker movements and evaluate foundational economic risks.

Economic Assessment “The Iran conflict has caused the largest oil supply disruption, resulting in surging prices. The entrenched nature of the conflict and the ensuing oil shock have increased the odds of a recession to nearly 50 percent,” noted Mark Zandi, chief economist at Moody’s Analytics.

Understanding this physical supply chain transmission mechanism helps identify the core macroeconomic forces dictating current equity valuations.

For investors closely tracking these macroeconomic threshold levels, our deep dive into how $112 oil impacts US recession models details the specific price points that institutional forecasters warn could push the economy into a prolonged contraction.

When big ASX news breaks, our subscribers know first

Stagnation Risks and Today’s Federal Reserve Strategy

The raw inflation data frames the immediate tension facing Federal Reserve Chair Jerome Powell this afternoon. The Federal Open Market Committee (FOMC) is widely expected to hold the effective rate steady today, keeping the target corridor at 3.50% to 3.75%. This stance signals that the central bank prioritises inflation control over immediate growth stimulus.

Policymakers are caught in a difficult stagnation trap. The severe downward revision in Q4 2025 GDP, falling from an initial 1.4% estimate to a final 0.5% annualised rate, confirms stalling economic momentum. Concurrently, persistent core Personal Consumption Expenditures (PCE) data driven by Middle East energy inflation prevents the central bank from cutting rates to support that growth.

The official BEA economic accounts validate the underlying weakness in the domestic market, demonstrating a clear deceleration in corporate profit margins and state-level gross domestic output alongside the headline GDP contraction.

| Macroeconomic Indicator | Current Reading (Late April 2026) |

|---|---|

| Q4 2025 GDP Growth (Final) | 0.5% annualised |

| WTI Crude Price | $103.30 per barrel |

| Target Fed Funds Rate | 3.50% to 3.75% |

| Consumer Sentiment Index | 49.8 |

The institutional outlook extends well beyond today’s press conference. Prospective Federal Reserve Chair Kevin Warsh faces a Senate confirmation vote today, marking a leadership transition that could heavily influence long-term policy expectations. Financial markets are actively pricing in a specific long-term trajectory based on these combined fiscal and geopolitical tensions.

March 2027 30-Day Fed Funds futures currently imply expectations for six 25-basis-point cuts extending into 2027. This extended timeline suggests institutional investors expect the macroeconomic strain to persist for multiple quarters before any meaningful policy relief arrives. Consequently, the cost of capital will continue constraining corporate expansion plans.

For investors, this stagnation dynamic indicates borrowing costs will likely remain elevated even as broader economic growth stalls. This high-rate environment fundamentally shifts how debt-reliant equities are valued across major indices. Companies requiring heavy capital restructuring face severe headwinds under these persistent conditions.

Corporate Casualties in Aviation and Global Travel

Macroeconomic pressures manifest clearly in corporate forward guidance across vulnerable sectors. The energy shock and geopolitical instability are actively degrading profit margins for the transport and hospitality industries. Companies are reporting distinct impacts based on their structural exposure to fuel costs versus shifting consumer demand.

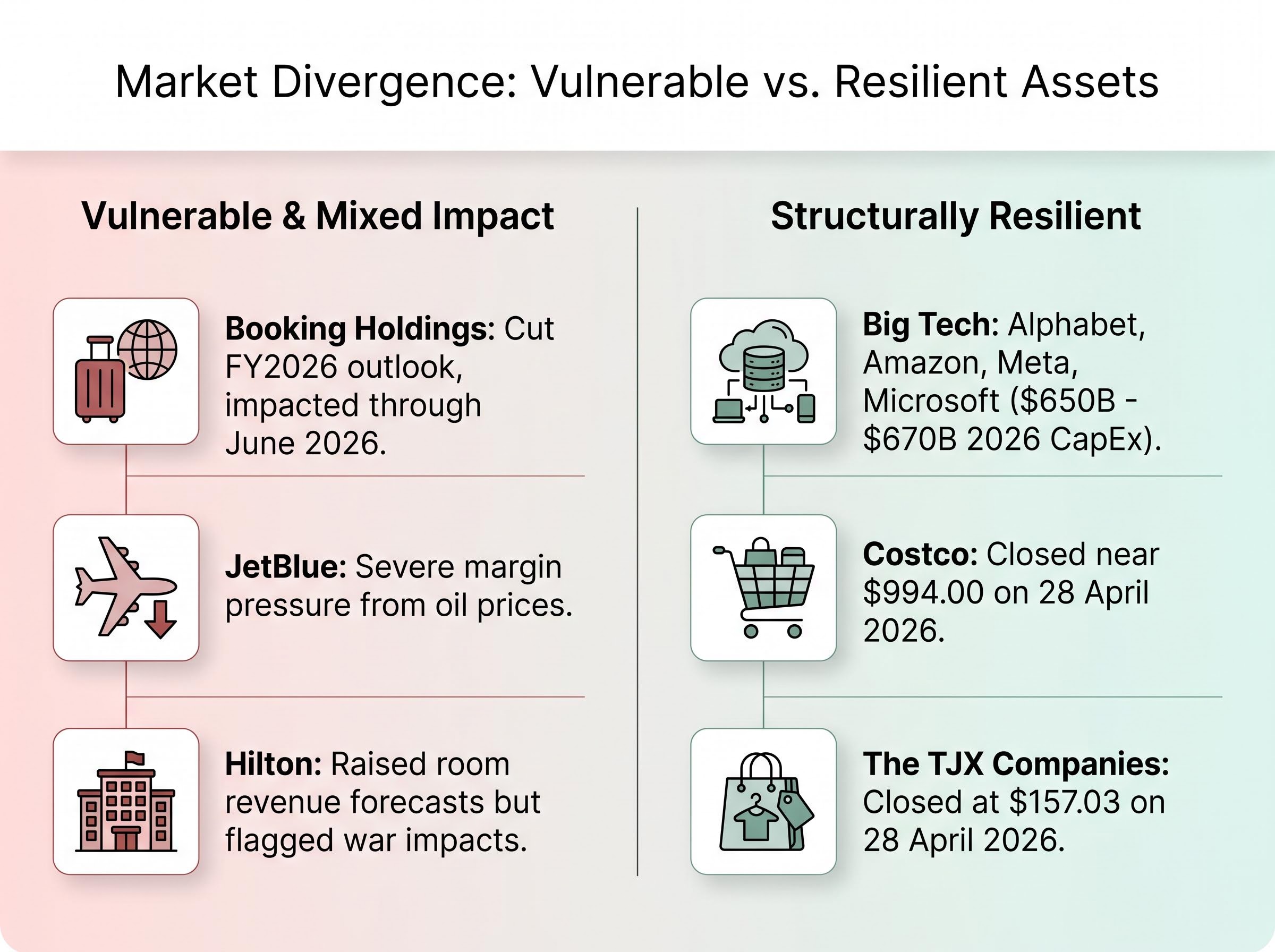

Booking Holdings recently cut its FY2026 outlook, projecting that the Middle East conflict will significantly impact travel demand through at least June 2026. This software-based booking platform faces shifting consumer sentiment but avoids direct commodity exposure. Conversely, Hilton presents a mixed picture, raising annual room revenue forecasts broadly while actively flagging negative impacts from the war.

Beneath these mixed retail signals lies a broader trend of unsustainable consumer spending patterns, as affluent buyers temporarily prop up aggregated demand while middle income households rapidly deplete their pandemic savings buffers.

This divergence translates abstract inflation data into concrete earnings risk. The market is distinguishing between companies managing wary consumers and those entirely exposed to raw input costs. Corporate guidance confirms the sector is baking in a prolonged timeline for Middle East hostilities.

Aviation Margin Squeeze

Physical transport operators face a more severe and immediate crisis. JetBlue is currently experiencing severe margin pressure directly linked to the near doubling of global oil prices. The broader aviation sector is absorbing the full force of this commodity shock without a clear hedging mechanism.

Airlines cannot easily pass all of these surging jet fuel costs onto passengers. The consumer base is already dealing with a broader affordability crisis, limiting their capacity to absorb higher ticket prices without reducing travel frequency. This demand destruction leaves operators with few options to maintain historical profitability metrics.

This dynamic creates a hard ceiling on revenue growth while operating expenses continue to climb. Consequently, airline equities remain particularly vulnerable to the current combination of high oil prices and wary consumers.

Portfolio Defense Through Value Retail and Tech Infrastructure

While transport sectors absorb the shock, specific market segments are successfully insulating themselves from macroeconomic chaos. Capital is rotating toward a barbell approach, balancing value-focused defensive retailers with massive technology capital expenditures.

- AI Infrastructure Providers: Big Tech companies remain largely immune to current consumer inflation pressures. Consensus expectations project Alphabet, Amazon, Meta, and Microsoft will spend a combined $650 billion to $670 billion in 2026 Capital Expenditures. This spending is driven by data centre demands, generating a revenue surge for infrastructure partners like Bloom Energy.

- Value Retailers: In a constrained consumer environment, defensive positioning provides structural resilience. Companies like Costco and The TJX Companies benefit from consumers trading down for basic necessities. Costco closed near $994.00 and TJX closed at $157.03 on 28 April 2026, demonstrating equity stability amidst broader market volatility.

- Digital Payment Networks: Companies providing critical transaction infrastructure benefit from the inflationary environment without carrying physical inventory risk. Second-quarter payment volume surges for Visa and American Express highlight how payment processors capture higher nominal transaction values as consumer prices rise.

Investors face a market where capital is selectively hiding and thriving. Artificial intelligence infrastructure and digital payment networks generate growth independent of physical supply chains. Concurrently, value retail captures the diverted consumer spending as household budgets tighten.

These sector divergence trends highlight the mechanistic impact of sustained inflation, where capital automatically rotates out of vulnerable hospitality businesses into companies with pricing power or essential tech utility.

This structural resilience provides an actionable blueprint for capital allocation. It allows investors to adjust allocations away from vulnerable sectors and toward companies providing critical efficiency infrastructure.

Managing the Prolonged Market Reality

The convergence of a geopolitical energy shock with the Federal Reserve’s restrictive policy stance creates a prolonged test for equity markets. Inflation pass-through from global conflict ensures that interest rates will likely remain elevated, even as domestic economic growth indicators stall.

Sovereign credit and macroeconomic risk analysis highlights that this specific combination of persistent energy inflation and tighter financing conditions pushes developed markets dangerously close to a formal recessionary threshold.

This environment demands extreme selectivity in equity allocation. The structural advantages of technology infrastructure and defensive retail clearly separate them from sectors carrying heavy commodity exposure. Adjusting portfolio weights to reflect these realities serves as a necessary defensive positioning strategy.

Looking forward, impending technology sector earnings releases will act as the ultimate test of market resilience against these macro headwinds. These financial reports will determine if corporate capital expenditure can continue offsetting the economic drag created by wary consumers.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are subject to change based on market developments and company performance.