Warsh Strips Fed Statement to 130 Words, Drops All Guidance

1 min ago

Apple CEO Tim Cook has told The Wall Street Journal that memory chip costs have become “no longer sustainable,” warning the situation will drive an “increasing impact” on the company’s business beyond June 2026. The comments arrive alongside a confirmed price increase on the entry-level Mac Mini in May 2026 and an admission that Apple has been burning through a stockpile of pre-purchased memory inventory to shield margins. Once that buffer is exhausted, the full weight of industry-wide memory inflation hits Apple’s cost structure directly. What follows breaks down exactly what Cook confirmed, what remains unannounced, how the cost pressure maps to Apple’s financials, and what the coming months mean for AAPL investors watching gross margins and the 30 July earnings call.

Cook’s language left little room for ambiguity. Memory costs were already elevated in the March quarter. They will be “significantly higher” in the June quarter. Beyond that, the pressure will drive an “increasing impact” on Apple’s business.

Cook characterised memory costs as “no longer sustainable,” signalling a structural shift rather than a temporary supplier squeeze.

The buffer strategy Apple has been running, selling through stockpiled memory inventory purchased at lower prices, is finite by design. As those supplies dwindle, the gap between what Apple pays and what it paid closes. The structural driver sits upstream: DRAM and NAND flash suppliers are redirecting manufacturing capacity toward AI and data-centre customers, where margins are higher and demand is surging. That capacity shift constrains supply for consumer electronics broadly, and it will not reverse on a quarterly timeline.

The capacity shift Cook is describing is not a typical inventory correction; it reflects a memory chip supercycle driven by hyperscaler AI spending that has redirected manufacturing capacity at the foundry level, with new production lines not expected to reach mass output before 2027.

Not all of the pricing narrative carries the same evidentiary weight. Investors should separate what has been executed from what has been signalled and from what remains outright speculation.

The Mac Mini entry-level price increase in May 2026 is confirmed. Cook’s comments to The Wall Street Journal, framing Mac and iPad lines as the earliest categories subject to higher pricing, represent a directional signal but not a formal announcement. Times of India characterised the same comments as Apple having “hinted at possible post-June price hikes” for RAM-sensitive devices. No formal product-by-product pricing schedule had been released as of 17 June 2026.

The speculated foldable iPhone Ultra at approximately $1,999 for a September 2026 event remains analyst and leaker commentary with no Apple confirmation.

| Claim | Status | Source |

|---|---|---|

| Mac Mini entry-level price raised | Confirmed (May 2026) | Apple pricing / Investing.com |

| Mac and iPad lines face higher pricing | Directional signal, not formally announced | WSJ (Cook interview) |

| Foldable iPhone Ultra at ~$1,999 | Speculation, no Apple confirmation | Analyst and leaker commentary |

Investors making near-term decisions need this hierarchy clearly in view. Conflating confirmed actions with speculative scenarios creates asymmetric risk heading into the 30 July earnings call.

Memory inflation refers to sustained price increases across the two main categories of memory chips used in consumer electronics: DRAM (the fast, temporary memory a device uses while running applications) and NAND flash (the permanent storage where files, apps, and the operating system reside). Both categories are affected by the same supply-side constraint: chipmakers are allocating more production capacity to AI accelerators and data-centre hardware, where demand and margins have surged, leaving less capacity available for consumer devices.

The IDC semiconductor market outlook projects DRAM revenues to nearly triple in 2026, driven by hyperscaler and AI infrastructure demand for high-bandwidth memory, a structural repricing of the memory market that leaves consumer electronics manufacturers with little negotiating room on supply costs.

Macs and iPads carry meaningfully higher memory and storage configurations than entry-level iPhones. A base-model MacBook ships with more DRAM and NAND than a base-model iPhone, which makes the per-unit cost impact of memory price increases larger on those product lines.

Apple has historically exhausted several options before raising sticker prices:

Cook’s public acknowledgement that the cost situation is “no longer sustainable” suggests these levers are reaching their limits.

Apple’s chip manufacturing diversification discussions with Intel and Samsung, while focused on logic chips rather than memory, illustrate the broader supply chain calculus Apple is running as it seeks to reduce exposure to any single external supplier relationship, a strategy that shapes how much pricing leverage it can realistically extract from memory vendors.

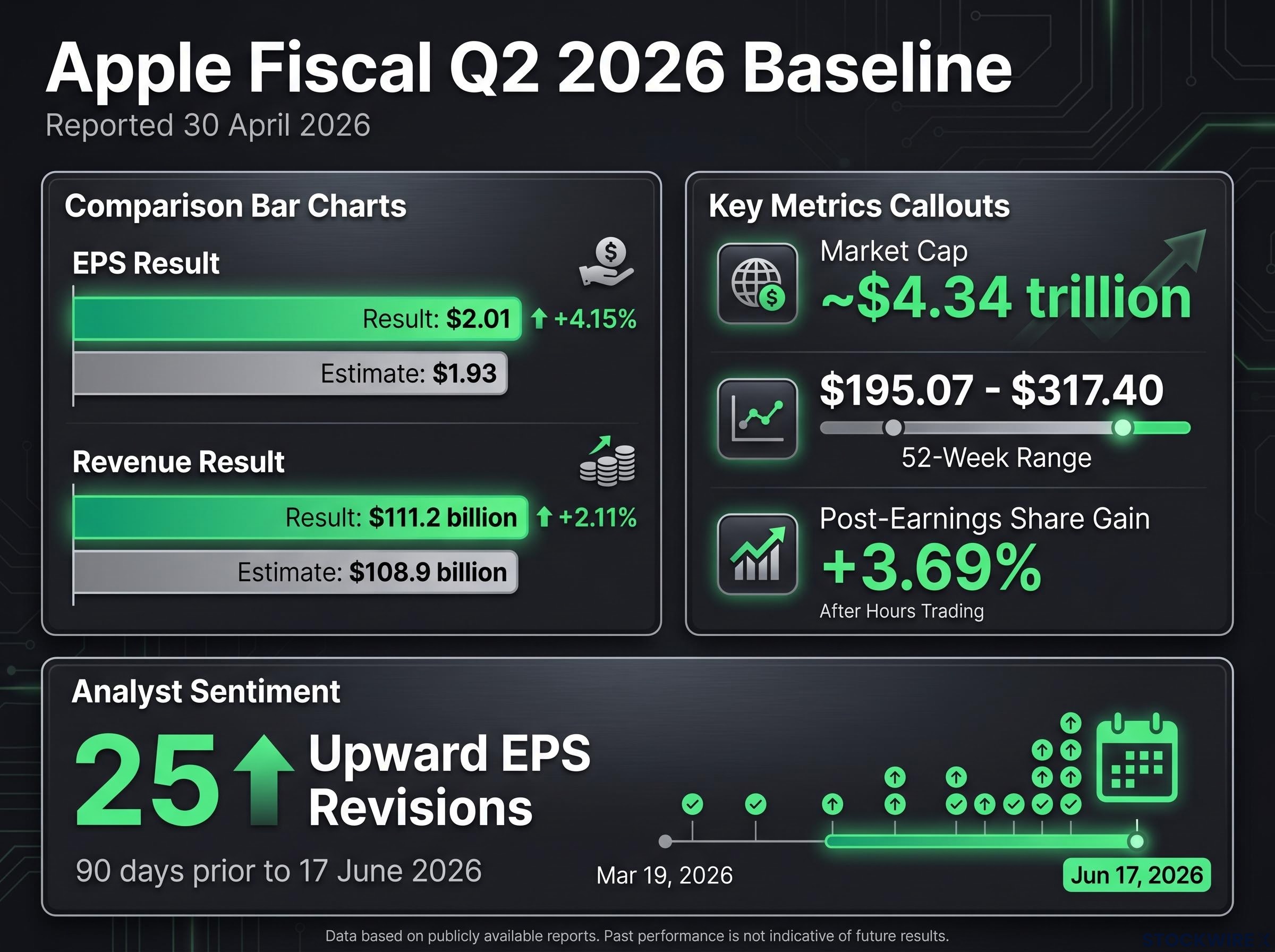

Apple’s fiscal Q2 2026 results, reported 30 April 2026, provide the performance baseline from which the memory cost headwind will be measured.

| Metric | Result | Analyst Estimate |

|---|---|---|

| Earnings per share | $2.01 | $1.93 |

| Revenue | $111.2 billion | $108.9 billion |

Shares gained 3.69% following the Q2 release. Analyst sentiment had been running strongly positive.

Over the 90 days prior to 17 June 2026, analysts issued 25 upward revisions to Apple’s EPS estimates, according to Investing.com.

On 17 June, the day the memory cost commentary circulated, AAPL closed at $295.95, down 1.10%, before recovering to approximately $297.00 (up 0.36%) in after-hours trading. The 52-week range sits at $195.07 to $317.40, with market capitalisation at approximately $4.34 trillion. (All financial figures reported by original source; verification against Apple’s 10-Q and primary market data services is recommended.)

Recent outperformance provides a margin cushion. It also raises the stakes: a gross margin miss driven by memory costs, after a period of upward revisions, carries greater downside surprise risk.

The gross margin trajectory is the central variable. Whether Apple prices through the cost increase, absorbs it while offsetting through mix, or absorbs it without offset determines the investment outcome.

| Scenario | Operative Condition | Gross Margin Implication |

|---|---|---|

| Base case | Targeted price increases on Macs and possibly iPads from late 2026; memory costs stay elevated one to two quarters | Modest temporary compression, then stabilisation |

| Bull case | Price increases plus richer product mix (higher-storage configs, services attach, potential premium tier) more than offset costs | Margin holds or expands; speculative foldable at ~$1,999 adds ASP upside |

| Bear case | Costs persist; competitive dynamics and consumer caution limit pricing power on Macs and iPads | Meaningful compression; unit volumes face dual pressure from higher prices and cautious demand |

The condition separating these paths is demand elasticity. Mac and iPad buyers are generally more price-sensitive than iPhone buyers, which means Apple’s pricing power in those categories has a ceiling. If consumer spending softens, the bear case becomes materially harder to avoid.

For investors seeking exposure to the same supply constraint that is pressuring Apple’s margins, memory chip stocks including Micron, SK Hynix, and Sandisk posted combined gains exceeding 250% over 30 days ending in May 2026, with the supply-demand imbalance that hurts Apple’s cost structure representing a direct revenue tailwind for the producers themselves.

Two events will determine which scenario is unfolding.

These two events are the information gates for AAPL positioning. Investors who monitor the specific signals above will have a materially cleaner read on whether the bull, base, or bear scenario is materialising.

The confirmed facts are clear: Cook has warned of escalating memory costs, Apple has already raised Mac Mini pricing, and the inventory buffer that shielded margins is running down. On the other side of the ledger, Q2 results beat expectations, analyst revisions have been overwhelmingly positive, and Apple retains meaningful product-mix tools.

The balance tips on gross margin. The 30 July earnings call will be the first opportunity to gauge the real P&L impact. Gross margin guidance, more than any headline revenue figure, is the single most important metric to track.

Investors are encouraged to review Apple’s official earnings releases and SEC filings (10-Q) for primary verification of the financial figures cited here and to consult a licensed financial adviser before making investment decisions.

Investors exploring the risk mechanics of positioning around memory-sensitive names will find our deep-dive into AI memory stock volatility useful; it examines how bellwether dependency, multiple expansion, and oligopoly concentration combine to produce 10% single-session swings on macro signals rather than fundamental changes, with direct implications for how investors size positions across the memory supply chain.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Memory inflation refers to sustained price increases in DRAM and NAND flash chips, driven by chipmakers redirecting manufacturing capacity toward AI and data-centre hardware. This raises the per-unit cost of producing Macs and iPads, which carry significantly more memory and storage than entry-level iPhones.

Mac and iPad lines are most exposed because they ship with higher memory and storage configurations than base-model iPhones, meaning the per-unit impact of memory price increases is larger on those product lines. Apple has already confirmed a price increase on the entry-level Mac Mini in May 2026.

Cook told the Wall Street Journal that memory costs are 'no longer sustainable' and will drive an 'increasing impact' on Apple's business beyond June 2026. He identified Mac and iPad lines as the earliest categories subject to higher pricing, though no formal product-by-product pricing schedule had been released as of 17 June 2026.

Investors should focus on gross margin guidance rather than headline revenue, as the magnitude of the memory cost headwind in the profit and loss statement will reveal whether Apple is pricing through the cost increase or absorbing it. Updated guidance ranges and the timing of any formal pricing actions for the back half of the fiscal year are the key signals to track.

Apple has been selling through a stockpile of pre-purchased memory inventory bought at lower prices, which temporarily shields gross margins from the full impact of industry-wide memory inflation. Cook's public acknowledgement that the situation is no longer sustainable signals this inventory buffer is nearly exhausted.