How Many Westpac Shares You Need for $10,000 in Income

2 hrs ago

The public comment period for a rule that could end mandatory quarterly earnings reports in the United States closed on 6 July 2026. Depending on how you invest, that sentence either sounds like relief or a quiet alarm.

The Securities and Exchange Commission (SEC) is weighing whether to make quarterly reporting optional for public companies, replacing it with a semi-annual cadence for those that choose it. The proposal carries political momentum across two Trump administrations, has drawn a fresh round of public submissions, and is being watched closely by corporate finance teams and equity analysts alike. The regulatory process ahead, however, is long. No finalisation date exists.

Here is what the rule would actually change, who benefits, who takes on new risk, and how much of the concern circulating right now is justified versus premature. If you are trying to decide how much attention this deserves today, the answer sits in the mechanics, not the headlines.

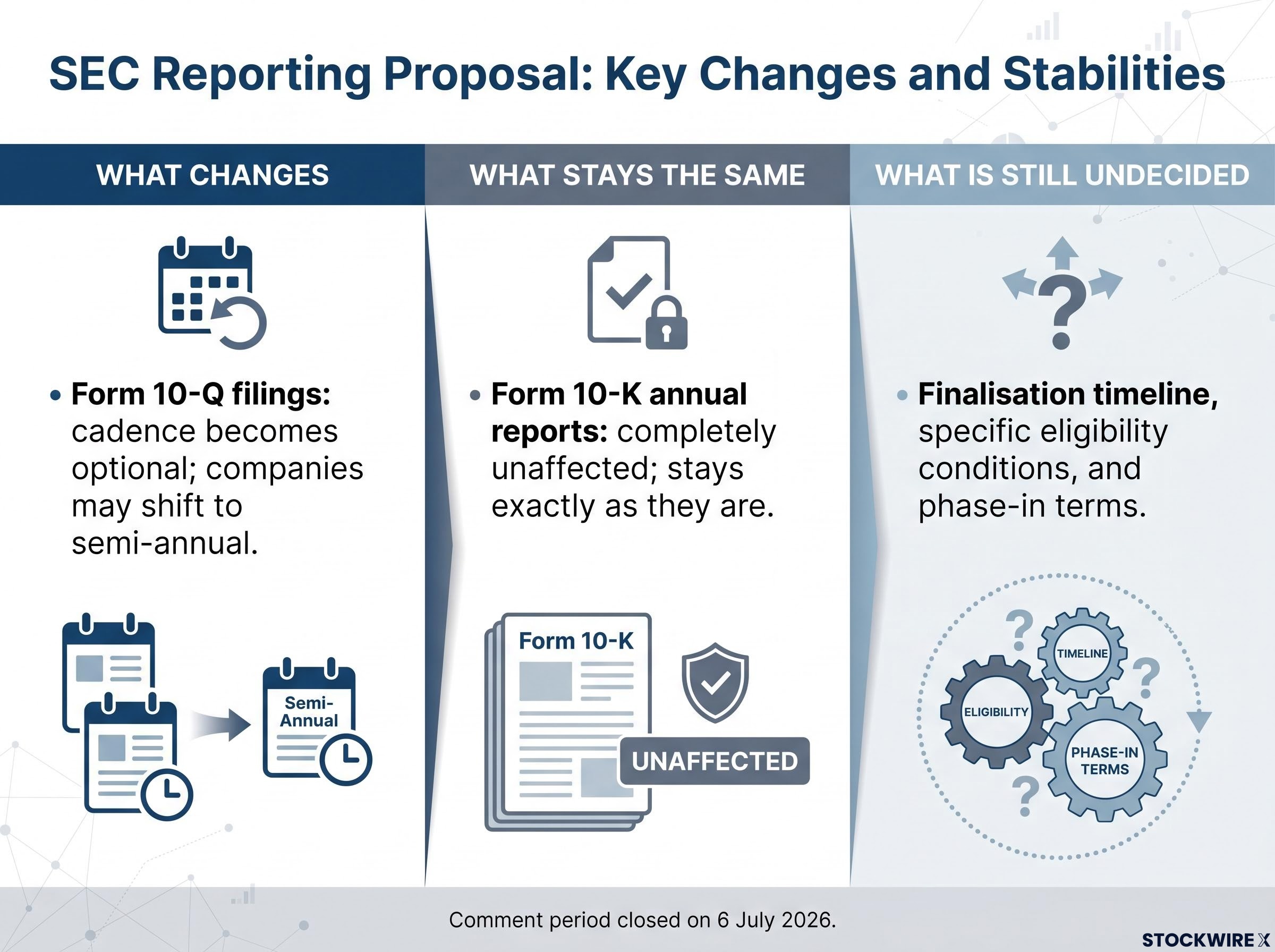

Most of the commentary around this proposal compresses a nuanced regulatory change into a single alarming sentence: “quarterly reporting is ending.” That framing is wrong on two counts.

The proposal makes quarterly Form 10-Q filings, the financial snapshots companies currently file four times per year, optional for eligible companies. It does not touch annual Form 10-K filings. Those stay exactly as they are.

The proposed SEC reporting changes were formally introduced on 5 May 2026, when the commission published its draft rule establishing a new semiannual Form 10-S as an alternative to quarterly Form 10-Q filings; that original proposal document contains the specific eligibility conditions and exclusion categories that the current comment-period submissions are responding to.

More importantly, this is an opt-in mechanism. No company is being forced to reduce its disclosure frequency. Companies that want to keep filing quarterly can do so. The rule, if finalised, creates a choice, not a mandate.

Here is where things stand and what remains undecided:

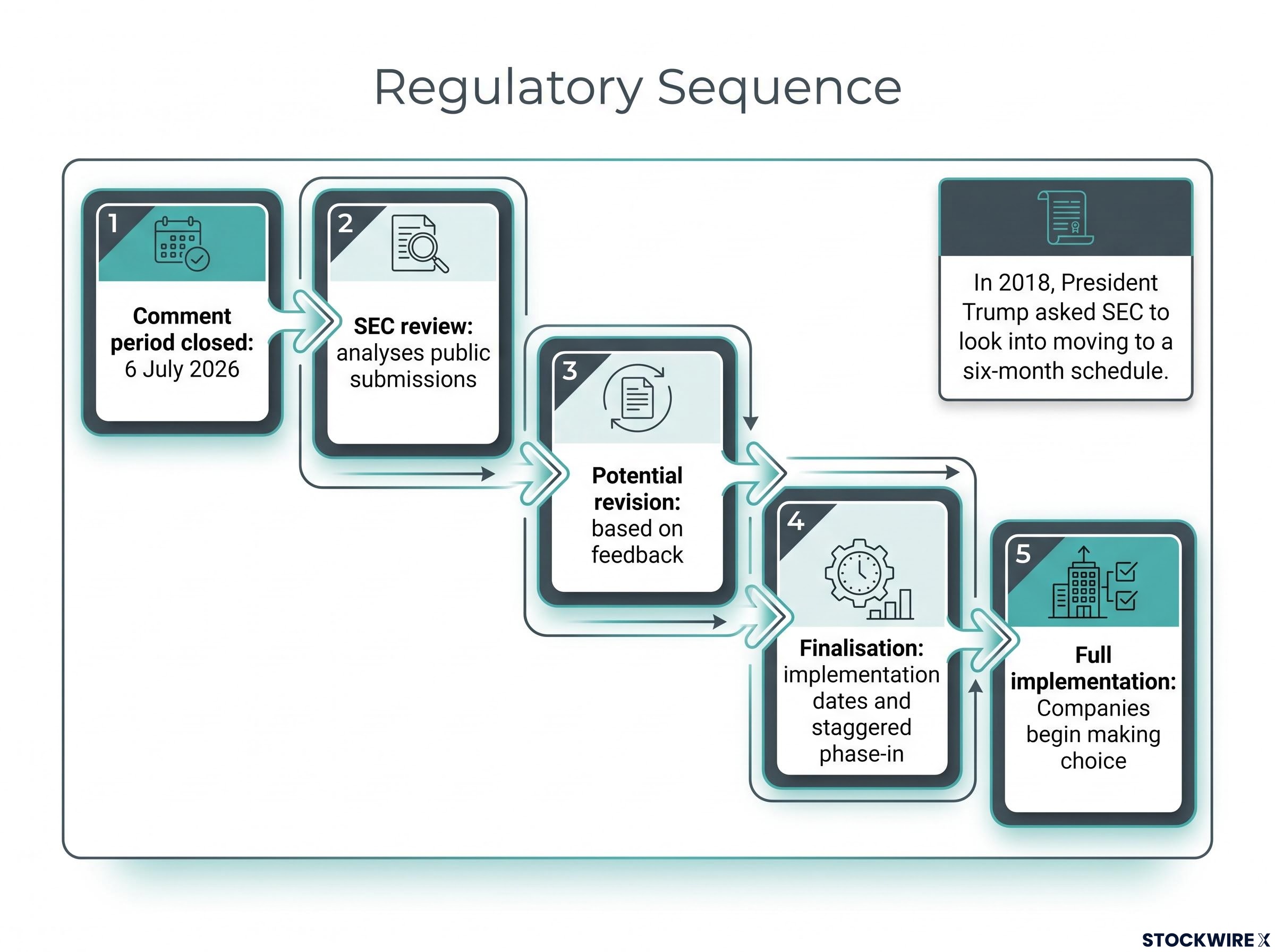

The comment period closed on 6 July 2026. The SEC now reviews submissions, may revise the draft, and moves toward a potential final rule. That process, for regulatory changes of this scale, historically spans several years. During his first term in 2018, President Trump asked the SEC to look into moving to a six-month reporting schedule; the exercise went nowhere and yielded no policy changes. The proposal has been reignited under his current term, but the distance between proposal and implementation remains substantial.

The 2018 SEC quarterly reporting review attracted considerable attention at the time, but the exercise produced no policy changes and the momentum behind it dissipated within months, a historical pattern worth keeping in mind when assessing how much weight to place on the current proposal.

If you are reading a headline that says quarterly reporting is over, you are reading compression of a far more conditional change.

The proposal did not emerge from nowhere, and the people supporting it are not simply arguing for less scrutiny. The case rests on three distinct arguments, each with different levels of evidence behind it.

The most concrete is compliance cost relief. Every 10-Q filing triggers a cycle of legal review, auditor engagement, and investor relations preparation. For smaller and mid-cap companies, where reporting overhead represents a larger share of total costs, reducing that cycle from four times a year to two frees resources that could flow toward operations or product development. No single dollar figure captures the saving cleanly, but the directional point is well established: quarterly reporting is proportionally more expensive for smaller issuers.

The second argument carries a different kind of weight. Supporters contend that reducing ongoing disclosure burden could make public listings more appealing, encouraging more companies to pursue IPOs and making going-private transactions marginally less attractive. If the friction of being public drops, the logic runs, more companies stay public, and more private companies consider listing.

The IPO incentive logic is straightforward: fewer mandatory filings reduce one of the recurring costs that private companies weigh when deciding whether to list. The going-private calculation shifts in the same direction; if disclosure burden is lighter, the appeal of retreating from public markets weakens at the margin. This is a directional argument rather than a transformational one, but it points in a direction regulators have been trying to move for years.

The third and most debated argument is that quarterly reporting fuels short-termism. The claim is that four-times-per-year earnings cycles pressure management teams to optimise for near-term beats rather than multi-year strategic decisions. This framing has prominent proponents, but it remains a hypothesis about corporate behaviour rather than an established finding. Whether reporting frequency actually drives short-term decision-making, or merely reflects it, is contested.

The compliance cost argument has the most concrete grounding. The short-termism argument is the one you will hear cited most often, but it is the least settled. Understanding the difference helps you assess why a specific company might opt in, and whether that choice tells you something useful about how management thinks.

You do not need to theorise about whether major equity markets can function on a twice-yearly disclosure cycle. The European Union already operates that way.

Semi-annual financial reporting is standard practice across EU equity markets. Research into the European experience has not identified measurable adverse effects on liquidity, price discovery, or the quality of institutional investment. Large, sophisticated markets function well with two mandated financial updates per year.

| Feature | U.S. (current model) | EU (current model) |

|---|---|---|

| Reporting frequency | Quarterly (Form 10-Q) plus annual (Form 10-K) | Semi-annual plus annual |

| Form of disclosure | Standardised SEC filings | Regulated interim and annual reports |

| Market depth | Deepest global equity market | Large, liquid, institutionally sophisticated |

| Transition status | Quarterly reporting is the entrenched norm | Semi-annual reporting is well established |

The European precedent tells you the destination is viable. What it does not tell you is how disruptive the American adjustment period would be. U.S. markets are deeply conditioned to the quarterly earnings season rhythm. Analyst models, financial media cycles, and investor positioning are all built around that four-times-per-year cadence. The infrastructure of expectation, not just regulation, would need to shift.

That distinction matters. Compatibility has been demonstrated. A smooth transition has not been guaranteed. When someone cites the European experience as proof the change will work seamlessly, you should recognise they are answering the right question with only half the relevant evidence.

If a company you hold switches to semi-annual reporting, the number of formal financial updates you receive drops from four per year to two. That sounds simple, but the downstream effects are worth thinking through concretely.

The most immediate change is what you lean on between filings. With longer gaps between structured data, your picture of the business depends more on:

None of these are new inputs. You probably use them already. But under a semi-annual cadence, they carry more weight because the formal data arrives less often.

Rigorous earnings report analysis already requires moving beyond the headline EPS figure to cash flow statements, accounts receivable trends, and management guidance language; under a semi-annual cadence, those deeper signals carry even more weight because each formal filing compresses six months of business activity rather than three.

The information asymmetry concern is the sharpest edge of this change. Longer windows between official filings widen the period during which management teams and large, well-connected institutional investors know more than you do. Retail investors and smaller institutions, with less access to alternative data, management relationships, and analytical infrastructure, absorb more of that asymmetry cost. The change is not neutral across investor types, and treating it as though it were understates the real distributional effect.

There is also the question of what happens when the numbers do arrive. With two reporting events per year instead of four, each one accumulates more news. Surprises, both positive and negative, have had longer to build. The result could be larger share price moves at each reporting date, while the frequency of smaller quarterly noise events declines.

That is a trade-off, not a clear win or loss. If you are a long-term holder focused on business quality, less quarterly noise may suit you. If you rely on quarterly data points to calibrate your position sizing or risk management, fewer formal checkpoints means a longer runway between course corrections.

If the rule is finalised, every public company faces a choice: stay quarterly or switch to semi-annual. That choice itself becomes data.

The signalling logic runs in a predictable direction. Companies with consistent results, strong balance sheets, and confident management teams have every incentive to maintain quarterly reporting. Transparency becomes a competitive advantage; frequent disclosure says “we have nothing to hide and want you to see the numbers.” Companies facing earnings volatility, complex restructuring, or margin pressure may find semi-annual cadence more attractive, not necessarily because they want to conceal, but because fewer reporting events mean fewer opportunities for market overreaction to short-term noise.

The same earnings disclosure patterns that investor relations teams use to bury weak results within quarterly filings apply with equal force to semi-annual reports; longer reporting windows give management more time to normalise adverse trends before they become visible in structured financial data.

The caveat matters: some high-quality smaller companies may switch purely for cost reasons. The compliance burden relief is real, and a switch by a well-run small-cap does not automatically signal performance anxiety.

Here is a three-step framework you can apply when a company you own or follow announces its choice:

The right first question when a company switches is not “what are they hiding?” It is “why are they making this choice, and does the reason fit what I already know about this management team?” Investors who treat reporting frequency as signal rather than administrative detail get a lightweight but durable screen for management attitude toward scrutiny.

The proposal is real, but it is not imminent. Here is the actual regulatory sequence:

For regulatory changes of this nature, the journey from proposal to working policy has typically stretched across multiple years, leaving markets considerable room to anticipate and price in the shift before it arrives. Legal challenges and shifting political priorities can extend that timeline further.

No implementation date exists. No portfolio decision you make today needs to be driven by anticipation of this rule.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The years-long timeline is not a reason to ignore the proposal entirely, but it is a reason not to restructure your holdings around it. What matters now is building the analytical habits, deeper business-model understanding, broader information sourcing, sharper reading of management signals, that will serve you regardless of which cadence ultimately governs.

The core takeaway is simpler than the debate suggests. If SEC semi-annual reporting becomes an option, it changes the timing of formal information, not the importance of what that information contains.

You should treat disclosure frequency as a signal worth reading, not just an administrative detail. You should build analytical depth that does not depend on a four-times-per-year information cycle. And you should use the European precedent as evidence of viability without mistaking it for a guarantee of frictionless transition.

The opt-in nature of the rule limits the systemic impact even in a finalisation scenario. Not every company will switch, and those that do will tell you something about themselves in the process. The investors best positioned if semi-annual reporting becomes widespread are those already focused on multi-year business quality rather than quarterly earnings beat cycles.

For readers wanting to understand the structural conditions that make business-quality analysis a durable edge, our dedicated guide to market inefficiency examines how passive investing dominance and behavioural biases widen the gap between price and underlying value, the exact dynamic that longer reporting windows could amplify.

These statements are speculative and subject to change based on market developments and regulatory outcomes. Past performance does not guarantee future results.

Continue watching the SEC’s finalisation process as one input among many. The fundamentals discipline, understanding balance sheets, competitive positioning, and management quality, is the hedge against any shift in how market information gets structured. That does not change with the reporting calendar.

SEC semi-annual reporting means companies would file formal financial updates twice a year instead of four times, using a new Form 10-S rather than the current Form 10-Q. The annual Form 10-K is unaffected under the current proposal.

No. The SEC proposal makes quarterly Form 10-Q filings optional, not mandatory to eliminate. Companies that want to keep filing quarterly can continue doing so, and no company is being forced to switch.

No implementation date exists. The public comment period closed on 6 July 2026, and the SEC must review submissions, potentially revise the draft, and finalise the rule before any phase-in begins, a process that historically spans multiple years.

Retail investors absorb more of the information asymmetry cost under a semi-annual cadence because longer gaps between official filings widen the window during which management teams and well-resourced institutional investors know more than the broader market.

It can signal cost-saving motivations for smaller companies or, in other cases, a preference for fewer formal reporting events during periods of earnings volatility or restructuring. The right first question is whether the stated reason fits what you already know about that management team's track record of transparency.