Most Australian ETF investors know they need to report their distributions at tax time. Fewer realise they are also required to adjust their cost base every single year, and that skipping this step, even once, can produce a compounding error that quietly inflates a capital gains bill years down the track. ETF investing has become mainstream for Australian retail portfolios, but the tax obligations attached to these products are meaningfully more complex than those attached to a savings account or even a direct shareholding. The ATO treats ETFs as managed investment trusts, which means distributions carry multiple components, each taxed differently, and each potentially changing the investor’s cost base. This article walks through every layer of the Australian ETF tax framework: what triggers a capital gains event, how the 50% CGT discount works and when it does not apply, what cost base adjustments are and why they are mandatory, how foreign income and franking credits fit in, and which tools can automate the compliance work so investors are not left doing it manually across dozens of parcels.

Why ETF tax is more layered than most investors realise

The assumption is familiar: ETFs are simple, passive, and set-and-forget. The ATO’s treatment of them is none of those things. Because ETFs are classified as managed investment trusts, every distribution an investor receives is not a single dividend payment but a bundle of components, each carrying a different tax treatment.

The managed investment trust classification is the structural reason ETF distributions carry multiple taxable components: the ATO applies trust taxation rules to flow each income and gains category through to unitholders separately, rather than treating the distribution as a single payment.

A typical ETF distribution may include any combination of the following:

- Income (interest, dividends, or rental income earned by the fund)

- Capital gains (from the fund’s internal buying and selling of underlying holdings)

- Return of capital or tax-deferred amounts

- Foreign income

- Franking credits (for Australian equity ETFs)

Each of these is reported and taxed differently. Critically, an investor does not need to sell a single unit for a tax obligation to arise. When the fund itself trades its underlying holdings and distributes a capital gain, that gain flows through to the investor’s tax return regardless of whether the investor has done anything at all.

The ATO managed fund distribution reporting rules require investors to break down each distribution into its component parts, including income, capital gains, foreign income, and tax-deferred amounts, and to report each component according to its own tax treatment rather than treating the distribution as a single undifferentiated payment.

What the ATO actually sees when your ETF distributes

The ATO receives data directly from fund managers, registries, brokers, and the ASX. In its 5 July 2023 media release, the ATO confirmed that share and managed fund capital gains are a compliance focus area, and that it uses data matching to detect unreported disposals and misreported investment income.

This means omissions or mismatches between what an investor reports and what the ATO already holds are detectable. The source document investors must use is the annual member statement issued by the ETF provider, typically arriving between August and September each year. A broker platform summary alone is not sufficient.

When big ASX news breaks, our subscribers know first

The cost base adjustment problem: why skipping it compounds over time

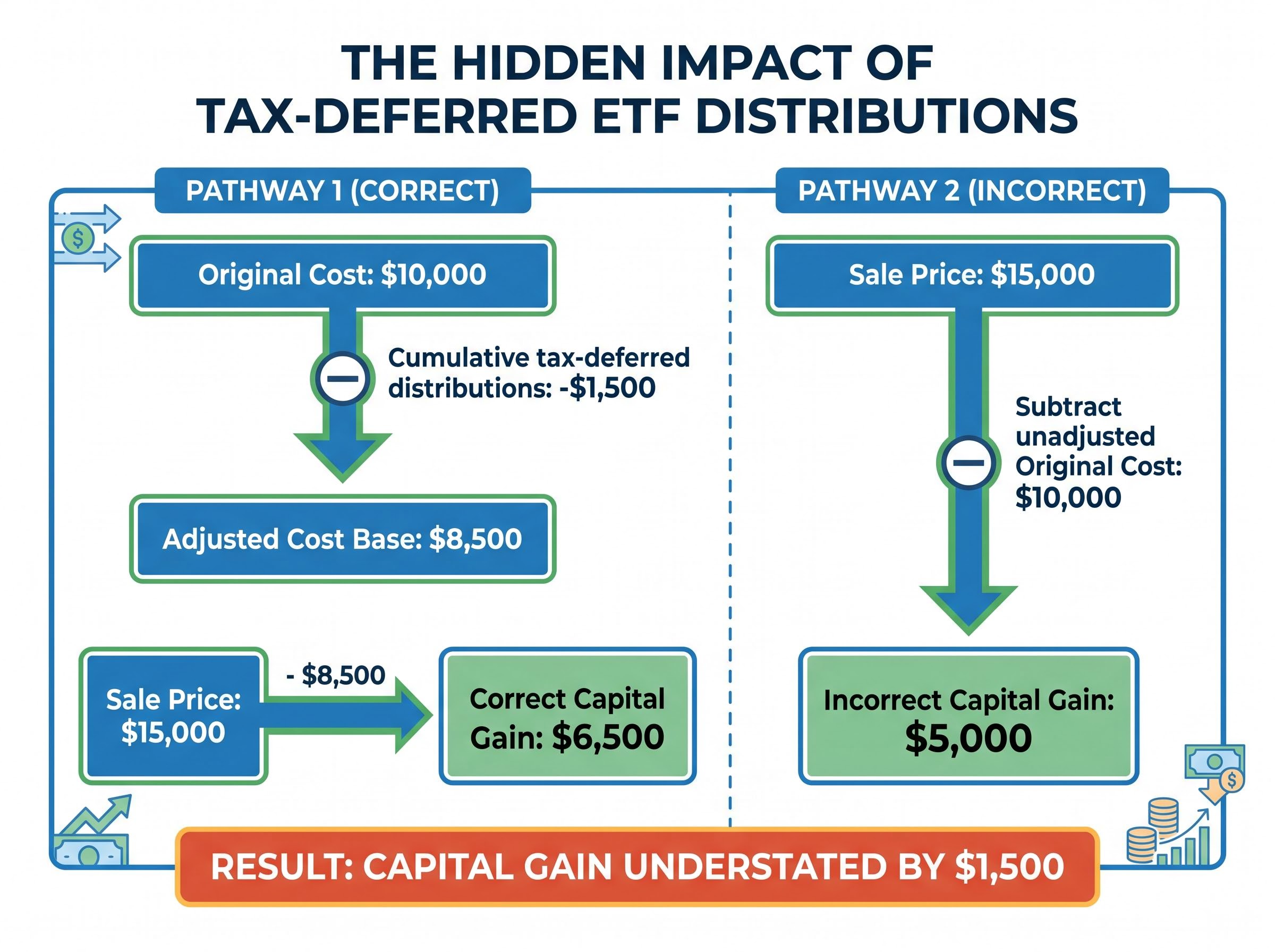

When an ETF distributes a tax-deferred or return-of-capital amount, that amount is not taxed immediately. Instead, it reduces the investor’s cost base in the units held. The cost base is the figure used to calculate the capital gain or loss when units are eventually sold. A lower cost base means a larger capital gain at the point of sale.

The adjustment must be applied parcel by parcel. For an investor who dollar-cost averages monthly, this means every new purchase creates a separate parcel, each with its own original cost and each requiring its own annual adjustment. Over a decade, a monthly contributor could accumulate well over 100 individual parcels. One investor cited in practitioner commentary had done exactly that across approximately 10 years of monthly contributions and had never applied a single cost base adjustment.

The ATO capital gains tax guidance sets out the record-keeping obligations that apply to each CGT asset, including the requirement to maintain parcel-level acquisition records and cost base adjustments for the full period of ownership, not just the year of disposal.

The worked example makes the compounding visible:

- An investor purchases ETF units for $10,000 (original cost base).

- Over several years, the ETF distributes $1,500 in cumulative tax-deferred amounts.

- The adjusted cost base is now $8,500, not the original $10,000.

- The investor sells all units for $15,000.

- The correct capital gain is $6,500 ($15,000 minus $8,500). An investor who never adjusted would calculate the gain as $5,000 ($15,000 minus $10,000), understating the gain by $1,500.

ATO pre-fill data does not perform this adjustment automatically. The obligation to apply it, using the figures from the annual member statement, rests entirely with the investor.

Money Magazine Australia described using a brokerage platform’s “average price” figure instead of the adjusted cost base as “a common and material error” for retail ETF investors.

How the 50% CGT discount works, and the traps around it

Australian individuals who hold a capital gains tax asset for more than 12 months before disposal are generally eligible to reduce the taxable capital gain by 50%. For a long-term ETF investor, this discount is one of the most valuable tax concessions available. The discount remains unchanged for individuals through FY2026; proposed Budget changes from 1 July 2027 are not yet law.

The proposed CGT discount changes announced in the 2026 Federal Budget would replace the 50% discount with CPI indexation and a 30% minimum tax floor from 1 July 2027, a structural shift that Stockspot modelling estimates could cost a business founder selling a $1 million asset more than $225,000 in after-tax proceeds.

The 12-month holding period runs from the acquisition date of each parcel separately. In a dollar-cost averaging portfolio, parcels purchased in different months will cross the 12-month threshold at different times. An investor selling units needs to identify which parcels are being disposed of and confirm each one individually qualifies.

| Scenario | Holding Period | CGT Discount Eligible | Common Error |

|---|---|---|---|

| Short-term ETF sale | Under 12 months | No | Applying the 50% discount to sub-12-month gains |

| Long-term ETF sale | Over 12 months | Yes | Failing to claim the discount when eligible |

| Fund-distributed gain already discounted | N/A (fund-level) | No (already applied inside the fund) | Applying the individual discount again, double-discounting the gain |

| Trading activity misclassified as investing | Varies | No (trading stock rules apply) | Claiming CGT discount on assets held on revenue account |

The Tax Institute reported in 2024 that investors frequently apply the 50% discount to gains on assets held less than 12 months. CPA Australia flagged a related pattern: investors confusing trading and investing activity, incorrectly claiming the CGT discount on assets that are properly treated as trading stock.

The DRP trap most investors overlook

Distribution reinvestment plan (DRP) units are treated as a new acquisition at the time of reinvestment. The cost base of those units equals the market value of units received on the reinvestment date. CPA Australia found in 2024 that investors frequently record no cost base at all for reinvested distributions, creating an additional omission that compounds alongside the cost base adjustment errors discussed above.

Foreign income and franking credits: the reporting obligations most investors miss

ETFs that hold US or global equities distribute foreign income to their Australian unitholders. The ATO expects this income to be reported at the gross pre-withholding amount, not the net figure the investor receives. The difference matters because US withholding tax, typically 15% under the Australia-US tax treaty, is deducted at the fund level before the distribution reaches the investor.

That 15% withholding is available to Australian investors as a foreign income tax offset, reducing the risk of double taxation, but only if the investor reports it correctly. H&R Block Australia noted in 2024 that foreign income from ETFs is frequently omitted entirely or entered as the net rather than the gross amount.

The correct reporting sequence for US-sourced ETF income:

- Locate the gross foreign income figure on the annual member statement.

- Locate the foreign tax paid figure on the same statement.

- Report the gross amount as foreign income in the tax return.

- Claim the foreign tax paid as a foreign income tax offset.

The AFR reported in 2024 that the ATO uses data matching with overseas tax authorities, including the US, and expects investors to declare gross foreign income and foreign tax paid as shown on the ETF annual tax statement.

Franking credits on Australian equity ETFs represent a separate mechanism. Fully franked dividends carry a tax credit reflecting company tax already paid. This credit must be included as part of the grossed-up income in the investor’s tax return. It is a tax offset, not a bonus cash payment. Treating franking credits as tax-free income, rather than grossing up the distribution and then applying the offset, is another frequently observed error.

How portfolio tracking tools automate the compliance burden

For investors with years of accumulated parcels and no history of cost base adjustments, the prospect of manual correction is daunting. Purpose-built Australian portfolio tracking platforms offer an alternative.

Sharesight is the most prominently discussed tool in 2024-2025 Australian financial media for this purpose. It supports automatic trade imports from major brokers, parcel-by-parcel CGT calculations, DRP tracking, franking credit handling, and foreign income reporting aligned to Australian tax rules. Users can enter ETF annual tax statement adjustments, and the platform reflects updated cost bases across all affected parcels.

Four approaches to ETF tax compliance, ranked by capability:

- Broker platform reports only: A starting point, but CPA Australia notes these often fail to incorporate ETF annual tax statement cost base adjustments, particularly for tax-deferred amounts and off-market corporate actions.

- Manual spreadsheet: Flexible but labour-intensive and error-prone, especially for portfolios with dozens or hundreds of parcels accumulated over years.

- Dedicated portfolio tracker (e.g. Sharesight): Automates parcel-by-parcel calculations, DRP cost bases, and generates tax reports. Handles the annual adjustment workflow that spreadsheets struggle with at scale.

- Portfolio tracker combined with ASX announcement tool: The AskAnna “Best ASX Stock Research Tools for 2026” guide recommends pairing a tracker with an announcement intelligence tool to cover “the full workflow from monitoring to analysis to record-keeping”, ensuring distribution and tax statement announcements are captured as they are released.

What to do if you have never adjusted your cost base

The first step is to locate prior-year annual ETF member statements. Most ETF providers make historical statements available through their online investor portal. From there, investors can either use a dedicated portfolio tracking platform to reconstruct cost base history or engage a tax professional to work through the adjustments before the next disposal event. Waiting until the ATO queries a return is the most expensive way to discover the problem.

For investors who want a step-by-step walkthrough of the annual adjustment workflow before the next distribution season, our dedicated guide to AMIT cost base adjustments for ETF investors covers the three annual tax obligations in sequence, including the parcel-by-parcel mechanics that trip up dollar-cost averaging portfolios.

What Australian ETF investors should do before 30 June

The annual ETF member statement typically arrives between August and September, after the financial year closes on 30 June. This means the pre-30 June action is planning and reviewing, with statement reconciliation completed in the new financial year before lodging the return.

A structured six-step checklist:

- Retrieve all prior-year annual member statements for every ETF held.

- Confirm cost base records exist for every parcel, including DRP units, and that annual adjustments have been applied.

- For any planned disposals before 30 June, verify the holding period of each parcel to confirm 50% CGT discount eligibility.

- Check that foreign income has been captured at the gross amount, with foreign tax offsets recorded.

- Confirm that franking credits are included as grossed-up income, not treated as tax-free cash.

- After the annual member statement arrives in August or September, reconcile all distribution components against the return before lodging.

Portfolio simplicity and tax administration are more closely linked than most investors appreciate: keeping an ETF portfolio to 2-6 funds reduces the number of annual member statements to reconcile, limits the number of cost base parcels accumulating each year, and makes the six-step pre-30 June checklist manageable rather than overwhelming.

The concessional superannuation contributions cap is $30,000 for FY2025-26, rising to $32,500 from 1 July 2026 (FY2027). Investors planning pre-30 June contributions to reduce taxable income should confirm remaining cap space before contributing.

The ATO has confirmed its compliance focus on share and managed fund CGT errors. Proactive record-keeping is a lower-cost exercise than retrospective correction after a data-matching query.

The cost of doing nothing is paid at the point of sale

Cost base adjustment errors are invisible for as long as the investor holds their units. They surface at disposal, when the investor’s calculated gain diverges from the figure the ATO can reconstruct using fund manager data. The gap produces amendment risk and potential penalties.

The four compliance layers covered in this article (CGT and cost base adjustments, the 50% CGT discount, foreign income reporting, and franking credit treatment) are interconnected. A cost base error changes the capital gain, which changes the CGT discount calculation, which changes the final tax payable. They compound rather than sit in isolation.

The practical starting point: locate the most recent ETF annual tax statement, verify whether cost base adjustments have been applied to each parcel held, and cross-check against a dedicated tracking platform. Where historical records are incomplete, engaging a tax professional before the next sale, rather than after an ATO query, is the lower-risk path.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Tax rules are subject to change based on legislative developments.