Austin Engineering Cuts FY26 Guidance as Americas Lag Despite Productivity Gains

Austin Engineering revises FY26 guidance as operational improvements take hold

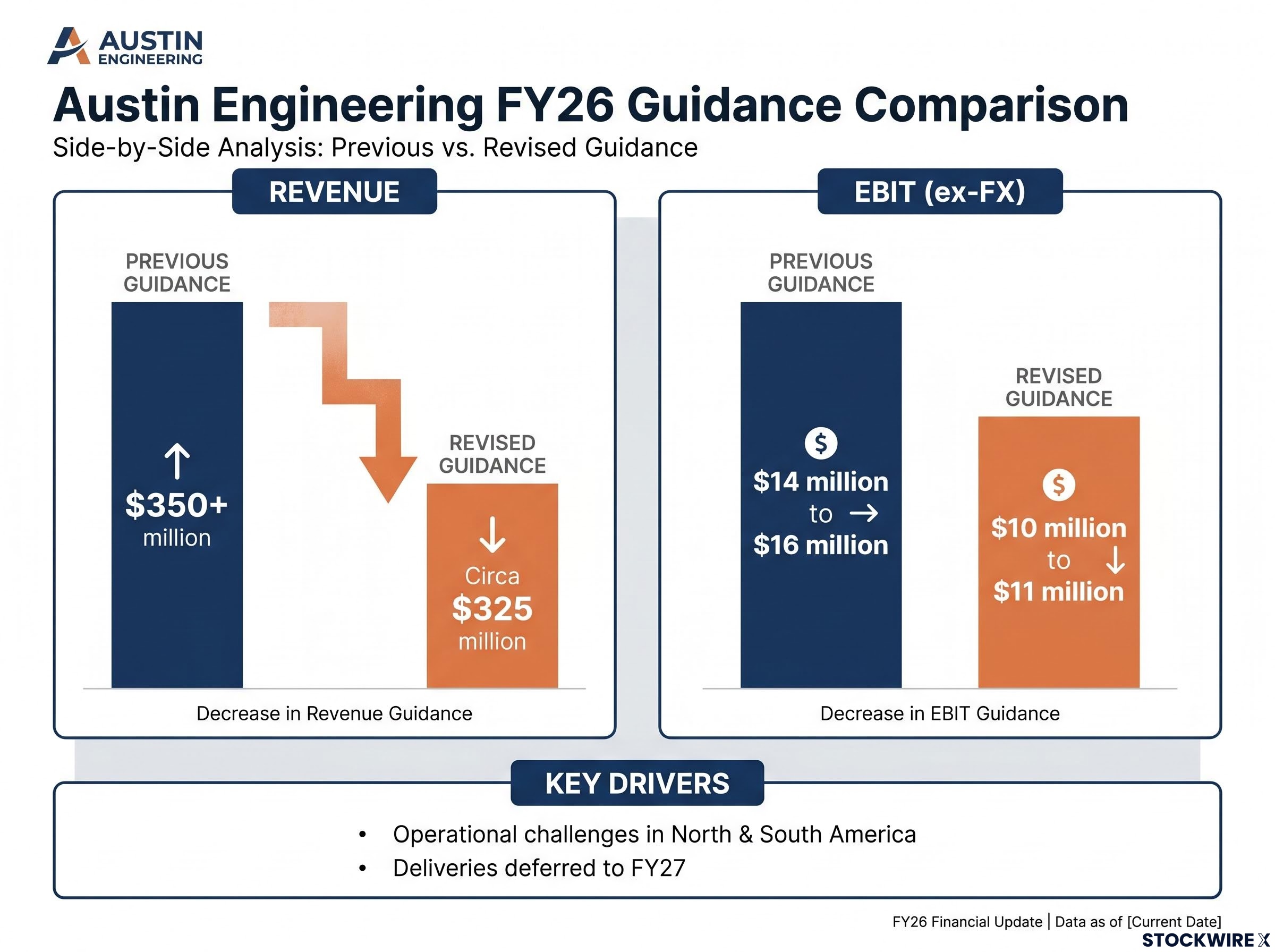

Austin Engineering has revised its full-year FY26 guidance, with revenue now expected at circa $325 million (down from $350+ million) and EBIT at $10 million to $11 million (excluding FX movements, previously $14 million to $16 million). The revision reflects a combination of operational challenges in North and South America and the timing of certain product deliveries now expected to occur in FY27 rather than FY26.

The company noted that whilst trading conditions improved during May and June 2026, the pace of operational improvement has been slower than anticipated, resulting in a number of sales and deliveries being deferred into FY27. This deferral represents a timing shift rather than lost demand, with implications for near-term financial performance but not a structural deterioration in the business.

| Guidance Metric | Previous FY26 Guidance | Revised FY26 Guidance |

|---|---|---|

| Revenue | $350+ million | Circa $325 million |

| EBIT (ex-FX) | $14 million to $16 million | $10 million to $11 million |

When big ASX news breaks, our subscribers know first

What’s driving the guidance revision?

The downgrade stems from two core factors: operational challenges in the Americas and the timing of product deliveries shifting into FY27. North America has shown measurable productivity improvement, rising to 75% from a low of 62%. Whilst progress has been encouraging, further efficiency improvements are required to increase throughput and bring margins to targeted levels.

South America has remained below expectations. Austin is mobilising additional operational expertise to Chile and will maintain a permanent senior management presence in the region for the next two months to ensure the planned systems and process improvements are embedded. This targeted intervention is designed to address site-specific performance issues.

Asia Pacific, comprising principally Australia and Indonesia, has continued to perform in line with expectations, indicating that the operational challenges are geographically isolated rather than systemic across the business.

The current revision is the second guidance reset in the FY26 cycle: the H1 FY26 guidance downgrade in February 2026 had already reduced revenue expectations from $370-380 million to $350+ million and EBIT from $30-34 million to $14-16 million, reflecting the scale of operational disruption that accumulated across Chile, North America, and Indonesia in the first half.

| Region | Performance Status | Key Detail |

|---|---|---|

| North America | Improving | Productivity at 75% (from 62% low) |

| South America | Below expectations | Senior management presence for 2 months |

| Asia Pacific | In line | Australia & Indonesia stable |

Understanding productivity metrics in heavy engineering

Productivity percentage in a manufacturing and engineering context measures how efficiently labour and equipment convert inputs into finished products. It captures the ratio of actual output to theoretical maximum output under optimal conditions. A facility operating at 62% productivity is producing roughly six units for every ten it could theoretically produce, leaving significant capacity underutilised.

Moving from 62% to 75% productivity represents a material improvement. Higher productivity means more output from the same cost base, which translates to improved margins over time as fixed costs are spread across greater volume. For investors, productivity gains are a leading indicator of margin recovery, even if revenue is temporarily softer due to timing delays or market conditions.

In Austin’s case, the North American productivity improvement suggests that operational interventions are taking effect, with throughput increasing without proportional cost increases. The company has noted that further efficiency improvements are required to reach targeted margin levels, indicating that productivity gains remain a key focus area for management.

Management response and FY27 positioning

Austin is taking targeted actions to address the operational challenges in South America, including mobilising additional operational expertise to Chile and embedding senior management presence in the region for the next two months. These interventions are designed to ensure that planned systems and process improvements are fully implemented and sustained.

The South American challenges have deeper roots than current operational execution: the Chile OEM contract renegotiation completed in March 2026 replaced a recurring loss-making arrangement with improved pricing and payment terms, with the $6.7 million initial purchase order principally executing in FY27.

In North America, the company continues to focus on further efficiency improvements to increase throughput and bring margins to targeted levels. The productivity increase to 75% demonstrates that the operational framework is responding to management’s initiatives, though additional gains are required to meet internal benchmarks.

Sy van Dyk, CEO and Managing Director

“While our FY26 result will be below our previous expectations, we are encouraged by the operational improvements being achieved across North and South America. The pace of improvement has been slower than anticipated, however the actions we are taking, position us well to deliver improved performance in FY27.”

Management has explicitly positioned FY27 as the year where these improvements should translate to better financial outcomes. The deferred deliveries from FY26 represent revenue that is expected to flow through in the next financial year, providing a degree of visibility into near-term order flow.

What this means for investors

The update presents a near-term setback but not a structural deterioration in the business. Key takeaways include:

- FY26 guidance reduced, but a portion relates to timing (deliveries deferred to FY27 rather than lost).

- Operational improvements are underway in the Americas, with measurable productivity gains in North America from 62% to 75%.

- Asia Pacific remains stable and on track, indicating that performance issues are geographically isolated.

- Management is deploying additional resources to address South American underperformance through senior management presence and operational expertise.

- FY27 is positioned as the year where these improvements should translate to better financial outcomes, with deferred deliveries expected to occur in FY27.

The investment case turns on execution in FY27. Investors will be monitoring whether the productivity gains in North America can be sustained and extended, and whether the interventions in South America deliver measurable improvement in the first half of the next financial year.

The next major ASX story will hit our subscribers first

Austin Engineering at a glance

Austin is a global engineering company with over 50 years of history, partnering with mining companies, contractors, and original equipment manufacturers to create engineering solutions that deliver productivity improvements to their operations.

- Market position: Leader in the design and manufacture of loading and hauling solutions, including off-highway dump truck bodies, buckets, water tanks, and related attachments for both open-cut and underground operations.

- Geographic footprint: Headquartered in Perth, with operations in Australia, USA, Chile, and Indonesia, serving major mining sites globally.

- Value proposition: Proprietary design and engineering IP focused on delivering the lowest cost per tonne to end users, reducing fuel usage per material carried and creating more sustainable mining operations.

- Service offering: Complementing its product range are repair and maintenance services performed in workshops and on client mine sites, plus spare parts supply.

Don’t Miss the Next Industrial Breakout

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to start receiving alerts the moment market-moving announcements hit the ASX.