Alfabs Eyes Triple Free Cash Flow by FY28 With $8M Cost Reduction Programme

Alfabs outlines pathway to triple free cash flow by FY28

In its June 2026 Investor Day presentation hosted at the Kurri Kurri facility, Alfabs Australia outlined a comprehensive free cash flow improvement plan targeting a 2x–3x increase by FY28. Managing Director and CEO Matt Torrance, alongside CFO Peter White, presented a disciplined capital allocation framework requiring all discretionary capital to meet >15% IRR hurdle rates. The presentation articulated a clear pathway to dividend reinstatement, subject to defined financial and leverage milestones through FY27.

The strategic update signals a fundamental shift from EBITDA-focused growth to cash conversion, addressing post-IPO underperformance in free cash flow generation despite strong earnings growth.

When big ASX news breaks, our subscribers know first

What is free cash flow and why does it matter?

Free cash flow represents the cash a business generates after paying operating costs, taxes, interest, and maintaining its equipment. It differs from EBITDA, which measures accounting profit before depreciation and interest, because FCF reflects actual cash available rather than paper earnings. For Alfabs, the presentation defined FCF as EBITDA minus interest, income tax, working capital changes, and maintenance capital expenditure.

This metric matters to investors because FCF funds dividends, debt repayment, and growth initiatives without requiring external capital. The presentation highlighted a critical gap: Alfabs’ recent EBITDA growth has not translated to proportional cash generation, with working capital investment and oversized workshop capacity constraining conversion rates through FY25 and H1 FY26.

Cash improvement plan targets ~$8 million pre-tax uplift in FY27

The Company detailed a cash improvement plan expected to deliver an ~$8 million pre-tax uplift in FY27, comprising two primary initiatives. Workshop resizing is forecast to contribute ~$5 million in annualised pre-tax cash flow uplift, while corporate cost reduction has been increased from an original $2 million target to ~$3 million in annualised savings.

Mining workshops are being consolidated into the fully-owned Kurri Kurri facility following completion of the Malabar contract build-out, with a smaller service presence retained in Wollongong. The presentation indicated a 20%–25% reduction in corporate costs is expected versus H1 FY26 annualised levels.

The workshop resizing initiative builds on the workshop consolidation and refinancing program Alfabs announced in April 2026, which originally targeted approximately $6 million in combined annual cash flow improvements through facility restructuring and a NAB loan tenor extension.

| Initiative | FY27 Cash Uplift |

|---|---|

| Workshop resizing | ~$5m |

| Corporate cost reduction | ~$3m |

| Total | ~$8m |

These initiatives represent near-term, tangible levers already in execution, providing visibility into the FY27 cash profile.

Capital allocation framework prioritises returns over growth

Management presented a disciplined capital allocation framework anchored in four key principles. First, the Company will prioritise reinvestment in opportunities targeting >15% IRR, including mergers and acquisitions. Second, a net debt target of 1.5x–2x EBITDA must be maintained before distributions are considered. Third, the dividend policy of 50% of NPAT was reconfirmed, conditional on FCF generation and leverage milestones. Fourth, excess cash will be returned to shareholders when available.

The presentation noted that a dividend reinvestment plan is under consideration. The NAB dividend covenant requires <2.25x leverage for a 50% NPAT dividend to be paid. This framework signals a shift away from “growth for growth’s sake” — acquisitions and capital expenditure must now clear explicit hurdle rates, protecting shareholder capital.

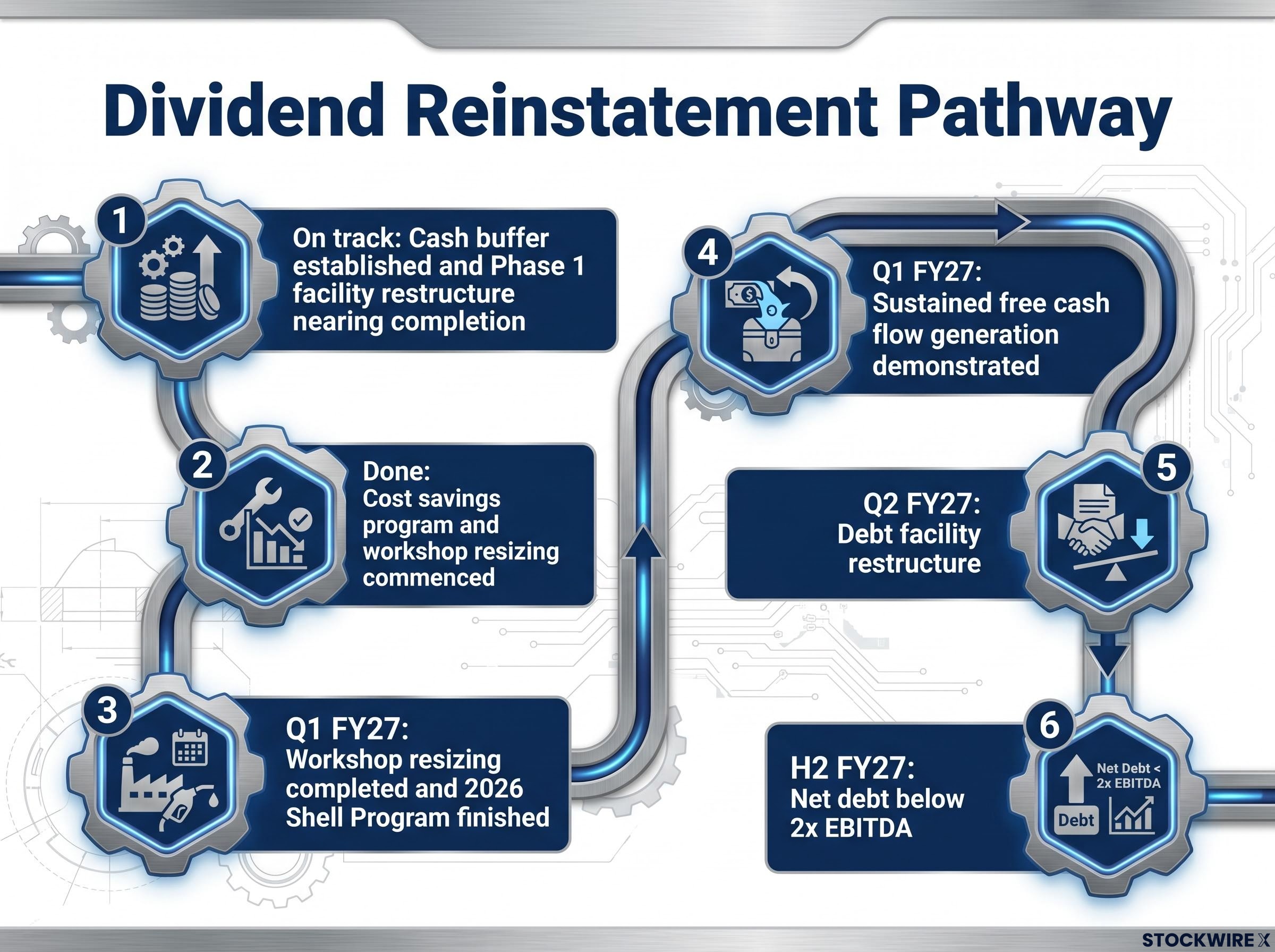

Dividend reinstatement pathway with defined milestones

The presentation outlined a clear timeline for dividend reinstatement through FY27, structured around six checkpoints:

- On track: Cash buffer established and Phase 1 facility restructure nearing completion

- Done: Cost savings program and workshop resizing commenced

- Q1 FY27: Workshop resizing completed and 2026 Shell Program finished

- Q1 FY27: Sustained free cash flow generation demonstrated

- Q2 FY27: Debt facility restructure

- H2 FY27: Net debt below 2x EBITDA

Management has provided explicit, trackable milestones — giving investors clear checkpoints to monitor progress toward shareholder returns.

Mining division remains the core cash engine

The Mining Services division represents approximately 50% of group revenue and maintains equipment utilisation currently exceeding 80%. The presentation highlighted the Shell Program as a key growth lever, which involves rebuilding acquired mining equipment at lower cost than buying new units.

FY26 Shell Program delivery included:

- 1 Continuous Miner

- 2 AX10s

- 6 Driftrunners

The Malabar contract, with a 4–6 year term worth approximately $10 million per annum, was cited as an example of long-term recurring revenue streams. The mining hire business generates stable, recurring cash flows — this is where FCF improvement will primarily originate.

Engineering positioned for infrastructure recovery in FY28

The Engineering division, also representing approximately 50% of revenue, is navigating near-term softness in the infrastructure pipeline. Management indicated FY27 is expected to remain soft, with recovery weighted to FY28. The business has maintained Queensland Government pre-qualified vendor status and Olympic-aligned credentials, though no Olympic-related work has been contracted to date.

Major venue and transport packages associated with the Brisbane Olympics are not expected to award until late 2027 or 2028. The Engineering division provides upside exposure to the infrastructure cycle with minimal capital employed — a capital-light complement to the mining business.

Global coal demand supports long-term equipment hire outlook

The presentation cited IEA Coal 2025 data showing global coal consumption reached a record 8,805 Mt in 2024, with 2025 forecast at 8,845 Mt — another record. Demand is expected to plateau above 8,680 Mt through 2030, not collapse. Metallurgical coal consumption remains stable at approximately 1,114 Mt.

Alfabs services 26 underground mines and 9 underground plus surface mines across New South Wales and Queensland. The “coal is dying” narrative does not align with IEA data — demand is plateauing at record highs, supporting sustained equipment hire volumes through the decade.

The next major ASX story will hit our subscribers first

Acquisition discussions continue but terms not yet agreed

The Company provided an update on the potential acquisition first announced on 23 February 2026. Discussions remain ongoing but commercial terms have not yet been agreed. Management stated it will proceed only if final terms align with return thresholds and value creation objectives. The process is taking longer than initially anticipated.

This demonstrates capital discipline in practice — walking away from deals that do not meet hurdle rates protects shareholder value.

The presentation’s stated key message was that maximum shareholder value will be created through reinvestment in the business.

Get Mining & Industrial News Before the Market Moves

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to stay ahead on Mining, Engineering, and Industrial sector announcements the moment they break.