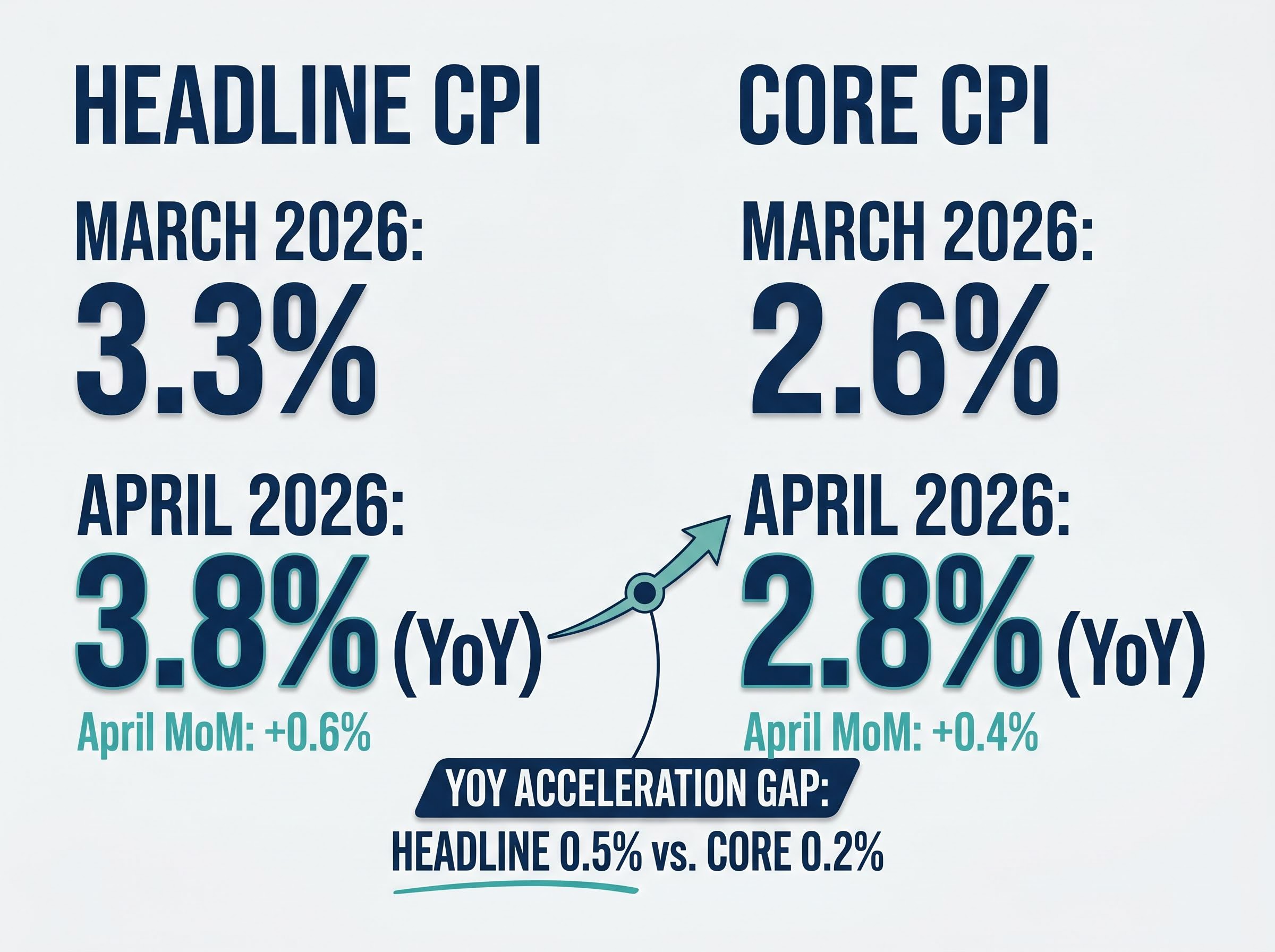

April’s 3.8% headline inflation print landed on 12 May 2026 like a verdict: the highest reading in over a year, enough to convince markets that the remaining 2026 rate cuts were dead on arrival. But headline numbers can deceive, and the composition of this one matters more than the total. The Bureau of Labor Statistics report showed core inflation (which strips out food and energy) rising to 2.8% from 2.6% in March, a comparatively modest move. Energy prices drove the bulk of the headline acceleration, from 3.3% to 3.8% year-over-year. The Federal Open Market Committee (FOMC) had already flagged rising global energy prices in its 29 April statement, signalling that policymakers were watching this dynamic closely before the data arrived. What follows is a decomposition of what actually moved in the April report, why the inflationary surge may prove more temporary than consensus fears suggest, and what the inflation trajectory means for equity investors positioning through the second half of 2026.

What the April CPI report actually showed, beneath the headline

The initial reaction was understandable. A 3.8% headline print, up from 3.3% a month earlier, with a +0.6% month-over-month increase, looks like inflation re-accelerating. Growth-sensitive equities sold off. Rate-cut expectations collapsed.

Then the detail beneath the headline told a different story.

Core CPI, which excludes the volatile food and energy categories, rose to 2.8% year-over-year from 2.6%, with a month-over-month increase of +0.4%. That is firmer than the Fed would like, but it is not the kind of broad-based acceleration that rewrites the monetary policy outlook.

The Bureau of Labor Statistics April CPI release confirmed the energy index rose 17.9% year-over-year and 3.8% month-over-month, making energy by far the largest single contributor to the headline acceleration and reinforcing the case that core inflation, not the headline figure, is the more reliable guide to underlying price pressure.

| Measure | March 2026 | April 2026 |

|---|---|---|

| Headline CPI (YoY) | 3.3% | 3.8% |

| Core CPI (YoY) | 2.6% | 2.8% |

| Headline CPI (MoM) | — | +0.6% |

| Core CPI (MoM) | — | +0.4% |

Energy accounted for the bulk of April’s headline acceleration. Core inflation, which excludes food and energy, moved only 20 basis points year-over-year, from 2.6% to 2.8%.

Investors who repositioned based on the headline alone may be making a different bet than they intend. The distinction between a broad-based inflation problem and an energy-driven spike carries materially different implications for rate policy, sector exposure, and portfolio duration.

When big ASX news breaks, our subscribers know first

Why energy-driven inflation spikes tend to behave differently from structural price pressure

Energy price surges and broad-based structural inflation produce the same headline number but follow different trajectories. For investors deciding whether April’s CPI warrants a portfolio repositioning, the distinction is where the answer starts.

Energy-driven spikes share three characteristics that typically differentiate them from structural inflation:

- Speed of onset: Energy shocks tend to hit CPI rapidly, within one to two monthly prints, rather than building gradually across categories over several quarters.

- Sensitivity to geopolitical resolution: Because the price pressure originates from supply disruption or conflict premium, even partial resolution or demand adjustment can reverse the effect faster than structural wage-price dynamics.

- Base-effect reversal: A sharp energy spike in one month creates a tougher year-over-year comparison in the same month the following year, meaning headline inflation can fall mechanically even without further price declines.

The 2022-2024 energy price shock episodes illustrate this pattern. Conflict-driven surges transmitted rapidly into headline CPI, prompted aggressive monetary tightening expectations, and then faded as supply conditions normalised, often faster than consensus had projected at the peak of the alarm.

Core inflation at 2.8% is the figure that strips out this volatile component and offers a cleaner read on underlying price pressure.

Oil price transmission into core CPI is not instantaneous; analyst pass-through estimates place 40-60% of a crude price increase into core categories over a 3-6 month lag, meaning the June and July CPI prints will carry more policy weight than the April figure in determining whether the current energy shock stays confined to headline inflation or begins broadening into services and goods.

The Fed’s own framing of the energy variable

The FOMC’s 29 April 2026 statement explicitly referenced “recent increases in global energy prices” as an inflation input. That language is significant. By isolating energy as a distinct variable, rather than characterising inflation broadly as re-accelerating, the Fed signalled that its policy calculus already distinguishes between the headline number and the underlying trend. This framing suggests rate decisions will weigh the durability of the energy shock, not simply react to the top-line print.

For investors wanting to understand the full context behind the Fed’s current posture, our full breakdown of the 29 April FOMC decision examines the four-way dissent in detail, including how the Strait of Hormuz closure shaped the committee’s language and why three hawks outnumbered the lone dovish dissenter in a split that has direct implications for how policymakers will respond to the April CPI data.

The money supply argument for a more favourable inflation path

Not every analyst interpreted the April report as the start of a sustained inflation problem. Fisher Investments offered a contrarian reading, arguing that the inflation outlook is “likely more favourable than current market consensus.”

The reasoning rests on a monetary framework. Sustained inflation, in this view, requires sustained monetary fuel: money supply growth that outpaces the economy’s capacity to absorb it. Without that fuel, price surges driven by external supply shocks tend to be self-limiting.

Fisher Investments cited two specific factors:

- Money supply restraint: Restrained monetary expansion reduces the probability that an energy-driven price spike translates into persistent, broad-based inflation.

- Historical transience of regional conflict energy effects: Past episodes of conflict-driven energy surges have typically faded as supply conditions adjusted, rather than embedding permanently into the price level.

Fisher Investments characterised the inflation outlook as “likely more favourable than current market consensus,” arguing that restrained monetary conditions reduce the probability of a sustained, larger inflation surge.

A data limitation is worth noting honestly. Verified M2 money supply series for 2025-2026 are not yet widely available in published form. The directional argument rests on the monetary framework and on Fisher Investments’ stated view as of 12 May 2026, not on a specific published M2 figure. China’s M2 grew 8.6% year-over-year in April 2026 (per FactSet), beating consensus, a counter-data point that complicates any global monetary restraint narrative.

This is one analytical perspective, not established fact. But the framework it applies, distinguishing between inflation with monetary fuel and inflation without it, is a useful lens for investors evaluating whether consensus fears are correctly calibrated.

What the rate-cut repricing means for equity markets right now

The April CPI print prompted markets to abandon remaining 2026 rate-cut expectations. For equity investors, this is where the inflation debate stops being abstract and becomes a portfolio decision.

Higher-for-longer rates raise the discount rate applied to future earnings. Growth-sensitive sectors, where valuations depend most heavily on earnings projected years into the future, face the sharpest compression. This was visible in the market reaction following the 12 May release, with growth equities coming under documented pressure as rate-cut timelines were repriced.

The equity market reaction to the April print was itself informative: the S&P 500 closed near 7,425 on 12 May without a significant sell-off, suggesting markets had already absorbed much of the inflationary deterioration in the weeks before the BLS release, and that the money supply argument against sustained inflation had already filtered into institutional positioning.

Why the consumer and industrial data complicate the inflation story

The inflation picture does not exist in isolation. April 2026 retail sales rose +0.5% month-over-month and +4.9% year-over-year, per FactSet. Industrial production increased +0.7% month-over-month and +1.4% year-over-year. These figures describe an economy that is not weakening under the inflation pressure, which complicates the Fed’s calculus: cutting rates into strong demand risks reinforcing inflation, but holding rates higher for longer risks overcorrecting if the energy surge fades.

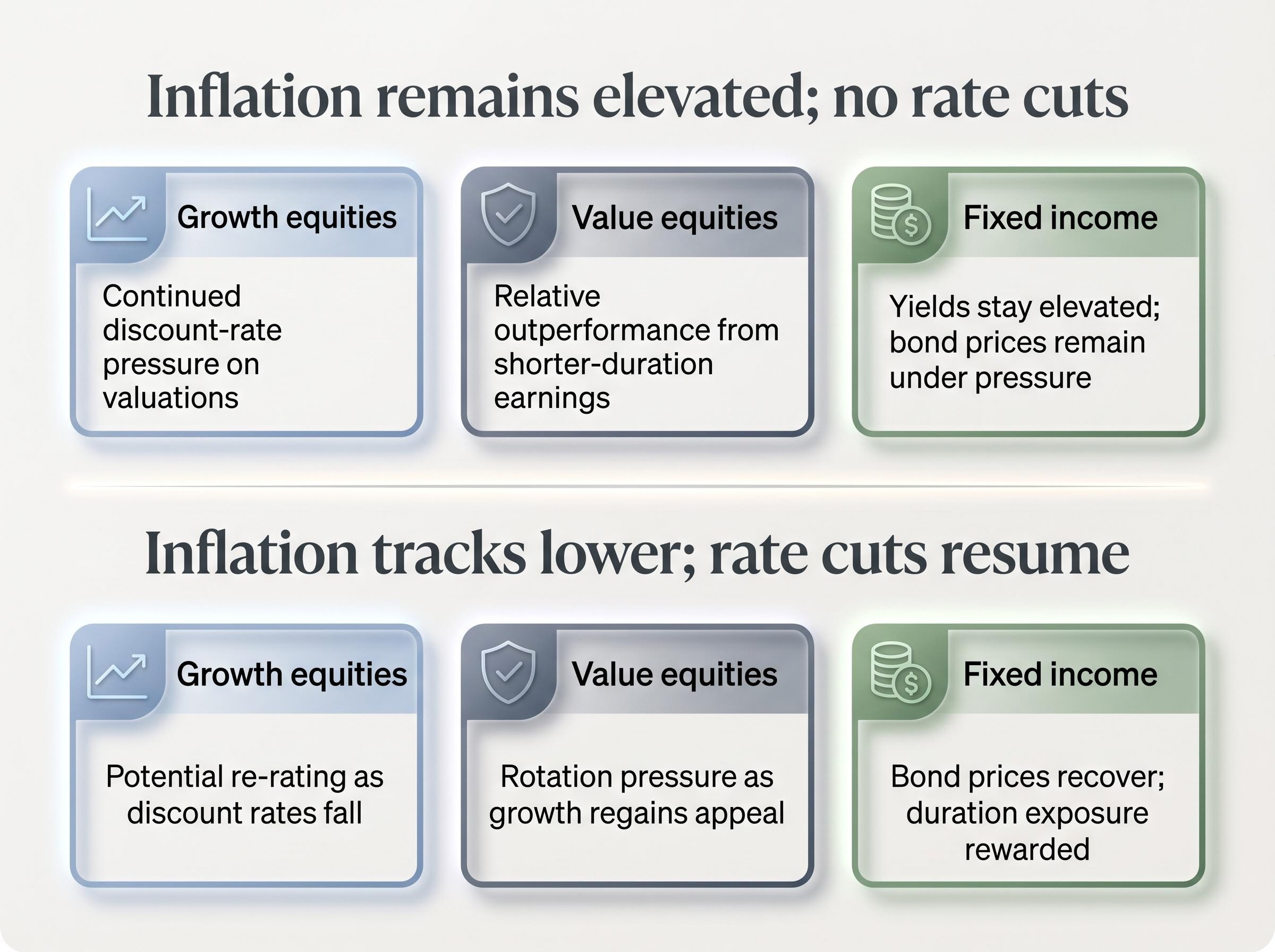

For equity investors, two scenarios carry distinct implications:

| Scenario | Growth equities | Value equities | Fixed income |

|---|---|---|---|

| Inflation remains elevated; no rate cuts | Continued discount-rate pressure on valuations | Relative outperformance from shorter-duration earnings | Yields stay elevated; bond prices remain under pressure |

| Inflation tracks lower; rate cuts resume | Potential re-rating as discount rates fall | Rotation pressure as growth regains appeal | Bond prices recover; duration exposure rewarded |

The rate-cut repricing is where the inflation call becomes a direct portfolio allocation decision. Knowing which scenario the data supports, and watching the signals that confirm or disconfirm each path, is more productive than reacting to each monthly print in isolation.

What a positive inflation surprise would actually look like for investors

If inflation does track more favourably than consensus currently expects, what would the confirming data look like? Fisher Investments characterised the outlook as “a potential upside surprise for investors,” and the conditions that would validate that view are specific enough to monitor.

A positive inflation surprise would mean:

- Energy price stabilisation or decline: If energy prices level off or retreat, headline CPI will begin converging toward core, reducing the gap that drove April’s alarm. The base-effect dynamic means that energy prices which spiked in April will face tougher year-over-year comparisons in subsequent months even if they merely hold steady.

- May core CPI contained near or below 2.8%: A core reading that holds steady or declines would confirm that the underlying inflation trend is not broadening beyond the energy component.

- Preliminary PMI readings for May 2026: Scheduled for the week of 18 May 2026, these will provide the next real-time signal on both activity levels and pricing pressure across manufacturing and services.

Fisher Investments described the inflation trajectory as “a potential upside surprise for investors,” suggesting the current consensus may be pricing in more persistent inflation than monetary and supply conditions warrant.

This is not a prediction. It is a monitoring framework. Investors who understand the specific conditions that would confirm a cooling trajectory can make more deliberate decisions, rather than reacting to each data release as if it were a standalone verdict.

The inflation call is a portfolio call, and the data is more nuanced than the market reaction suggests

April’s headline print was driven by energy. Core inflation moved modestly. The monetary backdrop, at least as Fisher Investments reads it, argues against sustained acceleration. And the consumer and industrial economy remains resilient enough to complicate any simple narrative.

Three takeaways for investors:

- The energy driver is identifiable and historically transient. Headline CPI and core CPI are telling different stories, and the distinction matters for rate policy.

- Core at 2.8% is firmer than the Fed would prefer, but not a structural breakout. The breadth of price pressure, not just the level, will determine whether policy tightens further.

- The confirming signals are specific and imminent. May PMI data, energy price trends, and the next core CPI print will either validate or undermine the more favourable thesis.

The Fisher Investments perspective is one analytical view, not a forecast guarantee. The energy and geopolitical uncertainties are real. But investors who treat the inflation data as a nuanced signal, decomposing the components rather than reacting to the headline, are better positioned to hold through volatility or act when confirming data arrives.

Investors ready to act on either scenario outlined above will find our dedicated guide to tactical inflation allocation in 2026 useful; it covers specific asset tilts toward Treasury Inflation-Protected Securities, REITs, and quality equities with pricing power, alongside the case for a cash buffer to exploit dislocations if the energy shock persists longer than the base case.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.