Why U.S.-Iran Conflict Is Sending Oil Up and Gold Down

4 mins ago

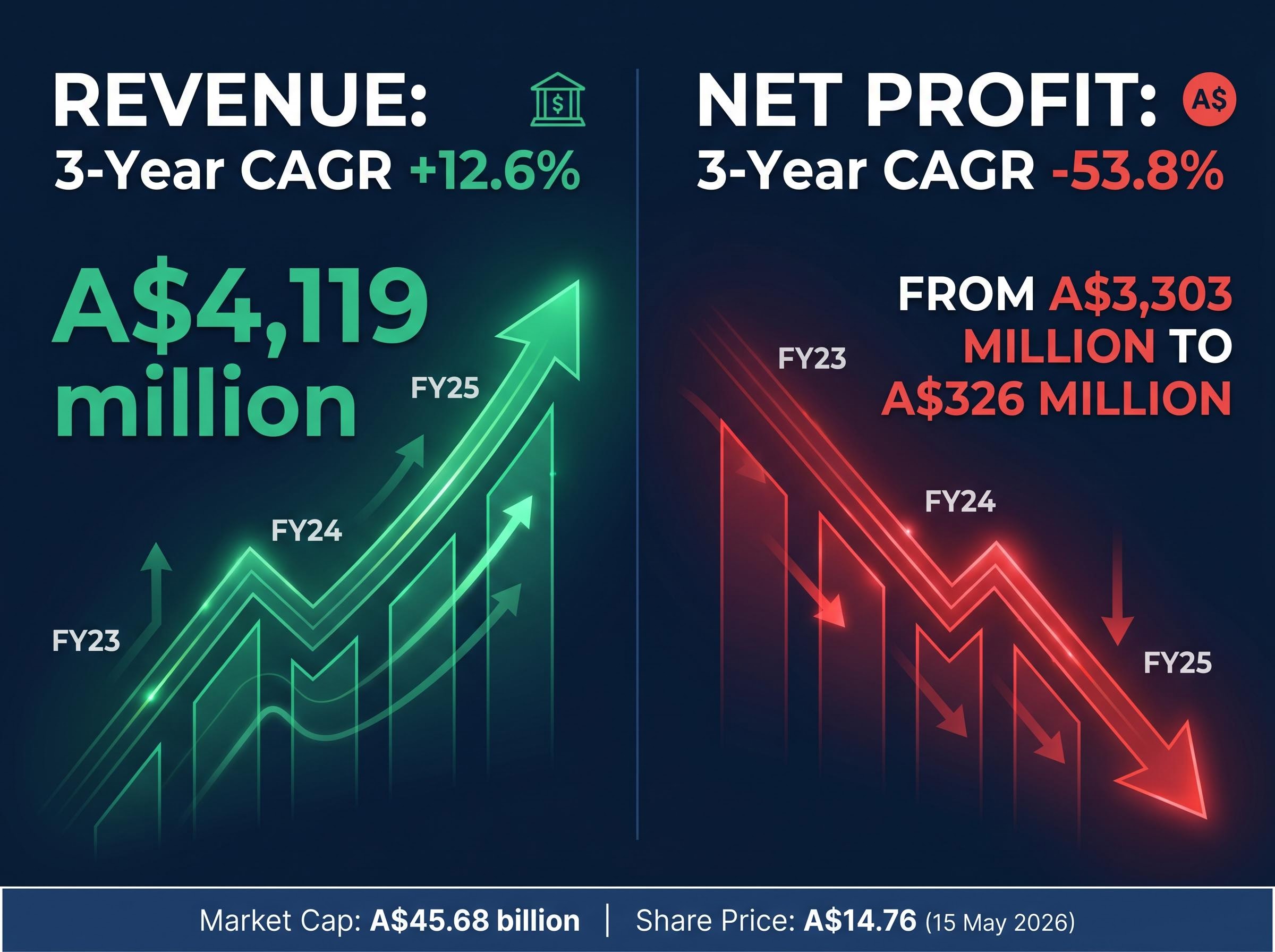

Transurban has grown revenue at a compound annual rate of 12.6% for three consecutive years. Over the same period, its net profit has fallen at a compound annual rate of 53.8%. Both statements are true, and together they define the central puzzle facing anyone researching the Transurban share price today. With the stock trading at approximately A$14.76 (close, 15 May 2026) and a market capitalisation of around A$45.68 billion, Transurban is one of the largest infrastructure names on the ASX. Its surface metrics look like a growth story. Its earnings metrics tell a different story entirely. This analysis unpacks what is actually driving the profit collapse, what the company’s debt load and low return on equity mean in practice for shareholders, how the higher-rate environment is reshaping the investment case for toll road operators broadly, and what questions investors should be asking before forming a position.

The numbers, placed side by side, do the work themselves.

Transurban’s most recently reported annual revenue came in at A$4,119 million, the latest print in a three-year run of 12.6% compound annual growth. Over the same three-year window, net profit fell from A$3,303 million to A$326 million, a compound annual decline of approximately 53.8%.

A$326 million in net profit on A$4,119 million in revenue, after three years of double-digit top-line growth. The earnings CAGR over that period: approximately -53.8%.

That gap is not a rounding error. It is the single most important framing question for anyone evaluating this stock at A$14.76 and a market capitalisation of A$45.68 billion.

| Metric | Three-year CAGR |

|---|---|

| Revenue | +12.6% |

| Net profit | -53.8% |

Revenue growth has not translated into earnings growth. The sections that follow explain why, and whether the divergence is temporary, structural, or some combination of both.

Management’s own commentary, across the FY24 results release (8 August 2024) and the 1H25 half-year report (6 February 2025), identifies four primary drivers. They range from accounting noise to structural cost pressures, and the distinction between the two categories matters more than the headline number.

The first two drivers are volatile and, in management’s framing, largely non-recurring:

These are real accounting entries, but they are not repeatable revenue streams. Their absence deflates reported profit without signalling operational deterioration.

The remaining two drivers are harder to dismiss:

Management has been explicit that the profit decline is not attributed to collapsing traffic or toll revenue. Free cash flow per security increased in FY24, and distributions are set by cash flow, not statutory profit. That framing is accurate on its own terms, but it does not make the earnings decline irrelevant. Equity valuations ultimately track earnings power, not just distribution capacity.

Toll road operators are not conventional equities, and reading their financials as though they were leads to consistent misinterpretation.

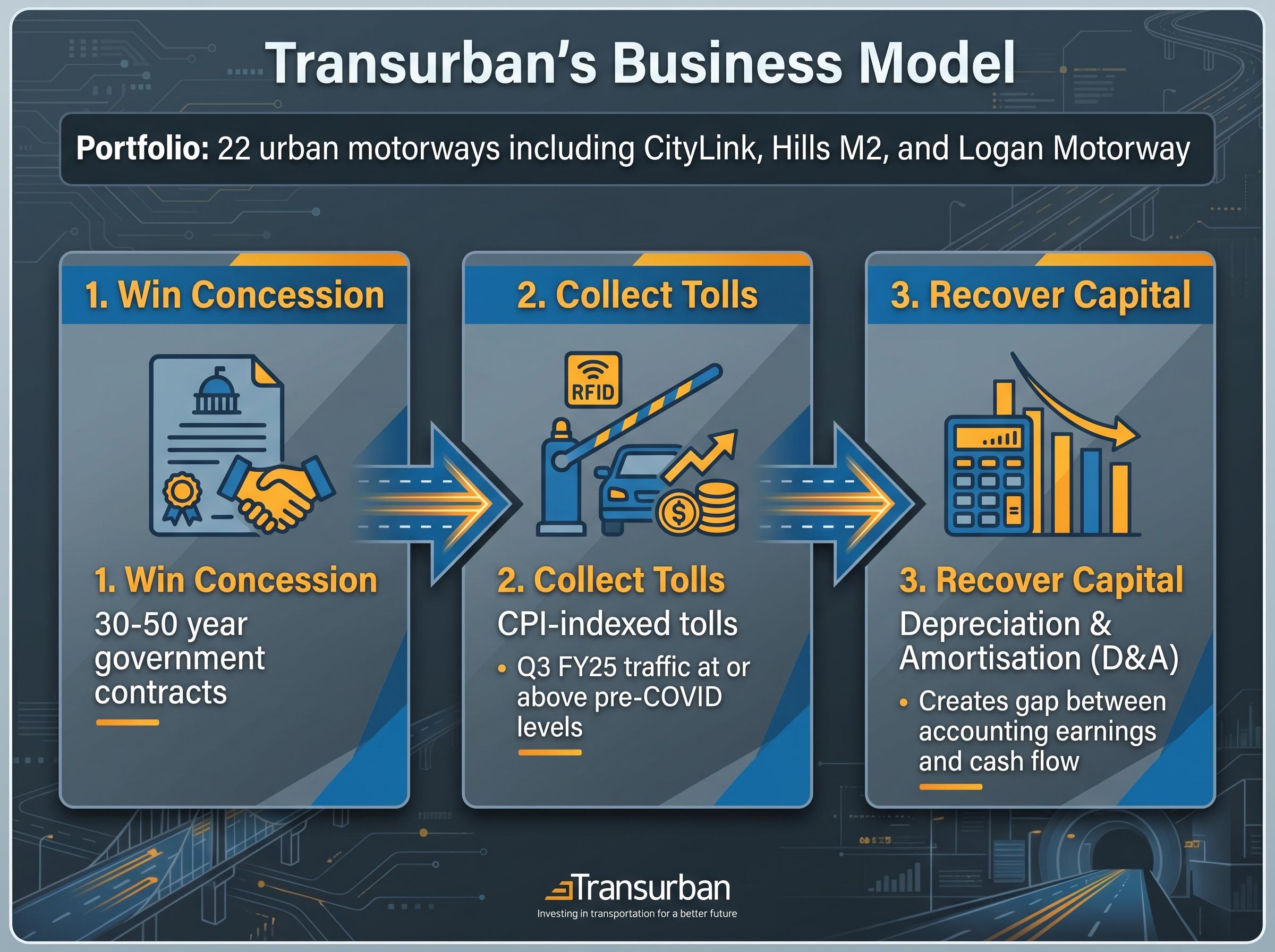

Transurban operates 22 urban motorways across Australia, Canada, and the United States. The Australian corridors, including CityLink in Melbourne, Hills M2 in Sydney, and Logan Motorway in Brisbane, form the core of the portfolio. The business model follows a three-step logic:

This structure means statutory net profit will almost always understate the cash the business produces. Fair-value movements on financial instruments and concession revaluations add further volatility to reported earnings that has no cash equivalent.

The Grattan Institute’s October 2025 report, “Paying for Roads in a High-Rate World,” noted that private toll road concessions designed in a low-rate environment can still be viable, but equity returns are squeezed as financing costs normalise. The implication: equity holders, not taxpayers, will bear more of the pain.

CPI linkage provides a partial inflation hedge. It does not, however, protect against rising interest costs when debt levels are as high as Transurban’s.

The explanatory framework above accounts for why reported profit looks weak. This section asks a different question: is shareholder capital working hard enough to justify the current share price?

| Metric | Value | Risk implication |

|---|---|---|

| Net debt | A$18,018 million | Material refinancing exposure as legacy low-rate debt matures through FY28 |

| Debt-to-equity | 175.1% | Amplifies sensitivity to rate movements and credit spread widening |

| Return on equity (FY24) | 3.0% | Below cost of equity; implies accounting value destruction, not creation |

A 3.0% ROE against a cost of equity estimated in the high teens (a comparison drawn in Australian Financial Review commentary on Transurban’s capital efficiency) implies the business is currently destroying rather than creating economic value in accounting terms.

Management’s counterargument is that distributions are cash-flow-supported and that statutory ROE understates the real return profile of long-dated infrastructure assets. There is merit to this view. But the tension between a healthy distribution yield and a sub-5% accounting return on equity is one that broker coverage has consistently flagged. Morgan Stanley retained an underweight stance on TCL, citing elevated net debt and rate sensitivity. UBS noted the stock trades at an EV/EBITDA premium to global peers despite the sub-5% post-tax ROE. Morningstar characterised TCL as “roughly fairly valued” for a long-duration bond substitute.

At A$14.76, investors need to judge whether the distribution yield compensates adequately for the balance-sheet risk the numbers describe.

Credit rating mechanics for leveraged infrastructure operators, illustrated by APA Group’s April 2026 Moody’s affirmation, show that investment-grade ratings are preserved through FFO/debt thresholds rather than absolute debt levels, a framework that contextualises why Transurban’s A$18 billion net debt position is not automatically a credit concern if cash flow coverage ratios remain within agency parameters.

Listed infrastructure stocks like TCL function as bond proxies. Their long-dated, inflation-linked cash flows attract capital seeking yield and duration, which means their share prices move inversely with long-term bond yields. When yields rise, the present value of those distant cash flows falls, and the multiple investors are willing to pay compresses.

The same rate transmission channels that compress REIT valuations apply with equal force to listed toll road operators: rising discount rates reduce the present value of distant cash flows, higher debt service costs eat into distributable income, and yield competition from government bonds narrows the premium investors demand for holding equity risk.

This mechanism is the single largest unresolved variable in the Transurban investment case. Three distinct but related risks sit within it:

The WestConnex debt structure offers a concrete illustration of how Transurban manages refinancing risk at the asset level: the April 2026 dual-tranche bond issuance staggered A$660 million of maturities to 2032 and A$550 million to 2036, ring-fenced from the TCL group balance sheet and sized to avoid a single concentrated refinancing event.

The RBA Financial Stability Review (April 2025) identified elevated leverage as a key vulnerability for corporate entities exposed to prolonged higher interest rates, noting that stress has picked up in pockets of the corporate sector where profits are under pressure, a dynamic that maps directly onto Transurban’s widening gap between cash generation and statutory earnings.

The NSW weekly toll cap is a government-funded rebate to motorists, not a direct reduction in Transurban’s contracted tolls. The IPART review has been completed and signals a potential shift toward distance-based tolling, but as at May 2026, no ASX disclosure has announced a formal concession restructuring. The risk is prospective, not current; investors should monitor it without pricing in a change that has not been formally proposed.

The NSW Independent Toll Review final report recommended that tolls shift to a declining distance-per-kilometre basis with IPART oversight of future toll setting, a structural change to the pricing framework that, if legislated, would represent a material departure from the CPI-indexed concession model Transurban’s current asset valuations assume.

Infrastructure Partnerships Australia’s May 2025 market update captured the sector tension precisely: listed infrastructure operators benefit from CPI-linked pricing but face margin pressure when interest and construction costs escalate faster than traffic or toll revenue growth.

The preceding analysis leaves the investment case in genuine tension. Transurban owns high-quality assets with inflation-linked revenue that is growing. It also carries A$18 billion in net debt, a 3.0% ROE, and a share price that broker coverage describes as ranging from roughly fair (Morningstar) to “expensive defensive” (Goldman Sachs, as characterised in media coverage).

Before forming a position at A$14.76 and a market capitalisation of A$45.68 billion, the following questions deserve specific answers:

Atlas Arteria’s results from FY25 provide a direct comparison point: the ASX-listed toll road operator posted 9.4% proportional revenue growth and maintained 75% EBITDA margins while statutory profit was compressed by French tax headwinds, a pattern structurally similar to the divergence between Transurban’s top-line growth and its reported earnings.

The investment case for Transurban sits in a genuine tension between strong asset quality and CPI-linked revenue on one side, and a sharply deteriorating profit trajectory with material balance-sheet risk on the other. Morningstar’s “roughly fairly valued” assessment and Goldman Sachs’s “expensive defensive” characterisation leave investors in uncertain territory rather than facing a clear signal.

TCL may be appropriate for investors with a specific, considered view on the rate cycle. It is less suitable as a default allocation made on the comfort of infrastructure’s defensive reputation alone. The revenue-versus-profit divergence will resolve, either through lower rates easing finance costs, or through a sustained re-rating that acknowledges the structural pressures. Investors should verify the current distribution yield directly from Transurban’s investor centre before drawing income conclusions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Transurban's profit decline is driven by a combination of non-recurring items (such as fair-value revaluation gains that inflated prior-year figures) and structural pressures including rising interest costs on A$18 billion in net debt and higher depreciation charges as new assets enter service. Revenue has grown at a 12.6% compound annual rate, but these cost pressures have driven net profit down at a 53.8% compound annual rate over the same three-year period.

A 3.0% return on equity, compared to a cost of equity estimated in the high teens, implies that the business is currently destroying rather than creating economic value in accounting terms. While management argues that cash flow generation better reflects the real return profile of long-dated infrastructure assets, the gap between accounting ROE and cost of equity is a concern flagged consistently by broker coverage including Morgan Stanley and UBS.

Transurban functions as a bond proxy, meaning its share price moves inversely with long-term bond yields. Rising rates reduce the present value of its long-dated cash flows, compress price-to-cash-flow multiples, and increase refinancing costs on its A$18,018 million net debt, all of which put downward pressure on the stock's valuation.

NSW policy scrutiny includes an IPART tolling review and a state government weekly toll cap scheme. The independent toll review recommended shifting to a declining distance-per-kilometre basis with IPART oversight, which would represent a material departure from the CPI-indexed concession model underpinning Transurban's current asset valuations, though as of May 2026 no formal concession restructuring has been announced.

Toll road concession operators like Transurban structurally generate more cash than their statutory profit suggests, because large non-cash charges including depreciation and amortisation of concession assets widen the gap between accounting earnings and actual cash generation. Distributions are set by cash flow rather than statutory profit, but equity valuations ultimately track long-term earnings power, so both measures need to be understood rather than one dismissed.