What the Broadcom Drop Reveals About AI Stock Valuations Now

2 hrs ago

By the close of trading on 25 June 2026, Singapore equities had reached record territory, completing a fourth straight quarter of gains and delivering an 11.3% return across the first half of the year. For a market often characterised as steady rather than spectacular, that performance is a signal worth understanding.

The rally is not a single-factor story. It reflects an unusual convergence: geopolitical shock absorption channelling safe-haven capital into Singapore, a banking sector firing on multiple cylinders simultaneously, an emerging semiconductor cycle tied to artificial intelligence (AI) infrastructure buildout, and a contrarian macro call on US interest rates that, if correct, extends the entire thesis well into the second half of 2026.

Here is what each layer of this rally actually rests on, which sectors are positioned to keep benefiting, and where the structural headwinds run deep enough that patience, rather than positioning, is the honest advice. The single macro variable most likely to determine whether this first-half performance extends or reverses sits at the end.

The ceasefire eased risk premiums on transportation-linked names across shipping, aviation, and logistics, lifting operational sentiment and valuations. But the larger effect was what happened to capital flows. When regional risk rises, Singapore’s political stability, rule of law, and financial infrastructure make it a natural parking destination for institutional and private wealth. That mechanism activated at scale.

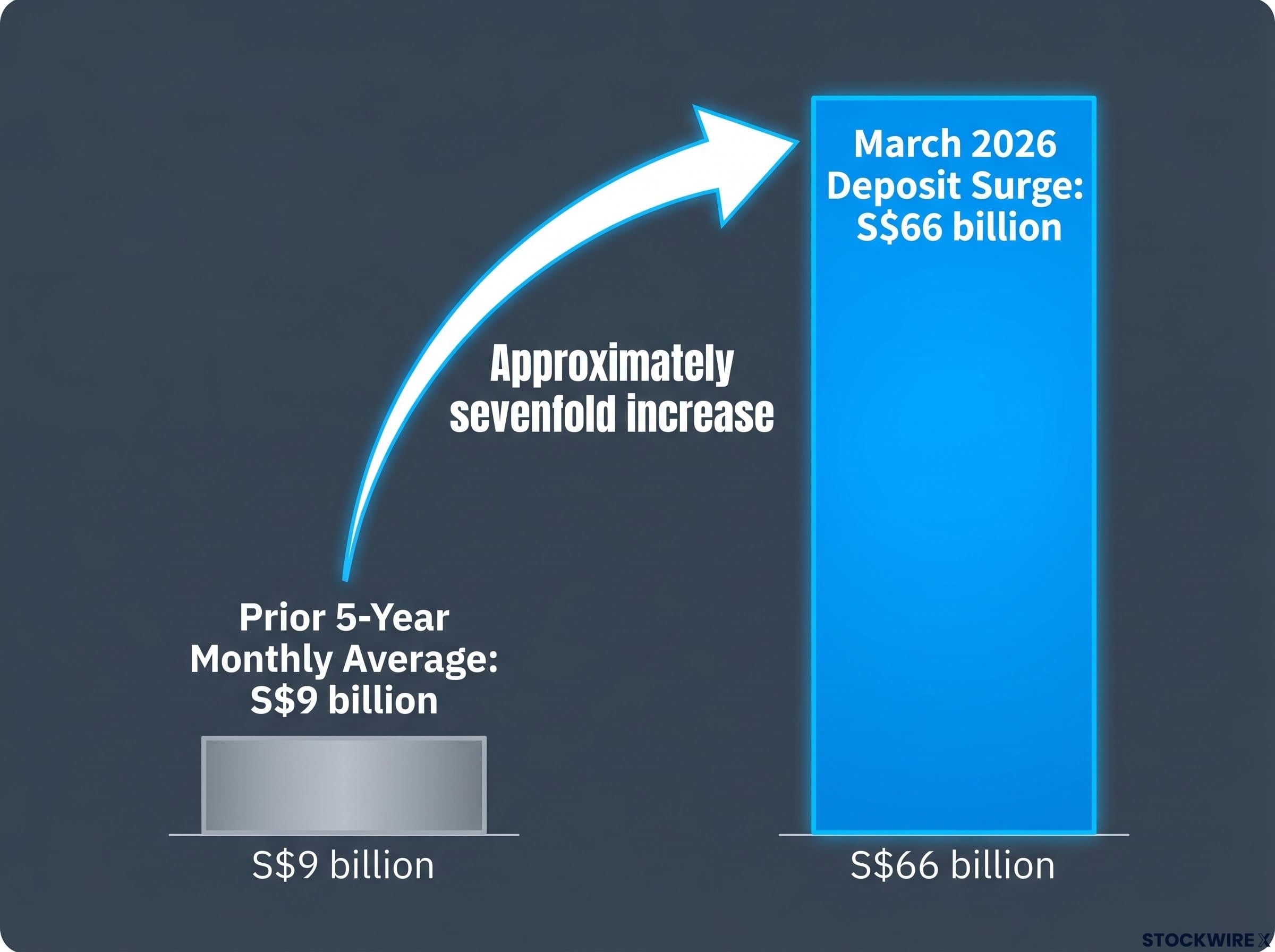

In March 2026, Singapore banks received a deposit surge of S$66 billion, a figure that dwarfs the prior five-year monthly average of roughly S$9 billion and represents an approximately sevenfold increase.

That is not a qualitative assertion about safe-haven status. It is a measurable capital commitment. Institutional and private capital treated Singapore as a regional crisis backstop, and the rally’s foundation includes genuine capital inflow rather than a sentiment re-rating alone.

The deposit surge itself is inseparable from the broader context of geopolitical pressure on Fed rate policy, which has suppressed global risk appetite and repeatedly redirected institutional capital toward perceived safe harbours, with Singapore capturing a disproportionate share of that rotation.

The deposit surge matters beyond the headline figure because capital parked in Singapore banks does not sit idle. It suppresses funding costs, expands loan capacity, and lifts fee income, which is exactly why banks have become the primary engine of this rally.

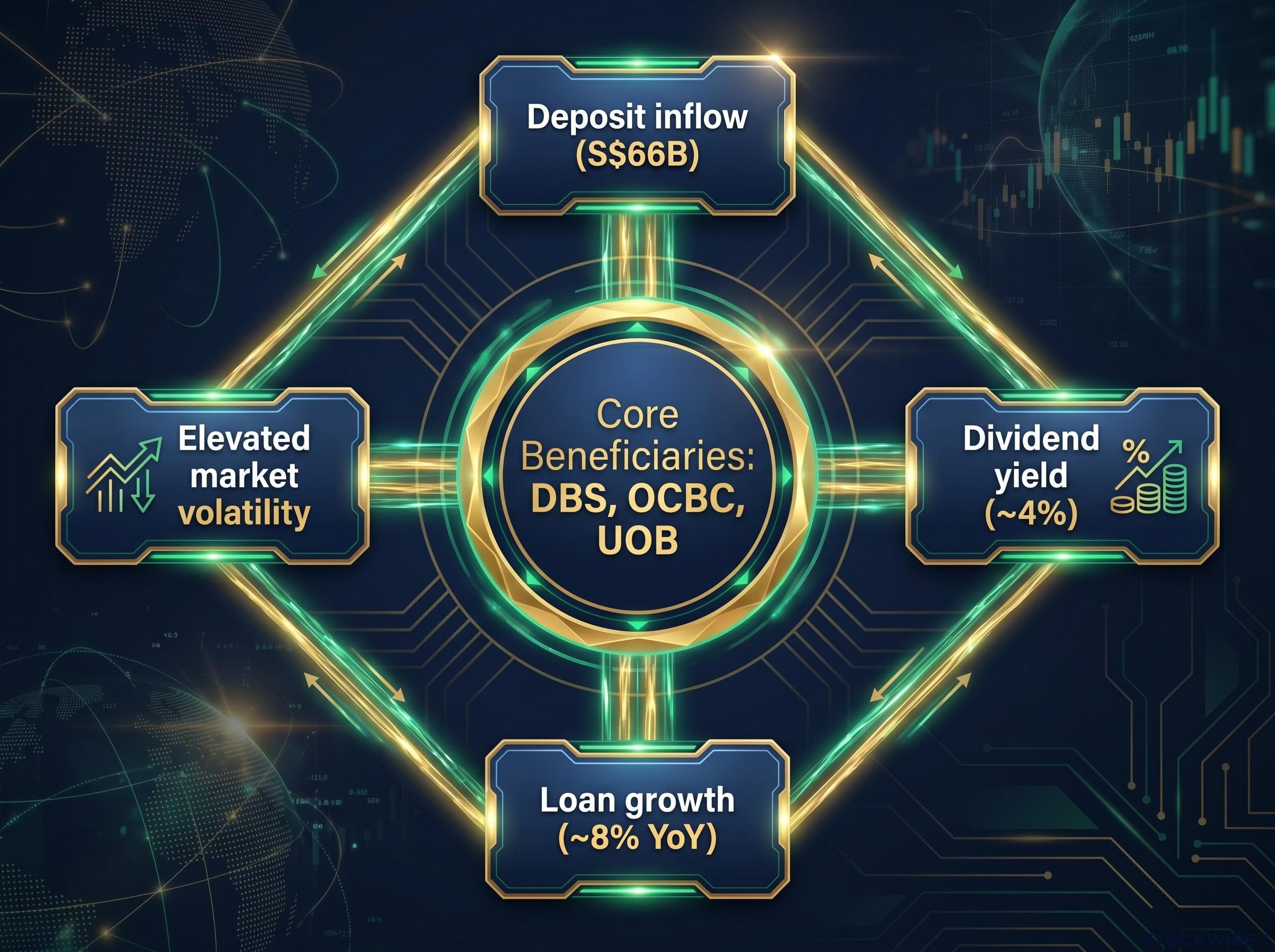

The banking sector is not riding a single tailwind. Four drivers are compounding simultaneously, and the reinforcement effect between them is what makes banks the structural anchor of the entire rally.

| Driver | Mechanism | Impact on banks | Status |

|---|---|---|---|

| Deposit inflow (S$66B) | Lower funding costs | Net interest margin expansion | Active |

| Loan growth (~8% YoY) | Credit volume at four-year high | Fee and interest income growth | Active |

| Elevated market volatility | Trading and treasury activity | Fee income uplift | Active |

| Dividend yield (~4%) | Investor anchoring | Valuation support | Active |

Each driver reinforces the others rather than substituting. The deposit surge lowers funding costs at the same time loan volumes are expanding, which lifts margins and credit income simultaneously. Volatility adds a fee-income layer that sits on top of the lending business. And the approximately 4% dividend yield keeps income investors anchored to bank stocks rather than rotating out, which supports valuations independently of the earnings momentum.

The three core beneficiaries:

When loan growth, margin expansion, fee income, and dividend yield all move in the same direction simultaneously, that combination rarely persists indefinitely. Understanding whether the rate environment preserves or interrupts it is what makes the second half of 2026 the key question, and that question gets its own section below.

Singapore is not a chip-making economy in the way Taiwan or South Korea are. Its listed semiconductor exposure sits in equipment, precision engineering, and specialist components rather than chip foundries. That distinction changes how the exposure behaves, and it is the reason most investors underestimate the growth component of Singapore equities.

Major equipment makers such as ASML, Applied Materials, and Lam Research are among the principal customers for Singapore-based component and precision engineering suppliers, and all three are operating with full order books and ongoing capacity build-outs. When those manufacturers invest in new fabrication capacity, their capital expenditure flows through to the equipment and component suppliers that build, calibrate, and maintain the production lines. Singapore captures that upstream demand.

The structural demand drivers sustaining those order books are not single-quarter phenomena:

IDC semiconductor market forecasts project the global market surpassing one trillion dollars in 2026, with data centre semiconductor revenues alone reaching $477 billion, a scale of capital expenditure that flows directly into the order books of the equipment and precision engineering suppliers where Singapore’s listed exposure is concentrated.

According to Phillip Securities Research, semiconductor stocks are forecast to deliver the strongest growth of any segment within the current Singapore rally.

Because Singapore’s exposure sits in equipment and precision engineering rather than chip fabrication itself, it benefits from capital expenditure cycles at the large manufacturers without carrying the inventory-cycle volatility that affects foundries directly. That is a structurally different and more durable growth profile. For investors looking for the upside torque in Singapore equity exposure rather than just income, this is where it sits.

Singapore’s upstream position in the chip supply chain means it captures the capital expenditure phase of the cycle with lower direct exposure to the inventory correction risk that dominates semiconductor cycle investing analysis, particularly the DRAM and NAND oversupply scenarios projected for 2028-2029.

Equity rallies built purely on financial conditions can unravel quickly. This one has a physical-economy anchor. Ready-mixed concrete demand is up approximately 29%, according to Phillip Securities Research, reflecting accelerating construction activity across public housing, infrastructure programmes, and commercial development. That pipeline does not reverse quickly.

The concrete figure tells you the rally has a foundation that equity multiples alone do not capture. Real construction is happening, and the companies supplying it are seeing that demand in their order books.

On the yield side, the story is more selective. Not all Singapore REITs (real estate investment trusts, which are listed funds that own and operate income-producing property) are positioned equally. The quality criteria that matter right now:

Phillip Securities Research exited its Prime US REIT position in the Absolute 10 model portfolio, substituting ST Engineering in its place. The move signals a deliberate shift away from US dollar rate-sensitive income exposure and toward a name offering structural defence and export-driven growth.

That swap is a concrete illustration of the selectivity required. Even within Singapore equities, where income is denominated and how it is refinanced matters enormously in the current rate environment. A REIT yielding 6% in US dollars with near-term refinancing risk is a fundamentally different proposition from one yielding 5% in Singapore dollars with a clean balance sheet.

The selectivity required within Singapore REITs extends well beyond balance sheet strength into S-REIT sub-sector positioning, where industrial and logistics assets carry structurally different tailwinds from office and non-prime retail, and where data centre REITs face domestic power constraints that are pushing incremental growth offshore.

Everything described above, bank margins, REIT valuations, the broad market re-rating, is sensitive to one variable: the path of US interest rates in the second half of 2026.

Phillip Securities Research holds a view that sits outside the mainstream: the firm anticipates the US Federal Reserve will leave rates unchanged throughout 2026, arguing that price pressures have crested and that the economic and political conditions for additional tightening are no longer present.

Most market participants are not aligned with that view. Consensus pricing currently points to a single Fed rate increase at some point in 2026, with September 2026 seen as the most probable meeting for that move.

Phillip Securities Research is not alone in watching Fed communication on rates closely: Warsh’s inaugural press conference in June 2026 established a deliberate departure from calendar-style forward guidance, meaning investors relying on conventional rate-path signals to position for September are working from an outdated model of how the current Fed chair communicates policy intent.

| Scenario | Rate path | Implication for Singapore equities |

|---|---|---|

| Phillip Securities view | No hikes in 2026 | Rally extension for banks and REITs; key global risk overhang removed; broader equity valuations supported |

| Market consensus | One hike, ~September 2026 | Second-half valuation test for rate-sensitive segments, particularly banks and REITs |

The no-hike path keeps funding conditions benign, removes a global risk overhang, and supports the conditions that have driven the first half’s performance. The consensus hike path introduces a valuation test for exactly the segments, banks and REITs, that have led this rally.

Whether you hold Singapore bank or REIT exposure or are considering adding it, this rate fork is the single macro variable most likely to determine whether the first half’s performance extends or reverses. A reader positioning now is implicitly taking a view on September’s Fed decision, whether they intend to or not.

These statements regarding future rate paths are speculative and subject to change based on market developments and central bank decisions.

Not every sector in Singapore is participating in this rally, and two sectors’ problems run deeper than timing.

Classifying a sector’s problems as structural rather than cyclical has a direct investment implication: a recovery timeline is measured in years, not quarters, and a patient-contrarian thesis requires much stronger positive catalysts than are currently visible in either sector. Knowing where not to add exposure is as valuable as knowing where to add it.

The first half of 2026 delivered an 11.3% return, four consecutive quarterly gains (including 5.8% in Q2 2026), and all-time highs recorded on 25 June 2026. The convergence of drivers behind that performance, geopolitical safe-haven flows, bank fundamentals, the semiconductor cycle, and real-economy construction demand, gives this rally more structural credibility than a single-catalyst move.

The sector hierarchy as it stands:

The second half hinges on the rate fork. The September 2026 Fed decision is the key forward variable. No hike extends the thesis. A hike in line with consensus tests it, particularly for the rate-sensitive segments that have led the rally.

That convergence of drivers makes the rally more durable than a single-catalyst move, but it does not make it unconditional. If you are positioning in Singapore equities now, you are implicitly expressing a view on September’s outcome, and the honest framework is to know which parts of your exposure are most affected by each path.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Singapore stock market reached all-time highs on 25 June 2026 after an 11.3% first-half return, driven by a convergence of geopolitical safe-haven capital inflows, four simultaneous tailwinds for the big three banks, AI-linked semiconductor demand, and accelerating construction activity confirmed by a 29% rise in ready-mixed concrete demand.

When regional geopolitical risk rose ahead of the ceasefire, institutional and private capital flowed into Singapore as a safe-haven destination, resulting in a S$66 billion deposit surge in March 2026, roughly seven times the prior five-year monthly average of approximately S$9 billion.

Singapore's listed semiconductor exposure sits in equipment, precision engineering, and specialist components rather than chip foundries, meaning it captures capital expenditure from manufacturers like ASML, Applied Materials, and Lam Research without carrying the inventory-cycle volatility that affects foundries directly.

Energy and healthcare are assessed as structural laggards: energy names face declining global oil and gas investment that reflects a durable shift rather than a temporary pricing dip, while healthcare profitability is being squeezed by tighter insurer reimbursements and intensifying competition from Thailand, Malaysia, and India on medical tourism.

The September 2026 Fed decision is the single most important forward variable for Singapore equities: if rates stay unchanged as Phillip Securities Research forecasts, bank margins and REIT valuations remain supported, but if the consensus single hike materialises, the rate-sensitive segments that have led the rally face a direct valuation test.