The Case for Copper and Battery Metals as Infrastructure Bets

5 hrs ago

Before 2022, the idea that central banks in Poland, Brazil, and South Korea would be systematically exiting U.S. Treasuries and accumulating gold would have seemed implausible. Today it is documented policy. Two structural forces have converged across 2025 and 2026 to reshape who buys gold and why: sovereign reserve managers reassessing the political safety of dollar-denominated assets, and Asian retail investors deploying capital that has run out of attractive domestic alternatives. Neither of these shifts looks cyclical.

What follows is an analysis of each structural driver, the scale of demand they represent, and what they mean for investors evaluating a gold allocation today. The case for holding gold has historically rested on inflation hedging and crisis protection. Those motives remain valid. But the buyer base underneath the metal has changed in ways that alter the allocation question itself, from “how much insurance do I need” to “what is my exposure to a permanently expanded demand floor.”

In February 2022, the United States and its allies froze approximately $300 billion in Russian central bank assets following the invasion of Ukraine. Simultaneously, Russia was excluded from the SWIFT payment system. For non-aligned and semi-aligned nations, the message was immediate: dollar-denominated reserves carry only conditional safety, and that conditionality can be activated without warning.

Gold addresses this specific vulnerability through three properties:

The institutional response was swift. Central bank net gold purchases exceeded 1,000 tonnes annually in the years following 2022, roughly double the pre-2022 pace. The People’s Bank of China (PBoC) has purchased gold consistently on a quarterly basis since 2022, extending its buying streak into 2026. Poland has framed its accumulation in explicitly geopolitical terms. Brazil and South Korea, countries that historically maintained orthodox, dollar-heavy reserves, have added gold as well.

The National Bank of Poland has stated that gold has “wartime transactional and operational value that bonds cannot provide,” citing diversification needs amid geopolitical instability.

Before 2022, central bank gold buyers were typically emerging-market outliers. The post-2022 expansion to mid-sized, traditionally orthodox economies represents something different. Poland, Brazil, and South Korea are not hedging against their own domestic instability. They are hedging against the political conditionality of the reserve system itself. That distinction makes this demand structural rather than cyclical, and unlikely to reverse with a change in inflation data or interest rates.

Gold produces no cash flows, pays no dividends, and generates no earnings. Conventional income-based valuation frameworks do not apply.

The more relevant framework is the size and durability of the investor base willing to hold it. The number of investors incentivised to own gold, and the structural reasons compelling them, functions as the closest equivalent to an intrinsic value assessment.

That reframe matters because gold’s track record is stronger than many investors assume. Over the past 20 years, gold’s price performance has approximately matched the S&P 500 on a total-return basis. Gold has also historically tended to outperform equities during periods of negative equity returns, providing both long-run return contribution and downside cushioning in the same instrument.

Ray Dalio has been referenced as endorsing gold holdings in the current environment. According to JP Morgan data, average investor gold allocation has shifted meaningfully over recent years.

| Metric | Pre-2020 | Current |

|---|---|---|

| Average portfolio gold allocation | ~1% | ~2-2.5% |

| 20-year gold return vs S&P 500 | Approximately matched on total-return basis | |

Understanding gold through the lens of investor base expansion, rather than attempting to derive a fair value from absent cash flows, removes the most common source of confusion for investors considering an allocation.

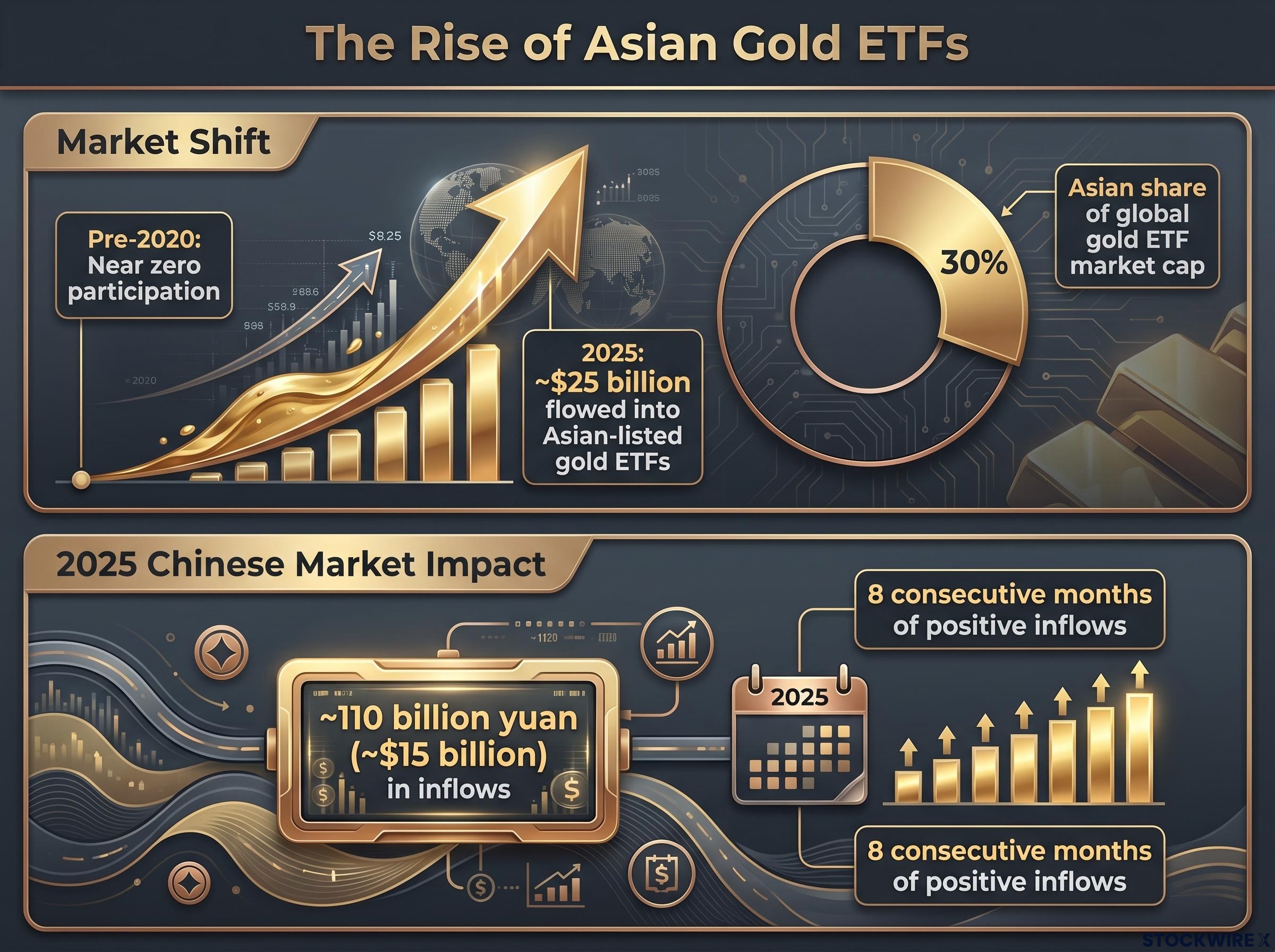

Prior to 2020, Asian participation in gold exchange-traded funds (ETFs) was negligible. Demand was expressed almost entirely through physical channels: jewellery, coins, and bars. The shift since then has been rapid enough to alter the structure of the global gold ETF market.

Approximately $25 billion flowed into Asian-listed gold ETFs in 2025. Asian products reached roughly 30% of global gold ETF market capitalisation, up from near zero previously.

Chinese gold ETF inflows alone reached approximately 110 billion yuan (around $15 billion) in 2025. These products recorded eight consecutive months of positive inflows despite significant price volatility, a pattern that indicates conviction rather than momentum chasing. When capital continues flowing through drawdowns, the signal points to structural reallocation.

The PBoC’s ongoing gold accumulation operates on two levels simultaneously. It is a sovereign reserve strategy, hedging against dollar-system risk. It is also an implicit domestic endorsement, signalling to Chinese retail investors that gold is both legitimate and politically safe. In a regulatory environment where official signals carry significant weight, this institutional green light is a material driver of household participation.

Three domestic conditions are pushing Chinese household capital toward gold:

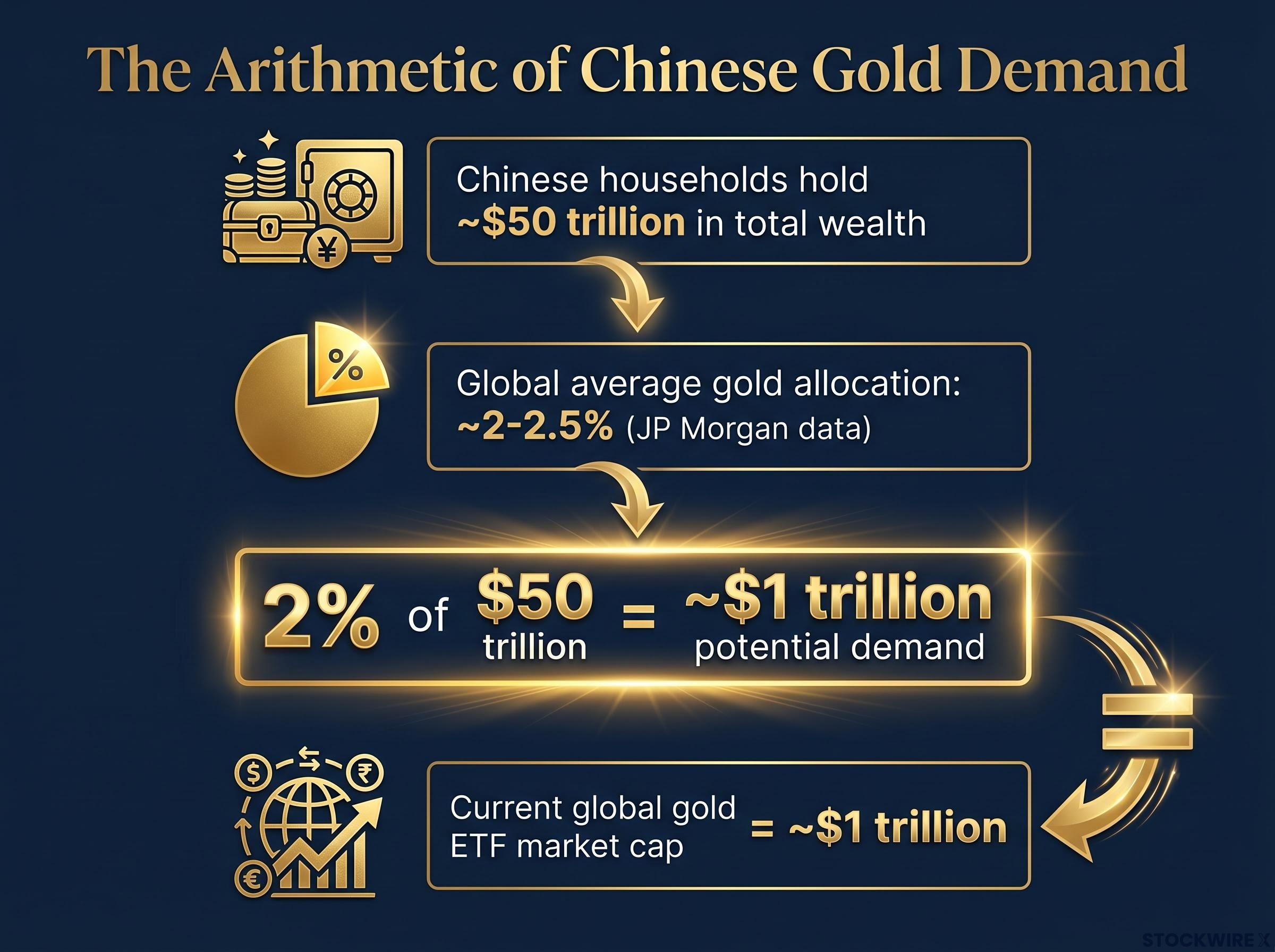

Chinese household wealth is estimated at approximately $50 trillion, among the most cash-rich investment pools globally. Gold fills multiple needs simultaneously: a long cultural and historical track record as a store of value, now accessible via liquid ETFs that remove custody friction.

The arithmetic of this reallocation warrants close attention. It requires no aggressive assumptions, only convergence toward what average global investors already hold.

A modest reallocation from one previously absent population could, in theory, match the current size of the entire global gold ETF market.

This calculation is not a price forecast. It is a scale illustration demonstrating how asymmetric the demand potential becomes when a very large, newly engaged investor base begins allocating even modestly to an asset class it was previously absent from.

The addressable market for gold has expanded dramatically relative to the pre-2020 period. The marginal buyer now includes a population whose incremental allocation decisions carry enough weight to move the global market. For investors, this means the structural case for gold does not require a crisis catalyst; it requires only continued convergence toward allocation levels that much of the world already maintains.

Central bank accumulation and Asian retail participation are not parallel trends operating independently. They form a feedback loop that becomes more durable as it develops.

The PBoC occupies a unique position in this dynamic. As a leading sovereign accumulator, its behaviour influences how other central banks think about reserve strategy. As a domestic signalling device, it legitimises retail gold participation across Chinese households. Official buying deepens retail liquidity. Growing retail depth integrates gold more centrally into the financial system. That integration, in turn, reinforces gold’s institutional credibility.

| Demand source | Primary driver | Nature of demand | Reversibility |

|---|---|---|---|

| Central banks | Geopolitical reserve hedging | Structural | Low; requires reversal of dollar-system risk perception |

| Asian retail | Reallocation from constrained domestic assets | Structural | Low; requires recovery of domestic alternatives |

The contrast with traditional demand drivers is instructive. Inflation fear and recession hedging are inherently cyclical; they intensify in downturns and fade in recoveries. The current reinforcing loop does not naturally self-correct in that way. Global gold ETF assets under management and holdings reached record levels by 2025-2026, and the shift from approximately 1% to 2-2.5% average portfolio allocation confirms the loop is already running. The allocation shift from 1% to 2.5% did not require a recession. It required a geopolitical catalyst and a structural reallocation, both of which remain in force.

The question investors historically asked about gold was whether it served as a good inflation hedge or crisis buffer at any given moment. That framing is no longer sufficient. The relevant question today is: what is the appropriate exposure to an asset with a permanently expanded and structurally supported demand base?

Traditional investment motives remain valid but are no longer the primary driver of marginal demand. Gold continues to offer:

What has changed is the buyer base underneath those properties. Central banks are accumulating for geopolitical resilience, not cyclical fear. Asian retail is reallocating from constrained domestic assets, not chasing a momentum trade. Both represent durable flows rather than easily reversed tactical positions.

The current global average allocation of 2-2.5% per JP Morgan data serves as a reference point. For investors whose allocation remains well below that level, the structural case outlined here provides a framework for reassessment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Two forces have converged to change the demand structure beneath gold. The 2022 freezing of Russian reserves permanently altered how sovereign reserve managers assess the political safety of dollar-denominated assets, triggering a broadening wave of central bank accumulation that shows no sign of reversing. Simultaneously, Asian retail investors have entered the gold ETF market at a scale that was absent in every prior cycle, driven by constrained domestic alternatives and implicit official endorsement.

Evaluating gold today means assessing structural buyer behaviour and reserve politics, not waiting for the next inflation print or recession signal. Future price paths remain uncertain, and short-term volatility is real. But the quality and durability of demand look materially stronger than in prior cycles. For investors building diversified portfolios, that shift in the demand floor changes what gold warrants as an allocation.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Two structural forces are driving gold demand: sovereign central banks diversifying away from dollar-denominated reserves following the 2022 freezing of Russian assets, and Asian retail investors reallocating capital from constrained domestic alternatives such as real estate, equities, and low-yield bonds into gold ETFs.

The 2022 freezing of approximately $300 billion in Russian central bank assets demonstrated that dollar-denominated reserves carry political conditionality; gold addresses this because it sits outside any national payment system, carries no sovereign counterparty risk, and cannot be frozen or excluded from SWIFT.

Chinese households hold an estimated $50 trillion in total wealth, and a 2% allocation (matching current global averages cited by JP Morgan) implies approximately $1 trillion in potential gold demand, a figure that matches the entire current global gold ETF market capitalisation.

Over the past 20 years, gold's price performance has approximately matched the S&P 500 on a total-return basis, and gold has historically tended to outperform equities during periods of negative equity returns, offering both return contribution and downside cushioning.

Cyclical demand, such as inflation fear or recession hedging, intensifies in downturns and fades in recoveries; structural demand, as seen today from central banks hedging geopolitical reserve risk and Asian retail investors reallocating from constrained domestic assets, does not naturally self-correct when inflation cools or economic conditions improve.