Lululemon Plunges 12% on CEO Pick Amid Activist Investor Battle

10 mins ago

The latest Parsons earnings report hit the wire early on 29 April 2026, delivering a sharp contrast between a 20% drop in net income and an immediate 3.15% pre-market share price surge. This early morning release arrived just before the scheduled 8:00 AM EDT earnings call, setting a complex tone for the broader first-quarter 2026 defence and infrastructure sector.

Investors looking purely at the surface metrics might initially see cause for concern regarding near-term profitability. However, unpacking these headline numbers exposes the operational efficiencies and a massive contract pipeline that are actually driving Wall Street’s early optimism.

The immediate market reaction demonstrated that headline net income rarely tells the full story for defence contractors. While Parsons reported a 20% drop in net income to $53 million, the company delivered an adjusted earnings per share beat that quickly shifted market sentiment. The stock jumped to $53.49 in pre-market trading, climbing 3.15% from the previous close of $51.84 on a prior day trading volume of 1,821,406 shares.

Analysts had set expectations lower. The company easily cleared this hurdle by posting an adjusted EPS of $0.79, improving upon the $0.78 recorded in the same period last year. This operational profitability metric overpowered the drop in GAAP EPS, which fell to $0.49 from $0.60 year-over-year.

| Metric | Q1 2026 Result | Q1 2025 Result | Analyst Expectation |

|---|---|---|---|

| Net Income | $53 million | $66 million (implied) | N/A |

| GAAP EPS | $0.49 | $0.60 | N/A |

| Adjusted EPS | $0.79 | $0.78 | N/A |

This core profitability proves that the foundational business remains intact despite top-line optical illusions. Institutional investors clearly weighted the adjusted earnings performance as a significant positive catalyst.

For readers wanting a comprehensive breakdown of the adjusted metrics, our detailed coverage of Parsons’ record profit margins examines how the company successfully overshadowed its surface-level revenue contraction with exceptional operational execution.

The top-line figures present a clear example of how government contracting cycles can temporarily skew a company’s financial profile. The firm reported total Q1 2026 revenue of $1.5 billion, representing a 4% year-over-year decline. However, this headline reduction masks strong underlying business growth entirely obscured by a single omitted contract.

Understanding defence sector financial reports requires distinguishing between ongoing operational health and planned contract conclusions. Undisclosed or classified government contracts often have strict, predefined lifespans that create massive revenue spikes during peak execution phases. When these specific agreements conclude or transition, the year-over-year comparisons can look artificially weak, even if the core business is expanding.

Omitting the impact of one specific undisclosed agreement completely changes the first-quarter narrative. According to company data, without that single contract, adjusted sales actually grew by 8%, supported by a 3% underlying organic growth rate. This growth was fueled by heavy ongoing demand in high-priority sectors, specifically space, missile defence, and critical infrastructure.

The 2026 defence space budget allocates significant capital toward advanced missile tracking and satellite architecture, creating an extremely favourable procurement environment for established government contractors.

Beyond adjusting for contract roll-offs, the company is actively extracting more profit from its existing operations. High margins act as a protective buffer against industry volatility, and management has successfully expanded profitability even while navigating complex transition periods. This raw operational efficiency explains why institutional analysts, including those at Truist, maintained buy ratings on the stock leading into the print.

A recent Truist Financial pre-earnings analysis highlighted these expanding margins as a key driver for long-term valuation growth despite broader macroeconomic headwinds.

The most compelling evidence of this execution lives in the cash utilisation and core earnings metrics. The company reported a highly favourable cash burn rate compared to the same period last year, signalling tighter financial controls.

Adjusted EBITDA hit a first-quarter peak of $151 million, representing a 1% increase year-over-year. The EBITDA margin expanded by 50 basis points to reach an all-time high of 10.1%. * According to company data, operating cash flow utilised only $4 million during the quarter, a significant improvement from the $12 million utilised during Q1 of the previous year.

Achieving record profitability metrics gives investors concrete evidence of management’s strong operational execution.

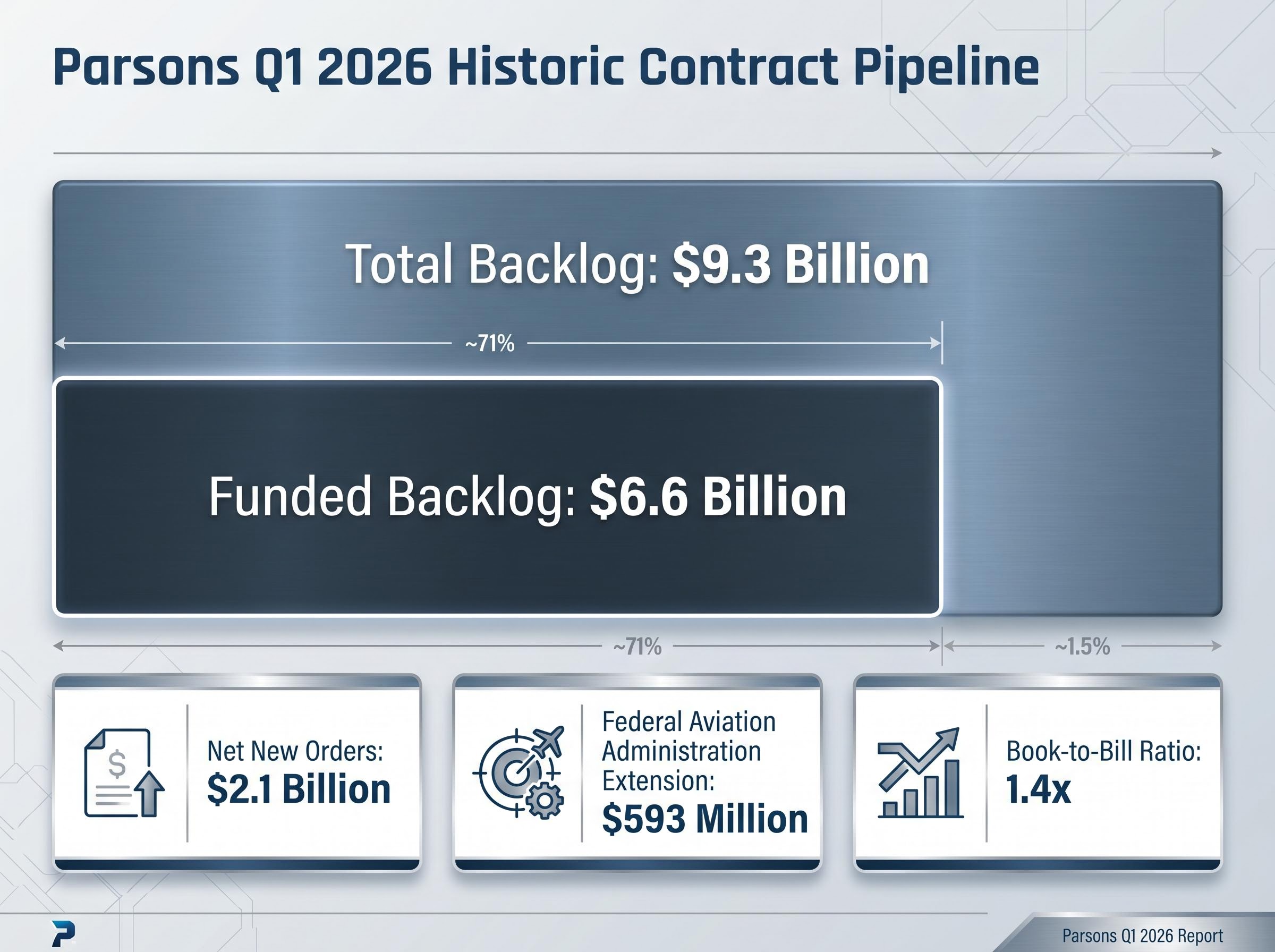

Short-term macroeconomic shocks hold little weight when a company sits on a guaranteed future pipeline. The sheer scale of the new order book heavily insulates the firm’s long-term commercial viability, providing deep revenue predictability through 2026 and well beyond. The business is currently winning new work significantly faster than it burns through existing obligations.

The broader expansion in targeted military appropriations, such as the massive increases in US defence drone spending, continues to provide a highly lucrative macro environment for contractors capable of meeting strict federal procurement standards.

This forward-looking strength is anchored by several historic milestones that define the bull case for the stock. The recent Federal Aviation Administration extension serves as a prime example of their targeted contract acquisition strength.

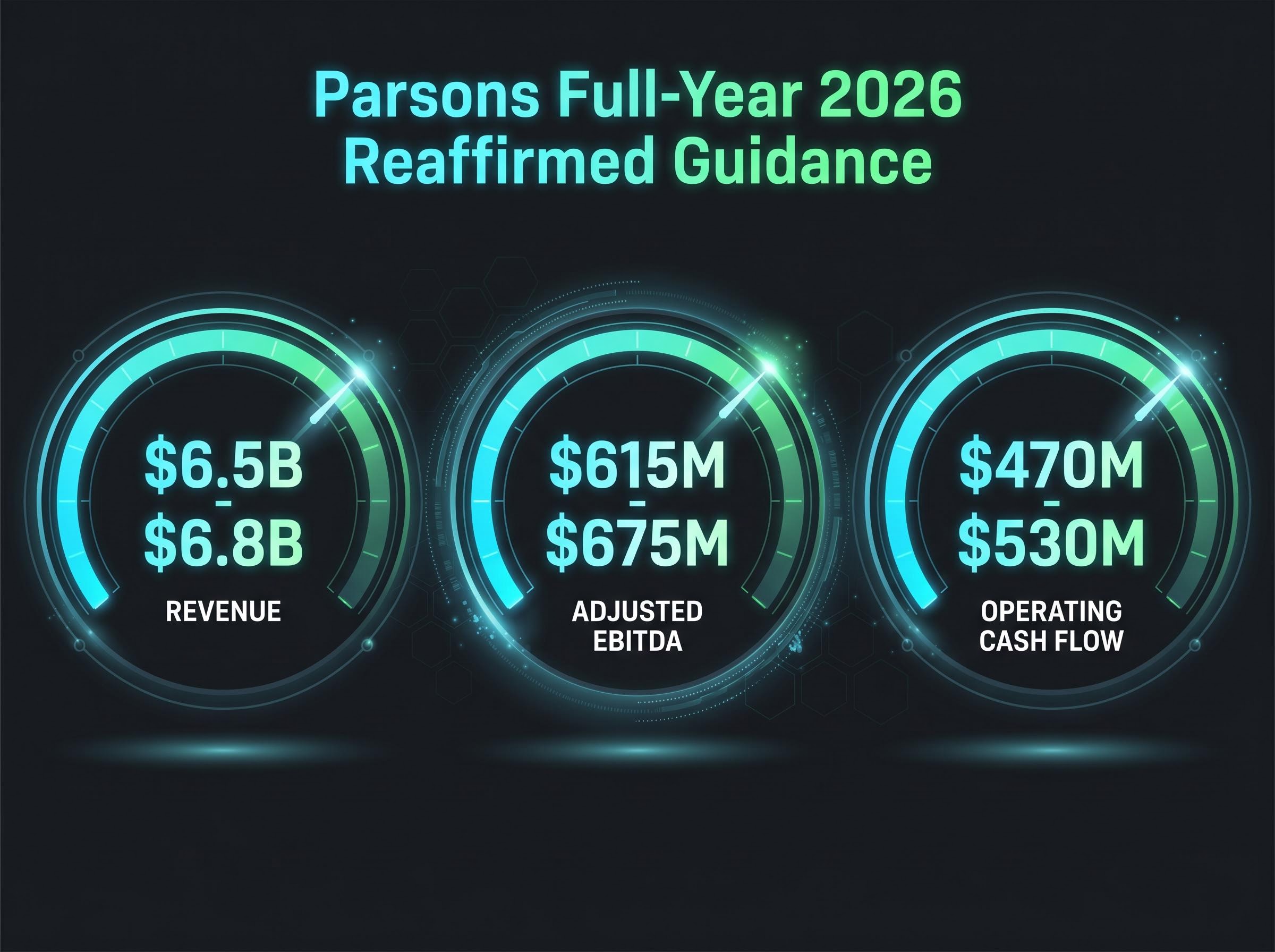

Because this earnings release arrived fresh on the morning of 29 April 2026, formal SEC 10-Q filings and post-call analyst price target adjustments remain pending. However, management provided immediate stability by maintaining their full-year financial projections despite the mixed surface-level first-quarter results. This reaffirmed guidance removes uncertainty, allowing investors to confidently model their portfolios for the remainder of the year knowing management stands by their initial targets.

The company maintained its full-year 2026 revenue projection at $6.5 billion to $6.8 billion. Full-year adjusted EBITDA guidance stands firm at $615 million to $675 million, alongside an operating cash flow projection of $470 million to $530 million.

Securing multi-year defence platform extensions creates high barriers to entry and fosters sticky customer relationships, which ultimately validate management’s confidence in these massive forward-looking revenue projections.

CEO Commentary “Our record adjusted EBITDA margin and strong book-to-bill ratio reflect solid demand across our defence, space, and critical infrastructure operations,” said Carey Smith, Chief Executive Officer.

Heading into the summer, the firm remains strongly positioned within the broader government contracting market.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The Q1 2026 Parsons earnings report showed a 20% drop in net income to $53 million, but a market-beating adjusted EPS of $0.79 and a 3.15% pre-market stock price increase. This mixed outcome was driven by strong operational efficiency and a record contract backlog.

Parsons' reported Q1 2026 revenue declined by 4% due to the planned roll-off of a single undisclosed government contract. Excluding this specific contract, the company's adjusted sales actually grew by 8%, fueled by demand in space, missile defense, and critical infrastructure.

Parsons reported a historic total backlog of $9.3 billion, a $235 million increase year-over-year, and a funded backlog of $6.6 billion. The company's book-to-bill ratio of 1.4x indicates that it is winning new work significantly faster than it completes existing obligations.

Yes, Parsons management reaffirmed its full-year 2026 financial guidance, projecting revenue between $6.5 billion and $6.8 billion, adjusted EBITDA of $615 million to $675 million, and operating cash flow of $470 million to $530 million. This provides investors with confidence in the company's future trajectory.

Parsons' adjusted EPS of $0.79, exceeding analyst expectations and improving year-over-year, signifies robust operational profitability and efficient management. This metric, combined with expanding EBITDA margins, suggests that the underlying business remains strong despite headline net income fluctuations.