ASX 200 Chart at a Supply Zone Test as NFP Week Looms

2 hrs ago

Starting from 1 July 2027, the proposed 2026-27 Federal Budget reforms retire the 50% capital gains tax discount for newly accrued gains, replacing it with cost base indexation so that only the inflation-adjusted real gain is taxable, alongside a 30% minimum tax rate applied to that real gain. The before-and-after is concrete, and it changes a calculation that every homeowner with spare cash has run in their head at least once: should the money sit in the offset account or go into an ETF?

That calculation has always turned on tax. What is shifting is which side of the comparison the tax system now favours. The reforms are announced in the 2026-27 Federal Budget but not yet enacted; they could be amended or not proceed. That caveat matters, and it belongs here at the outset rather than buried in a footnote.

Here is how to run the offset versus investing comparison under the proposed rules, across your own tax bracket, before 2027 arrives.

Three changes define the new regime:

The indexation piece brings the system closer to the original CGT design introduced in the 1980s, before the Howard government swapped it for the flat 50% discount. In a low-inflation environment, the indexed discount may produce a less favourable outcome than the current flat halving. When inflation runs higher, the real gain shrinks and partially offsets the impact of the minimum rate.

The CGT indexation rules that replace the flat 50% discount work by adjusting the cost base upward in line with CPI each year, so only the portion of nominal gain exceeding cumulative inflation becomes taxable; in high-inflation years the taxable gain shrinks materially, while in low-inflation years the real gain captured by the new regime can approach the full nominal gain.

The 30% floor is where the most common misreading will occur. It does not impose a flat 30% on every investor. A taxpayer already on a 37% or 45% marginal rate continues to pay CGT at their marginal rate; the floor does not reduce it. The 30% minimum binds only those whose effective marginal rate, after offsets, would otherwise sit below 30%. From 2027-28, the statutory brackets are 14%, 30%, 37%, and 45%, with the 2% Medicare levy generally added on top.

What this means for you depends heavily on two variables: your marginal rate and the inflation environment during your holding period. Both need to be known before you can draw any conclusion about your own portfolio.

Assets purchased before 1 July 2027 are not fully retrospectively taxed. Gains accrued up to that date still attract the 50% discount. Only gains accruing after 1 July 2027 fall under the new indexation and minimum rate regime, even if the asset was bought years earlier. Pre-CGT assets receive their own separate treatment and sit outside this comparison entirely.

The ATO does not treat the interest saved through an offset account as income or a capital gain. Depositing funds, accumulating interest savings, and withdrawing all occur without generating a taxable event. This is not an accidental gap in the rules or a policy loophole; it is a straightforward consequence of how the tax system characterises the return. The account holder is not receiving a payment. They are simply avoiding an interest charge that would otherwise apply.

ATO Taxation Ruling TR 93/6 on loan account offset arrangements establishes that no interest is derived by the account holder under a standard offset structure, meaning the benefit arising from the account does not constitute assessable income under the tax law.

“Under current rules, offset returns sit outside the income and CGT systems, making them structurally less exposed to these specific reforms.”

Any change to this treatment would require a distinct and separate policy intervention beyond the CGT reforms currently proposed. That does not make it impossible, but it is not part of what has been announced.

The asymmetry this creates is the point. The 2027 reforms make the investing side of the comparison more expensive after tax. The offset side stays exactly where it was. One leg of the comparison just moved; the other did not.

Before anchoring to the headline mortgage rate as the offset return, account for the costs that reduce the effective yield:

These costs must be netted against the gross offset benefit before the comparison is honest.

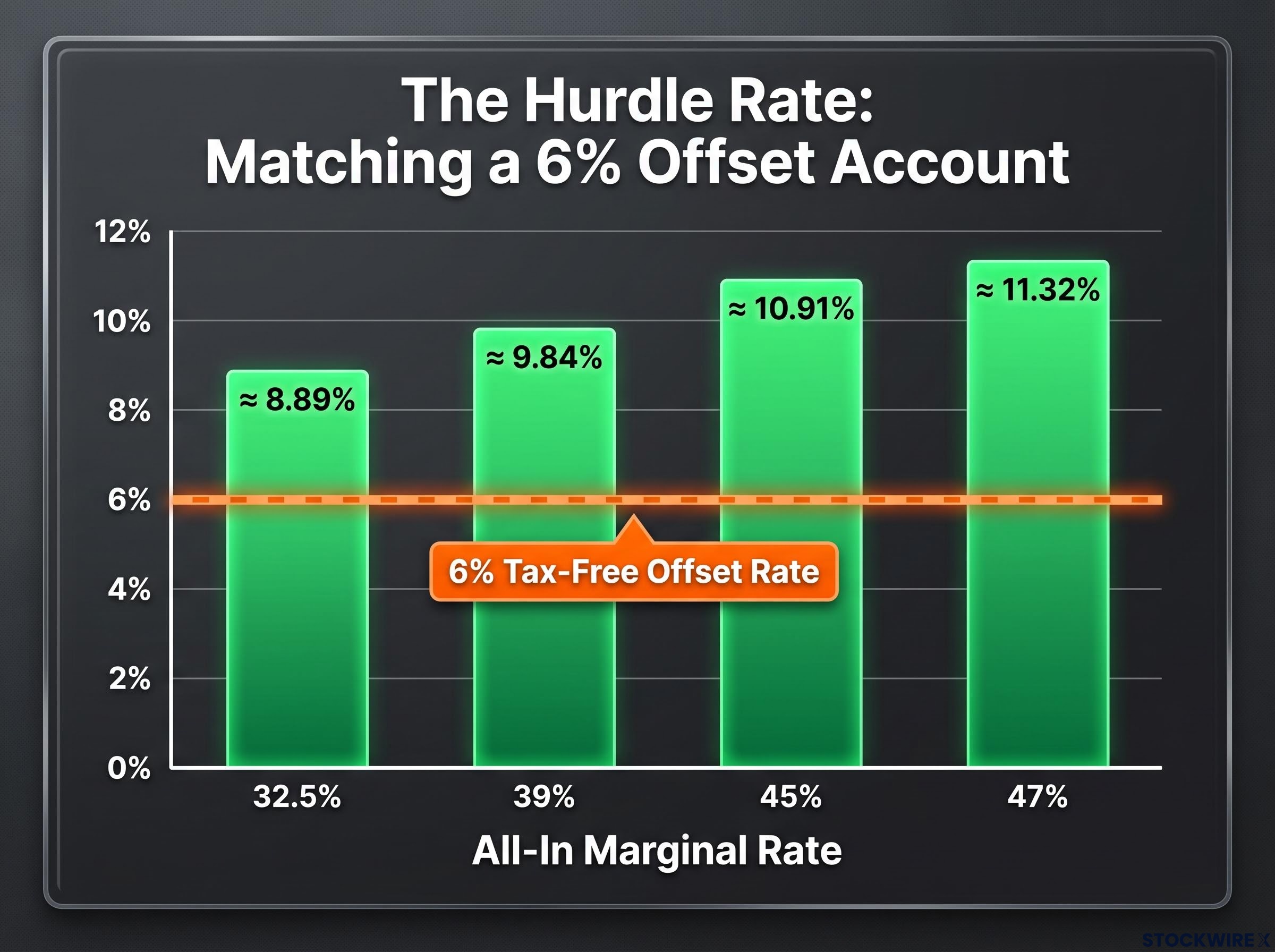

Most people anchor to the headline mortgage rate when thinking about what an offset account is worth. That anchor is wrong. The offset return is tax-free, so comparing it to a taxable investment return requires converting it into a gross equivalent yield, which is the pre-tax return an investment would need to deliver to match the offset after tax.

The same inflation dynamic that determines how much cost base indexation reduces taxable gains also erodes real purchasing power on any cash position left outside the mortgage structure, meaning the true comparison set is not just offset versus equities but offset versus savings account versus taxable investment, each with distinct inflation and tax drag profiles.

The formula is straightforward: offset interest rate ÷ (1 minus your marginal tax rate).

A practical example: at a 6% mortgage rate and a 39% all-in marginal rate (the 37% bracket plus 2% Medicare levy), the equivalent taxable return is approximately 9.84%. That means an investment would need to generate nearly 10% before tax to match what the offset delivers tax-free.

The numbers shift dramatically across brackets.

| All-In Marginal Rate | Offset Rate | Gross Equivalent Yield | Implication |

|---|---|---|---|

| 32.5% | 6% | ≈ 8.89% | Competitive but beatable in strong equity years |

| 39% | 6% | ≈ 9.84% | Hard for diversified ETFs to match consistently |

| 45% | 6% | ≈ 10.91% | Exceeds long-run equity averages |

| 47% | 6% | ≈ 11.32% | Extremely difficult to beat after tax |

For a 47% taxpayer, the offset is not competing against a 6% investment return. It is competing against 11.32%. That reframing changes the investment decision entirely.

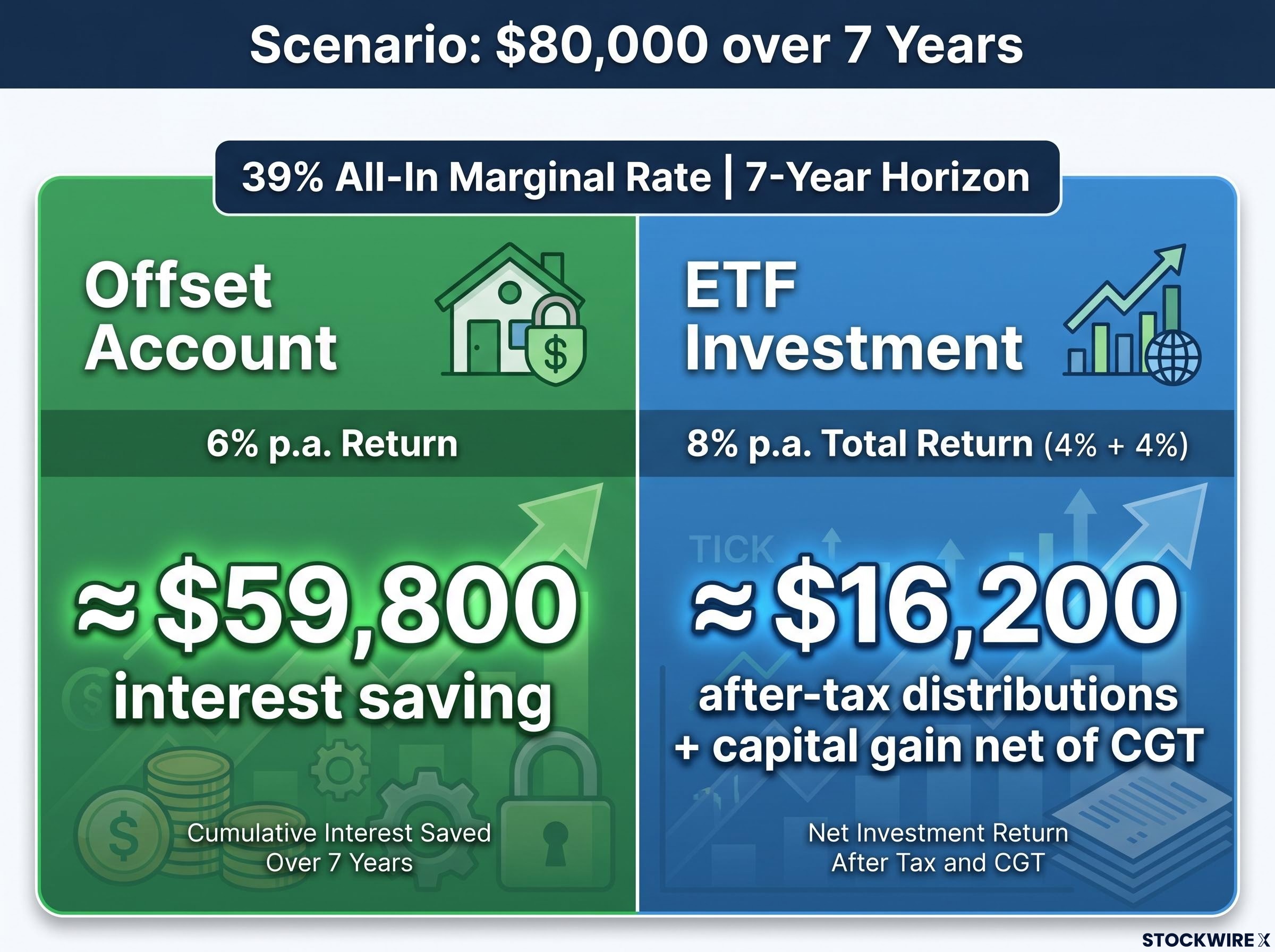

The clearest way to see the after-tax gap is to run both options through the same set of assumptions. The table below is a simplified illustration, not a precise tax model; it uses rounded compounding and ignores reinvestment frictions to isolate the directional impact of tax.

These examples use rounded compounding and simplified tax treatment to illustrate the directional impact of the reforms. They are not a substitute for personalised tax modelling.

Scenario assumptions: $80,000 initial amount, 6% p.a. mortgage rate, ETF total return 8% p.a. (split 4% distributions and 4% capital growth), 39% all-in marginal rate, 2.5% p.a. inflation, 7-year horizon.

| Scenario Metric | Offset Account | ETF Investment |

|---|---|---|

| Initial amount | $80,000 | $80,000 |

| Assumed return | 6% p.a. (interest saved) | 8% p.a. total (4% + 4%) |

| Tax on return | Nil | Distributions at 39%; capital gain at marginal rate on indexed gain |

| Estimated 7-year outcome | ≈ $59,800 interest saving (amortisation-dependent approximation) | ≈ $16,200 after-tax distributions + capital gain net of CGT |

| After-tax return equivalent | ≈ 6% p.a. tax-free | ≈ mid-4% p.a. after tax |

The ETF distribution component, 4% p.a. taxed at 39%, delivers approximately 2.44% p.a. after tax. Over seven years on a simplified non-reinvested basis, that totals roughly $16,200 after tax.

ETF distributions and CGT interact in ways the simplified scenario above necessarily compresses: the taxable component of an ETF distribution varies by fund structure, internal turnover, and whether gains are passed through or retained, and the 12-month holding period rule for CGT discount eligibility creates planning considerations that affect the timing of any realisation under the new post-2027 regime.

The capital growth component compounds $80,000 at 4% p.a. to approximately $105,300, a nominal gain of around $25,300. At 2.5% annual inflation over seven years, the cost base rises by approximately 17-19%, reducing the taxable real gain. The remaining real gain is then subject to the 30% minimum rate, or the investor’s marginal rate if higher.

The offset outcome, approximately $59,800 over seven years, reflects the amortisation dynamic of a 25-year variable mortgage: reducing the principal earlier produces accelerating interest savings in later years.

The after-tax gap is not marginal. Under these assumptions, the offset materially outperforms on a risk-adjusted, after-tax basis for a 39% taxpayer. That conclusion becomes stronger, not weaker, as the marginal rate rises.

The comparison does not produce a universal answer. Three conditions can tilt the numbers back toward ETF investing:

The honest framing is that the 2027 reforms tilt the comparison toward the offset for most middle-to-high income borrowers, but do not make it the universal answer. If your marginal rate is lower or your return assumptions are higher, you may reach a different conclusion.

An offset account produces a return that tracks the prevailing mortgage rate and does not fluctuate with market conditions, giving borrowers a stable, predictable outcome each month. For those carrying large mortgages or operating with limited financial headroom, that steadiness represents genuine practical value rather than a sales pitch. Funds remain fully accessible and liquid, unlike most investment structures, which matters for emergency reserves and financial flexibility.

That said, offset accounts provide no capital growth participation, no dividend reinvestment benefit, and no exposure to the long-term compounding that equities deliver at higher assumed return rates. The spreadsheet captures the tax comparison; it does not capture the opportunity cost of sitting outside equity markets for a decade.

The decision reduces to three variables you can identify right now:

These reforms are announced but not legislated. Monitoring parliamentary progress before making irreversible portfolio decisions is appropriate.

For investors wanting to redirect capital toward tax-advantaged structures before July 2027, our dedicated guide to superannuation contribution strategy covers the carry-forward rules, the rising concessional caps from 1 July 2026, and the specific scenarios where maximising super contributions produces materially better after-tax outcomes than either the offset or direct equity investment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions, particularly where significant capital gains have already accrued or where the 30% minimum rate interacts with other income sources.

For middle-to-high income Australian homeowners with variable mortgages, the 2027 CGT reforms narrow or eliminate the traditional after-tax return advantage that ETF investing held over offset accounts under the old 50% discount regime. That is not a case for abandoning investing. It is a case for recalibrating the allocation decision with the new tax reality factored in explicitly.

The reforms are not yet law. Monitoring legislative progress and reassessing when the final legislation is confirmed remains the prudent path. But the directional shift is clear: the after-tax, risk-free return available through your offset account has become a genuinely tougher benchmark for taxable investments to clear.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. The CGT reforms discussed are proposed and may be amended before enactment.

—

From 1 July 2027, the 50% CGT discount for newly accrued gains is replaced by cost base indexation, where only the inflation-adjusted real gain is taxable, with a 30% minimum tax rate applied to that real gain. These changes are announced in the 2026-27 Federal Budget but are not yet legislated.

The interest saved through an offset account is tax-free and untouched by the 2027 CGT reforms, while ETF returns face distribution tax at marginal rates and capital gains tax on indexed gains at a 30% minimum rate. For a 39% taxpayer at a 6% mortgage rate, an ETF would need to return nearly 9.84% before tax just to match the offset after tax.

No. The 30% floor only binds investors whose effective marginal rate would otherwise fall below 30%; taxpayers already on the 37% or 45% marginal rate continue to pay CGT at their marginal rate, and the floor does not reduce it.

Yes. Under the transitional rules, gains accrued up to 1 July 2027 still attract the existing 50% discount; only gains accruing after that date fall under the new indexation and minimum rate regime, even for assets purchased years earlier.

Divide your mortgage rate by one minus your marginal tax rate: at a 6% offset rate and a 39% all-in marginal rate, the gross equivalent yield is approximately 9.84%, meaning a taxable investment must return nearly 10% before tax to match what the offset delivers tax-free.