Delivery Hero Shareholders Reject Uber’s €33 Bid, Demand €40+

12 mins ago

A wildfire destroys a town, and the utility blamed for sparking it loses 70% of its share price in days. Most investors close the tab and move on. The question worth asking now, nearly three years later, is whether that reaction, entirely understandable at the time, has produced a pricing dislocation that rewards the investors who stayed.

Hawaiian Electric Industries (HEI) entered 2024 as a distressed company: dividend suspended, credit downgraded, and facing a $1.99 billion settlement obligation from the August 2023 Maui wildfires. By early July 2026, the stock has recovered approximately 27% year-over-year and trades near $13.63. That recovery looks significant until you measure it against a base case valuation estimate of roughly $25 per share. The gap between price and estimated intrinsic value remains wide.

For readers who evaluate special situations on probability-weighted expected value, the setup still warrants a close look. Here is the settlement mechanics, the regulated utility valuation framework, and the bear-to-bull scenario analysis, laid out so you can assess whether the remaining discount is opportunity, value trap, or something in between.

The market’s initial reaction to the Maui wildfires treated HEI as an open-ended catastrophic liability. That was reasonable in August 2023, when the scope of claims was unknown and the company’s survival was a genuine question. The settlement changed the calculus, not because it made the liability small, but because it made it modelable.

The persistence of a pricing dislocation in a name this widely covered requires an explanation rooted in investor behaviour rather than information asymmetry: loss aversion causes institutional holders to exit at precisely the moment the gap between price and business value widens most, and the passive-investing dominance that now controls roughly 63% of US equity fund assets further reduces the fundamental pricing signal for individual stocks navigating legal overhang.

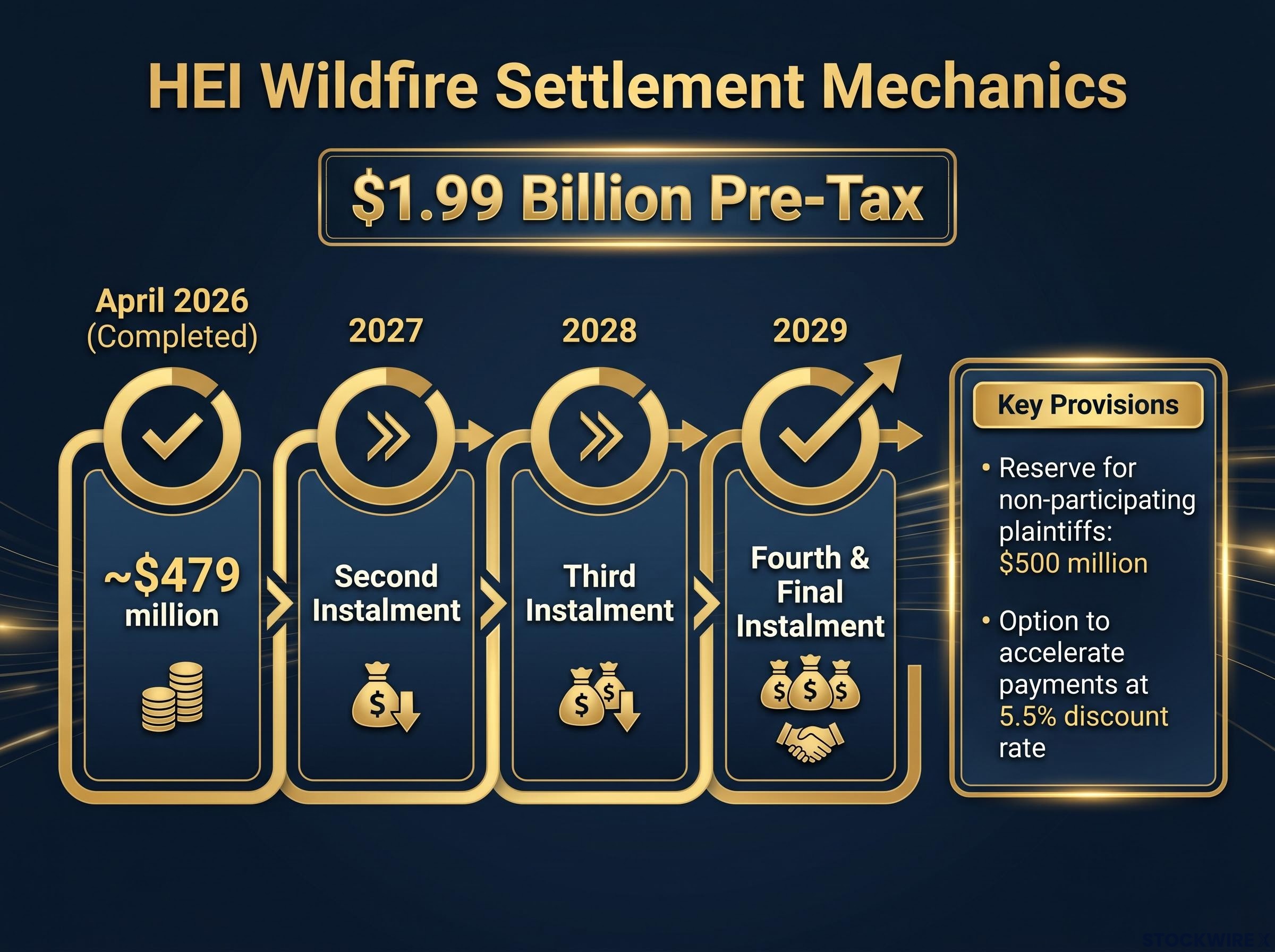

HEI and Hawaiian Electric Company agreed to a global settlement of approximately $4.0 billion across all co-defendants. HEI’s share is $1.99 billion pre-tax, structured as four equal annual instalments of approximately $478.75-$479 million each. The first instalment was completed in April 2026. Three remain, implying full payment around 2029 on a standard annual cadence.

The instalment timeline:

The companies retain the option to accelerate payments in whole or in part at a 5.5% discount rate. The settlement is explicitly without admission of liability and resolves wildfire tort claims arising from the Lahaina, Kula, and Olinda fires among participating plaintiffs and defendants.

A $500 million reserve within the total settlement is specifically designated for defendants to help defray costs related to non-participating plaintiffs, effectively capping the exposure from claims that fall outside the settlement framework.

That reserve is the detail most investors overlook. It means the tail risk from holdout plaintiffs is bounded, not open-ended.

The $47.75 million shareholder securities settlement, reported as reached in January 2026 and subject to court approval, is a separate obligation. It is substantially smaller in magnitude but remains unresolved. Judicial discretion over legal fees, objector treatment, and disbursement timing persists and could affect exact payment tempo. And the financing mix for the remaining instalments, including the ultimate split between debt, common equity, and equity-linked securities, has not been fully determined.

These are real uncertainties. They are also bounded ones, not open-ended threats to the settlement structure itself. The investment thesis here is not a binary bet on whether HEI survives; it is a duration trade. The question you are evaluating is whether the price paid today compensates for the four-year wait until settlement obligations clear.

Most distressed equity frameworks assume uncertain future revenues. A company in financial stress typically faces the combined risks of shrinking demand, competitive pressure, and operational deterioration. Hawaiian Electric operates under a different set of rules, and understanding them changes how you model the downside.

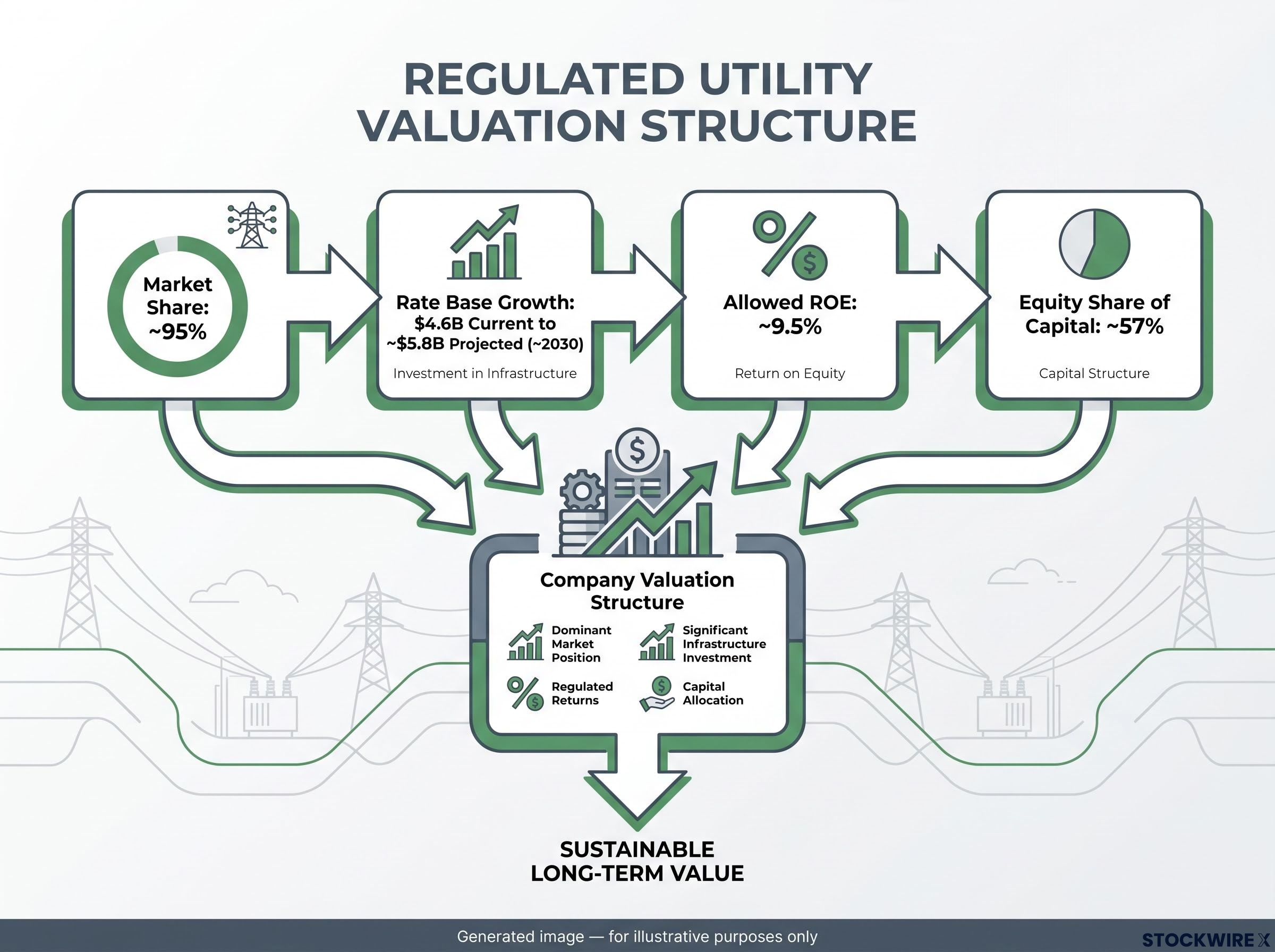

HEI supplies approximately 95% of Hawaii’s electricity through a Public Utilities Commission (PUC)-regulated monopoly. The PUC sets a maximum allowed return on equity (ROE), which is the profit rate the utility is permitted to earn on its invested capital. That ROE is currently approximately 9.5%. The cap constrains the upside, but it also functions as a de facto earnings floor under normal operating conditions, because the regulator allows the utility to set rates high enough to earn that return.

Common equity comprises approximately 57% of the capital structure. The current rate base (the value of assets on which the utility earns its allowed return) sits at approximately $4.6 billion, with a projected path to approximately $5.8 billion by around 2030, driven by approved capital investment in decarbonisation, grid hardening, and wildfire prevention.

| Metric | Current | Projected (~2030) | Modelled earnings implication |

|---|---|---|---|

| Rate base | $4.6B | ~$5.8B | Higher base drives higher allowable revenues |

| Allowed ROE | ~9.5% | Subject to PUC rate case | Sets the profit rate on invested capital |

| Equity share of capital | ~57% | Dependent on financing mix | Determines what portion of ROE flows to equity holders |

| Market share | ~95% | ~95% | No competitive displacement risk |

All projected figures are forward-looking modelling assumptions, not confirmed guidance. Subject to PUC decisions and capex execution.

The arithmetic works like this: rate base multiplied by allowed ROE multiplied by equity share of capital structure yields an estimated allowable net income. As the rate base grows through approved capital spending on grid hardening and wildfire mitigation, the allowable revenue grows with it at the fixed ROE.

The variable that matters most is PUC approval. Not all capex is automatically rate-recoverable. What portion of wildfire mitigation spending gets approved for inclusion in the rate base, versus absorbed by equity, directly affects whether realised earnings match allowed earnings. For you, evaluating this as a special situation, the regulated structure means earnings projections carry higher confidence than almost any unregulated equity in a comparable distressed state. The ceiling and the floor are both set by a regulatory body, not by competitive market dynamics.

The Hawaii PUC wildfire mitigation plans, including Order No. 42228 approving Hawaiian Electric’s 2025-2027 plan, set the regulatory framework that determines which capital expenditures qualify for rate base inclusion, a gating decision that directly shapes whether realised earnings track the modelled $1.40 EPS.

The equity yield curve is a framework that projects earnings yields across multiple forward years, analogous in concept to a bond yield curve but applied to an equity income stream. It works particularly well for regulated utilities because the earnings have fewer uncertain variables than typical equities: the return rate is set, the capital base is known, and the customer base is captive.

Regulated utilities have no product market exposure, no competitive displacement risk, and a known ROE ceiling set through a formal regulatory process. That combination makes projected cash flows more modelable than in virtually any other equity category. It is what enables the scenario analysis in the next section to produce narrower outcome bands than most distressed situations allow.

Intrinsic value estimation applied to regulated utilities requires stress-testing the terminal value assumption, which typically drives 60-80% of any DCF model’s implied worth, and for HEI that stress test centres almost entirely on what PUC approves for rate base inclusion rather than on competitive or demand-side variables.

Here is where HEI sits today. The yield on the stock is currently negative because settlement obligations exceed distributable earnings, and the dividend remains suspended. That negative yield is the distress the market is pricing in.

Once the final instalment clears around 2029, free cash flow becomes available for dividend reinstatement. Net income after settlement, based on the rate base and capital structure assumptions above, is projected at roughly $270-$275 million per year. Dividing that figure by an anticipated fully diluted share count of approximately 195 million shares, which accounts for expected equity issuance to finance the settlement payments, yields an estimated earnings per share of approximately $1.40.

Looking at the ten years prior to 2023, the market valued Hawaiian Electric at a median price-to-earnings multiple of 19.22 times earnings. Rounding that figure to 20x and applying it to the $1.40 EPS estimate points to a base case implied share price of around $25, which is roughly 85% above the current price of approximately $13.63.

At that current price, the forward earnings yield comes to approximately 10%. The US 10-year Treasury yields approximately 4-4.5%. The spread between those two numbers is the core of the valuation argument. What you need to assess is whether that premium adequately compensates for the duration risk, regulatory risk, and financing execution risk that sit between now and the point where the settlement clears.

All EPS, share count, net income, and rate base figures are forward-looking modelling assumptions, not confirmed guidance.

Probability-weighted expected value analysis separates special situation investing from speculation. Each scenario below is not just a price target; it is a story about what you need to believe for that outcome to materialise.

| Scenario | Key assumptions | Implied ~2030 price | Estimated return | Primary risk or catalyst |

|---|---|---|---|---|

| Bear | Lower rate base, ROE underperformance, possible additional disaster or dilution | ~$12 (approx. 11% loss) | -11% total by 2030 | Second catastrophic event; regulatory backlash |

| Base | Rate base to ~$5.8B, ROE near 9.5%, successful financing, dividend ~2029 | ~$25 | ~13% annualised (probability-weighted) | Financing execution and PUC approvals |

| Bull | Multiple expansion to mid-20s P/E, inflationary cost pass-through | >$30 | Above base case | HEI demonstrates wildfire mitigation leadership |

The bear case assumes the thesis breaks. Rate base approval comes in 10-20% lower than the $5.8 billion assumption. Realised ROE underperforms allowed ROE by 100-200 basis points (a basis point is one-hundredth of a percentage point). An additional $0.5-$1.0 billion of capital spending is partially unrecovered. The stress-test inputs:

Even under those conditions, the projected loss is approximately 11% by end of 2030. That is a narrower bear case than most distressed equities produce. But fat-tail risks, another major wildfire or hurricane, or aggressive regulatory backlash, could plausibly widen that band. You should stress-test those scenarios before accepting the probability-weighted return at face value.

The base case assumes rate base growth proceeds on schedule, the settlement is financed without excessive dilution, and the dividend is reinstated around 2029. That delivers an implied share price of approximately $25 and a probability-weighted annualised return of approximately 13%.

The bull case requires the market to apply a mid-20s P/E multiple, conditional on HEI demonstrating regional leadership in wildfire risk reduction. Because this is a post-crisis name with a highly public catastrophic event, investors may cap future multiples below pre-crisis highs unless climate risk perception shifts materially.

The settlement converted open-ended catastrophic liability into bounded, scheduled payments. It did not eliminate risk. Here are the specific mechanisms by which the thesis fails, each with what you should monitor.

Thesis checkpoint worth watching: Financing execution is the one variable most directly in management’s hands between now and 2029. If you want to monitor this position actively rather than passively, treat each capital raise announcement as the key data point for recalibrating your share count and EPS assumptions.

Knowing which risks are bounded (tort claims, non-participating plaintiff exposure) versus which remain open (financing mix, regulatory outcomes, climate events) helps you decide whether this is a position you monitor passively or actively re-evaluate with each new filing.

Value investors define risk as the probability of permanent capital loss rather than price volatility, and that distinction matters here because HEI’s share price volatility since August 2023 has been extreme while the probability of permanent loss, given the structured settlement and regulated revenue floor, is substantially lower than the share price movement implies.

The remaining upside estimate of approximately 85% to the base case target is substantial. It is also earned over a four-year horizon, not a near-term trade. There is no single announcement that unlocks value here. Value accrues progressively as each instalment is paid and the market begins to reprice the stock in line with its underlying regulated earnings capacity.

| Period | Expected development | Thesis checkpoint | What to monitor |

|---|---|---|---|

| 2026 (completed) | First instalment paid April 2026 | Settlement execution on track | Financing terms and share issuance |

| 2027-2028 | Second and third instalments | Market sentiment expected to shift ~2028 | PUC rate case outcomes, capex approvals |

| 2029 | Fourth and final instalment; dividend reinstatement targeted | Settlement fully discharged | Final share count, dividend policy announcement |

| 2030 | Full business normalisation | Base case price target ~$25 | Earnings delivery vs. modelled $1.40 EPS |

The 27% year-over-year appreciation through early July 2026 is real progress. But it has compressed the forward yield from earlier, higher estimates. Investors entering at today’s price of approximately $13.63 rather than near the crisis lows are buying a different return profile. As a reference point, the original position analysis describes an approximately $10 cost basis with a projected dividend yield on cost of approximately 10% at reinstatement. Entry price materially affects the return arithmetic.

The structural advantage for patient investors is genuine: the underlying business is an irreplaceable essential service with embedded downside protection, the payment schedule is known and partially executed, and rate base growth through approved capex provides a contractual pathway to higher allowable revenues. The distressed pricing reflects a mismatch between a 2029-2030 thesis maturation and the shorter-term focus of most market participants.

The question is personal rather than analytical. The probability-weighted annualised return of approximately 13% and the roughly 85% base case upside are the analytical outputs. Whether you have the patience the thesis explicitly requires, and whether that return justifies the wait relative to your alternatives, is a decision only you can make.

Klarman’s sourcing approach, which uses the worst-performing stocks over a 6-12 month window as a starting watchlist before overlaying balance-sheet strength and normalised earnings, is one structured method for identifying undervalued stocks in situations like HEI, where the price dislocation originates in structural seller pressure rather than permanent business deterioration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. All forward-looking projections, including EPS estimates, rate base growth, share count assumptions, and price targets, are modelling assumptions subject to change based on market developments, regulatory outcomes, and company performance. Past performance does not guarantee future results.

Hawaiian Electric Industries agreed to pay $1.99 billion as its share of a $4.0 billion global settlement covering the August 2023 Maui wildfires, structured as four equal annual instalments of approximately $479 million each, with the first completed in April 2026 and the final payment expected around 2029.

The stock remains depressed because the dividend is suspended, settlement obligations currently exceed distributable earnings, and institutional loss aversion has driven persistent selling pressure even after the liability was converted from open-ended catastrophic exposure into a bounded, scheduled payment structure.

Once the final instalment clears around 2029, HEI is projected to generate approximately $1.40 in earnings per share, derived from an estimated $270-$275 million in annual net income divided across a fully diluted share count of approximately 195 million shares.

The base case target is approximately $25 per share, calculated by applying HEI's historical median price-to-earnings multiple of roughly 20x to the projected $1.40 EPS estimate, and assumes the rate base grows to approximately $5.8 billion by 2030, the settlement is financed without excessive dilution, and the dividend is reinstated around 2029.

The primary risks are financing execution (greater equity dilution than modelled compresses EPS below $1.40), regulatory outcomes (the PUC could reduce the allowed ROE or deny capex for rate base inclusion), and a second catastrophic wildfire or hurricane before grid hardening is complete, which could reopen liability exposure beyond the settlement's $500 million reserve for non-participating plaintiffs.