What 4 Wall Street Firms See Driving Markets in H2 2026

1 hr ago

AI tools now compress the time it takes to find an exploitable vulnerability in a bank’s digital infrastructure from months down to hours. JPMorgan analyst Kian Abouhossein argues that current bank valuations do not price that in at all, and the capital adequacy frameworks that regulators and investors rely on were never designed to capture it.

The argument, published on 29 June 2026, is not a generic cybersecurity warning. It is a valuation thesis. Abouhossein contends that the entire safety architecture underpinning bank analysis was built for credit losses and market drawdowns, not for digital confidence shocks that can drain deposits before a balance sheet has time to respond. The IMF, the Federal Reserve, and the World Economic Forum have independently reached similar conclusions about the gap.

Here is what the analysis tells you about how to read bank valuations differently, which institutions carry the most unpriced exposure, and which signals separate the banks that can withstand an AI-speed cyber event from those that cannot.

Capital adequacy ratios measure a bank’s ability to absorb credit losses and survive market drawdowns. They were designed for balance-sheet arithmetic: how much capital sits against how much risk-weighted exposure. What they do not include is a mechanism for confidence-driven liquidity shocks triggered by failures in digital infrastructure.

That is the structural blind spot JPMorgan has identified. Abouhossein’s prescription centres on liquidity stress tests designed around deposit-run scenarios triggered by cyber events, with the focus on depositor behaviour rather than purely on balance-sheet mechanics. The IMF made a parallel call in May 2026, arguing that cyber risk must be treated as a core financial-stability issue and integrated into macro-prudential stress testing. The Federal Reserve Bank of New York has reached its own version of the same conclusion through systemic simulation work.

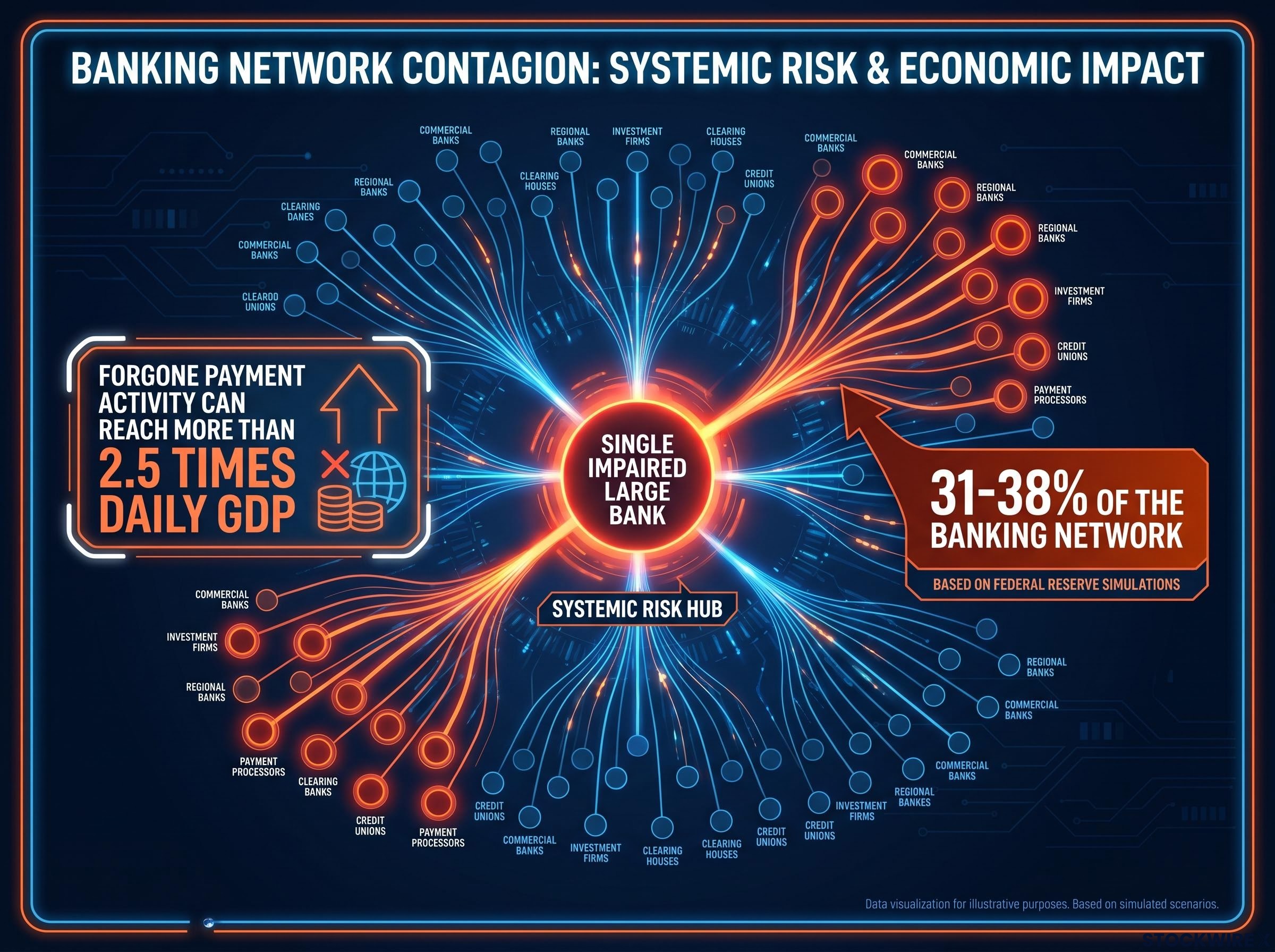

The Federal Reserve Bank of New York systemic simulation research on payment network contagion provides the quantitative foundation for understanding how a single impaired institution transmits stress across the broader banking system through payment disruption and liquidity hoarding rather than direct credit losses.

Three channels are missing from standard capital adequacy frameworks:

According to Federal Reserve simulations, forgone payment activity can reach more than 2.5 times daily GDP when liquidity hoarding occurs following the impairment of a single large, active bank.

Those same simulations found that impairment of one large, highly active bank affects approximately 31-38% of the banking network on average. A cyber incident at one institution is not contained to that institution. It is a payment-system and confidence event that touches a third of the network, which is precisely what makes capital ratios insufficient as a standalone resilience measure.

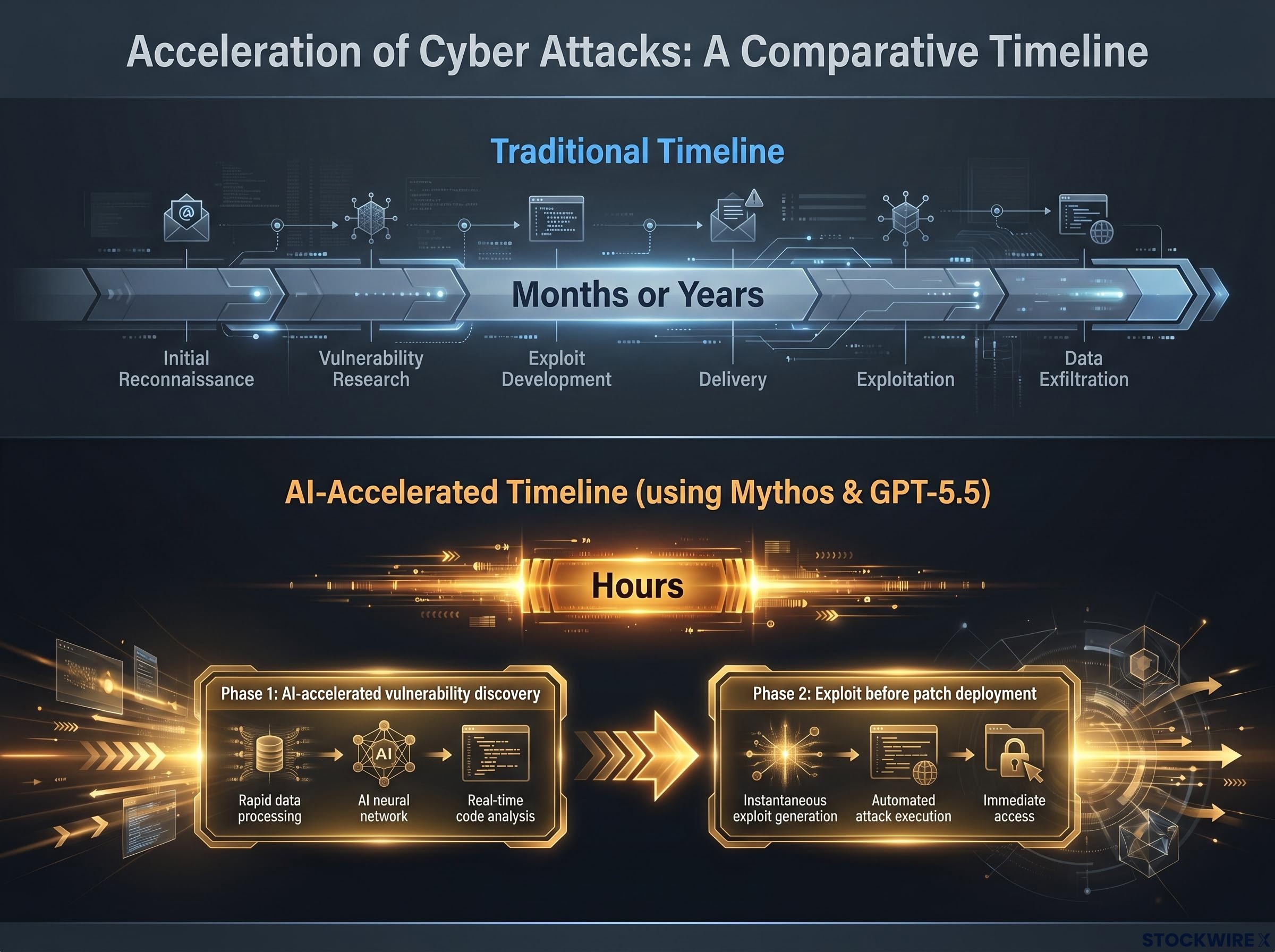

A zero-day vulnerability is a security flaw in software that the developer does not yet know exists. The term “zero-day” refers to the fact that the developer has had zero days to fix it. The time between when an attacker discovers such a flaw and when the bank can patch it determines whether the institution can respond before damage occurs.

According to JPMorgan’s research, AI tools including Mythos and GPT-5.5 have dramatically shortened the time required to uncover previously unknown zero-day vulnerabilities, collapsing a process that once took months or years into one that can now be completed in a matter of hours. The attack sequence works in two phases:

According to the WEF Global Cybersecurity Outlook 2026, 94% of survey respondents identified AI as the most significant driver of cybersecurity change, and 87% flagged AI-related vulnerabilities as the fastest-growing cyber risk. The WEF also noted that non-human identities, meaning machine accounts, APIs, and automated services, now massively outnumber human users across banking infrastructure, expanding the attack surface well beyond what traditional security teams were built to monitor.

A defence window measured in hours rather than months means that even a bank with a strong security posture cannot guarantee patch deployment before an exploit. That is the mechanism that transforms a technical vulnerability into a potential deposit-run event.

The offence-defence asymmetry is structural rather than cyclical: Palo Alto Networks’ internal AI scan compressed five to seven years of conventional vulnerability discovery into six weeks, a data point that independently validates JPMorgan’s assessment that compressed attack timelines are now a baseline condition rather than a tail risk.

Deposit outflows following cyber incidents are not hypothetical. Empirical work on smaller U.S. banks has documented modest but persistent outflows following attacks. The open question is how those dynamics scale when the target is a systemically important institution.

The transmission pathway moves through three stages:

In JPMorgan’s analysis, the Credit Suisse collapse serves as the benchmark case for how quickly depositor confidence can unravel once a damaging narrative takes hold, with social media identified as a force capable of driving extraordinary volatility in deposit flows.

That reference is doing specific analytical work. It tells you JPMorgan is not modelling a slow credit-quality deterioration. The stress scenario here is a fast confidence collapse, closer to the 2023 regional bank episode or Credit Suisse than to the 2008 balance-sheet insolvency model. Federal Reserve simulations reinforce the point: impairment of a single large, active bank affects 31-38% of the banking network on average, not through direct losses but through payment disruption and liquidity hoarding.

The transmission pathway JPMorgan is modelling has deep historical precedent: confidence-sensitive funding, not balance-sheet insolvency, was the core mechanism in the Panic of 1907, when a contained copper trade failure nearly collapsed the entire U.S. financial system through opacity and rapid depositor withdrawal.

Recognising this confidence-channel transmission mechanism matters for how you read bank valuations. Institutions with stable, broadly distributed deposit bases represent a more defensible proposition in a world where cyber risk can trigger rapid funding outflows. Banks reliant on volatile or wholesale-heavy funding structures carry a hidden vulnerability that capital ratios do not capture.

The research identifies five dimensions investors can use to compare banks on cyber resilience. Technology spend, which accounted for roughly 17% of total operating costs across global banks on average in 2025, is a starting point but tells you little without understanding the composition and quality of that spend.

| Dimension | What to look for |

|---|---|

| Technology and cybersecurity investment quality | Spending on secure engineering, incident response, and AI-enabled detection, not just customer-facing applications |

| AI governance and operational resilience | Documented AI use cases, vendor governance, data-handling standards, and defensive AI deployment |

| Deposit base stability | Mix of retail versus wholesale deposits; behaviour of the deposit base during past stress episodes |

| Vendor and concentration risk | Exposure to shared infrastructure, critical cloud providers, and payment network nodes |

| Disclosure quality and incident history | Transparency about breaches, remediation timelines, and investment responses versus boilerplate disclosures |

Disclosure quality is an underused analytical signal. Banks that are transparent about incidents, remediation timelines, and investment responses offer more visibility into true risk posture than those with sparse or formulaic disclosures. Sparse disclosure may indicate either a low-incident history or a governance culture that obscures exposure; without standardised requirements, you cannot easily distinguish between the two.

Vendor concentration risk runs through the same governance gaps that JPMorgan’s framework highlights: APRA found that regulated entities depending on a single AI provider across multiple critical functions lack adequate exit strategies, a pattern confirmed across surveys of 628 global financial institutions and flagged independently by the BIS, ECB, and Bank of England.

Regulators in multiple jurisdictions are increasing mandatory disclosure requirements for cyber incidents, which will make this signal more comparable over time. U.S. cybersecurity venture funding reached $11.5 billion in 2025, with $4.6 billion deployed through May 2026 alone; 72% of U.S. cyber deals involved AI-enabled companies. That ecosystem proximity gives U.S. institutions earlier access to frontier defensive tools, a practical advantage that does not appear in capital ratios but does affect resilience in the scenario JPMorgan is modelling.

The JPMorgan research makes a clear case that U.S. global systemically important banks hold a structural advantage, with Abouhossein pointing to their larger absolute technology budgets and proximity to cutting-edge AI defensive tools as the primary drivers. On this basis, the analysis contends that a valuation premium over European and Japanese peers is justifiable, reflecting the market’s recognition of stronger cyber preparedness in the form of a reduced cost of equity.

Three factors drive the U.S. advantage case:

The WEF Global Cybersecurity Outlook 2026 highlights “cyber inequity” across jurisdictions, with uneven infrastructure and governance capability creating different levels of systemic resilience depending on region.

The geographic argument matters most at the tail. In a severe, AI-enabled cyber event, the institution that can detect and respond within hours has a materially different outcome than one whose detection and response cycle takes days. That capability gap aligns roughly with technology ecosystem proximity, even if it does not map cleanly onto national borders. The research itself includes a caveat worth noting: geographic advantage is directionally plausible but should not be applied as a blanket assumption across all U.S. versus non-U.S. institutions. The individual bank matters more than the postcode.

The mechanisms are confirmed. AI is compressing attack timelines. Deposit outflows follow cyber incidents. Capital frameworks lack cyber-liquidity channels. What remains an analytical judgment, rather than a measured number, is the degree to which bank valuations are mispriced as a result.

Confirmed by independent evidence:

Analytical judgment requiring further data:

The variables that would move this from a directional thesis to a measurable valuation adjustment are standardised cyber-stress test results, mandatory and comparable incident disclosures, and a larger empirical dataset on deposit behaviour at large institutions following cyber events. The IMF and the Federal Reserve have both called for integrating cyber scenarios into macro-prudential stress testing; if implemented, those frameworks would provide exactly the standardised data currently missing.

The most useful parallel is interest-rate risk before 2022. Duration risk was widely acknowledged in principle and almost entirely absent from actual position sizing, until a crystallising event forced rapid repricing. Cyber mispricing may sit in the same category today.

For investors wanting to see how a real-world prudential regulator has framed exactly this gap, our full explainer on stress testing and imported systemic risk covers how APRA’s May 2026 exercise confirmed capital buffer adequacy while simultaneously flagging AI governance and cyber disruption as risks that capital alone cannot neutralise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The degree of valuation mispricing discussed is an analytical judgment, not an empirically quantified figure, and forward-looking assessments are subject to change based on market developments and regulatory action.

Three conclusions follow from this analysis. First, capital ratios are insufficient as a standalone measure of cyber resilience; they were built for a different category of shock. Second, the five-dimension comparative framework, spanning technology investment quality, AI governance, deposit stability, vendor concentration, and disclosure transparency, gives you a practical alternative for scoring banks against the risk JPMorgan has identified. Third, geographic allocation across bank equities should weight cyber-resilience capability alongside traditional metrics, with the caveat that institution-level assessment matters more than regional averages.

The next inflection point for this thesis is regulatory adoption of standardised cyber-stress testing. When that arrives, the mispricing argument will either be confirmed with numbers or revised with better data. Until then, the mechanisms are sound, the direction is plausible, and the gap between what capital ratios capture and what AI-accelerated cyber risk demands remains wide open.

A zero-day vulnerability is a security flaw in software that the developer does not yet know exists, meaning the bank has zero days to patch it before an attacker can exploit it. AI tools have now compressed the time to discover these flaws from months to hours, turning a manageable risk into a near-instantaneous threat that can trigger deposit outflows before any remediation is possible.

Capital adequacy ratios were designed to measure a bank's ability to absorb credit losses and market drawdowns through balance-sheet arithmetic; they contain no mechanism for confidence-driven liquidity shocks caused by digital infrastructure failures. JPMorgan's research, supported by independent IMF and Federal Reserve findings, identifies payment system impairment, interbank liquidity hoarding, and depositor confidence collapse as three contagion channels that sit entirely outside the standard framework.

Federal Reserve systemic simulations found that impairment of a single large, active bank affects approximately 31-38% of the banking network on average, not through direct credit losses but through payment disruption and liquidity hoarding as surviving institutions conserve their own reserves. Forgone payment activity can exceed 2.5 times daily GDP when this hoarding dynamic takes hold.

JPMorgan's framework covers technology and cybersecurity investment quality, AI governance and operational resilience, deposit base stability, vendor and concentration risk, and disclosure quality combined with incident history. Disclosure quality is highlighted as a particularly underused analytical signal, since banks transparent about breaches and remediation timelines offer more genuine visibility into risk posture than those with formulaic or sparse disclosures.

Banks most exposed are those reliant on volatile or wholesale-heavy funding structures, with opaque cyber disclosures, high vendor concentration in shared infrastructure, and limited integration with frontier AI defensive tools. U.S. global systemically important banks are assessed as structurally better positioned than European and Japanese peers, though JPMorgan's own caveat is that institution-level assessment matters more than regional averages.