Why Central Banks Are Cutting Dollars and Stockpiling Gold

17 mins ago

A NSW Supreme Court ruling handed down on 30 June 2026 confirmed that Regional Express Holdings (Rex) had no reasonable grounds for its optimistic profit forecast from mid-April 2023 onward, yet did not tell the market until June. That puts a precise number on what a continuous disclosure failure looks like: roughly 60 days of silence while internal reality diverged from the guidance investors were relying on.

Rex no longer exists as a listed company. It entered voluntary administration in July 2024, was acquired by US-based Air T in December 2025, and restructured as a proprietary entity. But the court’s findings carry live force for every ASX-listed board and for every investor trying to read guidance announcements intelligently. Guidance is not a one-time event. It is a living commitment that generates ongoing obligations until it is revised or withdrawn.

What the case record shows is more useful than the headline verdict. Here is what the court actually found, why the director accountability split matters, and what specific signals you can use to assess whether a company’s guidance is still credible.

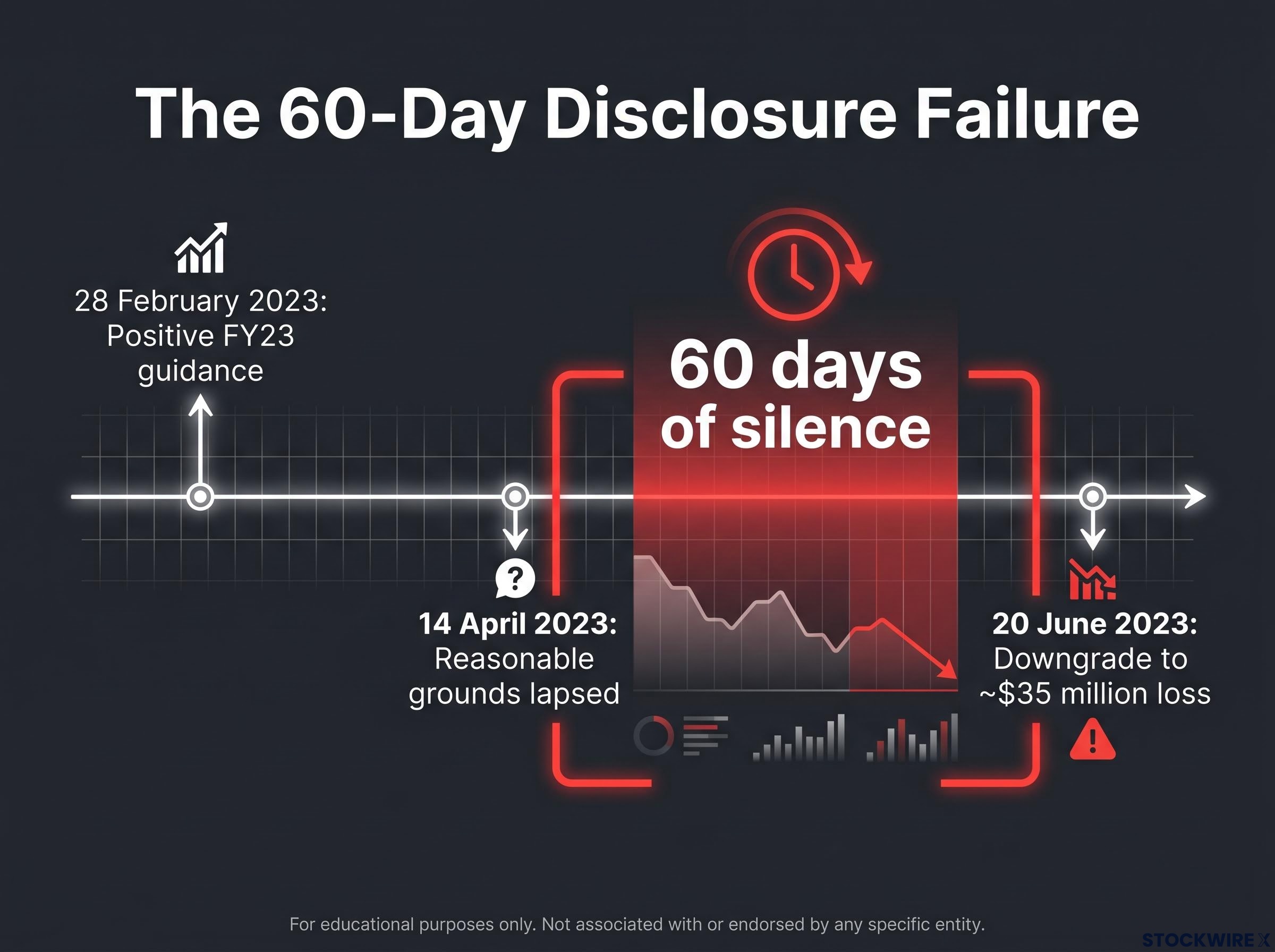

On 28 February 2023, Rex released an ASX announcement expressing optimism that the group would achieve positive operating profits for the full FY23 period. The statement was conditional, hinging on “no further external disruptions.” No formal FY23 forecast had been prepared. The tone was forward-looking, the language carefully hedged, and for the moment, it gave investors a reason to hold.

The court identified 14 April 2023 as the date when internal information had eroded any reasonable basis for that outlook. By that point, the data available to management made the positive profit expectation untenable. Rex said nothing.

Two months later, on 20 June 2023, the company announced it now expected a group operating loss of approximately $35 million for FY23. The actual reported loss came in at $31.7 million, closely tracking the downgrade estimate and confirming that the internal picture had been clear well before the market was informed.

| Event | Date | Significance |

|---|---|---|

| Optimistic profit guidance issued | 28 February 2023 | Rex told the market it expected positive FY23 operating profits, subject to no further disruptions |

| Reasonable grounds lapsed | 14 April 2023 | Court found internal data had made the positive outlook untenable from this date |

| Profit downgrade announced | 20 June 2023 | Rex disclosed an expected operating loss of ~$35 million, a reversal from positive guidance |

That two-month gap is not a procedural detail. It is the unit of harm continuous disclosure rules exist to prevent. For those 60 days, investors were trading on stale, misleading guidance while the company’s internal numbers told a different story.

The framework that Rex breached sits in two paired provisions: ASX Listing Rule 3.1 and section 674 of the Corporations Act 2001 (Cth). Together, they require a listed entity to immediately disclose any information a reasonable person would expect to have a material effect on the price or value of its securities. Narrow exceptions exist for confidentiality or insufficient certainty, but neither applied to Rex’s situation.

The framework that Rex breached sits in two paired provisions: ASX Listing Rule 3.1 and section 674 of the Corporations Act 2001 (Cth). Together, continuous disclosure obligations require a listed entity to immediately disclose any information a reasonable person would expect to have a material effect on the price or value of its securities, and narrow exemptions under Listing Rule 3.1A require all three qualifying conditions to be satisfied simultaneously, not selectively applied to manage uncomfortable announcements.

ASX Guidance Note 8 on continuous disclosure sets out the precise scope of Listing Rule 3.1 and its interaction with section 674 of the Corporations Act, including how the narrow exceptions for confidentiality and insufficient certainty are applied in practice.

Profit guidance falls squarely within this framework. Once a company has publicly committed to a particular earnings trajectory, three obligations attach:

The ongoing disclosure obligation arises from the moment guidance is issued. There is no safe harbour simply because the financial year has not yet ended.

The “reasonable grounds” standard is not frozen at the moment guidance is first released. It must be reassessed as internal data evolves. Rising losses, deteriorating cash flow, or the failure of key assumptions can progressively erode the basis for a forecast, and the law expects that erosion to be treated as disclosable information rather than “work in progress.”

The court found that Rex did not breach continuous disclosure at the moment it made the February 2023 announcement. At that point, the company had not yet accumulated the internal information that would make the positive outlook unreasonable. The rule does not prohibit optimism. It prohibits letting unrealistic optimism sit uncorrected in the market.

For you as an investor, that distinction matters. Understanding that reasonable grounds must be actively maintained means guidance silence is never neutral. When conditions visibly deteriorate and a company says nothing, the absence of an update is itself information.

Prior to the court handing down its ruling, Lim Kim Hai, the former executive chair, acknowledged every contravention alleged against him, doing so roughly six weeks ahead of the judgment. He agreed to penalties of a financial nature along with disqualification orders. A future court hearing is scheduled to determine the relief to be imposed.

For investors wanting to understand the full scope of personal exposure that executives like Lim Kim Hai face, our dedicated guide to ASIC director disqualification explains the statutory triggers under section 206F, what the ban prohibits in practice, and how to search the public register before assessing a company’s leadership risk.

Lim Kim Hai drafted and approved the key ASX announcement and failed to prevent the continuous disclosure breach. His admission stands as the clearest illustration of personal executive exposure under Australian corporate law.

The case ASIC mounted against the three former non-executive directors, The Hon John Sharp AM, Siddharth Khotkar, and Lincoln Pan, centred on whether they had fallen short of their directors’ duties in relation to the disclosure failure. The court rejected that contention and ruled in the directors’ favour, finding no personal liability was established on the evidence.

The split reflects a specific legal principle: non-executive directors are not expected to discover information that management has but does not share with them. Their liability turns on what information was actually presented to them and whether they responded to obvious red flags.

That acquittal is not a signal that board oversight is irrelevant. It is a signal that the quality and granularity of financial information flowing to the board is what will determine non-executive liability when the next case arises. Three governance implications follow directly:

ASIC’s separate misleading and deceptive conduct claim against Rex itself was also not made out.

In May 2021, Rex paid a $66,000 infringement notice penalty for a separate alleged continuous disclosure breach (ASIC media release 21-105MR, 18 May 2021). Infringement notices are not findings of guilt under Australian law. But they do signal that disclosure controls have attracted regulatory scrutiny.

What followed was a company with a flagged disclosure weakness that did not demonstrably strengthen its processes before the 2023 events. By the time the later matter reached the courts, Rex had already entered voluntary administration, which meant civil penalties against the company were no longer pursued.

A prior infringement notice in the disclosure space followed by a more serious breach that ends in court is precisely the type of escalating regulatory pattern you can identify using public records before committing capital. Three steps make this practical:

ASIC enforcement escalation across multiple disclosure categories, from missing annual reports to profit guidance failures, reflects a deliberate 2026 regulatory priority to pursue listed companies that allow governance processes to slip; investors who wait for formal enforcement action before reassessing a position may find liquidity in small-cap stocks already severely constrained by the time a penalty is announced.

Rex’s arc from guidance to administration moved faster than most investors expect:

Ordinary shareholders sit at the bottom of the recovery waterfall in administration. That makes the early warning signals in this sequence, particularly the prior notice and the two-month silence, worth understanding before a similar pattern appears in another name.

Rex’s February 2023 guidance was expressly conditional on “no further external disruptions.” Those conditions failed quickly. The gap between the lapse of reasonable grounds (mid-April) and the market update (20 June 2023) is the investor harm window: the period when you are exposed to a risk the company knows about but has not disclosed.

Several observable signals should prompt you to reassess a company’s guidance credibility:

Guidance is conditional and dynamic. Silence during deteriorating conditions is not reassurance; it is a disclosure risk flag that should prompt a reassessment of position sizing.

The Rex case gives you a specific mental model. When a company with positive guidance goes quiet while observable conditions deteriorate, that silence is the signal. Months of silence followed by a sudden, sharp downgrade is the pattern the court has now examined, measured, and penalised. You can watch for it before the court gets involved.

The ruling’s central implication is that the “reasonable grounds” standard is a continuous, evolving obligation, not a threshold crossed once at the time of initial guidance. The court’s decision, issued 30 June 2026, sets a marker that listed companies and their advisers will reference for years.

Misleading market representations carry liability even when the company making them is the exchange itself, as ASX demonstrated when it paid $20.5 million in penalties after admitting its ‘progressing well’ characterisation of the CHESS replacement project was inaccurate, a ruling that sits alongside the Rex outcome as evidence that the disclosure standard applies uniformly across the market ecosystem.

Three governance practices are now non-negotiable for any ASX-listed entity issuing earnings guidance:

Lim Kim Hai’s penalty and disqualification orders remain to be determined at a future hearing. Rex itself was acquired by Air T on 18 December 2025 and restructured as a proprietary company, ending its existence as a listed entity. The full arc, prior notice, serious breach, administration, delisting, is an extreme outcome. But the disclosure failure at its centre is one that any listed company with lax guidance processes could replicate.

For you as an investor, the ruling confirms that continuous disclosure enforcement is active and consequential. It produces personal liability for executives, it reaches the highest levels of company leadership, and it will be examined against a precise timeline when something goes wrong.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A continuous disclosure breach occurs when a listed company fails to immediately disclose information that a reasonable person would expect to materially affect the price or value of its securities. Under ASX Listing Rule 3.1 and section 674 of the Corporations Act, this includes failing to update or withdraw profit guidance when the reasonable basis for that guidance has lapsed.

The NSW Supreme Court found that from 14 April 2023, Rex had no reasonable grounds for its optimistic profit guidance issued in February 2023, yet waited until 20 June 2023 to disclose an expected $35 million operating loss, creating a 60-day window in which investors traded on stale, misleading guidance.

Lim Kim Hai, as executive chair, drafted and approved the key ASX announcement and failed to prevent the breach, so his personal liability was clear and he admitted every contravention. The non-executive directors were acquitted because their liability depended on what information management actually presented to them, and the court found no evidence they received or ignored the internal data that made the guidance untenable.

Watch for sector-wide headwinds that directly undermine stated guidance assumptions, quarterly results running below the implied guidance run-rate with no update, prolonged company silence on known operational stresses, and any prior ASIC infringement notices or disclosure-related enforcement action searchable through ASIC's media release archive.

Rex entered voluntary administration in July 2024, roughly 13 months after its profit downgrade, and was subsequently acquired by US-based Air T in December 2025 and restructured as a proprietary company. Ordinary shareholders rank at the bottom of the recovery waterfall in administration, meaning the extended silence before the downgrade directly affected the window investors had to reassess or exit their positions.