JB Hi-Fi’s 27% Drop: What the Financials Actually Show

12 mins ago

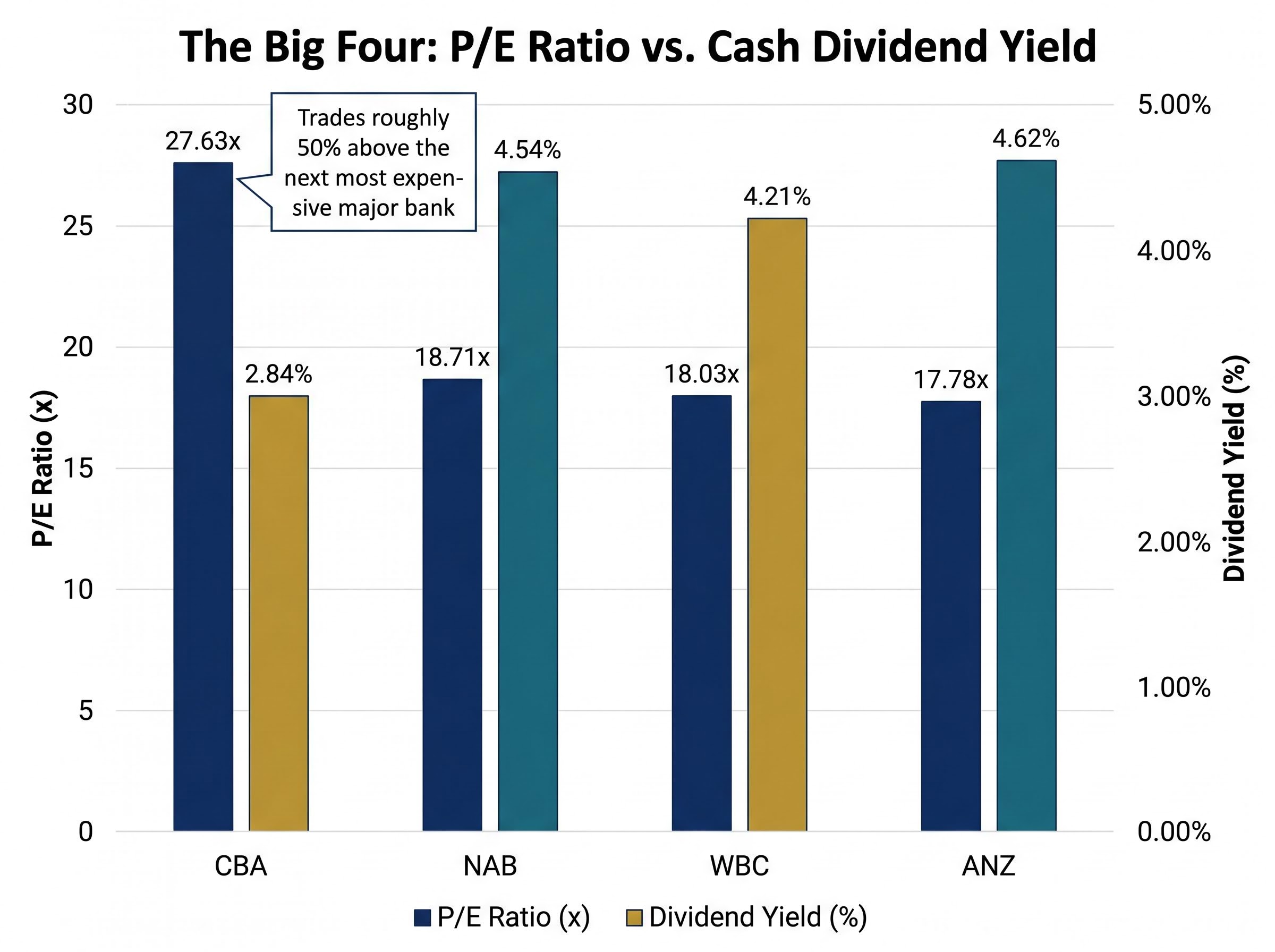

Commonwealth Bank of Australia closed at A$171.57 on 13 May 2026, trading at 27.63x earnings while its big four peers sit between 17.78x and 18.71x. That valuation gap is so persistent that no major broker has issued a buy rating on CBA since 2022. Against an analyst consensus price target of A$125.95, implying roughly 27% downside, and a forward dividend yield of just 2.84%, the question for new investors is not whether CBA is a quality business. It clearly is. The question is whether the entry price today makes sense relative to what income and growth the shares can realistically deliver. This analysis walks through the valuation mechanics, the income trade-off, the macro headwinds introduced by the 2026 Federal Budget, and the peer alternatives available on the ASX right now, giving readers a structured framework for deciding whether to buy, rotate, or wait.

At A$171.57, CBA commands a market capitalisation of A$286.886 billion and a price-to-earnings ratio of 27.63x. That multiple is not just high in absolute terms; it represents a decision the market has made. Buying CBA at this level implies the bank must sustain significantly higher earnings quality or growth than its peers to justify the gap.

The P/E comparison across the big four makes the premium concrete:

That is not a modest difference. CBA trades at roughly 50% above the next most expensive major bank.

The analyst consensus 12-month price target for CBA sits at A$125.95, implying approximately 27% downside from the current price. No major broker has issued a buy rating since 2022.

Past performance does not change today’s entry price. For a new investor, the question is forward-looking: what income and capital return can CBA deliver from A$171.57, and does that compensate for the premium being paid?

Many retail investors associate CBA with reliable income. At A$171.57, however, the forward dividend yield is 2.84%, based on trailing twelve-month dividends of A$4.95 per share.

That A$4.95 comprises the A$2.35 fully franked interim dividend for FY26 (a 4.44% increase on the FY25 interim of A$2.25) and the A$2.60 FY25 final dividend. The FY26 final dividend has an ex-date of 19 August 2026 and a pay date of 29 September 2026, but the amount has not yet been confirmed.

How does that yield compare across the big four?

| Bank | Share Price | P/E Ratio | Dividend Yield (Cash) | Grossed-Up Yield (Approx.) |

|---|---|---|---|---|

| CBA | A$171.57 | 27.63x | 2.84% | ~4.0% |

| ANZ | A$35.03 | 17.78x | 4.62% | ~6.6% |

| NAB | A$37.42 | 18.71x | 4.54% | ~6.5% |

| WBC | A$36.61 | 18.03x | 4.21% | ~6.0% |

The yield gap between CBA and its peers ranges from approximately 140 to 180 basis points on a cash basis. For a dividend-focused investor deploying a six-figure position, that difference is material.

CBA’s dividends are fully franked, which boosts the effective gross yield to approximately 4% or above for Australian resident taxpayers, reflecting the 30% corporate tax rate already paid. That is a genuine advantage for income investors.

However, ANZ, NAB, and Westpac also pay substantially franked dividends. The franking credit benefit is not exclusive to CBA. Even on a grossed-up basis, CBA’s effective yield remains the lowest of the four major banks by a meaningful margin.

CBA has historically commanded a valuation premium for legitimate reasons. It has delivered superior return on equity among the big four, built a widely regarded digital banking platform, maintained the lowest credit loss rates, and produced the most consistent record of fully franked dividend growth.

Those qualities deserve recognition. The question is whether today’s price reflects those advantages or has moved beyond them.

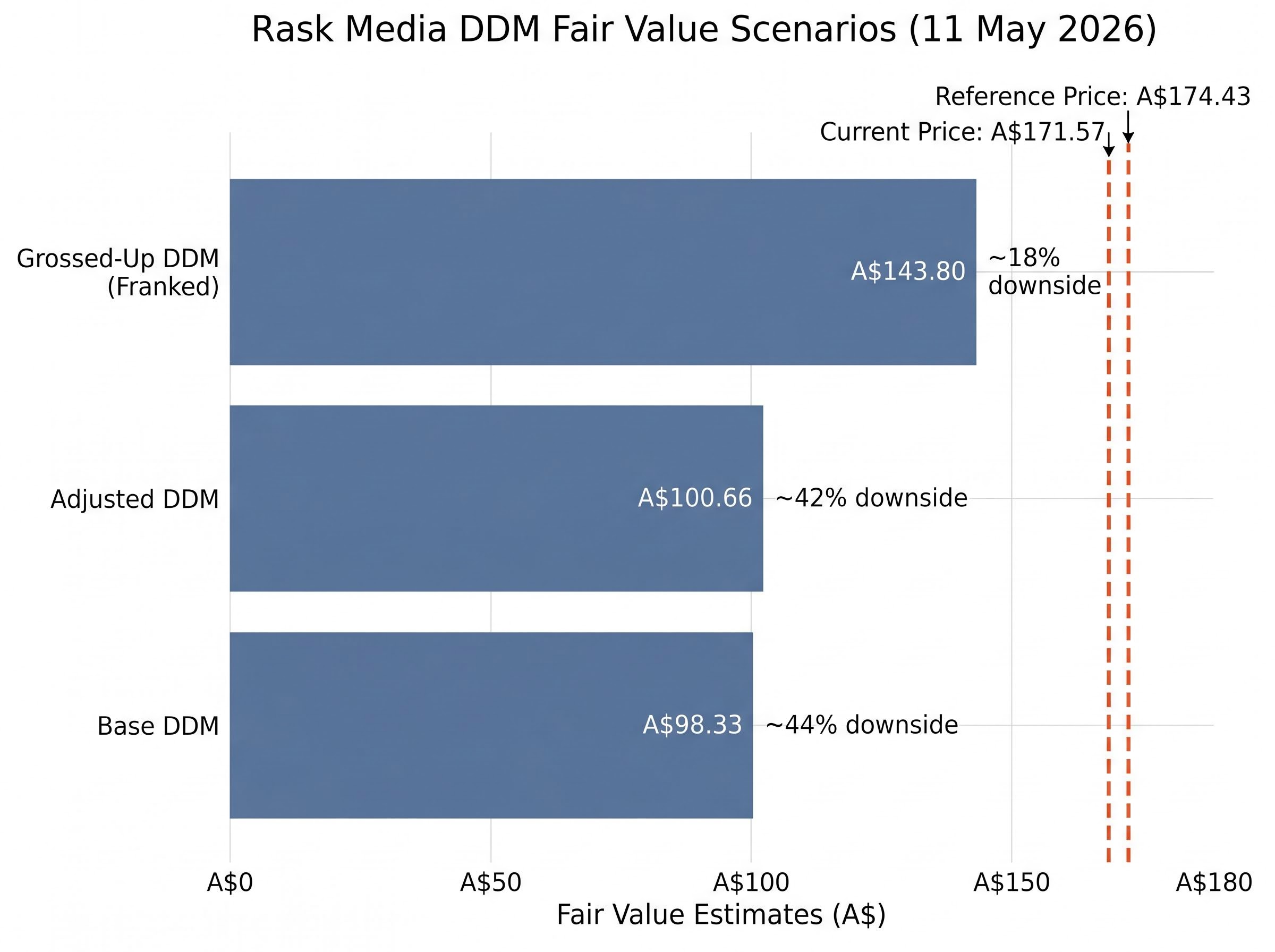

A dividend discount model (DDM) analysis published by Rask Media on 11 May 2026 (using A$174.43 as the reference price) tested three scenarios:

| Scenario | Dividend Assumption | Fair Value Estimate | Implied Downside from A$174.43 |

|---|---|---|---|

| Base DDM | A$4.65 | A$98.33 | ~44% |

| Adjusted DDM | A$4.76 | A$100.66 | ~42% |

| Grossed-Up DDM (Franked) | A$6.80 (effective) | A$143.80 | ~18% |

Even under the most favourable scenario, which accounts for the full value of franking credits, the DDM fair value estimate of A$143.80 sits approximately 16% below CBA’s current price of A$171.57.

CBA’s H1 FY26 cash net profit after tax came in at A$5.445 billion, a verified figure from the February 2026 half-year results. On the credit quality front, personal loan arrears climbed to 1.71% in Q3 FY26 (according to Rask Media reporting; this figure could not be independently verified against a primary CommBank release), while home loan and credit card arrears beyond 90 days held steady at approximately 0.7%.

One quarter of rising personal arrears does not constitute a trend. It does, however, warrant monitoring, particularly in a rate environment where household borrowing costs remain elevated.

The 2026-27 Federal Budget, announced around 12-13 May 2026, contains several measures with direct implications for bank lending growth:

These are not minor adjustments. Investor property lending has been a core growth channel for all four major banks, and policy changes that structurally reduce that demand represent a multi-year headwind, not a single-quarter disruption.

The transmission mechanism is straightforward. Fewer investor property loans mean lower net interest income growth across all four majors. Business lending growth at CBA reached a strong pace in Q3 FY26, according to Rask Media reporting (a primary CommBank release for this figure could not be independently located). Loan impairment expense for the same quarter was elevated, attributed to geopolitical and macroeconomic uncertainty (this figure could not be independently verified against a primary CommBank release).

CBA, trading at the highest P/E multiple among the big four, has the least valuation cushion if earnings growth moderates. A bank priced at 27.63x earnings needs to deliver meaningfully stronger growth than one priced at 18x to justify the premium. If investor lending volumes decline across FY27, that growth gap becomes harder to sustain.

These statements are speculative and subject to change based on market developments and company performance.

For investors whose primary objective is income, the big four peers and at least one diversified ETF offer materially higher yields at lower valuations. The following is structured as general financial information, not personal advice.

All three peer banks pay substantially franked dividends, meaning the franking credit advantage that partially closes CBA’s yield gap is available across the alternatives as well.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Three findings run through this analysis. CBA’s 27.63x P/E sits roughly 50% above its big four peers. Its 2.84% cash yield (approximately 4% grossed-up) trails the peer range of 4.21% to 4.62%, even after accounting for franking. And the 2026 Federal Budget introduces structural headwinds to investor lending that may weigh on earnings growth entering FY27.

For income-focused investors evaluating any large-cap bank stock, three levers provide a repeatable decision framework:

The distinction between an existing long-term holder and a new investor matters here. A shareholder who entered CBA years ago benefits from a lower cost basis and compounded returns. A new investor entering at A$171.57 faces a different equation: a lower starting yield, a wider valuation gap, and emerging policy headwinds.

The analyst consensus price target of A$125.95 serves as a reference point, not a prediction. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors. Readers should seek personal financial advice before making investment decisions.

CBA trades at a P/E ratio of 27.63x, which is roughly 50% above its big four peers: NAB at 18.71x, Westpac at 18.03x, and ANZ at 17.78x, as of May 2026.

At A$171.57, CBA offers a forward dividend yield of approximately 2.84% on a cash basis, or around 4% on a grossed-up basis once franking credits are accounted for, the lowest of the four major Australian banks.

The 2026-27 Federal Budget introduced a negative gearing wind-back and capital gains tax changes that are expected to reduce investor property lending demand, a core growth channel for all major banks, representing a multi-year headwind to earnings growth entering FY27.

The analyst consensus 12-month price target for CBA is A$125.95, implying approximately 27% downside from the May 2026 price of A$171.57, and no major broker has issued a buy rating on CBA since 2022.

ANZ offers a forward yield of 4.62%, NAB offers 4.54%, and Westpac offers 4.21%, all of which are materially higher than CBA's 2.84% cash yield, and all three pay substantially franked dividends.