Eli Lilly at 40x Earnings: Expensive Stock, Underpenetrated Market

1 hr ago

Berkshire Hathaway carries just under $300 billion in liabilities on its balance sheet that most analysts do not treat as debt. They are right not to. These are not bonds maturing next quarter or credit facilities with covenant triggers. They are insurance float and deferred tax liabilities, two funding sources that behave nothing like conventional borrowing despite occupying the same side of the ledger.

The distinction matters because it changes how you read the entire business. Berkshire’s structure is frequently described in broad strokes but rarely explained at the mechanical level. If you understand how float and deferred tax liabilities actually function, you gain a materially different view of how the company compounds capital, and why standard debt-adjusted valuation models can systematically misread it.

Here is the framework for identifying which liabilities on Berkshire’s balance sheet are funding the investment machine rather than constraining it, and why that architecture is almost impossible to replicate from scratch.

A straightforward reading of Berkshire’s liability column produces a number close to $300 billion in combined insurance float and deferred tax liabilities. On paper, that looks like a company carrying an enormous debt burden against approximately $700 billion in total investment assets, including roughly $400 billion in cash and Treasury securities (approximately 40% of its market capitalisation).

The standard reading misses something fundamental. Neither of these liability categories carries the economic characteristics that make conventional debt dangerous:

If you deduct these at face value from equity as though they were near-term interest-bearing debt, you are making a category error about what they actually cost and when they come due.

The distinction between a liability that constrains a business and one that funds it sits at the heart of value investing risk, which experienced practitioners define not as price volatility but as the probability of permanent capital loss on the underlying business, a framing that makes the float and DTL debate immediately legible.

The FASB insurance accounting standards that govern how loss reserves and unearned premiums are recorded require insurers to carry these obligations at their nominal undiscounted value on the balance sheet, which is precisely why the liability column overstates the economic burden of float for long-tail writers whose claims settle over many years.

When you buy an insurance policy, you pay the premium upfront. The insurer then holds that money until a claim is filed and settled, which could be months or decades later depending on the type of coverage. The pool of capital that sits between premium collection and claims payment is called insurance float: loss reserves, unearned premiums, and related insurance liabilities that policyholders effectively lend to the insurer.

The combined ratio tells you whether that float was free or costly. The combined ratio is total claims and expenses divided by total premiums. Above 100%, the insurer lost money on underwriting and paid for the privilege of holding the float. Below 100%, the insurer made a profit on the insurance itself before any investment income, meaning the float carried a negative cost.

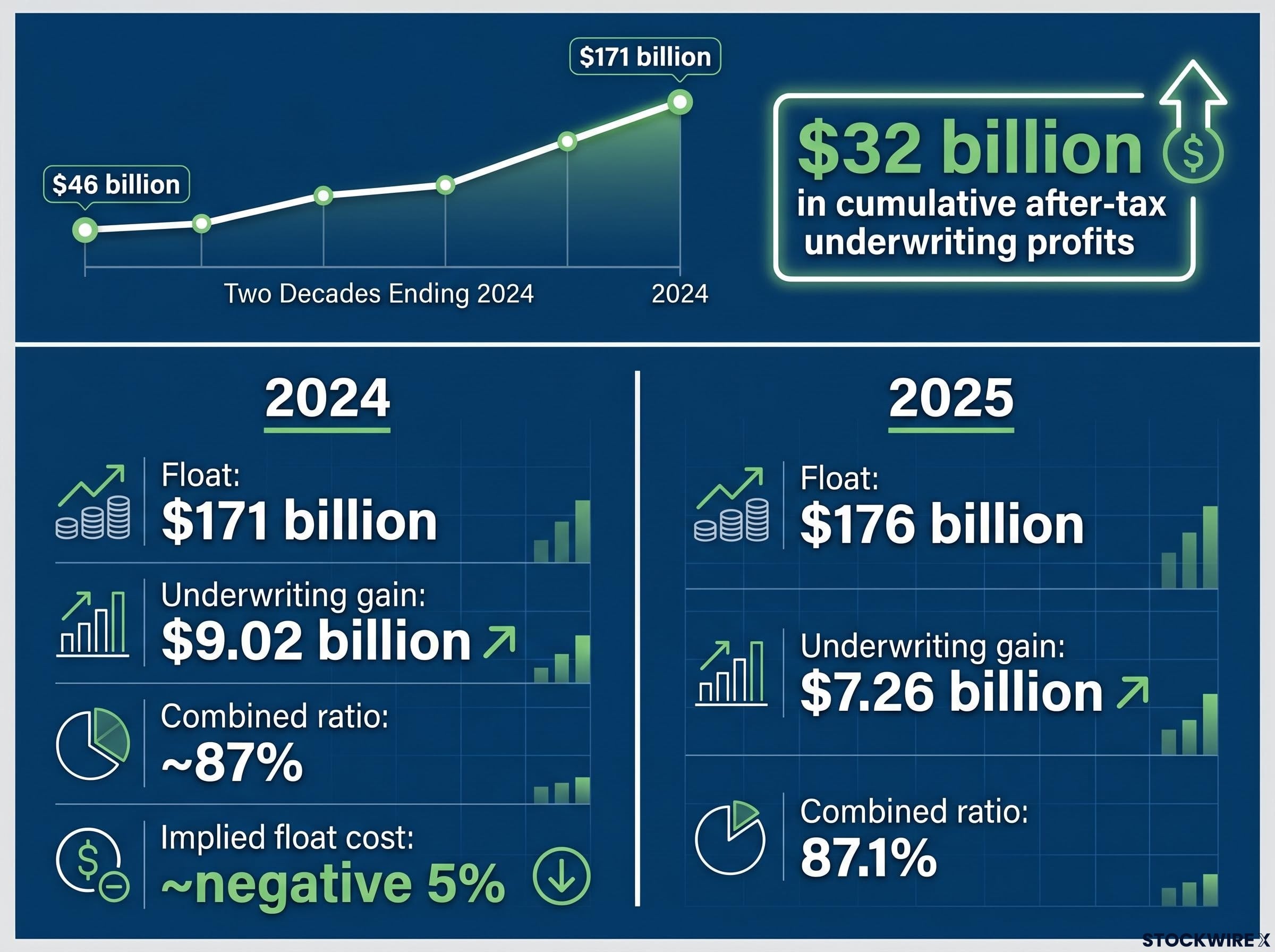

Berkshire has operated well below that threshold. In 2024, the combined ratio sat at approximately 87%, producing an underwriting gain of $9.02 billion on float of $171 billion. That implies an effective float cost of approximately negative 5%: policyholders were essentially paying Berkshire to hold their money before it was deployed into investments.

| Year | Float balance | Underwriting gain | Combined ratio | Implied float cost |

|---|---|---|---|---|

| 2024 | $171 billion | $9.02 billion | ~87% | ~negative 5% |

| 2025 | $176 billion | $7.26 billion | 87.1% | Negative (profitable) |

A negative cost of float means Berkshire is being paid to hold policyholders’ money before investing it. That is structurally different from any conventional borrowing arrangement and explains why float at scale is one of the most powerful funding mechanisms in corporate finance.

Not all float is equal. Short-tail lines like basic auto insurance generate float that turns over within months as claims settle quickly. Long-tail lines, such as workers’ compensation and catastrophe reinsurance, generate float that can persist for years or decades before claims are paid. The longer the insurer holds the money, the longer it can compound investment returns. Over two decades ending 2024, Berkshire’s float grew from $46 billion to $171 billion, and insurance operations generated $32 billion in cumulative after-tax underwriting profits. That is not a business subsidising its investment portfolio with underwriting losses. It is a business being paid to hold the capital that funds it.

By Q1 2026, float had grown to $176 billion and the record cash reserve had reached $397 billion, roughly 40% of Berkshire’s market capitalisation, a figure that reflects decades of compounding the underwriting profits and investment returns described in this section rather than any single year’s performance.

Berkshire’s 2025 combined ratio of 87.1% confirmed that the insurance operation remained profitable on an underwriting basis for the year, with float rising to $176 billion even as underwriting gains moderated to $7.26 billion from the prior year’s $9.02 billion, illustrating how the float pool can grow while still generating a negative cost of capital.

Berkshire is widely considered the most financially strong insurer in the world. That strength is not a passive feature; it actively generates deal flow that weaker competitors cannot access.

Large corporations and counterparties needing bespoke, catastrophic cover frequently find only a handful of insurers with the capital and reputation to take the risk at scale. Berkshire is almost always on the shortlist. This opens float streams from very large, long-dated policies and reinsurance treaties that are structurally inaccessible to smaller or less capitalised insurers.

The dynamic compounds on itself:

Warren Buffett and Charlie Munger explicitly pursued this strategy, expanding into long-tail reinsurance and specialty lines specifically to lengthen the duration of Berkshire’s float. The logic was straightforward: every additional year the float sits uninvested by claims is another year of compounding.

A recent arrangement with Tokyo Marine illustrated the reputational premium attached to Berkshire partnerships; Tokyo Marine’s share price rose approximately 20% on the announcement. That is not just a data point. It tells you that Berkshire’s reputational capital is itself an asset generating deal flow and float access that no competitor can replicate regardless of their own financial strength.

Most insurers invest their float conservatively in bonds or cash. Berkshire shifted to investing more of its float into equities and operating businesses, increasing the upside from the structural leverage. That combination of disciplined, profitable underwriting and aggressive capital deployment is what separates Berkshire’s float from every other insurer’s.

When Berkshire buys a stock, the purchase price is recorded on the balance sheet. If the stock appreciates, Berkshire records the higher fair value. The difference between the purchase price and today’s value represents an unrealised gain, and under GAAP (Generally Accepted Accounting Principles, the standard accounting rules public companies follow), Berkshire must record the tax it would owe on that gain if it sold today as a deferred tax liability (DTL).

The critical word is “if.” No cash leaves the business until Berkshire actually sells the asset. For positions held across decades, the DTL sits on the balance sheet growing alongside the portfolio’s appreciation, functioning as a source of invested capital rather than a near-term obligation.

Four properties make deferred tax liabilities behave as quasi-permanent capital:

A tax bill due in 20-30 years, discounted at any reasonable rate, is materially less burdensome than its nominal figure on the balance sheet. Analysts who treat it as an immediate, full-face-value obligation equivalent to near-term debt are overstating the economic cost of Berkshire’s capital structure.

If Berkshire holds Apple for another decade and the stock doubles, the DTL grows alongside it, but no cash leaves the building. The liability is simultaneously expanding on paper and continuing to fund an investment that more than covers the eventual tax cost. This is why experienced analysts discount the DTL rather than deducting it at face value when valuing the business.

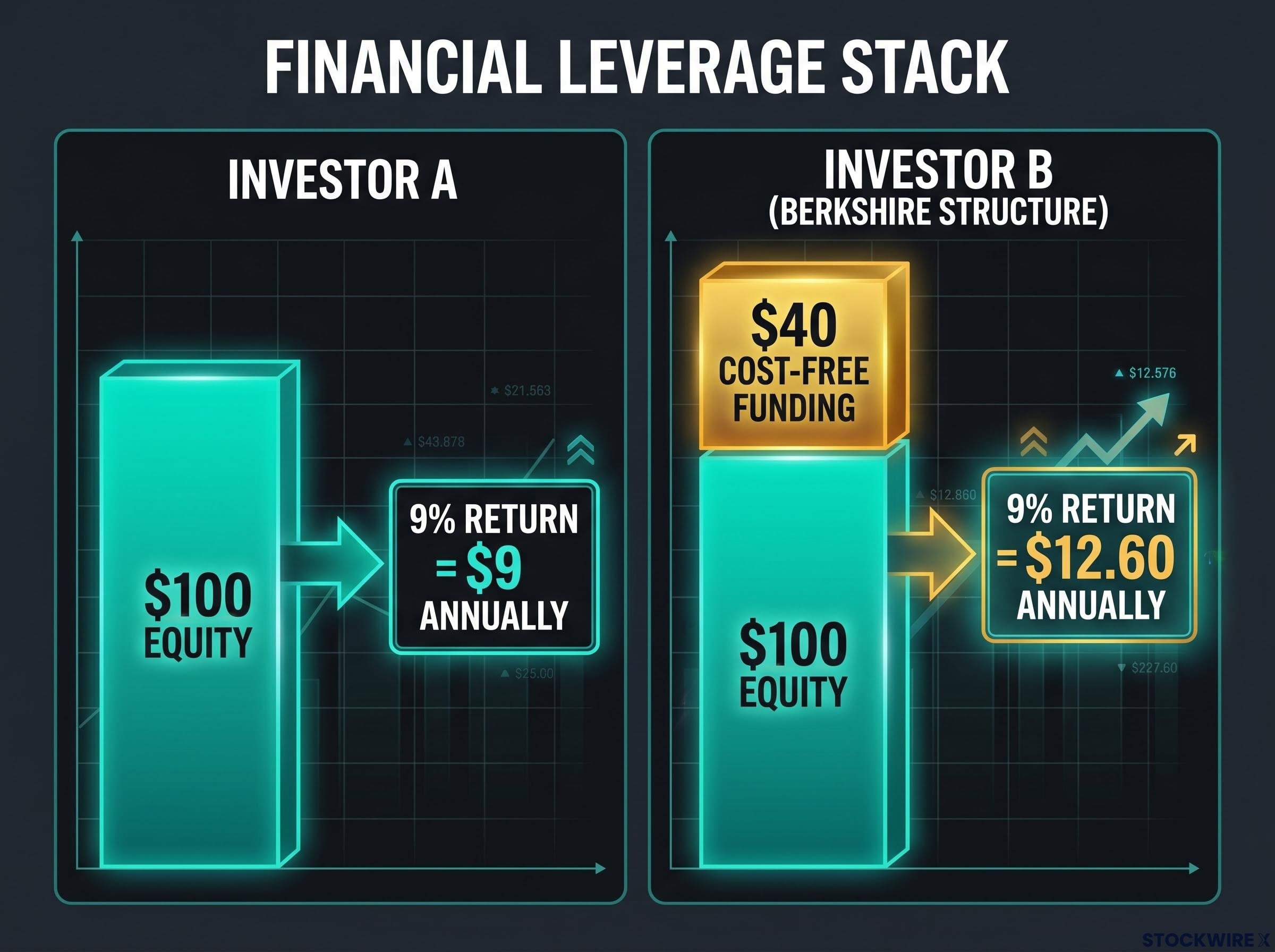

Bring the two mechanisms together and the arithmetic of structural leverage becomes visible. Berkshire’s funding stack looks like this: shareholder equity, plus insurance float (often at negative cost), plus deferred tax liabilities (zero interest, management-controlled timing), funding a portfolio of equities, operating businesses, cash, and Treasuries.

The economic advantage is best illustrated with a direct comparison:

Same portfolio return. Materially different return on equity. And critically, the $40 of cost-free funding carries none of the fragility normally associated with leverage: no fixed maturity, no covenants, no refinancing risk, no interest expense.

| Feature | Insurance float | Deferred tax liabilities | Conventional debt |

|---|---|---|---|

| Interest / cost | Often negative (paid to hold) | None | Fixed positive coupon |

| Maturity | No fixed date; renewed via premiums | Triggered only by asset sale | Fixed contractual date |

| Covenants | None | None | Leverage tests, restrictions |

| Funding stability | Long-tail lines persist for decades | Grows with portfolio appreciation | Must be refinanced on schedule |

| Management control | High; driven by underwriting discipline | High; Berkshire controls sale timing | Low; contractual obligations fixed |

The leverage stack means that even in years when Berkshire’s portfolio performs only modestly, the structural cost advantage of its funding sources provides a return-on-equity uplift that a purely equity-funded investor cannot access without taking on conventional debt risk.

If the structure is so advantageous, the natural question is: why doesn’t every large insurer replicate it?

The answer is that both engines are path-dependent. They are the product of decades of accumulated advantages, not capabilities available off the shelf.

The float engine requires three things that are exceptionally difficult to assemble simultaneously:

The deferred tax engine is equally path-dependent. The largest DTLs come from positions bought many years ago at low prices and held through major appreciation. No business entering the market today could build a comparable DTL profile without first spending decades compounding its capital base. And the holding periods required demand a corporate culture and shareholder base comfortable with extreme patience, a governance structure Berkshire built over half a century.

The conglomerate structure itself plays an enabling role. Unlike most listed companies, Berkshire faces minimal institutional pressure to distribute or recycle its cash hoard. That is unusual. Most conglomerates have underperformed or been broken up; Berkshire’s specific combination of float-funded capital deployment and a long-term ownership philosophy is what makes the structure work where others have failed. Individual operating businesses within it, such as the Class One railroad network (a natural monopoly on its routes that could not be economically replicated), compound the advantage further.

Whether that culture survives a leadership transition is a live question for investors, and Greg Abel’s first year as CEO has begun to reveal how closely his capital allocation philosophy mirrors the discipline described here, including a stated framework of acquisitions, organic growth, and disciplined repurchases that preserves the core float-and-patience structure.

For you as a reader evaluating Berkshire, the implication is not that this approach is a model to copy. It is that the structural cost-of-capital advantage should be treated as a durable feature of the business when assessing its long-run compounding capacity, precisely because it cannot be arbitraged away by new entrants.

Insurance float should be analysed through the combined ratio and long-tail risk profile, not deducted mechanically as if it were interest-bearing debt. Deferred tax liabilities should be discounted for timing and treated as part of the long-run tax drag on portfolio returns, not as immediate, face-value obligations equivalent to near-term borrowings.

Neither liability is fictional. Float will eventually be drawn down to meet claims, and taxes on realised gains will need to be settled. But because Berkshire controls the timing and has historically achieved profitable underwriting and long holding periods, these liabilities function as structural, largely cost-free leverage that amplifies returns on equity without the fragility normally associated with high debt loads.

The core insight in its most precise form: Berkshire’s structural advantage is the ability to fund a very large investment portfolio with capital that carries zero or negative cost, no fixed maturity, and no covenants, built over decades from a specific combination of insurance platform, investment culture, and accumulated history that is not replicable from a standing start.

When you evaluate Berkshire or any insurance-heavy investment holding company, the analytical work begins with identifying the true cost and duration of its funding sources, not with reading the liability column at face value. You now hold a framework for distinguishing between liabilities that constrain a business and liabilities that fund it, and that distinction applies well beyond a single company’s balance sheet.

Investors who want to see this capital deployment machine in action can follow our full coverage of Berkshire’s Taylor Morrison acquisition, an $8.5 billion all-cash deal that illustrates how the float-funded cash reserve described throughout this article gets converted into operating businesses at valuations the board assesses as below intrinsic value.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Insurance float is the pool of capital Berkshire holds between collecting premiums and paying out claims. Because Berkshire earns underwriting profits on top of holding this capital, the float often carries a negative cost, meaning policyholders effectively pay Berkshire to hold their money before it is deployed into investments.

Berkshire's combined ratio was approximately 87% in 2024, producing an underwriting gain of $9.02 billion on float of $171 billion, and 87.1% in 2025, with float growing to $176 billion and underwriting gains of $7.26 billion, confirming the insurance operation remained profitable on an underwriting basis in both years.

No. Deferred tax liabilities carry no interest charge, no fixed maturity date, and no covenants; they are only triggered when Berkshire chooses to sell the underlying asset. For positions held over decades, these obligations function as quasi-permanent, zero-cost capital rather than near-term debt obligations.

Berkshire's float advantage depends on three things that are extremely difficult to assemble simultaneously: the financial strength to underwrite large, long-dated bespoke risks; a disciplined underwriting culture sustained across cycles; and the capital allocation capability to deploy float into equities and operating businesses rather than just bonds. Building that combination took decades and is path-dependent, not something a new entrant can construct from a standing start.

Berkshire funds its investment portfolio with shareholder equity plus insurance float (often at negative cost) plus deferred tax liabilities (zero interest, management-controlled timing), which means the same underlying portfolio return produces a materially higher return on equity than a purely equity-funded investor would achieve, without the fixed maturities, covenants, or refinancing risk that make conventional leverage fragile.