Why Australia’s Rising Index Is Hiding a Market Under Stress

15 mins ago

The ASX could rise 50% under Australia’s proposed capital gains tax reforms, and that number would tell you almost nothing about whether the policy is working. The headline index is a blunt instrument. What matters is what sits underneath it: which sectors are absorbing the capital, which are losing it, and whether the economy’s capacity to produce the next generation of growth companies is being quietly hollowed out.

The Treasury Laws Amendment (Tax Reform No.1) Bill 2026 passed the House of Representatives on 4 June 2026 and is now under Senate inquiry, with reforms set to apply to gains from 1 July 2027. The public debate has centred on fairness. This analysis asks a different question: what happens to the composition of the Australian economy when the tax system structurally rewards income over growth?

What follows maps a two-stage mechanism, capital rotation first, then passive amplification, and identifies the sectors and signals worth watching as the new regime takes shape. This is analytical scaffolding, not a forecast.

The mechanics are worth walking through step by step, because the conclusion they produce is not intuitive until you see the full chain.

Under the current system, an investor who holds an asset for more than 12 months receives a 50% capital gains tax discount. The proposed regime replaces that discount with inflation-based indexation of the cost base and applies a minimum 30% tax on the real (inflation-adjusted) gain. For an investor in a high-growth company whose payoff arrives as a single capital gain years into the future, the effective tax rate on that gain rises materially.

The CGT indexation mechanics replacing the 50% discount operate differently depending on an investor’s income bracket, the inflation environment during the holding period, and the length of time the asset was held; investors who accumulated positions during the high-inflation years of 2022-2024 may face a lower effective burden under the new rules than those with long-held gains from the pre-inflation era.

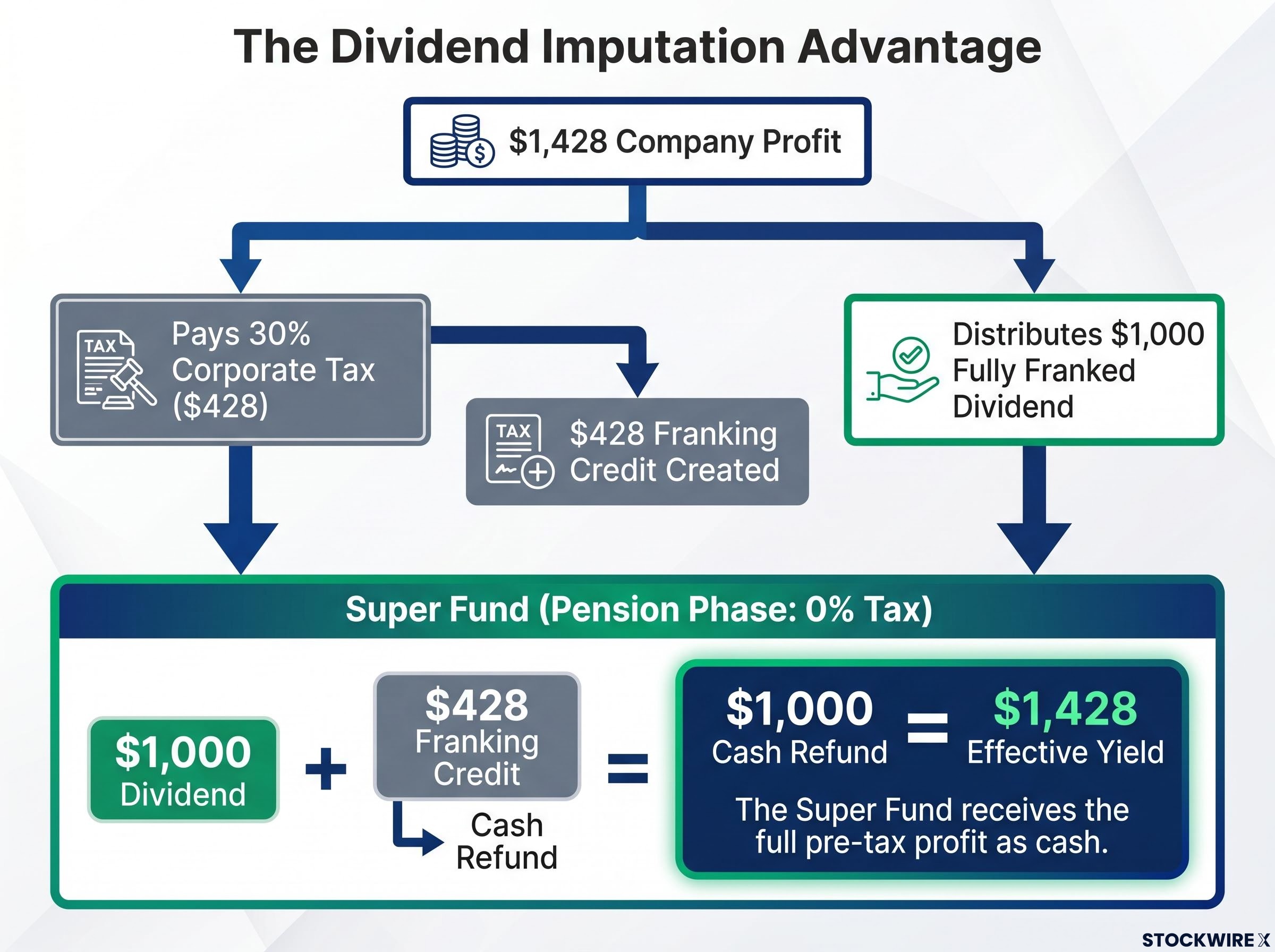

Now contrast that with what Australia’s dividend imputation system already does. Fully franked dividends from mature companies carry franking credits that offset the shareholder’s personal tax liability, making them unusually attractive on an after-tax basis. The CGT changes compound that existing asymmetry. They raise the cost of chasing capital gains while leaving the imputation advantage untouched.

The penalty falls hardest where returns are distant and speculative: biotech milestones, software exits, critical minerals discoveries. These investments pay off almost entirely through capital gains. There is no dividend stream to cushion the tax treatment.

A tapered CGT alternative, modelled on a $100,000 portfolio earning 10% annually, produces a tax bill more than $104,000 lower than the government’s indexation-plus-floor approach over 20 years, illustrating why the structural shape of the discount matters as much as its headline size.

The three categories of investor most exposed:

The Australian Industry Group notes that even with recent adjustments, the changes “lessen but don’t eliminate harm to investment.”

Steve Torso of Wholesale Investor warns the overhaul could “materially worsen outcomes” for founders and early-stage investors. The structural logic supports that concern. These reforms do not simply change a tax rate. They reprice the risk-reward calculation for every Australian investor deciding between a growth company and a dividend-paying incumbent.

The ASX’s current composition already reflects this dynamic before the reforms have taken effect. Major banks, BHP, REITs, supermarkets, and infrastructure companies hold dominant positions in the index. The rotation the CGT changes are likely to produce is not a new phenomenon; it is an intensification of a concentration that was already present.

ASX sector rotation toward fully franked dividend payers, including the major banks and diversified miners, is not simply a behavioural response to a tax change; it reflects a structural derating of the after-tax premium that growth and biotech valuations had priced in under the 50% discount regime.

| Sectors positioned to attract capital inflows | Sectors at structural disadvantage under the new regime |

|---|---|

| Major banks (fully franked dividends, dominant index weight) | Biotechnology (returns realised almost entirely as capital gains) |

| Utilities (stable income, franking credits) | Enterprise software (long development cycles, exit-dependent payoff) |

| Toll road operators and infrastructure (regulated cash flows) | Critical minerals juniors (exploration risk, distant capital gain) |

| REITs (income distribution mandates) | Deep tech ventures (pre-revenue, speculative exit horizons) |

| Supermarket chains (defensive earnings, consistent dividends) | Early-stage clean energy (capital-intensive, gain-dependent returns) |

The Centre for Independent Studies argues that higher effective CGT reduces investment, slows growth, and lowers productivity by making risky, long-horizon projects less attractive. That argument gains force when you look at the international context.

Under the US Inflation Reduction Act, the Section 45X Advanced Manufacturing Production Credit provides explicit incentives for critical minerals investment, covering lithium, cobalt, nickel, and rare earths, with no phase-out until after 2030. Allied nations are actively directing capital toward the sectors Australia’s CGT settings risk structurally disadvantaging.

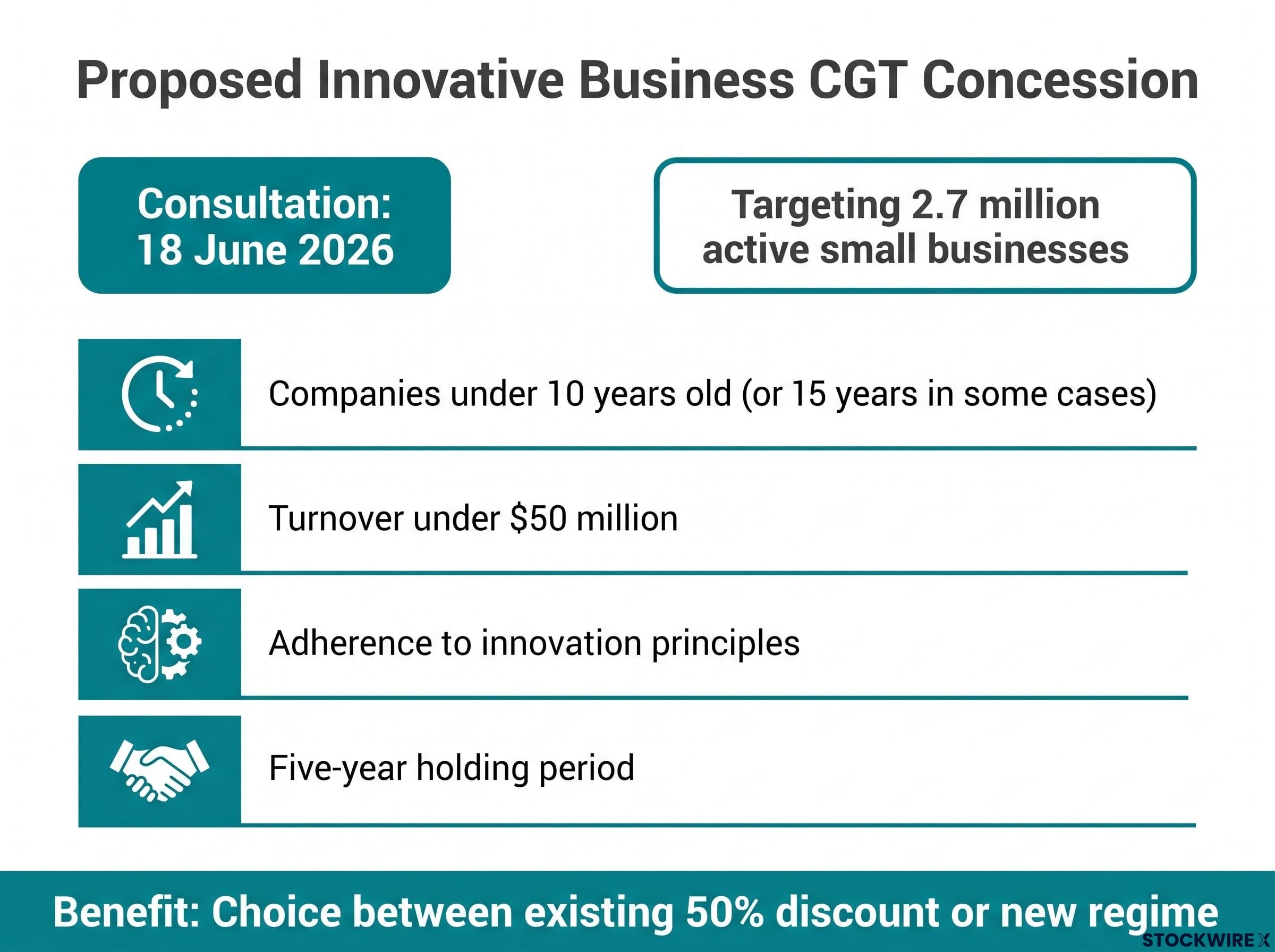

That divergence has consequences for where global capital locates itself. Treasury appears to recognise the problem: a consultation on the Innovative Business CGT Concession was released on 18 June 2026, signalling that the innovation pipeline risk is officially acknowledged.

Dividend imputation is the background machinery that makes Australia’s tax treatment of equities unusual by global standards. The CGT changes do not create a new bias; they amplify one that has been embedded in the system since 1987.

Here is how the mechanism works:

A concrete example makes the arithmetic visible. A company earns $1,428, pays $428 in corporate tax (at 30%), and distributes the remaining $1,000 as a fully franked dividend. The shareholder receives the $1,000 plus a $428 franking credit. For a superannuation fund in pension phase paying 0% tax, the grossed-up income is $1,428, the tax liability is zero, and the $428 franking credit is refunded in cash. The effective pre-tax yield on the investment is substantially higher than the nominal dividend.

This system already makes fully franked dividends from mature companies highly attractive to resident taxpayers. The proposed CGT changes raise the effective tax rate on capital gains relative to franked dividend income, compounding a bias that was structurally embedded before the reforms were proposed.

The ATO franking credits guidance confirms that the grossed-up dividend amount is assessable income and that the attached credit offsets the shareholder’s personal tax liability dollar for dollar, with any excess refunded, which is the mechanism that makes fully franked dividends from mature ASX companies structurally superior on an after-tax basis to capital gains under the proposed regime.

SMSFs in pension phase and large superannuation funds in accumulation phase are among the most tax-rate-sensitive holders of Australian equities. For these investors, the combined imputation and CGT signal creates a strong structural incentive to tilt toward high-yield incumbents.

Superannuation funds collectively hold a dominant share of domestic equities. Their reallocation behaviour in response to tax settings carries outsized market consequences. When the largest pool of capital in Australian equities faces a strengthened incentive to favour income over growth, the resulting rotation is not a marginal shift. It reshapes the market’s composition.

The capital rotation described above does not stop with active investor decisions. A mechanical feedback loop in passive index construction amplifies it.

Market-cap-weighted index ETFs, the structure underlying most broad ASX 200 and ASX 300 funds, allocate capital based on a company’s market capitalisation relative to the total index. As a company’s share price rises, its weight in the index increases, and the ETF must purchase more of it to track the benchmark. The ETF does not ask why the price rose.

The feedback loop runs in four steps:

Titan Wealth describes a “dangerous feedback loop” in index investing: strong performance by a subset of stocks boosts their index weights, pulls in more passive money, and further reinforces their outperformance.

Morningstar research notes that passive flows can distort prices by driving up the valuations of the largest index constituents. Russell Investments similarly asks whether passive investing is “feeding the mega-cap beast.”

It is worth noting that the scale of this effect remains genuinely uncertain. Academic evidence is divided on whether passive flows reliably cause systematic mispricing. Betashares research cautions against overstating the dynamic, observing that fundamentals continue to act as a constraint and that large-cap valuations are not uniformly distorted by passive demand. The loop is better treated as a structural risk and a plausible mechanism than as a predetermined outcome.

The practical implication is that an ASX 300 ETF showing strong gains in 2027 or 2028 could reflect tax-induced capital concentration in a handful of large incumbents rather than broad economic health. In a simple portfolio return figure, the two look identical.

The fact that Treasury released a consultation paper on 18 June 2026 specifically covering “capital gains tax reforms, arrangements for innovative start-ups” is itself a signal. Governments do not design carve-outs for problems they believe do not exist.

The proposed Innovative Business CGT Concession would allow eligible early-stage investors to choose between the existing 50% discount or the new regime. Eligibility criteria as currently proposed include:

On 18 June 2026, the Prime Minister announced further CGT concessions for small businesses and start-ups, framed as supporting 2.7 million active small businesses. The political recognition of the innovation risk is now explicit.

The question is whether the response matches the problem’s scale. The concession is a step in the right direction, but its final design is not fixed, its eligibility criteria are narrow, and the Senate inquiry (with reporting expected around 22 June 2026) will determine whether it emerges with enough breadth to matter.

Three concrete criteria can be applied to evaluate whether the final concession design adequately addresses the structural risk:

Breadth of eligibility. Does the concession extend to critical minerals explorers, mid-stage biotechs, and deep-tech ventures that may exceed the $50 million turnover threshold before reaching an exit event? If eligibility is too narrow, the sectors most at risk fall outside the safety net.

Monitoring obligations. Does the legislation commit to tracking venture capital deployment volumes, start-up formation rates, and sub-top-50 ASX capital raisings alongside headline index performance? Without measurement, policymakers will default to the ASX headline as their gauge of success.

Compensating mechanisms. Are co-investment vehicles, government guarantees, or production-style tax credits available for sectors that remain structurally disadvantaged even with the concession in place? The US Section 45X credit demonstrates that allied nations are willing to use explicit industrial policy to direct capital toward strategic sectors.

The Australian Industry Group’s assessment that changes “lessen but don’t eliminate harm to investment” suggests the current design leaves a gap that these three tests could help close.

For founders and early employees wanting to model specific exit scenarios, our full explainer on indexation and founder equity walks through why a $10,000 original outlay on a $5 million exit generates an inflation adjustment of only around $3,400, the comparative treatment across Canada and the UK where entrepreneur-specific relief was legislated alongside broader rate increases, and why the grandfathering cut-off at 1 July 2027 makes the timing of any equity event a material tax decision.

A rising ASX 200 after 1 July 2027 could mean the Australian economy is strengthening. It could also mean that tax-induced capital concentration is inflating the market capitalisation of a small number of large incumbents while the innovation pipeline contracts underneath. The headline index level cannot distinguish between the two.

The alternative indicators that would reveal whether the innovation economy is being preserved or hollowed out include:

The strategic dimension sharpens the stakes. As allied nations use explicit industrial policy to direct capital toward critical minerals and deep tech, Australia’s competitive position in these sectors will be partly determined by whether domestic tax settings support or structurally undermine investment in them.

The Centre for Independent Studies links higher effective CGT directly to lower productivity, making long-run productivity trend data another indicator worth watching alongside the sector-specific metrics.

The reform’s success or failure will not be visible in the ASX headline figure. It will show up years later in whether Australia’s knowledge-intensive sectors grew or contracted relative to peers. The monitoring framework above is how you see that signal before it becomes irreversible.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and legislative outcomes. The reforms discussed are prospective and subject to Senate passage and final legislative design.

—

The Treasury Laws Amendment (Tax Reform No.1) Bill 2026 passed the House of Representatives on 4 June 2026 and replaces the existing 50% capital gains tax discount with inflation-based indexation of the cost base plus a minimum 30% tax on the real gain, applying to gains from 1 July 2027.

Founders with equity and early-stage investors face the sharpest impact because their returns arrive almost entirely as capital gains on exit, with no dividend income to cushion the tax treatment; the higher effective rate directly raises the cost of backing long-horizon, speculative ventures like biotech and enterprise software.

Major banks, utilities, REITs, toll road operators, and supermarket chains are structurally favoured because they pay fully franked dividends whose tax treatment is untouched by the reforms; biotechnology, enterprise software, critical minerals juniors, deep tech, and early-stage clean energy are disadvantaged because their returns depend almost entirely on capital gains.

The Innovative Business CGT Concession, released for consultation on 18 June 2026, would allow eligible early-stage investors to choose between the existing 50% discount or the new regime; eligibility as currently proposed requires companies to be under 10 years old (or 15 in some cases), have turnover below $50 million, follow defined innovation principles, and involve a five-year holding period.

A rising ASX 200 after 1 July 2027 could reflect tax-induced capital concentration in a small number of large dividend-paying incumbents rather than broad economic health; the headline index cannot distinguish between genuine growth and a passive ETF amplification loop inflating the market capitalisation of the same large-cap names.