Why Australian Investors Are Missing the World’s Biggest 2026 Gains

27 mins ago

The week ending 22 June 2026 produced two simultaneous short-selling signals pointing in opposite directions. Institutional bears piled into uranium, lithium, and gold stocks with conviction. At the same time, they quietly retreated from consumer and growth names across restaurants, e-commerce, travel, and software.

That split is not noise. Short sellers are making a coordinated sector-level call that commodity valuations have run ahead of fundamentals, while simultaneously reassessing prior bearish bets on Australian consumer names as the domestic macro environment improves. The positioning data from ASIC tells you where professional conviction is building and where it is breaking down, and the coherence of both signals makes this week’s data worth more than a routine scan.

Here is exactly where that conviction sits, stock by stock, and what each directional signal tells you about the sectors in question. The result is a sharper view of where professional money sees the most near-term risk on the ASX, and where it has decided the risk trade is over.

Before naming individual stocks, the macro backdrop explains why the split is happening now rather than three months ago.

The commodity side of the ASX is absorbing three simultaneous pressure points:

On the other side, the consumer and growth short unwind reflects something different entirely. The original bearish theses on names like Credit Corp, Guzman Y Gomez, and Temple & Webster were built on cost-of-living pressure, earnings risk, and rate sensitivity. Those conditions have moderated. The domestic macro environment is less acute than in 2023-24, and shorts positioned for continued deterioration are finding less and less to support their bets.

What this tells you is that the positioning data is not a collection of random stock-level moves. It is a coherent macro rotation, and the individual names that follow are confirmation of a pattern you can track yourself.

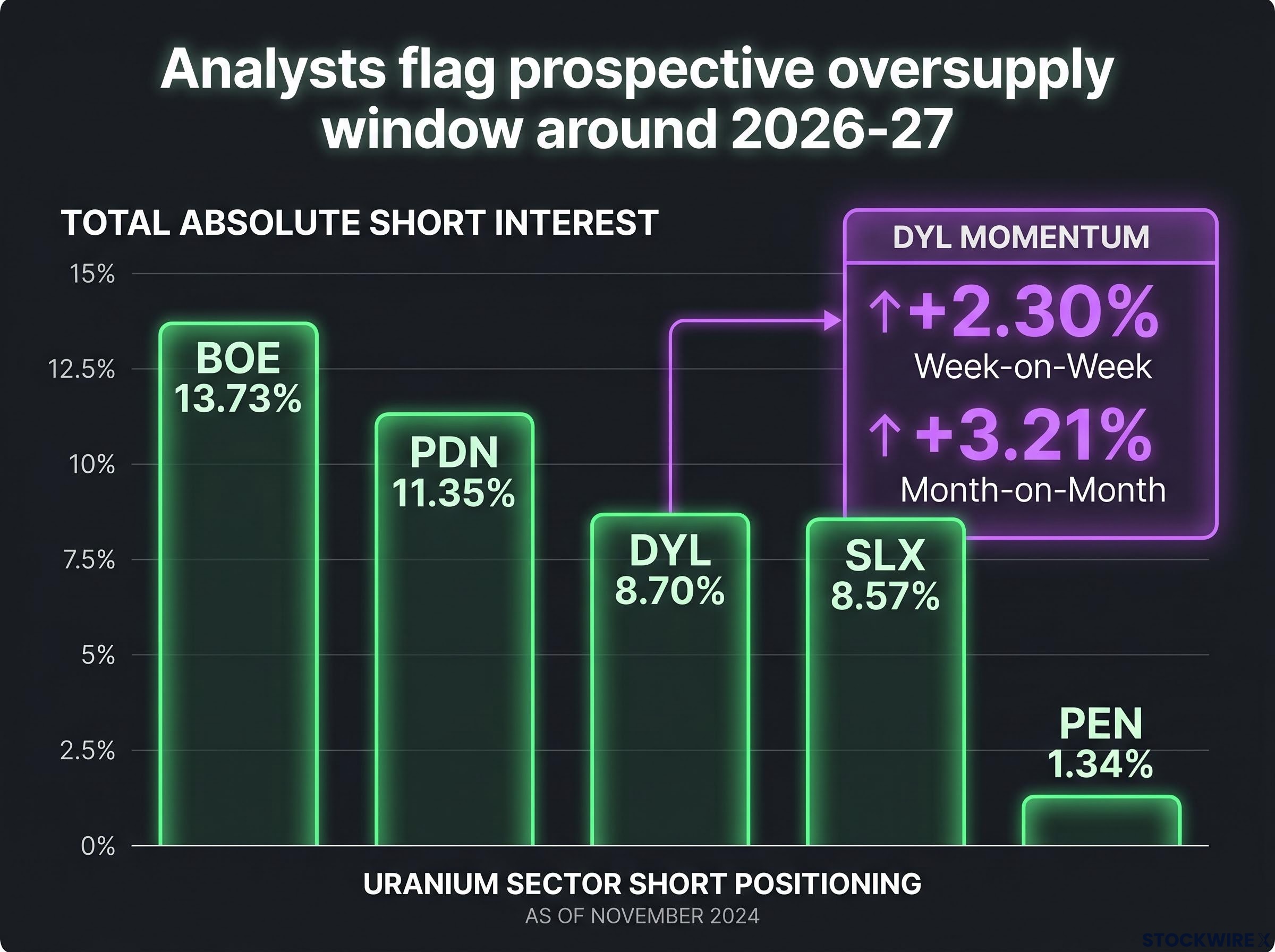

The uranium short trade is the cleanest directional signal in the data. Five names attracted fresh short positions during the week, and the breadth of the build leaves little room to dismiss it as isolated positioning.

| Stock | Short interest (%) | Week-on-week change (%) | Month-on-month change (%) |

|---|---|---|---|

| Boss Energy (BOE) | 13.73 | — | — |

| Paladin Energy (PDN) | 11.35 | — | — |

| Deep Yellow (DYL) | 8.70 | +2.30 | +3.21 |

| Silex Systems (SLX) | 8.57 | +0.55 | +0.29 |

| Peninsula Energy (PEN) | 1.34 | +0.67 | +0.40 |

BOE and PDN carry the highest absolute short interest, sitting at the top of ASX most-shorted lists. But the pace of the build is sharpest in DYL, where short interest climbed 2.30 percentage points in a single week and 3.21 percentage points over the month. That is not a tentative probe. That is conviction capital arriving.

The short thesis has a structural anchor: analysts flag a prospective uranium oversupply window around 2026-27, creating room for share prices to retreat even as the long-term energy transition case for uranium demand remains intact.

The distinction matters. These shorts are not a bet against nuclear energy. They are a tactical call that uranium equity valuations ran too hard on the back of strong 2026 year-to-date gains and that the near-term fundamentals do not yet justify the prices. If you hold uranium exposure, that is the timeframe question to resolve: the long-term structural case has not changed, but the near-term valuation gap is what bears are targeting.

Uranium short positioning was already deepening in the week ending 5 June 2026, with Pilbara Minerals showing a conflicting pattern of weekly covering alongside a monthly build that confirmed the structural bearish thesis remained intact despite tactical noise at the stock level.

The lithium short is messier than uranium, and that messiness is the signal. Positioning is shifting week to week, with some names showing covering alongside fresh builds.

The lithium short is not one trade. It is multiple overlapping tactical bets that can flip direction quickly, and that makes it harder to read as a single signal. If you hold lithium exposure, the implication is that you are dealing with a more active risk environment where positioning can shift within a week, not just across quarters.

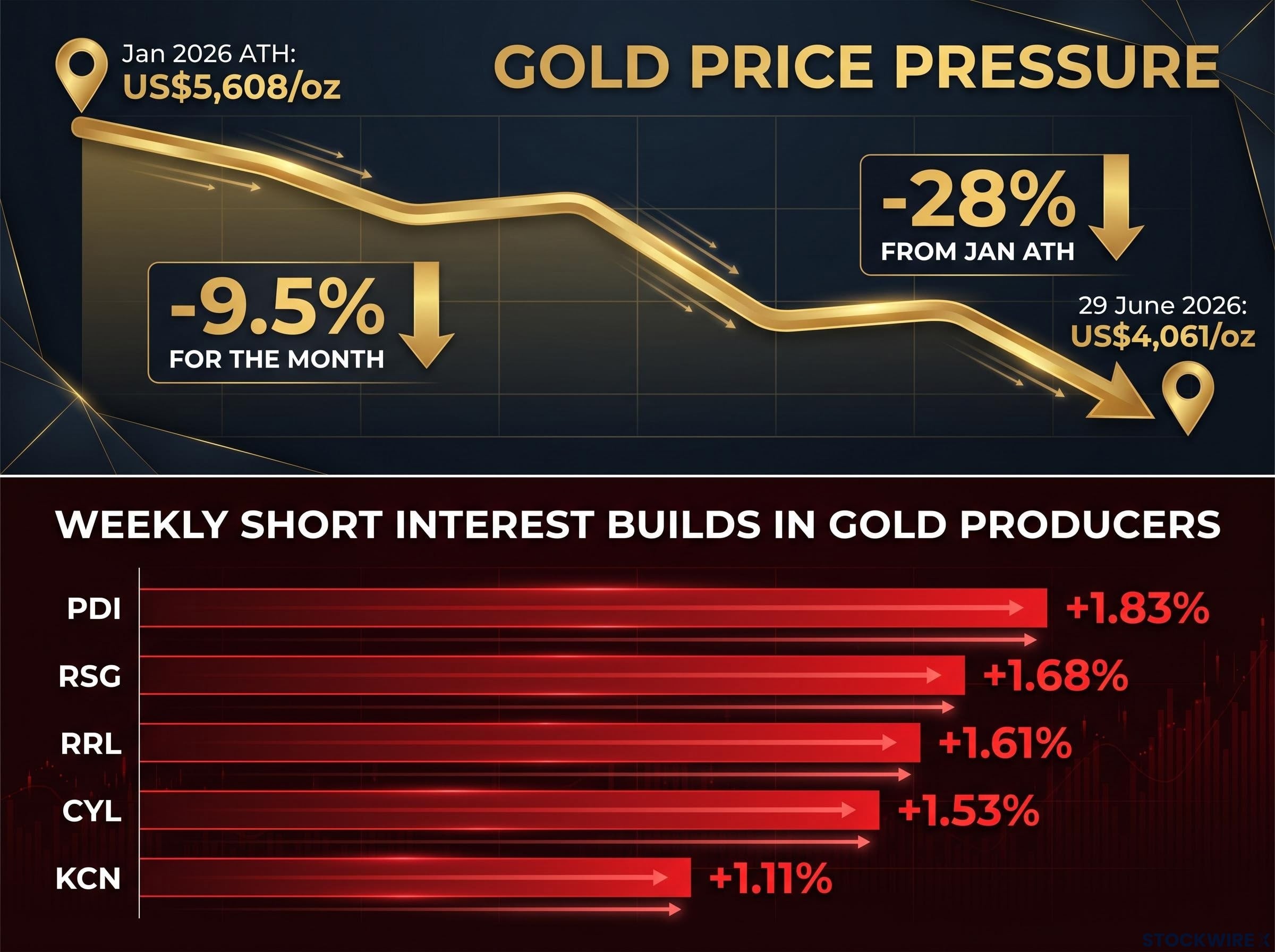

The gold short is more straightforward. Five mid-cap producers all saw short interest climb during the week, and the thesis is simple: gold’s 9.5% monthly price decline compresses margins directly.

The breadth here tells the story. This is not a company-specific call. It is a sector bet that gold producers face sustained margin pressure if the spot price does not recover. The gold short is more directly tied to price mechanics than the uranium or lithium trades, and for holders of gold equities, the variable to watch is simply where the spot price goes from here.

Short interest data is one of the few windows into institutional positioning that Australian retail investors can access in near-real time. Understanding what it can and cannot tell you prevents two common errors.

Short interest is best treated as a map of where professional conviction currently sits, not as a forecast of price direction. The contrarian risk that crowded shorts can unwind rapidly when the thesis cracks is real, and it applies directly to several names in this article.

For investors new to reading this data, our full explainer on ASIC short sale reporting covers how Australia’s transaction-level disclosure regime works and why accurate reporting matters, including the $35 million penalty Macquarie Securities received for systematic misreporting across 1.5 billion transactions.

The other side of the positioning split tells an equally clear story, and Credit Corp (CCP) is the centrepiece.

The arc is clean. A sharp 17% drop accompanied CCP’s first-half result in February 2026, a move the market has since come to regard as an overreaction to the underlying business performance. Short sellers added to positions into that weakness. By May 2026, management had moved to address those concerns directly, reaffirming full-year FY26 guidance and lifting the outlook for the lending division. The specific concerns driving the short thesis, earnings risk and lending deterioration, were directly addressed by management.

CCP’s short interest fell to 1.57%, declining 2.82 percentage points week-on-week and 4.64 percentage points month-on-month as of 22 June 2026, the largest short interest reduction on the ASX for the week.

The share price had not yet recovered to pre-February levels as of the reporting date. That lag is the pattern worth noting: short covering often precedes price recovery rather than following it.

CCP is not alone. The same directional signal appears across multiple consumer and growth names:

| Stock | Short interest (%) | Week-on-week change (%) | Month-on-month change (%) |

|---|---|---|---|

| Guzman Y Gomez (GYG) | 10.75 | -1.79 | -1.84 |

| SiteMinder (SDR) | 5.47 | -1.43 | -1.64 |

| Temple & Webster (TPW) | 6.69 | -1.39 | -1.36 |

| WEB Travel Group (WEB) | 4.69 | -1.31 | -1.62 |

| Treasury Wine Estates (TWE) | 11.38 | -1.03 | -2.33 |

The coverage spans e-commerce, travel, software, restaurants, and beverages. That breadth tells you this is not a handful of isolated covering events. It is a broad sentiment recalibration as the conditions that supported bearish consumer theses, acute cost-of-living pressure, rate sensitivity, earnings deterioration, have softened. For holders of heavily shorted consumer or growth names, the CCP template is directly relevant: when a company under short pressure addresses the specific concern driving the trade, covering can be rapid, and the share price often follows with a lag.

ASX short squeeze signals followed a recognisable pattern in May 2026: Guzman Y Gomez surged 20% intraday after announcing a US market exit, a catalyst that directly invalidated the bearish thesis and triggered rapid covering from a 12.59% short base, the same dynamic now embedded in the current positioning data for GYG at 10.75%.

The current positioning split is a snapshot, not a permanent state. It reflects institutional conviction on a specific set of macro assumptions, and those assumptions face tests in the coming weeks.

Three variables will determine whether the trades described in this article extend or reverse:

The asymmetric risk sits in the commodity names. BOE, PDN, and DYL carry short interest levels where covering, if triggered by a macro shift such as a gold recovery or a uranium demand surprise, would itself amplify upside moves. That is the contrarian case embedded in the data.

PLS at approximately 10.3% is the bridge case: structurally shorted but already showing tactical covering, making it a name where positioning can shift quickly in either direction.

Short interest data is most useful not as a static risk measure but as a leading indicator of conviction change. The trajectory of these numbers over the next several weeks will tell you whether the macro assumptions driving both sides of this rotation are being validated, or quietly revised.

Active fund manager positioning across 62 Australian equity funds tells a complementary story to the short interest data: industrials has flipped from a structural underweight to the clearest overweight in the cohort, while CBA carries the largest single-stock underweight at negative 8.0 percentage points, a distribution that sits alongside rather than contradicts the commodity and consumer rotation visible in short data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Short interest data reflects positioning as of the reporting date and is subject to rapid change.

ASX short selling involves borrowing shares and selling them with the expectation of buying them back at a lower price. ASIC collects transaction-level short sale data and publishes it weekly, making it accessible through platforms like ShortMan and Market Index.

Boss Energy (BOE) carries the highest short interest at 13.73%, followed by Paladin Energy (PDN) at 11.35%, with Deep Yellow (DYL) showing the sharpest weekly build at plus 2.30 percentage points for the week ending 22 June 2026.

The original bearish theses on consumer names like Credit Corp (CCP) and Guzman Y Gomez (GYG) were built on cost-of-living pressure and earnings risk; as domestic macro conditions have moderated and companies like CCP reaffirmed guidance, those bearish cases weakened and short sellers exited positions.

A short squeeze occurs when a bearish thesis cracks and short sellers rush to buy back shares simultaneously, driving the price sharply higher through covering activity itself. BOE at 13.73% and PDN at 11.35% carry the highest squeeze risk if a macro shift such as a gold or uranium demand surprise invalidates current positioning.

Gold's roughly 9.5% monthly price decline to approximately US$4,061/oz as of 29 June 2026 compresses producer margins directly, and short sellers responded by building positions across five mid-cap producers including Catalyst Metals, Regis Resources, and Resolute Mining during the week ending 22 June 2026.