A Chinese open-weight model ranked fourth in the world just triggered a sell-off in U.S. technology and semiconductor stocks, and Wall Street analysts are already revising the assumption that made those stocks worth what they were.

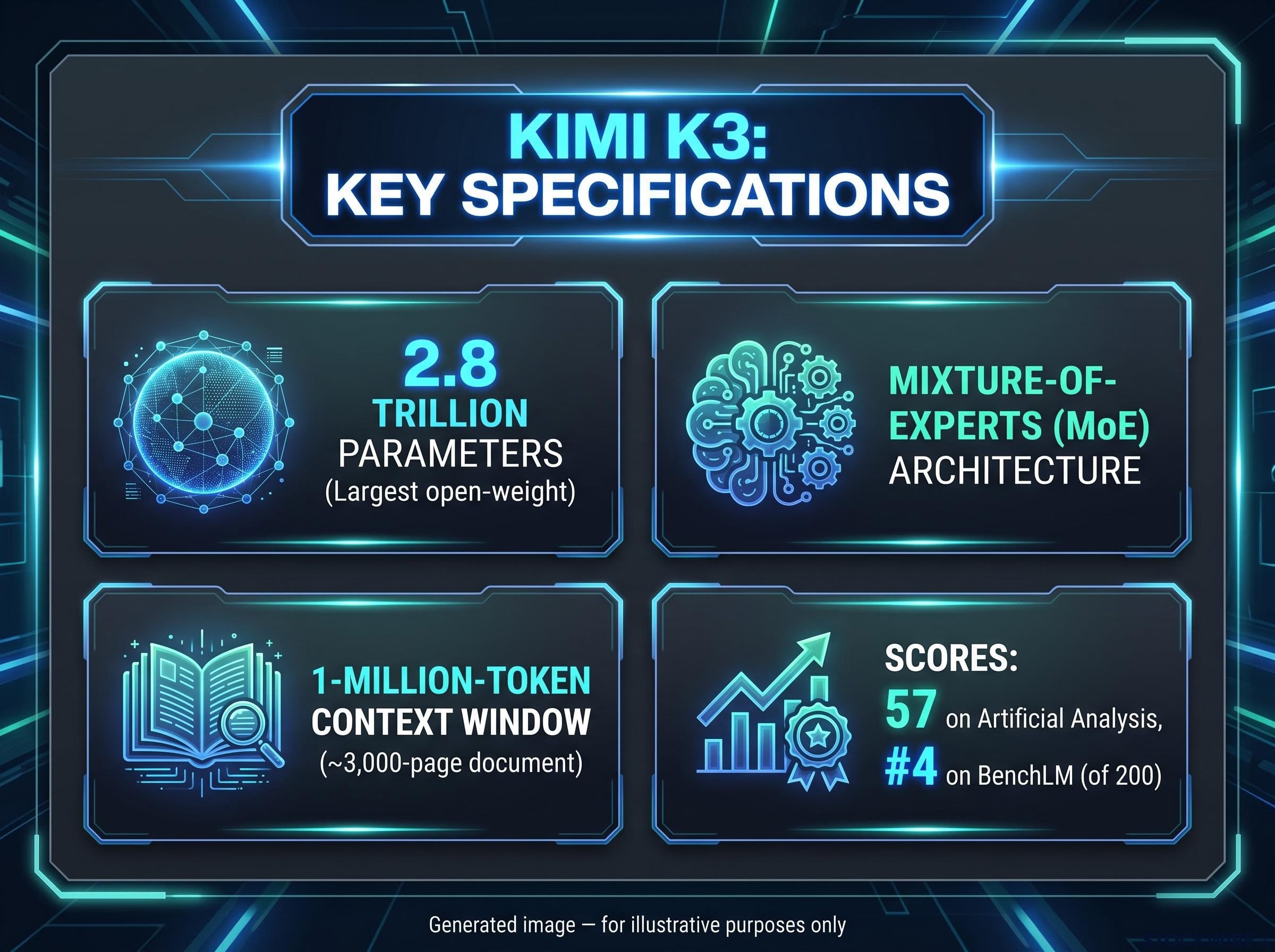

For several years, investor confidence in U.S. AI lab valuations and their chip suppliers rested partly on a structural premise: American frontier models enjoyed a durable lead over Chinese rivals measured in multiple months, and that gap was widely expected to hold. Kimi K3, released by Moonshot AI on approximately 16 July 2026, is the most direct challenge yet to that premise. It is not merely a strong benchmark performer. It is an open-weight, permissively licensed, 2.8-trillion-parameter model that multiple independent evaluators now place squarely within the global frontier band. That combination of performance and openness does structural work that a single impressive score cannot.

Here is a clear picture of what K3 actually is, which market assumptions it disrupts, and what signals to watch if you hold positions in U.S. AI or semiconductor names.

What Kimi K3 actually is, and why open weights change the calculus

The raw specifications land first:

- 2.8 trillion parameters, a scale that positions it as the largest open-weight model published anywhere in the world to date

- Mixture-of-Experts (MoE) architecture, a design that activates only a fraction of total parameters per query, keeping inference costs manageable despite the model’s scale

- 1-million-token context window, allowing the model to process roughly the equivalent of a 3,000-page document in a single pass

- Permissive open-weight licence, meaning any organisation worldwide can download and self-host the model without paying Moonshot AI

K3 achieves a score of 57 on the Artificial Analysis Intelligence Index, a result that places it within a narrow band below the leading U.S. proprietary systems. BenchLM’s composite leaderboard ranks it #4 of 200 models overall and #4 of 99 on the verified board.

“The strongest open-weight model anyone has shipped.” — BenchLM

Independent evaluators report top-tier coding scores across DeepSWE, ProgramBench, and Terminal-Bench, alongside the strongest open-weight GPQA Diamond reasoning result at launch. Morgan Stanley analyst Gary Yu characterised K3 as representing “all-around catch-up in model size, performance, and pricing,” a distinction that makes it strategically significant beyond any single benchmark.

| Model | Artificial Analysis Score | Open-Weight |

|---|---|---|

| Claude Fable 5 | ~60 | No |

| GPT-5.6 Sol | ~59 | No |

| Kimi K3 | 57 | Yes (permissive licence) |

The open-weight licensing is where “strong model” becomes “competitive threat.” Application builders worldwide can now access near-frontier capability without paying proprietary prices, directly undermining the pricing power that underpins closed-source AI lab valuations.

When big ASX news breaks, our subscribers know first

The gap that Wall Street assumed was safe no longer looks that way

Through much of the past year, Wall Street had settled into a confident position: U.S. labs were running several months ahead of Chinese counterparts at the frontier, and that head start was treated as a dependable feature of the investment case rather than a variable to monitor. K3 is not the event that changes that view. It is the third data point that confirms the view was already changing:

- DeepSeek V3 demonstrated Chinese labs could produce competitive frontier-adjacent models at scale

- GLM-5.2 (Zhipu, June 2026) drew praise from Morgan Stanley as an already impressive release, arriving before K3 had even been announced

- Kimi K3 (July 2026) now ranks fourth globally and outperforms closed U.S. systems on several coding benchmarks

Bernstein analyst Robin Zhu described K3 as a “confirmatory data point” supporting the view that Chinese AI can maintain pace with global state-of-the-art and gradually capture market share. Macquarie analyst Ellie Jiang reached a similar conclusion.

BenchLM frames the distance to the closed Western frontier as now measured “in months, not years.”

For investors, the pattern matters more than the single event. Three successive Chinese AI milestones within roughly eight months suggest the lead on which frontier AI premium valuations depend is eroding on a predictable trajectory, not being disrupted by an outlier.

Multiple AI valuation frameworks, including Minsky’s financing stages and the Shiller CAPE at 40.11, had already flagged elevated risk in AI-adjacent equities before K3 arrived, and the pattern of successive Chinese frontier releases adds a competitive erosion variable that those frameworks were not built to capture.

What the sell-off is actually pricing in

The K3 announcement triggered a sell-off in technology and semiconductor equities on 16-17 July 2026. Bernstein’s Robin Zhu noted that the immediate negative market reactions were broadly “rational responses” to the announcement. The question is what, specifically, the market is marking down.

Two structural assumptions are under challenge:

- The geographic lead assumption: U.S. labs hold the frontier exclusively, justifying premium multiples. A #4-ranked global model from China means the frontier is shared, not exclusively American.

- The closed-source moat assumption: Open models cannot compete at the frontier, protecting proprietary pricing power. K3 demonstrates they can.

Bernstein’s analysis holds that as reasoning capabilities converge at the frontier, the trajectory is negative for the long-run profit margins of AI model labs.

The margin compression mechanism is straightforward. If customers can access near-frontier capability at lower cost via open-weight models, U.S. labs face pressure to cut prices or expand rate limits. Notably, in the weeks prior to K3’s release, OpenAI and Anthropic had already moved into direct competition on pricing and rate limits, a sign that the squeeze on margins was well underway before K3 confirmed the wider trend.

B. Riley analysts described a frontier-class open-weight model narrowing the gap with leading U.S. systems as a net positive for companies at the application layer that embed AI into their products. That is the other side of the same coin: value migrates from model builders to model users.

The valuation implication is not that U.S. AI labs become worthless. It is that the premium investors have been paying for their presumed technological exclusivity now requires a more sceptical justification.

AI stock valuation risk was already intensifying before K3 arrived: Goldman Sachs’ May 2026 assessment found that AI-related technology spending as a share of US GDP had surpassed dot-com peak levels, and the four largest hyperscalers were collectively guiding toward combined capital expenditure well above $600 billion annually.

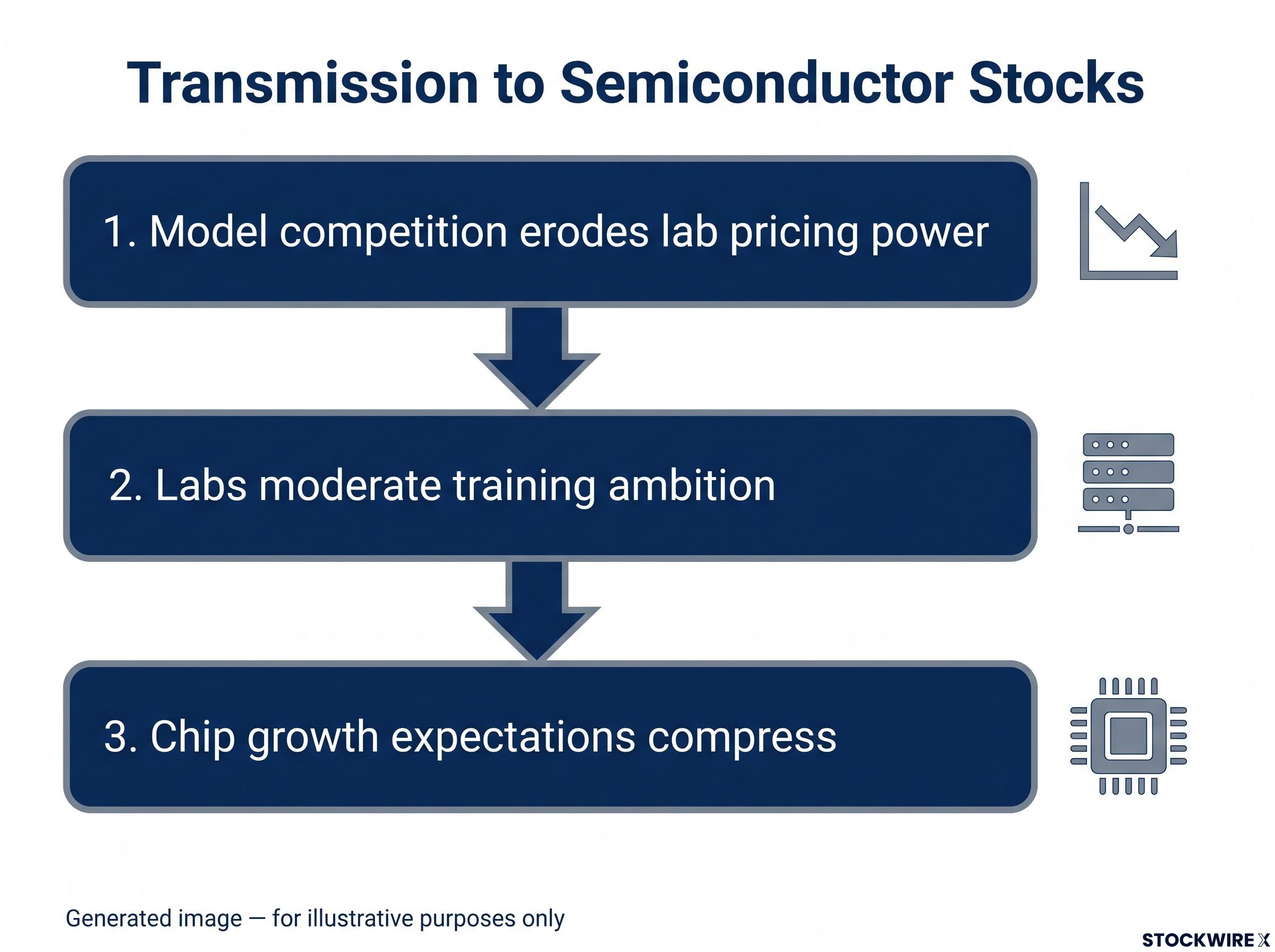

How competitive AI model pressure transmits to semiconductor stocks

The link from model competition to chip stocks is indirect but follows a clear chain:

- Model competition erodes lab pricing power. When customers can choose among multiple near-frontier options (including open-weight ones at lower cost), expected returns per model drop.

- Labs moderate training ambition. If returns per model fall, labs become more selective about future training expenditures. The incentive to endlessly scale parameter counts and training budgets weakens.

- Chip growth expectations compress. Semiconductor valuations have embedded AI-driven hyper-growth assumptions tied largely to U.S. frontier lab spending. If the duration or concentration of that spending growth is revised downward, multiples contract even without deteriorating near-term revenues.

There is a geographic dimension too. As Chinese labs demonstrate frontier capability, more global training and inference demand may shift toward Asian AI ecosystems, changing the customer mix for U.S. chipmakers even if total GPU demand remains high.

Semiconductor investors should recognise that even if chip revenues hold steady in the near term, a credible narrative that U.S. labs’ training ambitions may moderate is sufficient to compress multiples in a sector that trades on growth expectations. This is an expectations story as much as a fundamentals story. On upcoming earnings calls, listen specifically for changes in AI capex guidance and any references to geographical customer mix shifts.

Why K3 does not guarantee a rapid U.S. enterprise exodus

The bearish case writes itself cleanly. The reality has more friction.

B. Riley analysts raised a pointed concern in their note: that corporate deployment of Chinese open-weight models is likely to attract close scrutiny over data governance obligations and compliance requirements. Many regulated or government-adjacent enterprises have constraints on using foreign-origin software, particularly for sensitive data. K3’s open-weight self-hosting option can partially circumvent cloud-provider and jurisdictional concerns, but it does not remove compliance obligations.

Four verticals where domestic proprietary labs retain structural advantages:

- Government and defence-adjacent contexts with explicit procurement restrictions

- Financial services subject to data-localisation and vendor-risk requirements

- Healthcare with patient-data governance obligations

- Critical infrastructure where foreign-origin software faces heightened scrutiny

Bernstein’s Robin Zhu warned that K3’s emergence could accelerate Anthropic’s efforts to pursue regulatory strategies targeting Chinese AI competition, with comparisons drawn to U.S. restrictions on firms such as BYD.

That regulatory dimension is a genuine structural buffer for U.S. AI incumbents, but one that protects specific verticals rather than restoring the broad frontier premium that K3 has put in question.

The regulatory buffer for US AI incumbents sits within a broader geopolitical framework: chip export controls are grounded in national-security law with bipartisan Congressional backing, placing them outside the jurisdiction of trade negotiators and structurally insulating them from US-China diplomatic progress.

The next major ASX story will hit our subscribers first

Five signals that will determine whether the investor thesis holds

Rather than predict what happens next, here are five directly observable signals to monitor if you hold U.S. AI or semiconductor positions:

- Benchmark trajectory: Track K3’s scores on BenchLM, Artificial Analysis, and LMArena as more tests are added, and watch for new Chinese models matching or exceeding K3

- U.S. lab pricing moves: Price cuts or expanded rate limits from OpenAI and Anthropic are evidence of felt competitive pressure; note competition had already begun pre-K3

- AI capex guidance: On chipmaker and hyperscaler earnings calls, listen for references to training demand moderation or geographical customer mix shifts

- Regulatory signals: Monitor U.S. policy proposals on AI security, foreign model procurement rules, and whether incumbents like Anthropic actively lobby for restrictions

- Application-layer adoption: Public announcements from developers or SaaS platforms integrating K3 for cost or performance reasons would confirm the shift of bargaining power toward customers

| Signal | What to Watch | Why It Matters |

|---|---|---|

| Benchmark trajectory | New Chinese models on BenchLM and Artificial Analysis matching or exceeding K3 | Confirms whether gap compression is a trend or a one-off |

| U.S. lab pricing | Price cuts, expanded rate limits, or new open-weight releases from OpenAI and Anthropic | Direct evidence of competitive pressure on margins |

| AI capex guidance | Earnings call language on training demand moderation or customer mix shifts | Transmission channel from model competition to chip valuations |

| Regulatory signals | U.S. policy proposals on foreign AI models; incumbent lobbying activity | Could blunt or delay K3’s commercial impact in regulated markets |

| Application-layer adoption | Developers or SaaS platforms publicly integrating K3 | Confirms bargaining power shifting to model consumers |

If two or more of these signals move in the same direction within the next quarter, investors holding AI lab or semiconductor positions at frontier-premium multiples should treat that as evidence that the thesis has changed, not just that prices have moved.

What K3 changes for investors, and what it does not

K3 is not a catastrophic disruption. It is a concrete erosion of the two structural assumptions, geographic lead and closed-source moat, that have supported frontier AI premium valuations. The pattern of DeepSeek V3, GLM-5.2, and now K3 within roughly eight months suggests that erosion is durable, not a one-off surprise.

What has not changed: near-term fundamentals for most major U.S. AI and chip companies remain intact, and the compliance buffer in regulated verticals is real. What has changed is the credibility of a comfortable, uncontested American lead at the frontier.

The question for investors is no longer whether the frontier is exclusively American. It is how quickly the market reprices the competitive dynamics that K3 has confirmed.

For investors wanting to place K3’s competitive implications within a broader analytical structure for AI’s economic impact, our full explainer on the Howard Marks AI framework examines his argument that value migrates from model builders to model users as AI capability commoditises.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding AI competitive dynamics and market valuations are speculative and subject to change based on market developments and company performance.