SpaceX raised $75 billion in a single day. That figure alone makes the June 2026 listing the largest Initial Public Offering (IPO) in history at pricing, but the number only tells you part of the story. Most Australians have heard of SpaceX. Almost none had a clear path to owning shares before 12 June 2026.

The IPO priced at $135 per share, implying a valuation of approximately $1.77 trillion. Shares closed their first day of trading near $161, pushing the market capitalisation past $2.1 trillion. The mechanics behind how that price was set, who actually received shares at it, and what happens to early holders over the rest of 2026 are not widely understood by retail investors, and those mechanics matter far more than the headline number.

The SpaceX IPO is an unusually well-documented case study because of its scale and public attention. Here is how each structural layer works, from the offering itself through to the lockup window later this year, so you can apply the same evaluative framework to any major listing you encounter next.

What the $75 billion actually paid for

Start with the number: approximately 555-556 million shares sold at $135 each, raising roughly $75 billion (with total proceeds including underwriter overallotment potentially reaching approximately $86 billion). That makes it the largest IPO in history at pricing.

$75 billion raised, all flowing directly to SpaceX. No insiders sold a single share on listing day, making this the largest all-primary offering in public market history.

Now look at what sits underneath that number. Every dollar raised went directly to SpaceX the company. This was an all-primary offering, meaning all shares sold were newly issued. Existing shareholders, including employees and early venture backers, were not permitted to sell during the IPO itself.

That distinction matters more than it might seem. In a typical large IPO, the capital raised splits between the company (primary shares) and existing investors cashing out (secondary shares). When insiders are selling on listing day, it tells you they have decided the public market price is high enough to take money off the table. When they are not, it removes one of the red flags you should always check for, but it also means the insider liquidity question is deferred, not eliminated.

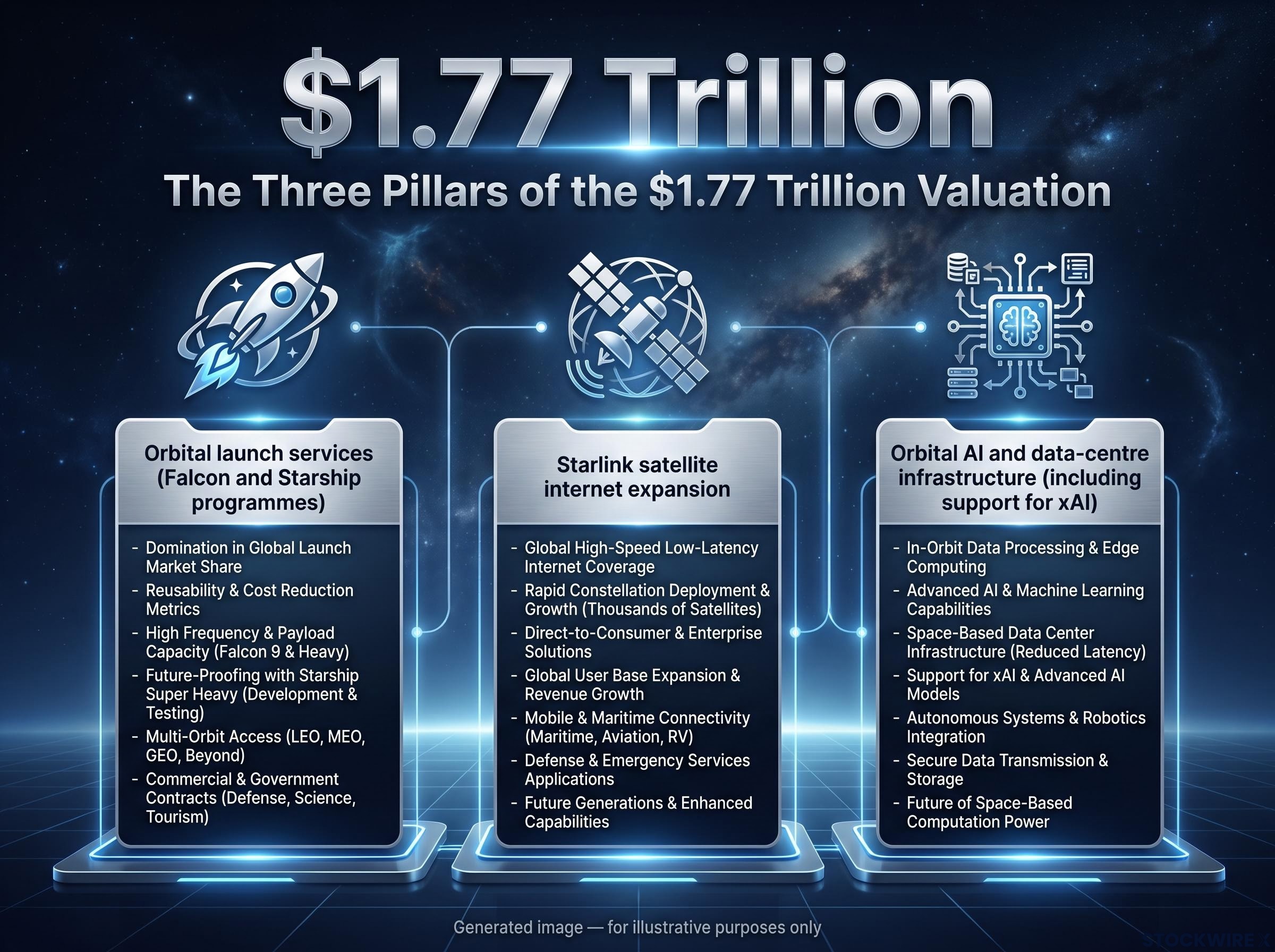

SpaceX outlined three areas for deploying the capital:

- Rockets and launch infrastructure (Falcon and Starship programmes)

- Starlink satellite internet expansion

- Orbital AI and data-centre infrastructure, including support for xAI

| Feature | All-primary offering (SpaceX) | Mixed offering (typical large IPO) |

|---|---|---|

| Where proceeds go | Entirely to the company | Split between company and selling shareholders |

| What it signals about insiders | Not cashing out at listing; growth-focused | Some insiders realising gains immediately |

| Deferred liquidity implication | Insider selling deferred to post-lockup window | Partial insider liquidity achieved on day one |

The all-primary structure tells you that SpaceX’s insiders were not cashing out on listing day. That removes one red flag, but it means the full insider liquidity event arrives later in 2026 when lockup restrictions expire, a risk window worth watching.

When big ASX news breaks, our subscribers know first

How a $1.77 trillion valuation gets negotiated

A share price of $135 sounds precise. It is not. It is the output of a negotiation process between a company, its investment banks, and the institutional investors those banks canvass for demand.

Here is how IPO pricing typically works:

- The company mandates investment banks to manage the offering

- Banks set a preliminary price range based on comparable companies, growth projections, and early investor conversations

- A formal bookbuilding process runs during the roadshow, where institutional investors indicate how many shares they want and at what price

- A final price is struck based on aggregate demand, usually at or near the top of the indicated range if demand is strong

SpaceX departed from this process at step three. The $135 price was fixed before the full investor roadshow and bookbuilding had run their course. That is unusual. Standard practice involves publishing a range and adjusting it based on demand signals. By fixing the price early, SpaceX concentrated pricing authority with its own leadership rather than letting institutional demand discovery set the final number.

What that tells you is that the $135 figure reflects SpaceX’s conviction about its own value, not a price confirmed through the standard back-and-forth between banks and buyers. On its first trading day, shares closed near $161, pushing the market capitalisation to approximately $2.1-2.2 trillion, which suggests institutional demand validated the conviction, but the mechanism that produced the price was not the conventional one.

The three pillars of the $1.77 trillion valuation

The $1.77 trillion implied valuation at pricing rests on projected growth across three business lines, each carrying a different evidence base.

Orbital launch services form the established revenue foundation. The Falcon 9 programme has a long commercial track record, and Starship development represents the next generation of heavy-lift capability. This pillar has demonstrated revenue and operational history.

Starlink is the high-growth connectivity business. Subscriber numbers have expanded rapidly across global markets, making this the pillar with the clearest near-term growth metrics. Revenue trajectory is visible, even if profitability at scale remains a forward assumption.

Orbital AI and data-centre infrastructure is the most speculative pillar. This includes space-based computing capabilities and support for xAI. The total addressable market projections are large, but the revenue base is largely forward-looking, with limited established public-market data to benchmark against.

For you as a retail investor considering SPCX in secondary trading, the benchmark is not the negotiated $135 IPO price. It is the growth assumptions embedded in whichever price the market has reached by the time you can access shares through a broker.

For readers wanting to stress-test the growth assumptions embedded in the $1.77 trillion pricing figure, our full explainer on SpaceX’s IPO valuation breaks down what portion of the market capitalisation reflects current fundamental value versus priced-in optionality across Starship, orbital compute, and the AI infrastructure thesis.

Why most investors could not buy shares at $135

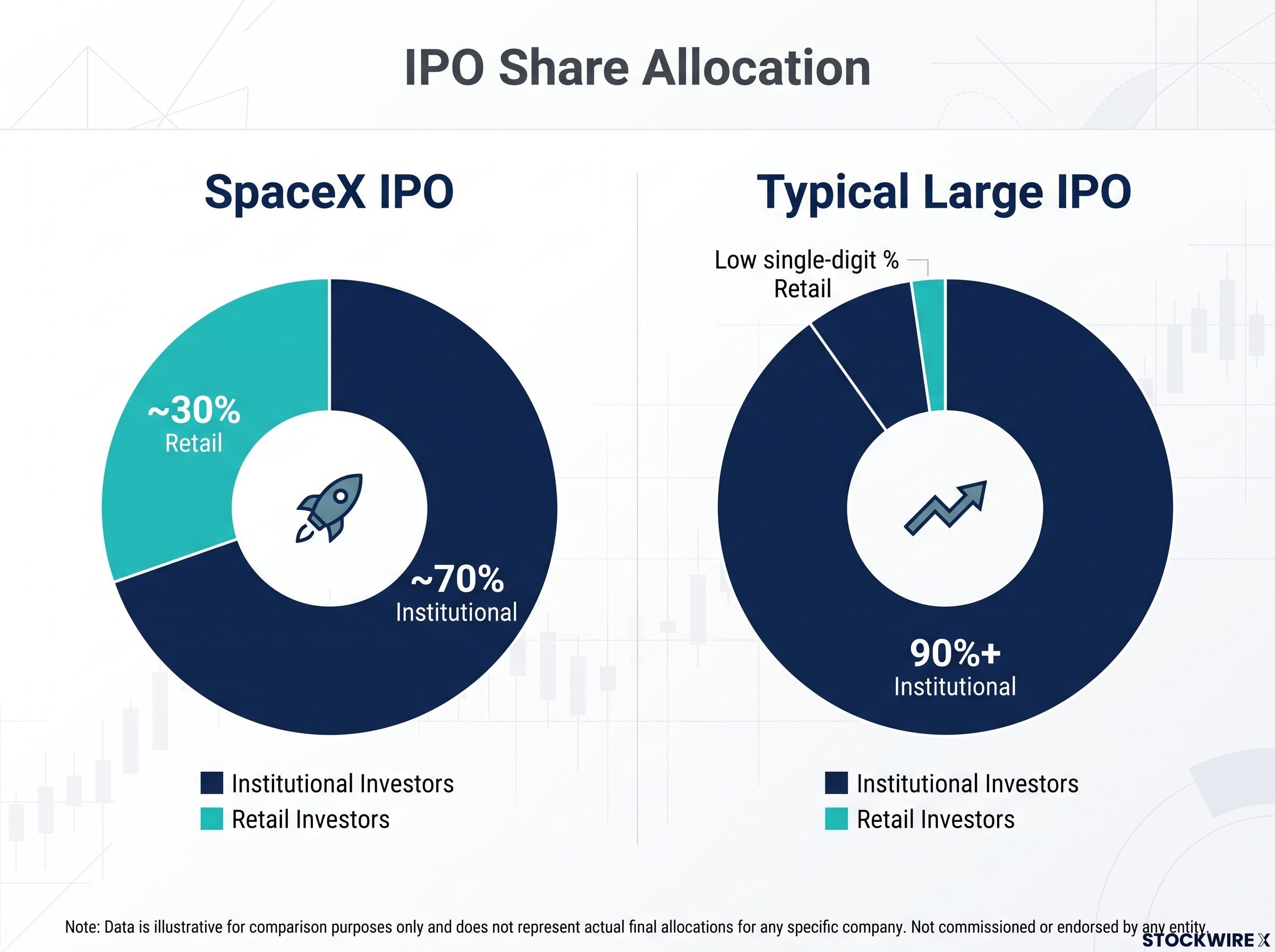

If you tried to buy SpaceX shares at the IPO price and could not, that is not a personal failure. It is how IPO allocation works by design.

In most large IPOs, the vast majority of shares are allocated to institutional investors via the underwriting banks’ client lists. Retail investors typically receive low single-digit percentages of the total offering. Investment banks distribute pre-IPO allocations to their largest clients and wealthiest individuals first; by the time the share price firms through that process, retail and everyday investors face very long odds of accessing shares at the listing price.

IPO allocation mechanics consistently disadvantage retail participants because investment banks distribute pre-listing shares to their largest institutional clients first, with everyday investors receiving whatever remains after that institutional priority queue has been satisfied.

SpaceX was a deliberate outlier. Approximately 30% of available shares were reserved for retail and smaller investors, far higher than the single-digit slices common in comparable deals. Institutions still received the majority, roughly 70%, but the retail allocation was materially larger than standard practice.

Reuters described SpaceX’s retail allocation as a “stark contrast” to normal large IPO practice, reporting that Elon Musk aimed to reserve up to 30% of shares for smaller investors.

| Feature | Typical large IPO | SpaceX IPO |

|---|---|---|

| Retail allocation | Low single-digit % | Approximately 30% |

| Institutional allocation | 90%+ of offering | Approximately 70% |

| Structural rationale | Banks prioritise largest clients | Deliberate effort to broaden individual access |

For Australian retail investors specifically, any path to IPO-price shares ran through global brokerage platforms or specific IPO programmes. In practice, quantities available to individuals were small relative to demand, and oversubscription was likely. The relevant question for you is not whether you missed the $135 price but whether the secondary market price available through your broker accurately reflects the growth assumptions SpaceX is selling.

ASIC MoneySmart guidance on international investments specifically cautions that foreign-listed shares not offered by licensed Australian providers may fall outside ASIC’s regulatory protection, a consideration that applies directly when accessing SPCX through international brokerage platforms rather than ASX-connected services.

IPOs explained: what they are and why companies pursue them

An IPO is the mechanism through which a private company first sells shares to the general public and lists on a stock exchange. It is primarily a capital-raising tool. The company issues new shares, sells them to investors, and uses the proceeds to fund operations, expansion, or debt repayment at a scale that private funding sources cannot efficiently provide.

There are three primary reasons companies pursue IPOs:

- Capital raise at scale: Public markets give access to a far larger pool of capital than private venture or equity rounds can provide

- Liquidity event for employees and early investors: People who received stock as compensation or made early-stage investments can eventually sell their holdings for cash through public trading

- Public profile and currency for acquisitions: A listed stock can be used as currency for mergers and acquisitions, and public listing raises the company’s commercial profile

The liquidity motivation is where IPO wealth-creation stories come from. Employees who accumulated stock over years at prices well below the listing price can, once trading begins and lockup restrictions lift, convert paper gains into real money. For SpaceX, that liquidity event is deferred to post-lockup trading, not the IPO itself, because the all-primary structure meant no insiders sold on listing day.

Understanding that an IPO is primarily a capital-raising tool helps you evaluate every listing you encounter. The first question is always whose capital need is being served and whether the price offered to public buyers reflects a fair exchange for the risk being transferred to them.

What happens before the IPO: the private funding stages

Before listing, companies typically raise capital through a series of private funding rounds, from early venture capital backing through to late-stage private equity. SpaceX raised capital privately across many years as it developed its launch and satellite businesses. When the scale of its ambitions, spanning rockets, global satellite connectivity, and orbital computing, outgrew what private markets could efficiently fund, public markets became the next step. The Nasdaq listing under ticker SPCX on 12 June 2026 was the end point of that private-to-public progression.

The next major ASX story will hit our subscribers first

The lockup clock and what it means for shareholders in late 2026

A lockup period is a contractual restriction that bars pre-IPO shareholders from selling their holdings for a set window after the company lists. The mechanism exists to shield the newly public share price from an immediate wave of selling by employees, founders, and early investors, all of whom typically hold shares at a cost far below the IPO price.

The standard lockup duration for U.S. IPOs is 180 days from listing. Here is how that timeline maps to SpaceX:

- 11 June 2026: IPO pricing at $135 per share

- 12 June 2026: Shares begin trading on the Nasdaq

- June-December 2026: Standard 180-day lockup period runs

- Approximately December 2026: Lockup restrictions expire for most pre-IPO holders under standard terms

- Post-expiry: Pre-IPO shareholders gain the legal ability to sell on the open market

A large cohort of employees and early investors hold shares at cost bases well below the $135 listing price, let alone the first-day close near $161. When the lockup lifts, that entire population gains the legal ability to sell. Whether they actually do, and at what volume and price, determines the real impact on the stock.

Important caveat: Exact lockup terms are defined in SpaceX’s prospectus and SEC filings. Extended restrictions may apply to major holders including Elon Musk. Investors should consult the latest filings to confirm expiry dates before making decisions based on the lockup timeline.

For investors holding SPCX or considering secondary market entry through late 2026, our dedicated guide to the SpaceX lockup schedule details the roughly 12 distinct unlock events, the performance trigger that could release shares before August 2026, and why the standard 180-day endpoint is a cleanup event rather than the primary supply moment.

The lockup expiry does not predict a price decline. What it does is mark the first moment when the full population of pre-IPO holders can make independent decisions about realising gains. That means volatility risk rises regardless of direction. If you hold SPCX through late 2026 or are considering entry in the secondary market, understanding this timeline is the difference between being surprised by a volatility period and being positioned for it.

What the SpaceX case study actually teaches retail investors

What makes the SpaceX IPO genuinely instructive is not the company’s profile or scale, but the way it lays bare, more visibly than almost any other listing, each structural layer that recurs in every IPO you will ever evaluate.

Four structural filters emerged across the preceding sections. These are the questions you should ask about any major listing:

Post-listing performance factors, including investor base composition, the conservatism of initial guidance, and the structural conditions set during bookbuilding, are largely locked in before the first trade executes, which means the quality of the business and the quality of the deal are two separate evaluations you need to run independently.

- Offering structure: Is the company raising fresh capital (primary), or are insiders cashing out (secondary), or both? The answer tells you who benefits most from the listing.

- Allocation split: What percentage goes to institutions versus retail? This tells you how much of the pricing was negotiated between large players before you could participate.

- Valuation evidence base: Is the price built on established revenue and public trading history, or on projected growth across unproven business lines? This shapes how much assumption you are buying.

- Lockup timeline: When can pre-IPO holders sell, and how large is the eligible supply relative to daily trading volume? This tells you where the next volatility window sits.

| Structural element | What it is | SpaceX example | What to ask next time |

|---|---|---|---|

| Offering type | Primary vs. secondary vs. mixed | All-primary; $75B to SpaceX, zero to insiders | Who receives the proceeds? |

| Retail allocation | % of shares reserved for individual investors | ~30%, far above typical single-digit % | How much was negotiated before I could bid? |

| Valuation basis | Evidence supporting the implied price | Three pillars with varying evidence depth | Am I buying proven revenue or projected growth? |

| Lockup period | When pre-IPO holders can first sell | ~180 days; approximately December 2026 | When does insider supply enter the market? |

For Australian investors specifically, by the time SPCX is accessible through ASX-connected brokers or international platforms, the price already reflects negotiations completed between SpaceX, its banks, and large global funds at the $135 level and above. That does not mean the opportunity has passed. It means the question you should be asking is not “did I miss the IPO?” but “do the growth assumptions priced into today’s market price justify the risk I am taking on?”

The figures and events covered here reflect reporting through mid-2026. Readers should consult current SEC filings and market data before making any investment decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.