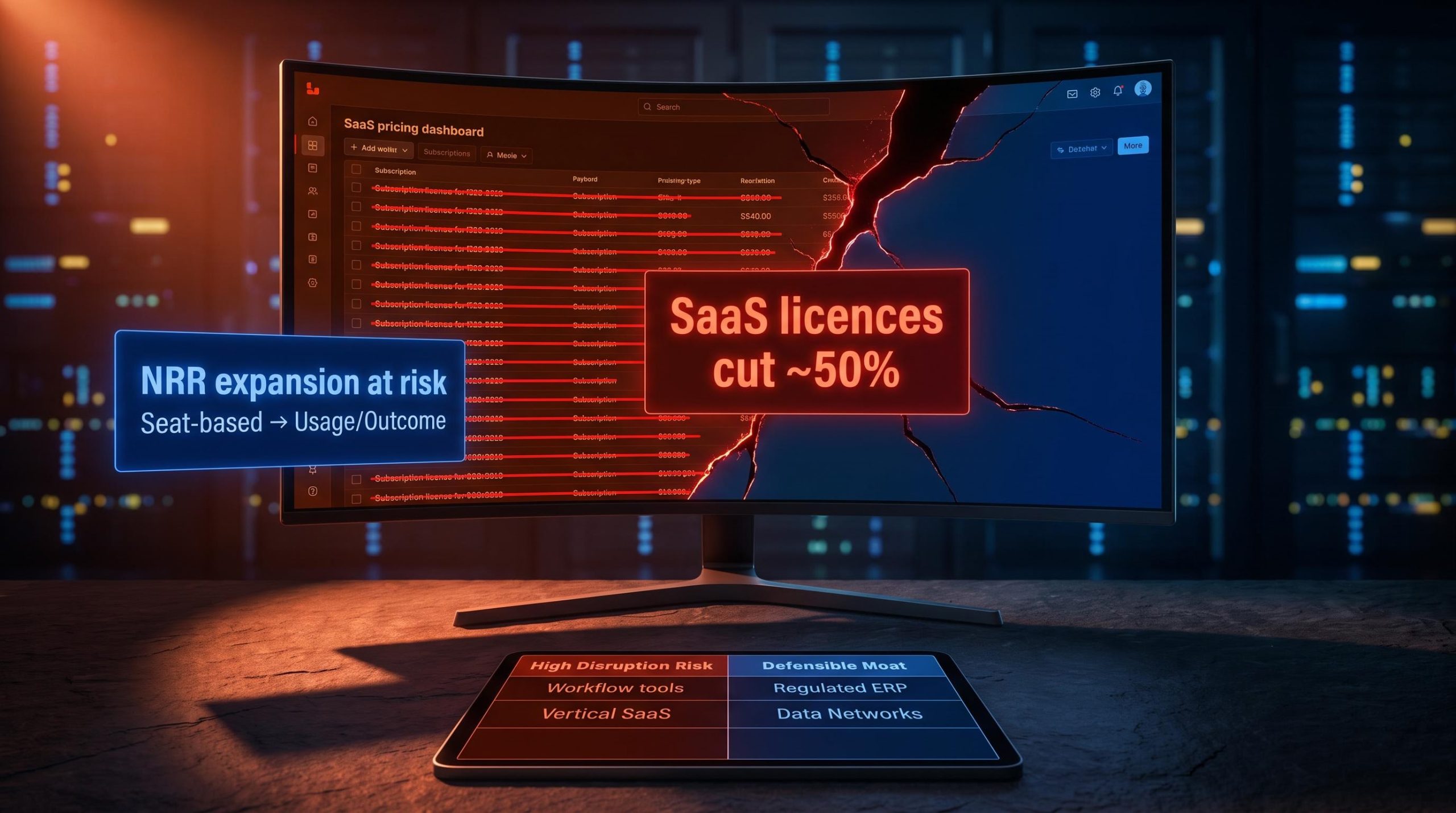

Publicis Sapient, one of the world’s largest digital transformation consultancies, cut its traditional SaaS licences by approximately 50% last year. That included displacing Adobe. The trigger was not a cost-reduction programme. It was a deliberate substitution: AI tools doing the work that commercial software subscriptions once handled, at a fraction of the cost and a multiple of the speed.

This is not a trend piece about what might happen. It is evidence that a decision process investors assumed was still theoretical, the enterprise choice to build internal tools instead of buying SaaS subscriptions, is already playing out in named organisations with documented results.

For more than a decade, the SaaS business model earned premium valuations on three pillars: predictable subscription revenue, high switching costs, and net revenue retention (NRR) that expanded organically as headcount grew. The assumption underneath all three was that building custom software was too expensive and too slow to be a rational alternative. AI-assisted development platforms have broken that assumption. Here is a framework for separating the SaaS businesses that will reprice from those that will not.

The “build instead of buy” calculation has already flipped for some enterprises

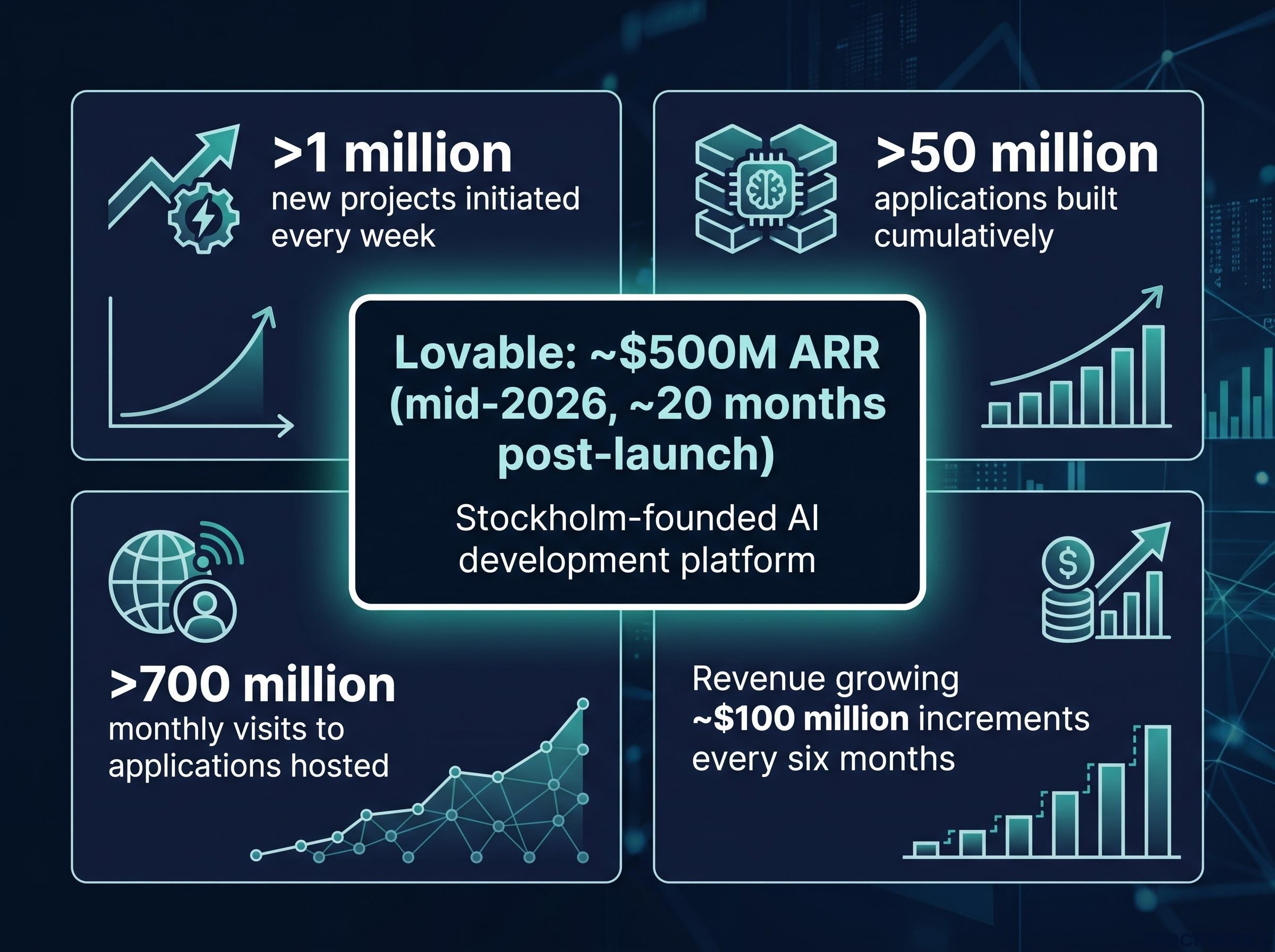

The numbers are arriving faster than most sector analysts expected. Lovable, a Stockholm-founded AI development platform, reached approximately $500 million in annualised revenue as of mid-2026, roughly 20 months after launch. The platform’s scale metrics tell you something about the velocity of adoption:

- Over 1 million new projects initiated every week

- More than 50 million applications built cumulatively

- Over 700 million monthly visits to applications hosted on the platform

- Revenue growing in roughly $100 million increments every six months

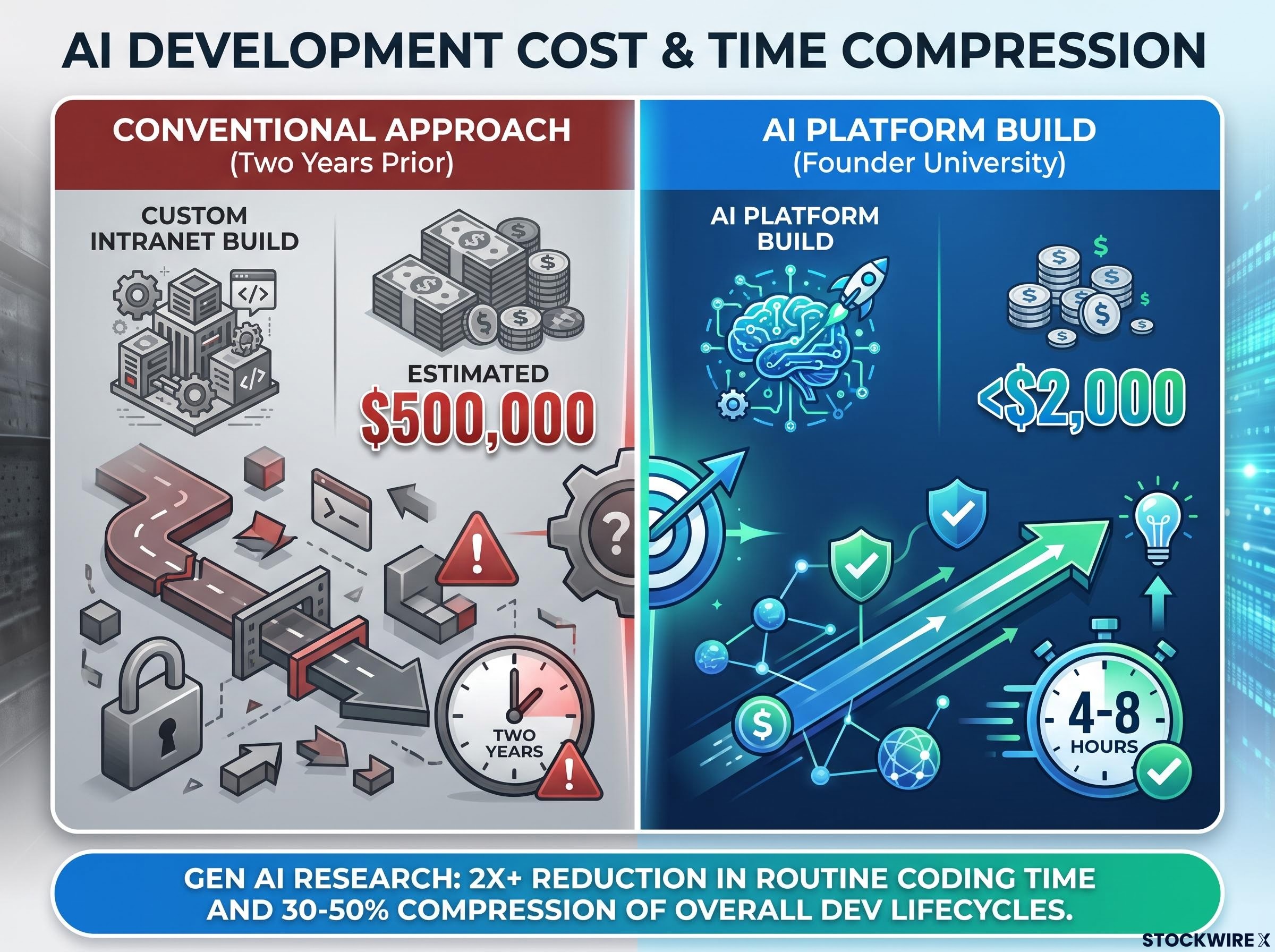

The enterprise use cases are specific. Nursa, a US-based company, replaced more than 10 existing software tools with custom applications built on the platform, saving over $1 million annually. Founder University completed a full custom intranet build in roughly 4-8 hours, with total costs coming in below $2,000, a project that would have required an estimated $500,000 under conventional development approaches just two years prior.

These are anecdotal cases, not statistical proof. But they are directionally consistent with independent findings: generative AI research shows a 2x or greater reduction in routine coding time and a 30-50% compression of overall development lifecycles in early deployments.

Enterprise AI build programmes at named organisations are producing documented licence reductions, with Starbucks targeting $10 million in direct software licensing savings by replacing Microsoft, IBM, and Oracle applications with internally developed AI tools, a case that extends the Publicis Sapient pattern into a very different industry and scale context.

Publicis Sapient executives described their AI agents as “10x faster, 100x smarter” than junior staff, making many user seats economically redundant.

The pattern is concentrated in workflow-centric, moderate-complexity tools, not mission-critical regulated systems. But the cost curve shift is generalised enough to change the rational build-versus-buy threshold for any organisation with moderate internal technical capacity.

When big ASX news breaks, our subscribers know first

Why the SaaS model was always partly a labour arbitrage, and why that matters now

Most investors think of a SaaS subscription as paying for software. It is more accurate to think of it as paying for a bundle of four components: functionality, engineering labour, maintenance, and security and infrastructure. Subscription pricing presents this as access to features, but buyers were always paying for all four, and engineering labour was the most expensive one to replicate independently.

That is precisely the component AI platforms attack most directly. Before 2024, building a custom business application meant hiring developers, managing sprints, and spending months on deployment. The engineering labour cost made “build” irrational for most organisations, which is why “buy” won so consistently. AI development platforms have structurally deflated that cost, and three specific breaks explain why this is not a feature war but a repricing of what custom software costs to produce.

- Collapse of barriers to entry. AI coding agents have made building enterprise-grade software dramatically cheaper and faster, lowering both capital and talent requirements. According to Fortune, this increases competition and alternative options, pressuring the margins SaaS vendors have long enjoyed.

- Commoditisation of features and UX. Generative AI can rapidly replicate premium features that took SaaS vendors years and millions to develop. HFS Research argues that this lets firms assemble composable applications from functional modules faster and cheaper than buying monolithic apps. Natural language interfaces reduce the importance of sophisticated UX as a moat.

- AI agents abstracting the application layer entirely.

When AI agents become the interface, the application disappears

This is the most forward-looking of the three breaks. IDC describes AI agents as a new interface tier that sits across multiple SaaS products and systems, executing workflows via conversational interaction. The user interacts with the agent, not with the individual application. The agent orchestrates actions across multiple underlying systems, so the individual SaaS product becomes invisible, undifferentiated infrastructure. The stickiness that UI familiarity and workflow habit once provided erodes when the user never sees the app.

The result: the part of the SaaS bundle that was “renting engineering labour and packaged workflows” is being reproduced and surpassed by AI platforms. The disruption is structural, not competitive.

Which SaaS segments face genuine displacement risk, and which do not

The temptation is binary framing: SaaS is dying, or SaaS is fine. Neither is accurate. Disruption risk varies by segment, and the dividing line is not company size or industry. It is the nature of the moat.

Most exposed: where the build-versus-buy calculation tips first

Workflow and productivity tools, such as intranets, task trackers, and lightweight collaboration platforms, are the most immediately vulnerable. These are high-specificity, low-complexity tools that organisations bought because building bespoke solutions was previously too expensive. That cost barrier has collapsed.

Vertical SaaS vendors without strong data moats face a particular paradox. The industry-specific workflow argument that justified their existence now makes them easier to replicate. IDC and HSBC Innovation Banking both note that AI agents move business logic away from vertical, database-oriented SaaS solutions. Vendors that mainly encode workflow logic, rather than aggregating scarce cross-organisational data, are exposed.

Mid-market collaboration and operations software sits in a similar position: expensive enough to motivate build-versus-buy reconsideration, but lacking the deep integration moats that make replacement prohibitively risky.

More defensible: what genuine moats look like in this environment

Regulated core systems, including ERP and financial platforms with deep audit trails, retain defensibility because switching costs are driven by compliance certifications and risk management, not just engineering economics. No internal AI build replicates a decade of regulatory approval history.

Systems of record defensibility rests on a specific mechanism that the displacement thesis frequently underweights: AI agents executing multi-step enterprise tasks depend on incumbent SaaS platforms for authoritative data, meaning deeply embedded platforms may function as infrastructure for AI deployment rather than as targets for replacement.

Data network-effect platforms, such as benchmarking services, industry analytics, and ad networks, are difficult to supplant because organisations cannot replicate the shared data pool with an internal tool.

Communication and collaboration networks with external participants retain value because the moat is the network itself. No internally built application recreates who else is using the product.

| Segment | Disruption risk | Primary vulnerability | Defensibility factor |

|---|---|---|---|

| Workflow and productivity tools | High | Low complexity, easily replicated by AI builds | Minimal; UX familiarity only |

| Vertical SaaS (no data moat) | High | Workflow logic replicable; specificity now a liability | Low unless proprietary data aggregated |

| Mid-market collaboration and operations | Moderate-High | Cost motivates replacement; lacks integration depth | Limited; depends on integration lock-in |

| Regulated core systems (ERP, financial) | Low | Compliance switching costs dominate | Strong; regulatory certification depth |

| Data network-effect platforms | Low | Value is the aggregated dataset, not the interface | Strong; data pool cannot be internally replicated |

| Communication networks (external participants) | Low | Moat is the network, not the software | Strong; external network effects |

For an investor holding a diversified software portfolio, the segment map tells you that the revenue line matters less than the moat type. A high-growth vertical SaaS with no data asset may be structurally more exposed than a slower-growing regulated infrastructure vendor.

What the displacement thesis means for SaaS valuation multiples

The operational disruption story told in the previous sections has direct financial mechanics. Start with seat-based expansion, historically the engine of SaaS revenue growth. When AI agents can do the work of several human users, paying per seat becomes economically irrational. Aurelian Research and L.E.K. Consulting both tie this directly to decelerating NRR, because the historic path of “add users as the business grows” no longer reliably translates into expanding revenue for the vendor.

IDC forecasts that by 2028, approximately 70% of SaaS vendors will have refactored pricing away from pure seat-based models toward consumption, outcome, or capability metrics.

That transition implies margin volatility and lower predictability during the shift period, which is a risk factor even for vendors successfully adapting. Christian Owens, CEO of Paddle, frames this as a structural move from per-user to usage and value metrics that AI is accelerating.

The switching cost assumptions embedded in current valuation models for exposed segments need particular scrutiny. If firms can build and host alternatives in weeks rather than committing to multi-year migration projects, customer lifetime value models based on backward-looking churn data are likely overstating retention durability. Three valuation assumption categories now require segment-specific stress testing:

The market repricing of software stocks in response to individual enterprise build announcements illustrates how acutely investors are watching for displacement signals: IBM, Salesforce, and ServiceNow each fell 3-4% in premarket trading on a single report, even though the underlying Starbucks programme had not yet moved beyond internal testing.

- NRR expansion logic: Does seat growth still correlate with customer growth when AI agents reduce headcount requirements?

- Switching cost durability: Are switching costs rooted in regulation and data, or in UX familiarity and historical inertia that AI builds can now overcome rapidly?

- Total addressable market (TAM) estimates: Do TAM models assume every workflow becomes a separate SaaS product, when AI agents may consolidate many workflows into a single orchestrated layer?

An investor using backward-looking churn data to assess customer lifetime value may be materially overestimating retention durability for exposed segments. Churn models built before AI-assisted development was economically viable do not account for switching costs that can now be overcome in weeks rather than years.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The next major ASX story will hit our subscribers first

A diagnostic framework for software sector portfolio analysis

The analysis above gives you the structural picture. These six questions convert it into something you can apply to individual holdings in your next analyst call or due diligence session. They move sequentially from exposure assessment through moat diagnosis to behavioural signal identification.

- How much of this company’s revenue comes from workflows that AI-assisted internal development can realistically replace? Break revenue by use-case type, not just by industry or customer size. Simple workflow tools are exposed; regulated core systems are not.

- Are the switching costs rooted in regulation, data, and integration, or mostly in UX familiarity and historical inertia? High historical NRR may reflect inertia rather than durable moats in a world where AI rebuilds applications quickly.

- Is the company proactively shifting away from pure seat-based pricing toward usage or outcome-based models? If not, how exposed is its expansion logic to AI-driven digital labour that reduces human seat counts?

- Is the product ready to be orchestrated by AI agents? IDC expects AI agents to become the primary interface for many workflows. Vendors without robust APIs (application programming interfaces, the connectors that let different software systems communicate), strong security, and data governance risk becoming invisible, undifferentiated infrastructure, or obsolete entirely.

- Are acquisition costs rising and conversion rates falling, even if current churn looks stable? Rising customer acquisition cost and falling conversion are often early indicators that build-versus-buy alternatives are affecting new deals before they appear in retention metrics. These signals frequently precede visible churn by several quarters.

- What proprietary datasets or network effects would be impossible for a customer to replicate with an internal AI-built tool? This is the single most important question for long-term defensibility.

The goal is not to short every SaaS company. It is to differentiate holdings by structural defensibility and allocate accordingly. Treat the enterprise cases discussed in this piece as early pattern signals. Anchor decisions in observable behaviour: licence reduction, pricing changes, slowing seat growth, rising acquisition costs.

What survives the transition, and where the durable software value actually sits

The SaaS model is not disappearing. It is being stratified. The application layer is commoditising, but data assets, integration infrastructure, and network effects are becoming more valuable, not less. HSBC Innovation Banking frames the viable strategic direction as “infrastructure, not interface,” positioning around data and workflow orchestration with strong APIs and compliance guarantees rather than trying to defend a front-end application that AI agents will bypass.

The software businesses most likely to compound value through the transition share specific characteristics:

- Proprietary cross-organisational data that customers cannot replicate internally

- API-first architecture ready for AI agent orchestration

- Regulatory moats with genuine compliance certification depth

- Pricing models already adapted to usage or outcome metrics

Incumbent vendors have strategic options: infrastructure repositioning, data monetisation, AI-native product rebuilds, and pricing model migration. Each carries execution risk, and outcomes are far from certain. HFS Research describes a market emerging for modular functional components, not just monolithic apps, which creates openings for vendors willing to unbundle. IDC’s agent-as-interface thesis suggests that API readiness and data governance are becoming the new interface requirements.

The investment question is not whether to hold software exposure. It is whether your holdings are positioned on the commoditising application layer or on the data, integration, and network layer that is gaining value as the application layer deflates. Multiple analyst perspectives converge on a consistent framing: SaaS as we know it is being disrupted by evolution, not decline. The returns will accrue to investors who can tell the difference.

For investors whose software portfolio analysis leads them to consider reweighting toward AI infrastructure beneficiaries, our full explainer on AI investment frameworks covers the three-tier structure across hardware, cloud platforms, and pure-play software names that J.P. Morgan, BlackRock, and Goldman Sachs independently converge on for positioning AI exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.